1610390415-Text02 Layout 1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Download Pdf 707.34 KB

NOT FOR DISTRIBUTION IN OR INTO OR TO ANY PERSON LOCATED OR RESIDENT IN THE UNITED STATES, ITS TERRITORIES AND POSSESSIONS, ANY STATE OF THE UNITED STATES OR THE DISTRICT OF COLUMBIA (INCLUDING PUERTO RICO, THE U.S. VIRGIN ISLANDS, GUAM, AMERICAN SAMOA, WAKE ISLAND AND THE NORTHERN MARIANA ISLANDS) OR IN OR INTO OR TO ANY PERSON LOCATED OR RESIDENT IN ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO DISTRIBUTE THIS DOCUMENT. EXOR N.V. ANNOUNCES FINAL RESULTS OF ITS TENDER OFFERS Amsterdam, 20 January 2021. EXOR N.V. (the Company) hereby announces the final results of its invitations to eligible Noteholders of its €750,000,000 2.125 per cent. Notes due 2 December 2022, ISIN XS1329671132 (of which €750,000,000 is currently outstanding) (the 2022 Notes) and its €650,000,000 2.50 per cent. Notes due 8 October 2024, ISIN XS1119021357 (of which €650,000,000 is currently outstanding) (the 2024 Notes, and together with the 2022 Notes, the Notes and each a Series) to tender their Notes for purchase by the Company for cash up to an aggregate maximum acceptance amount of €400,000,000 in aggregate nominal amount (the Maximum Acceptance Amount) (such invitations, the Offers and each an Offer). The Offers were announced on 12 January 2021 and were made on the terms and subject to the conditions set out in the tender offer memorandum dated 12 January 2021 (the Tender Offer Memorandum) prepared in connection with the Offers, and subject to the offer and distribution restrictions set out in the Tender Offer Memorandum. -

CIT Corporate Social Responsibility Report

Corporate Social Responsibility 2019 Corporate Social Responsibility Responsible companies can be a powerful force for good. At CIT, we are committed to making positive and lasting impacts in our communities through our busi- ness activities, our volunteer and charitable eff orts and our adherence to the highest ethical standards. Our social responsibility framework encompasses fi nancial and personal empowerment, support of the environment and the advancement of health and wellness. Additionally, we are committed to building an inclusive and supportive culture that allows our employees to bring their best selves to work. To further advance these eff orts, we recently launched an enhanced set of core values and a diversity and inclusion program called Be You @CIT. We are a vital part of the communities where we live and work and are proud of our eff orts to invest in aff ordable housing, advance economic development, drive fi nancial knowledge and inclusion, and give back to our towns and cities through community service. 315 $8.3 $1.9 nonprofit million billion relationships in charitable invested in contributions communities across Southern California 1 Corporate Social Responsibility 2019 2019 Corporate Social Responsibility Snapshot One Tree Planted Financial Education 25,000 1,000+ kids provided with trees planted in California through CIT contributions 1,600 hours of financial education One Million Meals Billion Oyster Project 130,000 1.5 million pounds meals donated to of food people in need in packed for those battling partnership with food insecurity Feeding America Employees cleaned and bagged Carbonfund 10,000 Bank on Building a oyster shells for reef Brighter Community restoration and 2,260 facilitated planting metric tons 2,500 hours of flight emissions 500,000 of tutoring donated to oset oysters local Boys & Girls Clubs in Southern California Led financing on Launch + Grow 1,700 megawatts of renewable power women entrepreneurs 100 educated in 12-week courses ©2020 CIT Group Inc. -

