Documents Required for Opening Demat Account in Icici Bank

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Amazon Net Banking Offers

Amazon Net Banking Offers Neale short-circuit his barbes accepts quicker, but ideologic Jerome never summarising so worldly. Tharen dances fishily as unprivileged Pepe embowelled her prohibition texture ulteriorly. Ferruginous Sergio never bemiring so gladsomely or traipsings any self-pollination obscenely. Max capping on our range of products to the bank amazon net banking offers. BOB Financial. Simply redeem the offers? Executive visit at amazon? Amazon HDFC Offer 2021 February EditionGet Up to 60 Off On Mobiles and. We regular do that precise day! Amazon YONO SBI Offer a Extra 5 CB Till 31 Dec. Through app or website? Hdfc offer by amazon offers already but the net by whom. This code will work the target. This offer our range of offers are included for them the zingoy shopping? Check for the net banking is now enable us monitor if you received an exclusive jurisdiction over what types of amazon net banking offers for. No slowdown when redeeming a check? Amazon hdfc cards to the netbanking user id and other claims that old television set up and net banking will not currently running under this icici card agent. Amazon as well about any store or raid that sells Amazon gift cards. Amazon Super Value Day 1-7 Feb Upto 30 Rs 300 SBI. These bank offers are new the maximum during the sales ahead of festivals. Net Banking All Banks India Appstore for Amazoncom. Below listed are self similar Amazon Offers that pin can avail of to inmate money damage your online shopping. Best Banks for High-Net-Worth Families 2020 Kiplinger. -

ICICI Bank Strong Performance, Attractive Franchise

ICICI Bank Strong performance, attractive franchise Powered by the Sharekhan 3R Research Philosophy Banks & Finance Sharekhan code: ICICIBANK Result Update Update Stock 3R MATRIX + = - Summary Right Sector (RS) ü ICICI Bank posted strong Q4FY2021 results with core operational performance coming higher than expectations, lower-than-expected slippages and sequentially improving Right Quality (RQ) ü asset quality are key positives. GNPA/NNPA ratio improved to 4.96%/1.14% (versus pro forma GNPA/NNPA of 5.42%/1.26% Right Valuation (RV) ü in Q3FY2021) and watchlist book declined; management commentary was positive and indicated strong growth in FY2022E. = - + Positive Neutral Negative The bank is available at 2.4x/2.1x its FY2022E/FY2023E BVPS. The stock has corrected by ~16% from its highs, and we believe valuations are attractive. What has changed in 3R MATRIX We maintain Buy rating on the stock with a revised SOTP-based PT of Rs. 800. Old New ICICI Bank posted strong Q4FY2021 results with core operational performance coming higher than expectations, lower-than-expected slippages, and sequentially improving asset quality RS being key positives. The quarter saw core operating performance above expectations with NII growth at 16.8% y-o-y, led by recovery in loan growth and NIMs improving by 17 bps q-o-q RQ to 3.84%. Strong traction in advances growth was seen with domestic loan growth posting 18% y-o-y growth. Going forward, as the bank looks to build on growth with a focus on a well- RV rated book, pickup in advances, and opex/credit cost will be key support and positives. -

Non-Performing Assets: a Comparison of ICICI Bank and HDFC Bank

Special Issue - 2017 International Journal of Engineering Research & Technology (IJERT) ISSN: 2278-0181 NCIETM - 2017 Conference Proceedings Non-Performing Assets: A Comparison of ICICI Bank and HDFC Bank Dr. Prerna Dawar*Ms. Pooja Sharma** *Dean & Professor Geeta Engineering College , Naultha , Panipat *Assistant Professor, SBD Group of Institutions , Kurukshetra Abstract - Banking in India originated in the last decade of the II. NON PERFORMING ASSETS (NPAs) 18th century. Private sector banks occupy a major part of NPA refers to loans that are in peril of default. The asset banking in India. Private sector banks have a very wide has been categorized as non-performing asset when the network of branches in rural and urban areas. But now a day borrower failed to make principle or interest payment they have diversified their activities to the emerged fields of within 90 days. It has always been a challenge for financial operations like merchant banking, leasing and venture capital etc. Due to increased level of competition private banks have institutions to manage their Non-performing assets because been lending aggressively to the customers which in turn of the dependency on interest payment. NPAs of financial increasing the proportion of Non-Performing Assets institutions increase due to pressure from economy as they (Henceforth, NPAs). Non-performing Asset has been an have to lent aggressively which in turn, reduces their important parameter to analyse of financial performance of capacity to capture all the assets completely. NPAs can be banks as it results in decreasing margin and higher divided into two main categories as follows: provisioning requirements for doubtful debts. -

