Principles of Investment Risk Management

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Asset and Risk Allocation Policy

____________________________________________________________________________ UNIVERSITY OF CALIFORNIA GENERAL ENDOWMENT POOL ASSET AND RISK ALLOCATION POLICY Approved March 15, 2018 ______________________________________________________________________________ UNIVERSITY OF CALIFORNIA GENERAL ENDOWMENT POOL ASSET AND RISK ALLOCATION POLICY POLICY SUMMARY/BACKGROUND The purpose of this Asset and Risk Allocation Policy (“Policy”) is to define the asset types, strategic asset allocation, risk management, benchmarks, and rebalancing for the University of California General Endowment Pool (“GEP”). The Investments Subcommittee has consent responsibilities over this policy. POLICY TEXT ASSET CLASS TYPES Below is a list of asset class types in which the GEP may invest so long as they do not conflict with the constraints and restrictions described in the GEP Investment Policy Statement. The criteria used to determine which asset classes may be included are: Positive contribution to the investment objective of GEP Widely recognized and accepted among institutional investors Low cross correlations with some or all of the other accepted asset classes Based on the criteria above, the types of assets for building the portfolio allocation are: 1. Public Equity Includes publicly traded common and preferred stock of issuers domiciled in US, Non-US, and Emerging (and Frontier) Markets. The objective of the public equity portfolio is to generate investment returns with adequate liquidity through a globally diversified portfolio of common and preferred stocks. 2. Liquidity (Income) Liquidity includes a variety of income related asset types. The portfolio will invest in interest bearing and income based instruments such as corporate and government bonds, high yield debt, emerging markets debt, inflation linked securities, cash and cash equivalents. The portfolio can hold a mix of traditional (benchmark relative) strategies and unconstrained (benchmark agnostic) strategies. -

Tracking Error

India Index Services & Products Ltd. Tracking Error TRACKING ERROR An Index Fund is a mutual fund scheme that invests in the securities in the target Index in the same proportion or weightage of the securities as it bears to the target index. The investment objective of an index fund is to achieve returns which are commensurate to that of the target Index. An investment manager attempts to replicate the investment results of the target index by holding all the securities in the Index. Though Index Funds are designed to provide returns that closely track the benchmarked Index, Index Funds carry all the risks associated with the type of asset the fund holds. Indexing merely ensures that the returns of the Index Fund will not stray far from the returns on the Index that the fund mimics. Still there are instances, which are mentioned below, that leads to mismatch of the returns of the index with that of the fund. This mismatch or the difference in the returns of the Index with that of the fund is known as Tracking Error. Tracking Error Tracking error is defined as the annualised standard deviation of the difference in returns between the Index fund and its target Index. In simple terms, it is the difference between returns from the Index fund to that of the Index. An Index fund manager needs to calculate his tracking error on a daily basis especially if it is open-ended fund. Lower the tracking error, closer are the returns of the fund to that of the target Index. -

TRACKING ERROR: an Essential Tool in Evaluating Index Funds

JOURNAL OF INVESTMENT CONSULTING TRACKING ERROR: An Essential Tool in Evaluating Index Funds By Chris Tobe, CFA As the dollars being indexed grow and portfolio management becon1es more sophisticated, consultants should demand tighter tracking to the index in question from their index n1anagers. In fact, the key to assessiI1g index fund managers is determining if their performance has tracked their benchmarks within reasonable tolerances. The alltl10r reviews what is known about this aspect of performance evaluation. He also sl1ares 11is experie11ce in detern1ining what factors caused a difference in performance for a $3 billion S&P 500 index fund. This article is based on a study written by the author and should be no attempt to outperform the index or Dr. Ken Miller for Kentucky State Auditor Edward B. bencl1mark. William F Sharpe holds that a passive Hatchett Jr. The study was reported in the July 27, 1998, strategy requires the manager issue of Pensions and Investments. Earlier versions of this ... to hold every security from the market, with each article were presented at two conferences on indexing. represented in the same manner as in the n1arket. Thus, if security X represents 3 percent of the value ver $1 trillion is now being managed of the securities in the market, a passive investor's within index funds. Lipper lists the portfolio will have 3 percent of its value invested in Vanguard 500 Index fund as the second X. Equivalently; a passive manager will hold the same percentage of the total outstanding amount of largest stock fllnd in the world with a each security in the market. -