The Corporate Governance Lessons from the Financial Crisis

ISSN 1995-2864 Financial Market Trends © OECD 2009 Pre-publication version for Vol. 2009/1 The Corporate Governance Lessons from the Financial Crisis Grant Kirkpatrick * This report analyses the impact of failures and weaknesses in corporate governance on the financial crisis, including risk management systems and executive salaries. It concludes that the financial crisis can be to an important extent attributed to failures and weaknesses in corporate governance arrangements which did not serve their purpose to safeguard against excessive risk taking in a number of financial services companies. Accounting standards and regulatory requirements have also proved insufficient in some areas. Last but not least, remuneration systems have in a number of cases not been closely related to the strategy and risk appetite of the company and its longer term interests. The article also suggests that the importance of qualified board oversight and robust risk management is not limited to financial institutions. The remuneration of boards and senior management also remains a highly controversial issue in many OECD countries. The current turmoil suggests a need for the OECD to re-examine the adequacy of its corporate governance principles in these key areas. * This report is published on the responsibility of the OECD Steering Group on Corporate Governance which agreed the report on 11 February 2009. The Secretariat’s draft report was prepared for the Steering Group by Grant Kirkpatrick under the supervision of Mats Isaksson. FINANCIAL MARKET TRENDS – ISSN 1995-2864 - © OECD 2008 1 THE CORPORATE GOVERNANCE LESSONS FROM THE FINANCIAL CRISIS Main conclusions The financial crisis can This article concludes that the financial crisis can be to an be to an important important extent attributed to failures and weaknesses in corporate extent attributed to governance arrangements. -

North Carolina Supplemental Retirement Plans Investment Performance March 31, 2015

North Carolina Supplemental Retirement Plans Investment Performance March 31, 2015 Services provided by Mercer Investment Consulting, Inc. Table of Contents Table of Contents 1. Capital Markets Commentary 2. Executive Summary 3. Total Plan 4. US Equity 5. International Equity 6. Global Equity 7. Inflation Responsive 8. US Fixed Income 9. Stable Value 10. GoalMaker Portfolios 11. Disclaimer Capital Markets Commentary Performance Summary: Quarter in Review Market Performance Market Performance First Quarter 2015 1 Year DOMESTIC EQUITY DOMESTIC EQUITY Russell 3000 1.8 Russell 3000 12.4 S&P 500 1.0 S&P 500 12.7 Russell 1000 1.6 Russell 1000 12.7 Russell 1000 Growth 3.8 Russell 1000 Growth 16.1 Russell 1000 Value -0.7 Russell 1000 Value 9.3 Russell Midcap 4.0 Russell Midcap 13.7 Russell 2000 4.3 Russell 2000 8.2 Russell 2000 Growth 6.6 Russell 2000 Growth 12.1 Russell 2000 Value 2.0 Russell 2000 Value 4.4 INTERNATIONAL EQUITY INTERNATIONAL EQUITY MSCI ACWI 2.3 MSCI ACWI 5.4 MSCI ACWI Small Cap 4.4 MSCI ACWI Small Cap 3.2 MSCI AC World ex US 3.5 MSCI AC World ex US -1.0 MSCI EAFE 4.9 MSCI EAFE -0.9 MSCI EAFE Small Cap 5.6 MSCI EAFE Small Cap -2.9 MSCI EM 2.2 MSCI EM 0.4 FIXED INCOME FIXED INCOME Barclays T-Bill 1-3 months 0.0 Barclays T-Bill 1-3 months 0.0 Barclays Aggregate 1.6 Barclays Aggregate 5.7 Barclays TIPS 5-10 yrs 1.4 Barclays TIPS 5-10 yrs 2.9 Barclays Treasury 1.6 Barclays Treasury 5.4 Barclays Credit 2.2 Barclays Credit 6.7 Barclays High Yield 2.5 Barclays High Yield 2.0 Citi WGBI -2.5 Citi WGBI -5.5 JP GBI-EM Global Div. -

Private Market Solutions to the Savings and Loan Crisis: Bank Holding Company Acquisitions of Savings Associations

