17Th ANNUAL REPORT 2013–2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

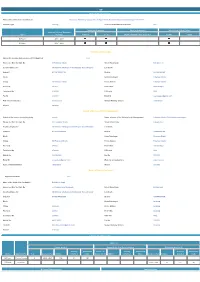

SIF Institutional Information Current Approval Status

SIF Institutional Information Name of the Institution / Institution ID Veer Vijay Pharmacy College Vill Fatehpur Bhado Post Chhutalpur Dist Saharanpur / PCI-2574 Institute Type existing Year of Establishment of Institute 2017 Extension of approval Raise in Admission Introduction of New Course Starting of Course (Academic Course Session) Conduct u/s 12 Number of admissions requested Yes/No Intake B.Pharm 2017 - 2018 D.Pharm 2017 - 2018 Institutional Information Upload the documentary evidence of PCI Approval View House no./ Bld. No./ Apt. No 11 Fatehpur bhado Street/ Road/ Lane Kalsiya road Area/locality/sector vill fatehpur bhado post chhutmalpur dist sahranpur Landmark State/UT UTTAR PRADESH District SAHARANPUR Block Gram Panchayat Fatehpur bhado Village vill fatehpur bhado Police Station Fatehpur bhado Pin Code 247662 Post Office Chhtumalpur Telephone No 2781020 STD code 0132 Fax No 2781030 Email ID [email protected] Web site of institution www.vvpc.in Nearest Railway Station saharanpur Airport sarsawa Details of the Society/Trust/ Management Status of the course conducting body private Name, address of the Society/Trust/ Management Fatehpur bhado Chhutmalpur saharanpur House no./ Bld. No./ Apt. No 011 Fatehpur bhado Street/ Road/ Lane Kalsiya road Area/locality/sector vill fatehpur bhado post chhutmalpur dist sahranpur Landmark State/UT UTTAR PRADESH District SAHARANPUR Block Gram Panchayat Fatehpur Bhado Village Vill Fatehpur Bhado Police Station Fatehpur bhado Pin Code 247662 Post Office Chhutmalpur Telephone No 2781020 STD code 0132 Mobile No 9997486050 Fax No 2781030 Email ID [email protected] Web site of trust/society www.vves.in Nearest Railway Station saharanpur Airport sarsawa Details of Head of Institution Appointment letter View Name of the Head of the Institution Dr Rakesh singh House no./ Bld. -

Statistical Diary, Uttar Pradesh-2020 (English)

ST A TISTICAL DIAR STATISTICAL DIARY UTTAR PRADESH 2020 Y UTT AR PR ADESH 2020 Economic & Statistics Division Economic & Statistics Division State Planning Institute State Planning Institute Planning Department, Uttar Pradesh Planning Department, Uttar Pradesh website-http://updes.up.nic.in website-http://updes.up.nic.in STATISTICAL DIARY UTTAR PRADESH 2020 ECONOMICS AND STATISTICS DIVISION STATE PLANNING INSTITUTE PLANNING DEPARTMENT, UTTAR PRADESH http://updes.up.nic.in OFFICERS & STAFF ASSOCIATED WITH THE PUBLICATION 1. SHRI VIVEK Director Guidance and Supervision 1. SHRI VIKRAMADITYA PANDEY Jt. Director 2. DR(SMT) DIVYA SARIN MEHROTRA Jt. Director 3. SHRI JITENDRA YADAV Dy. Director 3. SMT POONAM Eco. & Stat. Officer 4. SHRI RAJBALI Addl. Stat. Officer (In-charge) Manuscript work 1. Dr. MANJU DIKSHIT Addl. Stat. Officer Scrutiny work 1. SHRI KAUSHLESH KR SHUKLA Addl. Stat. Officer Collection of Data from Local Departments 1. SMT REETA SHRIVASTAVA Addl. Stat. Officer 2. SHRI AWADESH BHARTI Addl. Stat. Officer 3. SHRI SATYENDRA PRASAD TIWARI Addl. Stat. Officer 4. SMT GEETANJALI Addl. Stat. Officer 5. SHRI KAUSHLESH KR SHUKLA Addl. Stat. Officer 6. SMT KIRAN KUMARI Addl. Stat. Officer 7. MS GAYTRI BALA GAUTAM Addl. Stat. Officer 8. SMT KIRAN GUPTA P. V. Operator Graph/Chart, Map & Cover Page Work 1. SHRI SHIV SHANKAR YADAV Chief Artist 2. SHRI RAJENDRA PRASAD MISHRA Senior Artist 3. SHRI SANJAY KUMAR Senior Artist Typing & Other Work 1. SMT NEELIMA TRIPATHI Junior Assistant 2. SMT MALTI Fourth Class CONTENTS S.No. Items Page 1. List of Chapters i 2. List of Tables ii-ix 3. Conversion Factors x 4. Map, Graph/Charts xi-xxiii 5. -