Ten Reasons Why Commodities

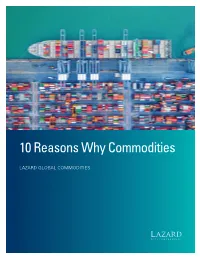

10 Reasons Why Commodities LAZARD GLOBAL COMMODITIES 1. Build a bridge to the new economy Commodity trading is indispensable in the production and delivery of the fossil fuels that power today’s economy, and it will be equally indispensable as energy markets evolve. Global futures markets are developing for the trading of carbon allotments as well as wind and solar power. And even now many of the components of tomorrow’s transport—such as the rare metals used in batteries for electric vehicles—trade on futures exchanges. 2. Invest in the global recovery Commodity returns rise fastest when business confidence returns and the pace of economic growth begins to quicken. Base commodity demand does not vary—people have to heat and eat regardless of economic conditions. As the business cycle revives, as it has recently, incremental demand should surge. 3. Profit from inflation Rising Inflation Just as rising commodity prices drive Average Month-on-Month Change (1990–Present) consumer price inflation, they also drive (%) Commodities Equities Bonds commodity returns. No other asset class 2 responds more or more consistently 1 to heightened inflation and inflation 0 expectations. At low inflation levels like those -1 currently, commodities have historically -2 -3 delivered positive returns in contrast to 1%–2% Inflation 2%–3% Inflation 3%–5% Inflation 5%+ Inflation equity and fixed income markets, and these (25 Months) (53 Months) (73 Months) (11 Months) returns have remained positive when inflation As of 30 November 2017 Inflation was rising in 167 months and not rising in 167 months. Months of rising has become extreme. -

Corporate Methodology

Criteria | Corporates | General: Corporate Methodology Global Criteria Officer, Corporate Ratings: Mark Puccia, New York (1) 212-438-7233; [email protected] Chief Credit Officer, Americas: Lucy A Collett, New York (1) 212-438-6627; [email protected] European Corporate Ratings Criteria Officer: Peter Kernan, London (44) 20-7176-3618; [email protected] Criteria Officer, Asia Pacific: Andrew D Palmer, Melbourne (61) 3-9631-2052; [email protected] Criteria Officer, Corporate Ratings: Gregoire Buet, New York (1) 212-438-4122; [email protected] Primary Credit Analysts: Mark S Mettrick, CFA, Toronto (1) 416-507-2584; [email protected] Guy Deslondes, Milan (39) 02-72111-213; [email protected] Secondary Contacts: Michael P Altberg, New York (1) 212-438-3950; [email protected] David C Lundberg, CFA, New York (1) 212-438-7551; [email protected] Anthony J Flintoff, Melbourne (61) 3-9631-2038; [email protected] Pablo F Lutereau, Buenos Aires (54) 114-891-2125; [email protected] Table Of Contents SUMMARY OF THE CRITERIA SCOPE OF THE CRITERIA IMPACT ON OUTSTANDING RATINGS EFFECTIVE DATE AND TRANSITION METHODOLOGY WWW.STANDARDANDPOORS.COM/RATINGSDIRECT NOVEMBER 19, 2013 1 1218904 | 300023050 Table Of Contents (cont.) A. Corporate Ratings Framework B. Industry Risk C. Country Risk D. Competitive Position E. Cash Flow/Leverage F. Diversification/Portfolio Effect G. Capital Structure H. Financial Policy I. Liquidity J. Management And Governance K. Comparable Ratings Analysis SUPERSEDED CRITERIA FOR ISSUERS WITHIN THE SCOPE OF THESE CRITERIA RELATED CRITERIA APPENDIXES A. Country Risk B. Competitive Position C. Cash Flow/Leverage Analysis D. -

Budgeting, Planning and Forecasting for Asset Management

BUDGETING, PLANNING AND FORECASTING FOR ASSET MANAGEMENT YOU MANAGE ASSETS, LET US MANAGE YOUR PERFORMANCE Just about everything in investment management is uncertain: you’ve got volatile markets, shifting investor profiles, fluctuating portfolios, demanding clients, an uncertain political climate and increased regulation to deal with - your performance shouldn’t be a mystery. CCH Tagetik enables you to keep a finger to the pulse of your corporate performance, while equipping you with the tools to create budgets, plans, models and forecasts faster and more efficiently to drive illuminating insights and better business decisions. CCH TAGETIK PLANNING FOR ASSET MANAGEMENT Align Finance & Operations Reduce Planning Cycle Plan True Revenue and with Unified Planning Time Automate Fees Increase accuracy and confidence in As a single unified source for all your Build a comprehensive view of your numbers when budgets, plans, planning data, CCH Tagetik shaves customers, plan across different asset forecasts and models across your days, weeks, or in some cases months types, and automate fee processes with company are created using a single off the planning cycle. With dynamic highly customized accounting rules. version of the truth in a single system. dashboards, workflow and controls, View real-time assets under With automated real-time and historical Managers can address bottlenecks management, revenues and expenses data, CCH Tagetik aligns strategic, before they happen. Planners work with automated calculations, whether financial and operational planning smarter and more efficiently with that’s bank deposits, mutual funds, enterprise-wide, so the cycle is personalized work papers, task lists and cash or other funds under discretionary completed faster and with a 360* view self-service analysis. -