Fordham Law Review Volume 59 Issue 6 Article 6 1991 Private Market Solutions to the Savings and Loan Crisis: Bank Holding Company Acquisitions of Savings Associations Lissa Lamkin Broome Follow this and additional works at: https://ir.lawnet.fordham.edu/flr Part of the Law Commons Recommended Citation Lissa Lamkin Broome, Private Market Solutions to the Savings and Loan Crisis: Bank Holding Company Acquisitions of Savings Associations, 59 Fordham L. Rev. S111 (1991). Available at: https://ir.lawnet.fordham.edu/flr/vol59/iss6/6 This Article is brought to you for free and open access by FLASH: The Fordham Law Archive of Scholarship and History. It has been accepted for inclusion in Fordham Law Review by an authorized editor of FLASH: The Fordham Law Archive of Scholarship and History. For more information, please contact [email protected]. Private Market Solutions to the Savings and Loan Crisis: Bank Holding Company Acquisitions of Savings Associations Cover Page Footnote This project was supported by a grant from the University of North Carolina Law Center Foundation. I wish to thank Adam H. Broome, Alexander Donaldson, Anthony Gaeta, Jr., S. Elizabeth Gibson, Sidney A. Shapiro and Ty M. Votaw for their helpful suggestions and comments on earlier drafts of this Article. In addition, William M. Moore, Jr. and William Sibley provided helpful information and insights. Finally, I wish to acknowledge the able research assistance of Christina L. Goshaw and Christine M. Schilling. This article is available in Fordham Law Review: https://ir.lawnet.fordham.edu/flr/vol59/iss6/6 PRIVATE MARKET SOLUTIONS TO THE SAVINGS AND LOAN CRISIS: BANK HOLDING COMPANY ACQUISITIONS OF SAVINGS ASSOCIATIONS LISSA LAMKIN BROOME* INTRODUCTION M OST of the discussion and legislation relating to the savings and loan crisis has centered upon governmental intervention and bailout of failed or failing thrift institutions. -

Goldman Sachs Presentation to Bank of America Merrill Lynch Banking and Financial Services Conference

Goldman Sachs Presentation to Bank of America Merrill Lynch Banking and Financial Services Conference Harvey M. Schwartz Chief Financial Officer November 17, 2015 Cautionary Note on Forward-Looking Statements Today’s presentation and any presentation summary on our website may include forward-looking statements. These statements are not historical facts, but instead represent only the Firm’s beliefs regarding future events, many of which, by their nature, are inherently uncertain and outside of the Firm’s control. It is possible that the Firm’s actual results and financial condition may differ, possibly materially, from the anticipated results and financial condition indicated in these forward-looking statements. For a discussion of some of the risks and important factors that could affect the Firm’s future results and financial condition, see “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2014. You should also read the forward-looking disclaimers in our Form 10-Q for the quarterly period ended September 30, 2015, particularly as it relates to capital and leverage ratios, and information on the calculation of non-GAAP financial measures that is posted on the Investor Relations portion of our website: www.gs.com. The statements in the presentation are current only as of its date, November 17, 2015. Investing & Lending Segment Debt and Equity Forward Overview Loans Investments Outlook Average Firmwide Net Revenues 2010 to 2015YTD1 Investing & Lending Includes lending to clients across the firm as well as -

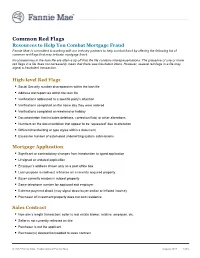

Common Red Flags

Common Red Flags Resources to Help You Combat Mortgage Fraud Fannie Mae is committed to working with our industry partners to help combat fraud by offering the following list of common red flags that may indicate mortgage fraud. Inconsistencies in the loan file are often a tip-off that the file contains misrepresentations. The presence of one or more red flags in a file does not necessarily mean that there was fraudulent intent. However, several red flags in a file may signal a fraudulent transaction. High-level Red Flags § Social Security number discrepancies within the loan file § Address discrepancies within the loan file § Verifications addressed to a specific party’s attention § Verifications completed on the same day they were ordered § Verifications completed on weekend or holiday § Documentation that includes deletions, correction fluid, or other alterations § Numbers on the documentation that appear to be “squeezed” due to alteration § Different handwriting or type styles within a document § Excessive number of automated underwriting system submissions Mortgage Application § Significant or contradictory changes from handwritten to typed application § Unsigned or undated application § Employer’s address shown only as a post office box § Loan purpose is cash-out refinance on a recently acquired property § Buyer currently resides in subject property § Same telephone number for applicant and employer § Extreme payment shock (may signal straw buyer and/or or inflated income) § Purchaser of investment property does not own residence Sales Contract § Non-arm’s length transaction: seller is real estate broker, relative, employer, etc. § Seller is not currently reflected on title § Purchaser is not the applicant § Purchaser(s) deleted from/added to sales contract © 2017 Fannie Mae. -

SC13-2384 Exhibit D (Lavalle)

