Future of Credit Cards, Plastics

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

News Blaze of the Week August 16, 2020 Issue 09

News Blaze of the Week August 16, 2020 Issue 09 Page | 1 Research and Development Unit Editorial Panel Quotation Corner Fahmida Chowdhury EVP & Principal, DBTI In charge R&DU “You only live once, but if you do it Farzana Afroz PO, R&DU right, once is enough.” — Mae West “Money and success don’t change people; they merely amplify what is already there.” — Will Smith Contact us: “Life is not a problem to be solved, but a [email protected] reality to be experienced.” – Soren Kierkegaard Page | 2 Govt Initiatives Banks and Financial Institutions Govt to form 'Delta Fund' to finance climate projects 05 18 banks added to bKash Add Money service 08 Agreement on first bio-tech plant signed 05 Southeast Bank Limited shifted its Pragati Sarani Branch at the Bank's own premises at Pearl 09 Pubali Bank donates bus to BSMMU 09 Karmasangsthan Bank launches loan product 09 Banks seek Tk 18 million as interest subsidy 10 Abdul Hai Sarker elected chairman of Dhaka Bank 10 National Milestone Shahjalal Islami Bank approves 10pc dividend 11 Per capita income rises to $2,064 06 IPDC offers exclusive auto loan 11 College fees being paid through 'Nagad' 12 Prime Bank, Ajkerdeal partner for MSME credit 12 Central Bank Regulation BB relaxes loan restructuring policy for NBFIs 07 BB asks banks to tap NRB deposits 07 Page | 3 Corporate Market Update Stock Market Update Walton's IPO subscription begins today 16 Stocks rebound after five months 13 Ten cos account for 27pc DSE transactions 13 Square Pharma tops DSE turnover chart 14 DSEX exceeds 4,600-mark as -

Unclaimed Deposit Statement for Bank's Website-As on 31.12.2020

SL Name of Branch Present Address Permanent Address Account Type Name of Account/ Beneficiary Account/Instrument No. Father's Name Amount BB Cheque Amount Date of Transfer Remarks No. 1 SKB Branch Law Chamber, Amin Court, 5th Floor, 62-63 Motijheel C/A, Dhaka. NA Current Account Graham John Walker 0003-0210001547 NA 130,569.00 130,569.00 18-Aug-14 2 SKB Branch NA NA NA Grafic System Pvt. Ltd. PAA00014522 NA 775.00 3 SKB Branch NA NA NA Elesta Security Services Ltd. PAA00015444 NA 4,807.00 5,582.00 22-Nov-15 4 SKB Branch 369,New North Goran Khilgaon,Dhaka. Vill-Maziara, PO-Jibongonj Bazar, Nabinagar, Brahman Baria Savings Account Farida Iqbal 0003-0310010964 Khondokar Iqbal Hossain 1,212.00 5 SKB Branch Dosalaha Villa, Sec#6,Block#D,Road#9, House# 11,Mirpur ,Dhaka. Vill-Balurchar, PO-Baksha Nagar,PS-Nababgonj,Dist-Dhaka. Savings Account Md. Shah Alam 0003-0310009190 Late Abdur Razzak 975.00 6 SKB Branch H#26(2nd floor)Road# 111,Block-F,Banani,Dhaka. Vill- Chota Khatmari,PO-Joymonirhat, PS-Bhurungamari,Dist-Kurigram. Savings Account S.M. Babul Akhter 0003-0310014077 Md. Amjad Hossain 782.00 7 SKB Branch 135/1,1st Floor Malibag,Dhaka. Vill-Bhairabdi,PO-Sultanshady,PS-Araihazar,Dist-Narayangonj. Savings Account Mohammad Mogibur Rahman 0003-0310012622 Md. Abdur Rashid 416.00 14,951.00 6-Jun-16 8 SKB Branch A-1/16,Sonali Bank Colony, Motijheel,Dhaka. 12/2,Nabin Chanra Goshwari Road, Shampur, Dhaka. Savings Account Salina Akter Banu 0003-0310012668 Md. Rahmat Ali 966.00 9 SKB Branch Cosmos Center 69/1,New Circular Road,Malibage,Dhaka. -