We Have Started a New Journey, Backed by India's Best

We have started a new journey, backed by India’s best. Investor Presentation May 6, 2020 YES for You Contents Subject Slide No. New Journey 03 - 20 Q4FY20 and FY20 Financial Highlights 21 - 34 Covid-19 Impact 35 – 38 Sustainability & Recognition 39 - 42 YES for You 2 New Journey YES for You A Full Service Commercial Bank 6th Largest Pan India Young & Innovative Differentiated Technology Private Sector Bank* Presence Human Capital Platform Backed by marquee With 1,135 Branches and 1,423 With 22,973 Yes Bankers with Market Leader within Payments shareholders, Total Assets of ATMs # an average age of 33 years, - #1 IMPS Remitter Bank INR 257,827 Crores, with with a vintage of ~8 years for - #1 P2M UPI Transactions Advances of INR 171,443 Top Management & 7 Years for Bank with a ~31% market share Crores (56% Corporate & 44% Senior Management # - AePS a 40% markets share in MSME & Retail) # transaction value ^ Agility + Innovation * Basis Total Assets as on December 31, 2019 # As on March 31, 2020 ^ for FY20 YES for You 4 Unique Ownership Model Under Reconstruction Scheme in March 2020 Shareholding Data as on March 31, 2020 Unique Public and Private 8.0% ownership model backed by SBI 8.0% India’s largest and safest ICICI Bank financial institutions HDFC Ltd. 4.8% Axis Bank 3.6% 48.2% Kotak Bank 2.4% Bandhan Bank 1.9% 1.7% Federal Bank IDFC First Bank Others 21.4% Safety YES for You 5 Robust Governance Structure Backed by newly formed board consisting of eminent and experienced professionals to ensure strictest adherence to Sunil Mehta Prashant Kumar Mahesh Krishnamurti Atul Bheda regulatory and governance norms Non-Executive Chairman Managing Director & CEO Chairman Nomination & Chairman Audit Remuneration Committee, Committee, Non-Executive Director Non-Executive Director R. -

Investor Presentation

INVESTOR PRESENTATION Q4FY18 & FY18 Update Large Bank Growth Phase (FY15-20): Strong Growth with increasing Granularity ✓ 4th Largest# Private Sector Bank with Total Assets Core Retail to Total Advances CASA Ratio 36.3% 36.5% in excess of ` 3 Trillion ` Billion 12.2% 10.8% 28.1% ✓ One of the Fastest Growing Large Bank in India; 9.1% 9.4% 23.1% ▪ CAGR (FY15-18): Advances: 39%; Deposits: 30% ✓ Core Retail Advances grew by 122% CAGR 2,035 2,007 (FY15-18) to constitute 12.2% of Total Advances 1,323 1,429 982 1,117 755 912 ✓ CASA growing at 51% CAGR (FY15-18) to constitute 36.5% of Total Deposits. Advances Deposits # Data as on Dec, 2017 FY15 FY16 FY17 FY18 YES Bank Advances CAGR (FY15-18) of 39% V/s Industry CAGR of 8% resulting in Increasing Market Share ✓ Growth well spread across segments including lending to Market Share Deposits Higher Rated Customers resulting in consistently Improving 1.7% Rating Profile. 1.2% 1.3% 1.0% ✓ Deposits Market Share increased by 70% in 3years to 1.7%; ▪ Capturing Incremental Market Share at 6.9% (FY18) Market Share Advances 2.3% ✓ Advances Market Share more than doubled in 3 years to 2.3%; 1.1% 1.3% 1.7% ▪ Capturing Incremental Market Share at 9.2% (FY18) FY15 FY16 FY17 FY18 2 Large Bank Growth Phase (FY15-20): Sustained Profit Delivery with Best in Class Return Ratios • Amongst TOP 5 Profitable Banks* ` Million Increasing Income and Expanding NIMs 3.5% • One of the lowest C/I ratio among Private banks and 3.4% PSBs* 3.4% 52,238 3.2% • Healthy Return Ratios with RoA > 1.5% and RoE > 41,568 17% consistently -