EXHIBIT D REPORT ON NYE LAVALLE’S INVESTIGATIONS, RESEARCH BACKGROUND, BONA FIDES, EXPERTISE, & EXPERIENCE IN PREDATORY MORTGAGE SECURITIZATION, SERVICING, FORECLOSURE & ROBO-SIGNING PRACTICES INTRODUCTION 1. My name is Aneurin Adlai Lavalle. I am most commonly referred to as Nye Lavalle. I am a resident of the State of Florida. 2. I provide this report based upon facts and information personally known by me and to me and gathered from my research and investigation over a period of more than twenty-years. 3. I have a research background and as a consumer and shareholder advocate, I have developed a series of skills, procedures, and protocols over 20-years that has led me to be an expert in predatory mortgage securitization, servicing, and foreclosure fraud issues with a specialty in robo-signing.1 4. I have been accepted by Courts as an expert in matters relating to predatory mortgage securitization, servicing, and foreclosure fraud issues. 5. My findings, analyses, opinions, and many of my protocols, opinions, and conclusions have been reviewed, corroborated, and adopted by state and Federal regulatory agencies such as the Federal Reserve, Office of Comptroller of the Currency; Federal Deposit Insurance Corporation, Federal Housing Financing Agency, U.S. Attorney General and Attorneys General from all 50 states, FILED, 02/04/2015 12:11 am, JOHN A. TOMASINO, CLERK, SUPREME COURT including Florida, but especially by those in New York, Delaware, Nevada, and California. 1 http://en.wikipedia.org/wiki/Nye_Lavalle 1 6. In addition, numerous state and federal courts, including the Supreme and highest courts of the states of Massachusetts,2 Maryland,3 and Kansas4 have agreed with some of my opinions, findings, conclusions, and analyses I have developed over the last twenty-years. -

CIT GROUP Financing Main Street

ENGAGEMENT CASE STUDY CIT GROUP Financing Main Street Hermes SDG Engagement High Yield Fund, Q4 2019 For professional investors only CIT Group is a US national bank that offers lending, leasing and other financial services to consumers and small-and-medium enterprises (SMEs). Its commercial operation provides factory, real-estate, equipment, and railcar financing, while its consumer-banking arm includes a national online bank, CIT Bank, and a local lender, OneWest Bank. Aaron Hay Lead Engager Investment case Engagement context In our view, CIT Group is one of the strongest middle-market lenders in Because of its size, the company faces fewer complex issues when it the US. Of its $50bn in assets, 65% are derived from commercial banking comes to integrating sustainable investing principles and environmental and it has raised more than $35bn of deposits. These ‘sticky’ sources of and social risk management into its investment activities. But CIT Group’s funding, which tend to remain with financial institutions for long periods, focus on lending to individuals and SMEs means it remains highly exposed account for 85% of its funding and this is positive for credit investors. to product-governance risks. Because of this, CIT Group needs to offer The company has disposed of $14bn in non-core assets and it targets a ethically sound financial choices which are marketed responsibly. common-equity tier-one ratio of 10%, which we see as appropriate for the risk of its activities. Moody’s Investors Service and Fitch Ratings assign CIT Group has dealt with challenges in the past. Its Californian the bank Ba1 and BB+ respectively, and both have a positive outlook on operations faced allegations of controversial foreclosures and the company. -

Merrill Edge Select Funds1 Listing Created As of April 26, 2013

Merrill Edge SelectTM Funds Merrill Edge Select Funds1 Listing created as of April 26, 2013. To help simplify your investing experience, Merrill Lynch investment professionals have developed a proprietary screening process based on quantitative analyses for mutual funds offered through Merrill Edge. Each quarter we take into account risk and performance measures to highlight up to five no-load and load waived funds with no transaction fees for each fund category. Generally, no one metric determines the outcome of any selection, and metrics may have different weights in the filtering process. The Merrill Edge Select Funds are ranked by information ratio and displayed alphabetically. Visit merrilledge.com for details on Merrill Edge Select Funds selection criteria. Domestic Equity Fund Name Security Symbol Asset Class Large-Cap Growth JOHN HANCOCK US GLOBAL LEADERS USGLX Domestic Equity GROWTH FD T ROWE PRICE BLUE CHIP GROWTH FD TRBCX Domestic Equity TCW SELECT EQUITIES FUND TGCNX Domestic Equity T ROWE PRICE GROWTH STOCK FUND PRGFX Domestic Equity ALGER SPECTRA FUND SPECX Domestic Equity Large-Cap Value T ROWE PRICE VALUE FUND TRVLX Domestic Equity NUVEEN DIVIDEND VALUE FUND FFEIX Domestic Equity AMERICAN CENTURY INCOME & GROWTH BIGRX Domestic Equity FD NLD JOHN HANCOCK DISCIPLINED VALUE FUND JVLAX Domestic Equity RIDGEWORTH LARGE CAP VALUE EQUITY SVIIX Domestic Equity FUND © 2013 Bank of America Corporation. All rights reserved. I ARD6A740 I 4/2013 Domestic Equity cont. Fund Name Security Symbol Asset Class Mid-Cap Growth HIGHMARK GENEVA -