ANNUAL REPORT 2016 2 Table of Contents

Annual Report Year ended 31st December 2016 2016 leading financial institution of the Country, IIDFC was promoted by 10 banks, 3 insurance companies, the ICB and Mr. Md. A Matiul Islam, the first finance secretary of the Government of Bangladesh. With a Board of Directors comprising of top level bankers and former senior civil servants, the main emphasis of IIDFC is promoting and financing investments in largeindustrial and infrastructure projects. IIDFC’s debut in the capital market was through flotation of convertible zero coupon bond, a new and innovative financial instrument. Its presence in the capital market is through its two subsidiaries—one for merchant banking operation and the other for brokerage services. jv‡Lv kwn‡`i i‡³ †fRv Avgv‡`i GB evsjv‡`k ï×vPv‡i F× n‡q `ybx©wZ‡K Kie †kl| -mvMi Avkivd IIDFC LIMITED ANNUAL REPORT 2016 2 Table of Contents IIDFC Commitments 04 S Notice of the 16th Annual General Meeting 06 T Milestone Events 07 Corporate Information 10 Our Bankers 11 Shareholding Structure 12 EN Board of Directors 14 Brief Profile of the Directors 15 T Executive Committee of the Board 22 Audit Committee of the Board 23 Committees of IIDFC 24 Senior Management Team (SMT) 25 IIDFC Staff Members 27 Products & Services 36 Carbon Finance : Caring Nature and Environment 38 Ratings of IIDFC 40 Financial Highlights 41 Sector-wise Exposure 44 Sources of Fund 45 Directors’ Report 46 Foreword 52 Auditors’ Report to the Shareholders of IIDFC Limited 54 Auditors’ Report to the Shareholders of IIDFC Capital Limited 116 Auditors’ Report to the Shareholders of IIDFC Securities Limited 135 Photographs from IIDFC’s Album 158 Notes 173 Proxy Form 175 TABLE OF CON OF TABLE IIDFC LIMITED ANNUAL REPORT 2016 3 IIDFC Commitments Our Commitments to the Nation To contribute to the Country’s economic growth in all possible ways. -

Depository & Non-Depository Financial Institutions of Bangladesh

Depository institution A depository institution is a firm that accepts deposits from households and firms and uses the deposits to make loans to other households and firms. The deposits of three types of depository institution make up the nation’s money. Some depository institution of Bangladesh are Commercial banks Thrift institutions Money market mutual funds Commercial banks This is a financial institution providing services for businesses, organizations and individuals. Commercial bank is defined as a bank whose main business is deposit- taking and making loans. State-owned Commercial Banks Sonali Bank Agrani Bank Rupali Bank Janata Bank Private Commercial Banks BRAC Bank Limited Dutch Bangla Bank Limited Eastern Bank Limited United Commercial Bank Limited Mutual Trust Bank Limited Dhaka Bank Limited Islami Bank Bangladesh Ltd Uttara Bank Limited Pubali Bank Limited IFIC Bank Limited National Bank Limited The City Bank Limited NCC Bank Limited Mercantile Bank Limited Southeast Bank Limited Prime Bank Limited Social Islami Bank Limited Standard Bank Limited Al-Arafah Islami Bank Limited One Bank Limited 11 Sumon Bank Limited Exim Bank Limited First Security Islami Bank Limited Bank Asia Limited The Premier Bank Limited Bangladesh Commerce Bank Limited Trust Bank Limited Jamuna Bank Limited Shahjalal Islami Bank Limited ICB Islamic Bank AB Bank Jubilee Bank Limited Specialized Development Banks BangladeshKrishi Bank Progoti Bank RajshahiKrishi Unnayan Bank BangladeshDevelopment Bank Ltd Bangladesh Somobay Bank Limited Grameen Bank BASICBank Limited Ansar VDP Unnyan Bank The Dhaka Mercantile Co-operative Bank Limited(DMCBL) Karmasangsthan Bank Foreign Commercial Banks Citibank HSBC Standard Chartered Bank Commercial Bank of Ceylon State Bank of India Woori Bank Bank Alfalah National Bank of Pakistan ICICI Bank Habib Bank Limited Thrift institutions The thrift institutions are Savings and loan associations Savings banks Credit unions. -