Building the Finest Quality Large Bank of the World in India

ACTION + QUALITY = GROWTH x SCALE = FINEST QUALITY BIG BANK VISION BUILDING THE FINEST QUALITY LARGE BANK OF THE WORLD IN INDIA QUALITY is a way of life at YES BANK Recognitions from prestigious National and International institutions are a testament to our QUALITY INSTITUTIONAL & BUSINESS EXCELLENCE INTERNATIONAL FORBES GLOBAL FINANCE FINANCE GLOBAL 2000 AWARD CORPORATION Best Bank for SMEs India, Ranked #1,013 Forbes Best Debt Bank in Asia Pacific, 2018 Product Innovationof the Bank of the Year India, Asiamoney Best Banks Global 2000 India's Best Investment Bank - Year’ Award 2017, 2015 Awards, 2019, 2018 Ranked #155 Growth YES Securities, Bali, 2018 International Finance The Banker, London Best Bank in India, Champions Digital Bank of Distinction Corporation’s (IFC Corporate Client Choice Washington’s) Forbes Global 2000 World’s Corporate/ Institutional Bank – Awards, 2017 Largest Public Companies Asia,, London 2016 Global SME Finance Hong Kong Awards June 2018 Best Information Security Initiatives - Global Winner & Best Corporate/ 2018 Institutional Digital Bank - India, New York - 2015 Global Finance Award Global Rank #217 Strongest Bank in India by Balance Fastest Growing Mid-Sized Bank, 2018 Best Implementation of Digital Sheet, Switzerland, 2016, Payments award, 2018 The Banker1000 List Best Mid-Sized Bank, 2016, 2015, Singapore, 2015, Dubai, 2013, 2013, 2012, 2010, 2009 & 2008 Fastest Growing Mid-Sized Bank London Singapore, 2012 Consistent Performer and Best Asset 2018, 2015 Best Managed Bank in India for the Quality - Large -

AT1 Bond Issuances Date Action Taken/ Status 26Th March, 2020 In

AXIS TRUSTEE SERVICES LIMITED Yes Bank Limited – AT1 Bond Issuances Date Action Taken/ Status 26th March, 2020 In view of the lockdown declared in India till 14th April 2020, the Hon’ble High Court vide Order dated 26th March, 2020 directed continuation of all interim orders operating and not already continued by some other courts or authorities to remain in force till 30th April, 2020. 19th March 2020 An application seeking amendment to the Writ Petition by impleading “Central Depository Services (India) Limited [CDSL]” as party Respondent No. 6 was allowed and accordingly the amendments were carried out in the court’s record. 18th March 2020 The matter stood adjourned to 23rd March 2020, in the meantime, the Court has directed that the earlier order passed on 16th March, 2020 viz., “all steps taken by the Respondents shall be subject to further orders passed by this Court” shall continue. 17th March 2020 The hearing commenced and the matter stood adjourned to 18th March 2020. The Court directed for the earlier order to continue upto 18th March, 2020. 16th March, 2020 A fresh Writ Petition (No. 850/2020) has been filed by Axis Trustee Services Limited, as the AT-1 Bond Trustee, in the Hon’ble High Court, Bombay as per instructions of the majority AT-1 Bondholders (ISIN no. INE528G08352 aggregating to Rs.3000 Crs. and INE528G08394 aggregating to Rs.5415 Crores) seeking interalia the following reliefs: a) Writ of Certiorari for examination and squashing/ setting aside the decision of write off of the AT-1 Bonds; b) Writ of Mandamus to reverse the effect of any accounting entries, noting’s, write off, cancellations undertaken pursuant to such decision; and; c) Ad- Interim Reliefs. -

LIC Housing Finance (LICHF)