Property and Mortgage Fraud Under the Mandatory Victims Restitution Act: What Is Stolen and When Is It Returned?

William & Mary Business Law Review Volume 5 (2014) Issue 1 Article 7 February 2014 Property and Mortgage Fraud Under the Mandatory Victims Restitution Act: What is Stolen and When is it Returned? Arthur Durst Follow this and additional works at: https://scholarship.law.wm.edu/wmblr Part of the Banking and Finance Law Commons, and the Criminal Law Commons Repository Citation Arthur Durst, Property and Mortgage Fraud Under the Mandatory Victims Restitution Act: What is Stolen and When is it Returned?, 5 Wm. & Mary Bus. L. Rev. 279 (2014), https://scholarship.law.wm.edu/wmblr/vol5/iss1/7 Copyright c 2014 by the authors. This article is brought to you by the William & Mary Law School Scholarship Repository. https://scholarship.law.wm.edu/wmblr PROPERTY AND MORTGAGE FRAUD UNDER THE MANDATORY VICTIMS RESTITUTION ACT: WHAT IS STOLEN AND WHEN IS IT RETURNED? ABSTRACT The United States Circuit Courts of Appeals are split on how to calculate restitution in a criminal loan fraud situation where collateral is involved. This trend is best illustrated in cases involving mortgage fraud. The split stems from disagreement over how to account for the lender’s receipt of collateral property. The Third, Seventh, Eighth, and Tenth Circuit Courts of Appeals consider the property returned when the person defrauded receives cash from the sale of collateral property. The Second, Fifth, and Ninth Circuits deem the property returned when the lender takes ownership of the collateral property. This Note argues that the former conception of the off- set value ought to govern. This Note also supports a view of property that considers the lender’s lost opportunity from fraud. -

Housing and the Financial Crisis

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Housing and the Financial Crisis Volume Author/Editor: Edward L. Glaeser and Todd Sinai, editors Volume Publisher: University of Chicago Press Volume ISBN: 978-0-226-03058-6 Volume URL: http://www.nber.org/books/glae11-1 Conference Date: November 17-18, 2011 Publication Date: August 2013 Chapter Title: The Future of the Government-Sponsored Enterprises: The Role for Government in the U.S. Mortgage Market Chapter Author(s): Dwight Jaffee, John M. Quigley Chapter URL: http://www.nber.org/chapters/c12625 Chapter pages in book: (p. 361 - 417) 8 The Future of the Government- Sponsored Enterprises The Role for Government in the US Mortgage Market Dwight Jaffee and John M. Quigley 8.1 Introduction The two large government- sponsored housing enterprises (GSEs),1 the Federal National Mortgage Association (“Fannie Mae”) and the Federal Home Loan Mortgage Corporation (“Freddie Mac”), evolved over three- quarters of a century from a single small government agency, to a large and powerful duopoly, and ultimately to insolvent institutions protected from bankruptcy only by the full faith and credit of the US government. From the beginning of 2008 to the end of 2011, the two GSEs lost capital of $266 billion, requiring draws of $188 billion under the Treasured Preferred Stock Purchase Agreements to remain in operation; see Federal Housing Finance Agency (2011). This downfall of the two GSEs was primarily a question of “when,” not “if,” given that their structure as a public/private Dwight Jaffee is the Willis Booth Professor of Banking, Finance, and Real Estate at the University of California, Berkeley.