ANNUAL REPORT 2018 Bangladesh Bank Training Academy

ANNUAL REPORT 2018 Bangladesh Bank Training Academy Page 1 of 55 Published by Phone: 880-2-8033650 Fax: 880-2-8032110 E-mail: [email protected] Website: www.bb.org.bd Page 2 of 55 FOREWORD FROM training, research and development THE GOVERNOR programs to keep pace with this new era. BBTA is rightly setting its foot to move forward in this fast changing arena. I am extremely happy to know that the team of BBTA faculty has completed a remarkable job in developing this year’s ATP along with its course curriculum with an advanced outlook. The commitment of BBTA in pursuing its objectives is inspirational. It is FazleKabir Governor praiseworthy that BBTA is offering training Bangladesh Bank programs online for seeking appropriate nominations of participants from the next It is indeeda great pleasure to learn that calendar year. Bangladesh Bank Training Academy is publishing its Annual Report for 2018 in It is encouraging to note that BBTA is addition to the regular publication of providing foundation training to newly Academic Calendar. This report encapsulates recruited Assistant Directors and Officers of the overall functions of the academy during General and Special sides of Bangladesh Bank the calendar year 2018. It envisages an and In-service training to the existing integrated view of the academy and the way manpower on a regular basis. The in-house the activities are administered all the year and guest speakers’ resource pool of BBTA is round. As Bangladesh is moving towards an greatly contributing to developing human upper middle income country and looks set resources in the relevant fields. -

Md. Abdus Salam

Md. Abdus Salam CEO and MD, Janata Bank Limited Mr. Md. Abdus Salam joined as the CEO & Managing Director of Janata Bank Limited on 28 October, 2014. Before joining here, he served as the Managing Director of Bangladesh Krishi Bank. He was born on 1st December, 1956 in a respectable family of late Ahmed Ali and Mrs. Rabeya Ahmed. Mr. Salam studied at Dhaka College, Dhaka for his higher secondary education, followed by his graduate and postgraduate studies at the Department of Accounting of the University of Dhaka where he obtained his B.Com. (Hons.) and M. Com. in Accounting. He is a Fellow of Chartered Accountant (FCA) from the Institute of Chartered Accountants of Bangladesh (ICAB). Mr. MD. Abdus Salam, FCA started his banking career in 1983 as Principal Officer of Bangladesh Krishi Bank. Before adorned the position of CEO & MD of Janata Bank Limited, he served as Deputy Managing Director in Agrani Bank Limited & Janata Bank Limited and as General Manager in Sonali Bank Limited & Karmasangsthan Bank. On his initiative Bangladesh Krishi Bank, for the first time, acted as ‘Banker to the Issue’ and also introduced Mobile Banking & On-line Banking in the same Bank. His notable and luminous works were- preparation of Asset Liability Management Manual, Risk Management Manual and implementation of automated foreign remittance distribution system in Sonali Bank Limited. He also contributed his effort to introducing On-line Banking in Agrani Bank Limited. He developed an Accounting System for Bangladesh Computer Council in 1990 while he was on deputation. He attended various workshops, seminars and received different training in home and abroad. -

Details of the Related Party Transactions Have Been Disclosed in Annexure-F

INTERNATIONAL FINANCE INVESTMENT AND COMMERCE BANK LIMITED Consolidated Balance Sheet as at 31 December 2018 Amount in BDT Particulars Note 31 December 2018 31 December 2017 PROPERTY AND ASSETS Cash 16,020,741,583 15,487,553,511 Cash in hand (including foreign currency) 3.a 2,899,030,289 2,251,768,572 Balance with Bangladesh Bank and its agent bank(s) (including foreign currency) 3.b 13,121,711,294 13,235,784,939 Balance with other banks and financial institutions 4.a 8,118,980,917 10,623,519,846 In Bangladesh 4.a(i) 6,823,590,588 8,068,534,922 Outside Bangladesh 4.a(ii) 1,295,390,329 2,554,984,924 Money at call and on short notice 5 3,970,000,000 3,830,000,000 Investments 32,664,400,101 29,290,877,363 Government securities 6.a 27,258,506,647 23,943,582,942 Other investments 6.b 5,405,893,454 5,347,294,421 Loans and advances 210,932,291,735 183,296,111,106 Loans, cash credit, overdrafts etc. 7.a 198,670,768,028 171,593,194,706 Bills purchased and discounted 8.a 12,261,523,707 11,702,916,400 Fixed assets including premises, furniture and fixtures 9.a 5,445,835,394 3,539,338,093 Other assets 10.a 9,003,060,522 10,277,591,453 Non-banking assets 11 373,474,800 373,474,800 Total assets 286,528,785,052 256,718,466,172 LIABILITIES AND CAPITAL Liabilities Borrowing from other banks, financial institutions and agents 12.a 9,969,432,278 8,473,580,748 Subordinated debt 13 3,500,000,000 3,500,000,000 Deposits and other accounts 14.a 226,228,549,042 200,148,679,835 Current deposit and other accounts 40,849,197,782 30,611,131,194 Bills payable 2,066,079,056 -