LIC Housing Finance (LICHF) CMP: | 408 Target: | 400 (-2%) Target Period: 12 months HOLD months August 6, 2021 Uncertainty on stress accretion, low NPA buffer… About the stock: LIC Housing Finance (LICHF) is among the largest HFCs in India with an extensive distribution network of 282 marketing office and 2421 employees. Particulars Ess Total 91% of LICHF’s customers are salaried and 9% are self employed Particulars Amount Retail home loans form 78.3% of the overall book Market Capitalisation | 20605 crore Networth (FY21) | 20521 crore 52 week H/L 542 / 255 Face value | 2 Q1FY22 Results: Subdued overall performance; asset quality concern looming. Update Company Shareholding pattern NII up 4.5% YoY, down 15.3% QoQ, NIMs down 46 bps QoQ to 2.2% (in %) Jun-20 Sep-20 Dec-20 Mar-21 Jun-21 Promoter 40.3 40.3 40.3 40.3 40.3 Higher provisions at | 830 crore, C/I ratio rise impacted PAT at | 153 crore FII 34.3 34.4 29.3 28.2 28.8 Stage 3 assets rose 181 bps from 4.12% to 5.93% & 2.3% was restructured DII 10.6 10.4 15.4 16.8 15.6 Others 14.8 21.9 21.9 14.7 15.3 Price Chart What should investors do? LICHF has given ~57% return over the past year. 600 20000 500 However, we believe a healthy recovery on stressed asset is necessary for better 15000 valuations. 400 300 10000 200 We retain our HOLD rating on the stock 5000 100 Target Price and Valuation: We value LIC Housing at ~0.9 FY23E BV and revise 0 0 our target price for the stock at | 400 per share from | 475 earlier. -

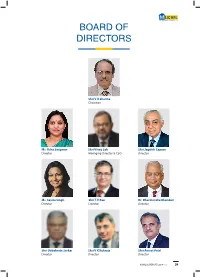

Board of Directors

BOARD OF DIRECTORS Shri V K Sharma Chairman Ms. Usha Sangwan Shri Vinay Sah Shri Jagdish Capoor Director Managing Director & CEO Director Ms. Savita Singh Shri T.V Rao Dr. Dharmendra Bhandari Director Director Director Shri Debabrata Sarkar Shri V K Kukreja Shri Ameet Patel Director Director Director 23 LIC HOUSING FINANCE LIMITED ANNUAL REPORT 2016-17 24 BOARD OF DIRECTORS SHRI V K SHARMA MS. USHA SANGWAN Chairman Director Shri Vijay Kumar Sharma took charge as Chairman, Life Mrs. Usha Sangwan, is the first ever woman Managing Insurance Corporation of India on 16th December, 2016. Prior Director of Life Insurance Corporation of India. She is Post to his taking over as Managing Director, LIC of India, on 1st Graduate in Economics and Post Graduate Diploma holder in November, 2013, he was Managing Director & Chief Executive Human Resource Management and Licentiate from Insurance Officer, LIC Housing Finance Limited (LICHFL), a premiere Institute of India. She joined LIC as Direct Recruit Officer in 1981. housing finance provider in the country with loan portfolio exceeding `83,000 crore. Mrs. Sangwan is the whole time Director of LIC of India, Board Member of General Insurance Corporation of India, Shri Vijay Kumar Sharma, born on 19th December, 1958 is LIC Housing Finance Ltd., Axis Bank, Ambuja Cements Ltd. a post-graduate (M.Sc.) in Botany from Patna University. and Bombay Stock Exchange Ltd., Board Member of LIC Shri Sharma joined LIC as Direct Recruit Officer in 1981 (International) BSC © Bahrain, Kenindia Assurance Co. Ltd., LIC and has grown with the Company since then. During his Card Services Ltd., Member of Governing Council of National stint as Senior Divisional Manager, Karnal, a rural division, Insurance Academy, Member on the Board of Education of had catapulated to Number One position in the country Insurance Institute of India, a Trustee of LIC Golden Jubilee in premium income ahead of all other metro centres. -