Lazard Commodities Fund Monthly

Lazard Commodities Fund APR Commentary 2019 Market Overview OPEC discipline continued to drive performance in oil and related products for the BCOMTR during April, and the top performers were gasoline, crude oil and heating oil. Elsewhere, non-OPEC capital discipline proved helpful, even for US shale, and the Baker Hughes US Crude Oil Rotary Rig Count fell by 26 rigs during the month. is occurred despite the renewal of economic sanctions prohibiting the sale of Iran oil, and the continued decline in Venezuela oil production resulting from the country’s political crisis, and the recently imposed oil sanctions. e iron ore sector continued to wrestle with the consequences of the Brumadinho mine collapse in Brazil. It has been estimated that 10% of iron ore supply has been immediately suspended, and additional tailings dams are under review. In agriculture, there was concern about oods in the US Midwest delaying crop plantings, especially for corn, which require a much longer planting cycle than soy. Some of this appears to have been offset by healthy grain inventories, and the trade dispute with China. e number of African swine fever (ASF) outbreaks continued to rise during the month. e top three performers in the BCOMTR were: • RBOB Gasoline +11.0% • Brent Crude +7.4% • WTI Crude +6.6% e bottom three detractors in the BCOMTR were: • Kansas Wheat -9.7% • Wheat -6.9% • Aluminum -6.6% April Performance of Commodities, Stocks and Bonds Currency (US$) 4/2019 Bloomberg Commodity Total Return Index -0.42% S&P 500 Index 4.05% MSCI World 3.60% Bloomberg Barclays US Aggregate Total Return Bond Index 0.03% Bloomberg Barclays Global-Aggregate Total Return Bond Index -0.30% Portfolio Review We deploy a blended approach to commodity investing by investing in commodities and commodity related equities. -

Asset Management Risk 101 Where to Start Triage Have You Ever Wondered Why…

Asset Management Risk 101 Where to start Triage Have you ever wondered why… • How would you prioritize all transportation asset related investments across the country? • Where would you start? “The objective of this performance and outcome-based program is for States to invest resources in projects that collectively will make progress toward the achievement of the national goals.” FTA MAP-21 Fact Sheet Federal perspective “MAP–21 fundamentally shifted the focus of Federal investment in transit to emphasize the need to maintain, rehabilitate, and replace existing transit investments.” (Federal Register / Vol. 81, No. 143 / Tuesday, July 26, 2016 / Rules and Regulations, P. 48912) “In these financially constrained times, transit agencies will need to be more strategic in the use of all available funds.” (Federal Register / Vol. 81, No. 143 / Tuesday, July 26, 2016 / Rules and Regulations, P. 48946) MAP-21 Goal area National goal Safety To achieve a significant reduction in traffic fatalities and serious injuries on all public roads Infrastructure condition To maintain the highway infrastructure asset system in a state of good repair Congestion reduction To achieve a significant reduction in congestion on the National Highway System System reliability To improve the efficiency of the surface transportation system Freight movement and economic vitality To improve the national freight network, strengthen the ability of rural communities to access national and international trade markets, and support regional economic development Environmental sustainability To enhance the performance of the transportation system while protecting and enhancing the natural environment Reduced project delivery delays To reduce project costs, promote jobs and the economy, and expedite the movement of people and goods by accelerating project completion through eliminating delays in the project development and delivery process, including reducing regulatory burdens and improving agencies’ work practices MAP 21: FTA requirements for TAMP elements No. -

Hedging Climate Risk Mats Andersson, Patrick Bolton, and Frédéric Samama

AHEAD OF PRINT Financial Analysts Journal Volume 72 · Number 3 ©2016 CFA Institute PERSPECTIVES Hedging Climate Risk Mats Andersson, Patrick Bolton, and Frédéric Samama We present a simple dynamic investment strategy that allows long-term passive investors to hedge climate risk without sacrificing financial returns. We illustrate how the tracking error can be virtually eliminated even for a low-carbon index with 50% less carbon footprint than its benchmark. By investing in such a decarbonized index, investors in effect are holding a “free option on carbon.” As long as climate change mitigation actions are pending, the low-carbon index obtains the same return as the benchmark index; but once carbon dioxide emissions are priced, or expected to be priced, the low-carbon index should start to outperform the benchmark. hether or not one agrees with the scientific the climate change debate is not yet fully settled and consensus on climate change, both climate that climate change mitigation may not require urgent Wrisk and climate change mitigation policy attention. The third consideration is that although the risk are worth hedging. The evidence on rising global scientific evidence on the link between carbon dioxide average temperatures has been the subject of recent (CO2) emissions and the greenhouse effect is over- debates, especially in light of the apparent slowdown whelming, there is considerable uncertainty regarding in global warming over 1998–2014.1 The perceived the rate of increase in average temperatures over the slowdown has confirmed the beliefs of climate change next 20 or 30 years and the effects on climate change. doubters and fueled a debate on climate science There is also considerable uncertainty regarding the widely covered by the media. -