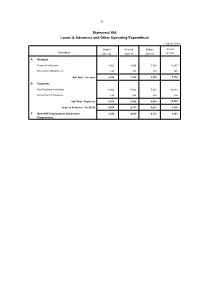

Statement VIA Loans & Advances and Other Operating Expenditure

40 Statement VIA Loans & Advances and Other Operating Expenditure (Taka in Crore) Budget Revised Budget Actual Description 2021-22 2020-21 2020-21 2019-20 A. Receipts Financial Institution 3,861 3,682 3,764 9,187 Government Employees 163 101 110 167 Sub Total - Receipts : 4,024 3,783 3,874 9,354 B. Payments Non-Financial Institutions 8,000 7,962 7,501 10,333 Government Employees 530 538 583 226 Sub Total - Payments : 8,530 8,500 8,084 10,559 Loans & Advances - Net (B-A) : 4,506 4,717 4,210 1,205 C. Non-ADP Employment Generation 5,990 4,610 4,722 3,343 Programmes : 41 List of Guarantee (Valid beyond 30 June, 2021) (Amount in Crore) Issue Date Sl. Purpose of Guarantee/Counter In Favour of (Extension Outstanding No. Date) Agricultural Credit 1 Agricultural Credit Programme of Bangladesh Bank 29/06/2004 1,893.82 Bangladesh Krishi Bank (cumulative arrear (29/08/2009) for the period from 31/12/2003 to FY 2008-09) 2 Agricultural Credit Programme of Bangladesh Bank 02/09/2019 1,000.00 Bangladesh Krishi Bank (2019-20) (15/09/2020) 3 Agricultural Credit Programme of Bangladesh Bank 09/07/2020 1,000.00 Bangladesh Krishi Bank (2008-09) 4 Agricultural Credit Programme of Rajshahi Bangladesh Bank 29/06/2004 573.50 Krishi Unnayan Bank (cumulative arrear for the period from 31-12-2003 to FY 2008-09) 5 Agricultural Credit Programme of Rajshahi Bangladesh Bank 20/03/2020 500.00 Krishi Unnayan Bank (2020-21) Total -Agricultural Credit : 4,967.32 Biman 1 Senior Loan for purchasing 1st 777-300 JP Morgan 20/10/2011 227.00 Boeing by Bangladesh Biman 2 Senior -

A Case Study of the Banking and Insurance Sector in Bangladesh

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Ahmad, Salahuddin; Khanal, Dilli Raj Working Paper Services Trade in Developing Asia: A Case Study of the Banking and Insurance Sector in Bangladesh ARTNeT Working Paper Series, No. 38 Provided in Cooperation with: Asia-Pacific Research and Training Network on Trade (ARTNeT), Bangkok Suggested Citation: Ahmad, Salahuddin; Khanal, Dilli Raj (2007) : Services Trade in Developing Asia: A Case Study of the Banking and Insurance Sector in Bangladesh, ARTNeT Working Paper Series, No. 38, Asia-Pacific Research and Training Network on Trade (ARTNeT), Bangkok This Version is available at: http://hdl.handle.net/10419/178396 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. www.econstor.eu Asia-Pacific Research and Training Network on Trade Working Paper Series, No. -

INTERNSHIP REPORT on an EVALUATION of the EFFECTIVENESS of TRAINING PROGRAMS of NATIONAL BANK LIMITED. Submission Date

INTERNSHIP REPORT ON AN EVALUATION OF THE EFFECTIVENESS OF TRAINING PROGRAMS OF NATIONAL BANK LIMITED. Supervised By: Mr. Sheikh Abdur Rahim Associate Professor Department of Business Administration Faculty of Business & Entrepreneurship Daffodil International University Prepared By: Name: Sonia Khatun Id: 171-14-2330 Department of Business Administration Faculty of Business & Entrepreneurship Daffodil International University Submission Date: 15th December, 2018 ©Daffodil International university Letter of Transmittal Date: 15th December, 2018 To, Mr. Sheikh Abdur Rahim Associate Professor Department of Business Administration Faculty of Business &Entrepreneurship Daffodil International University Subject: Prayer for the Submission of Internship Report Dear Sir, I have the pleasure to inform you that, I have prepared my internship report on “An Evaluation of the Effectiveness of Training Program of National Bank Limited”. I have tried my level best to prepare this internship report properly. I would like to thank you for your value a see support and guidance during my Internship and preparing the report. May I therefore pray, and hope that you would be lived enough to accept my internship report and obedient thereby. Sincerely Yours, Name: Sonia Khatun ID :171-14-2330 MBA Program (Major in HRM) Batch: 46th Department of Business Administration Faculty of Business & Entrepreneurship ©Daffodil International university i Declaration I do hereby that the presented internship report on” Evaluation of the Effectiveness of Training Programs of National Bank Limited” is prepared by me.I tried my best to collect relevant information that made the report specific and original .This report is not submitted for any other course, degree, and fellowship. Whole report is uniquely prepared by me. -