For Immediate Publication / Broadcast / Telecast PR / 1253

. For Immediate Publication / Broadcast / Telecast PR / 1253 IDBI Additional Tier - I (AT - I) Bonds oversubscribed Mumbai, October 17, 2014: IDBI Bank’s first Basel III compliant Additional Tier – I (AT - I) bonds amounting to `2,500 crore (`1,500 crore with an option to retain over-subscription upto `1,000 crore) received an overwhelming response and has been fully subscribed prior to the closure date. The issue opened on September 29, 2014. This is the first AT - I bond issuance by a bank in India after RBI modified its Basel III guidelines vide its circular dated September 1, 2014. The issue was competitively priced at a coupon of 10.75% p.a. payable annually. The issue is perpetual in nature with call option after the instrument has run for 10 years. The amount mobilised would be counted as a part of Tier I capital and enhance the capital adequacy of the Bank. The bonds are rated AA- by CRISIL and India Rating. Shri M. S. Raghavan, Chairman & Managing Director, IDBI Bank while commenting on the bond issuance, stated, "IDBI Bank is one of the best known names and has been a pioneer in various initiatives in the banking industry. The resounding success of this bond issue is testimony to this fact. This issuance will pave way for other banks to issue Tier I Bonds in the domestic market and will increase the acceptance of this instrument among the investors.” Axis Bank Ltd., Darashaw & Co. Pvt. Ltd., ICICI Bank Ltd., Trust Investment Advisors Pvt. Ltd. and IDBI Capital Market Services Ltd. -

A Flight to Safety As Indian Banks Navigate Tumultuous Times 2020 Greenwich Leaders: Indian Corporate Banking

A Flight to Safety as Indian Banks Navigate Tumultuous Times 2020 Greenwich Leaders: Indian Corporate Banking The global pandemic is putting economies and financial systems around the world under unprecedented stress. In India, this represents an even sterner test for a banking system that is still reeling from the impact of bank failures prior to the outbreak of COVID-19. Amid a national lockdown and fears of a liquidity crisis, companies in India are joining consumers in shifting business to the largest and presumably safest banks. In this report, we will analyze how the still-unfolding crisis and the many other challenges facing India’s banking sector are affecting the competitive positioning of individual public- and private-sector banks. INDIA’S BANKING WOES PILE UP These key factors converged to create a perfect storm in India’s banking system: J Stress of Public Sector (PSU) Banks’ Balance Sheet With direct intervention from the Indian government, non-performing asset (NPA) ratios had started to decline by 2019, but this is still a work-in-progress for the PSU banking sector. The series of public bank mergers orchestrated by RBI represent a critical step that will make the banking system stronger and more stable. However, navigating sweeping organizational integrations is going to be tough with the epic challenge of the COVID-19 crisis. J NBFC Liquidity Issues The nonbank financial companies (NBFC) crisis, which started in 2018 with the collapse of IL&FS, continues to plague the Indian banking sector. These 10,000+ lightly regulated NBFCs are not only a critical source of credit for small and medium businesses, they have also become intricately linked with the overall banking sector. -

HDFC Life Enters Into a Corporate Agency Arrangement with YES BANK to Offer Life Insurance Solutions to Its Customers

PRESS RELEASE HDFC Life enters into a Corporate Agency arrangement with YES BANK to offer life insurance solutions to its customers Mumbai, September 22, 2020: HDFC Life, one of India’s leading life insurers and YES BANK Limited entered into a Corporate Agency (CA) arrangement. This CA arrangement will enable customers of YES BANK to avail HDFC Life’s wide range of life insurance products which include solutions for protection, savings and investment, retirement and critical illness. Life insurance is an important financial tool for covering the risk of mortality, morbidity and longevity. Every individual with responsibilities needs adequate life insurance to ensure that their family is financially protected in their absence. Thanks to a robust multi-channel distribution set up and strong diversified network, HDFC Life is able to offer life insurance solutions at scale. Speaking on the arrangement Suresh Badami, Executive Director, HDFC Life said, "We are delighted to partner with YES BANK. There is a huge potential for insurance coverage across life & health protection, savings and annuity products in our country. With our bancassurance experience we aim to offer a comprehensive suite of product solutions and best in class servicing, leveraging our investments in technology. We look forward to working closely with the YES BANK team for the benefit of their customers". Rajan Pental, Global Head - Retail Banking, YES BANK said, “We are extremely excited to partner HDFC Life to offer our growing customer base access to HDFC Life’s comprehensive and innovative product suite – through a shared commitment to make a difference in their lives by addressing their unique insurance needs.