Tracking Error and the Information Ratio

It Is More Than]ust Performance: TRACKING ERROR AND THE INFORMATION RATIO By Jay L. Shein, Ph.D., ClMA, CFP ONE OF OUR MOST POPULAR CONTRIBUTORS REVIEWS SOME QUANTITATIVE TECHNIQUES THAT CAN ASSIST THE CONSULTANT IN MANAGER SELECTIONS AND IN ASSET ALLOCATION DESIGN. Introduction properly these statistical measures can be dentifying and selecting the most appropri useful tools. ate mutual fund or money manager to use Tracking error was defined by Tobe (1999) as in an investor's portfolio are major aspects the percentage difference in total return between of the investment consultants responsibili an index fund and the benchmark index the fund ties. This is true for both active and passive was designed to replicate. This definition of track money manager searches and selection. ing error is best used for evaluation of a passive When searching for and selecting money man manager such as an index fund. Tracking error agers, consultants and investment advisors typical used in the context of active manager evaluation is ly look at both qualitative and quantitative infor better defined as active manager risk. For purpos mation before making their recommendations. The es of this commentary, tracking error is defined as investment consultant knows that items such as the standard deviation between two return series philosophy, process, people, and strategic business written as: 1 plans are important, if not sometimes more impor tant than historical performance. Even though the qualitative side is important, the investment con TE= i-I sultant will ultimately use some quantitative mea N-l sure such as a ratio, statistic, risk-adjusted measure of performance, and/or absolute performance to Where: validate the qualitative component of money man IE = Tracking Error ager search and selection. -

Asset Management Tax Update: a New Limited Partnership Fund

Asset Management – Tax update A new Limited Partnership Fund regime for Hong Kong The introduction of the Limited Partnership Fund Bill is one of the Hong Kong Summary Government’s flagship initiatives and a major development in continuing to promote The Limited Partnership Hong Kong as Asia’s leading Private Equity hub. This follows extensive consultation Fund Bill is an important by the Government with the asset management industry in Hong Kong with the development for the funds objective of introducing an LPF regime that is on par with the more established industry in Hong Kong as domicile jurisdictions. the Hong Kong Asian focused funds have always looked to Hong Kong as a regional hub in which to Government looks to situate their investment teams. However, these funds have typically established or encourage funds to domiciled their collective investment vehicles in jurisdictions such as the Cayman domicile here. The Islands because such jurisdictions provide a regulatory framework with which proposed Limited investors are familiar, and a tax neutral investment platform which allows investors to Partnership Fund (LPF) be taxed on investment returns in their home jurisdictions. regime will provide a We anticipate that the LPF regime will prove beneficial to asset managers looking for comparable regulatory an alternative jurisdiction to establish their offshore funds. framework to other jurisdictions commonly used by Asian focused Key features of the regime funds and should cement Establishing an LPF The fund must be constituted by a limited partnership Hong Kong’s position as agreement with one general partner and at least one limited partner. -

Asset Management and Financial Stability

OFROFFICE OF FINANCIAL RESEARCH Asset Management and Financial Stability September 2013 Contents Introduction 1 Industry Activities 3 Vulnerabilities 9 Transmission Channels 21 Data Gaps 24 Appendix: Asset Management Firms and Activities 27 References 29 Introduction This report provides a brief overview of the asset management industry and an analysis of how asset management firms and the activities in which they engage can introduce vulnerabilities that could pose, amplify, or transmit threats to financial stability. The Financial Stability Oversight Council (the Council) decided to study the activities of asset management firms to better inform its analysis of whether—and how—to consider such firms for enhanced pruden- tial standards and supervision under Section 113 of the Dodd-Frank Act.1 The Council asked the Office of Financial Research (OFR), in collaboration with Council members, to provide data and analysis to inform this consideration. This study responds to that request by analyzing industry activities, describing the factors that make the industry and individual firms vulnerable to financial shocks, and considering the channels through which the industry could transmit risks across financial markets. The U.S. asset management industry oversees the allocation of approximately $53 trillion in financial assets (see Figure 1). The industry is central to the allocation of financial assets on behalf of investors. By facilitating investment for a broad cross-section of individuals and institutions, discretionary asset management plays a key role in capital formation and credit intermediation, while spreading any gains or losses across a diverse population of market participants. The industry is marked by a high degree of innovation, with new prod- ucts and technologies frequently reshaping the competitive landscape and changing the way that financial services are provided.