Download PDF (1.8

© 2005 International Monetary Fund November 2005 IMF Country Report No. 05/410 [Month, Day], 2001 August 2, 2001 January 29, 2001 [Month, Day], 2001 August 2, 2001 Bangladesh: Poverty Reduction Strategy Paper Poverty Reduction Strategy Papers (PRSPs) are prepared by member countries in broad consultation with stakeholders and development partners, including the staffs of the World Bank and the IMF. Updated every three years with annual progress reports, they describe the country's macroeconomic, structural, and social policies in support of growth and poverty reduction, as well as associated external financing needs and major sources of financing. This country document for Bangladesh, dated October 16, 2005, is being made available on the IMF website by agreement with the member country as a service to users of the IMF website. To assist the IMF in evaluating the publication policy, reader comments are invited and may be sent by e-mail to [email protected]. Copies of this report are available to the public from International Monetary Fund x Publication Services 700 19th Street, N.W. x Washington, D.C. 20431 Telephone: (202) 623-7430 x Telefax: (202) 623-7201 E-mail: [email protected] x Internet: http://www.imf.org Price: $15.00 a copy International Monetary Fund Washington, D.C. ©International Monetary Fund. Not for Redistribution This page intentionally left blank ©International Monetary Fund. Not for Redistribution BANGLADESH Unlocking the Potential National Strategy for Accelerated Poverty Reduction General Economics Division Planning Commission Government of People’s Republic of Bangladesh October 16, 2005 ©International Monetary Fund. Not for Redistribution This page intentionally left blank ©International Monetary Fund. -

Annual Report-2018 CORPORATE INFORMATION

Annual Report 2018 DËiv e¨vsK wjwg‡UW Avengvb evsjvi HwZ‡n¨ jvwjZ Letter of Transmittal All Shareholders, Bangladesh Bank, Bangladesh Securities and Exchange Commission, Registrar of Joint Stock Companies and Firms, Dhaka Stock Exchange Limited and Chittagong Stock Exchange Limited. Subject: Annual Report for the year ended December 31, 2018. Dear Sir(s), We are delighted to enclose a copy of the Annual Report 2018 together with the audited Financial Statements as at the position of December 31, 2018. The report includes Income Statements, Cash Flow Statements along with notes thereon of Uttara Bank Limited and its subsidiaries namely “UB Capital & Investment Limited” and “Uttara Bank Securities Limited”. This is for your kind information and record please. Best regards. Yours sincerely, Iftekhar Zaman Executive General Manager & Secretary Contents Notice of the 36th Annual General Meeting 4 Corporate Information 5 Highlights of the 35th Annual General Meeting 6 Board of Directors 8 Executive Committee, Audit Committee & Risk Management Committee 9 Profiles of the Board of Directors 10 Message from the Chairman 18 Message from the Vice Chairman 20 Message from the Managing Director & CEO 22 CEO and CFO’s declaration to the Board 25 Report of the Audit Committee 26 Photo Album 28 SMT, RMC & ALCO 31 Some activities of Uttara Bank Limited 32 Name of the Executives 40 Directors’ Report 42 Five years at a Glance 76 Corporate Governance 78 Certificate on compliance status of Corporate Governance Guidelines of BSEC 79 Report on Risk Management 89 Report on Green Banking 120 Report on Corporate Social Responsibility 122 Credit Rating Report 124 Auditors’ Report 126 Consolidated Financial Statements 132 Financial Statements: Uttara Bank Limited 138 Notes to the Financial Statements 144 Highlights on overall activities of the Bank 208 Annexures 209 Financial Statements: Off-Shore Banking Unit 214 Value Added Statement 220 Economic Value added Statement 221 Market Value Addition Statement 222 Auditors' Report to the Shareholders of UB Capital and Investment Ltd.