List of Class Wise Ulbs of Uttar Pradesh

List of Class wise ULBs of Uttar Pradesh Classification Nos. Name of Town I Class 50 Moradabad, Meerut, Ghazia bad, Aligarh, Agra, Bareilly , Lucknow , Kanpur , Jhansi, Allahabad , (100,000 & above Population) Gorakhpur & Varanasi (all Nagar Nigam) Saharanpur, Muzaffarnagar, Sambhal, Chandausi, Rampur, Amroha, Hapur, Modinagar, Loni, Bulandshahr , Hathras, Mathura, Firozabad, Etah, Badaun, Pilibhit, Shahjahanpur, Lakhimpur, Sitapur, Hardoi , Unnao, Raebareli, Farrukkhabad, Etawah, Orai, Lalitpur, Banda, Fatehpur, Faizabad, Sultanpur, Bahraich, Gonda, Basti , Deoria, Maunath Bhanjan, Ballia, Jaunpur & Mirzapur (all Nagar Palika Parishad) II Class 56 Deoband, Gangoh, Shamli, Kairana, Khatauli, Kiratpur, Chandpur, Najibabad, Bijnor, Nagina, Sherkot, (50,000 - 99,999 Population) Hasanpur, Mawana, Baraut, Muradnagar, Pilkhuwa, Dadri, Sikandrabad, Jahangirabad, Khurja, Vrindavan, Sikohabad,Tundla, Kasganj, Mainpuri, Sahaswan, Ujhani, Beheri, Faridpur, Bisalpur, Tilhar, Gola Gokarannath, Laharpur, Shahabad, Gangaghat, Kannauj, Chhibramau, Auraiya, Konch, Jalaun, Mauranipur, Rath, Mahoba, Pratapgarh, Nawabganj, Tanda, Nanpara, Balrampur, Mubarakpur, Azamgarh, Ghazipur, Mughalsarai & Bhadohi (all Nagar Palika Parishad) Obra, Renukoot & Pipri (all Nagar Panchayat) III Class 167 Nakur, Kandhla, Afzalgarh, Seohara, Dhampur, Nehtaur, Noorpur, Thakurdwara, Bilari, Bahjoi, Tanda, Bilaspur, (20,000 - 49,999 Population) Suar, Milak, Bachhraon, Dhanaura, Sardhana, Bagpat, Garmukteshwer, Anupshahar, Gulathi, Siana, Dibai, Shikarpur, Atrauli, Khair, Sikandra -

Annexure-V State/Circle Wise List of Post Offices Modernised/Upgraded

State/Circle wise list of Post Offices modernised/upgraded for Automatic Teller Machine (ATM) Annexure-V Sl No. State/UT Circle Office Regional Office Divisional Office Name of Operational Post Office ATMs Pin 1 Andhra Pradesh ANDHRA PRADESH VIJAYAWADA PRAKASAM Addanki SO 523201 2 Andhra Pradesh ANDHRA PRADESH KURNOOL KURNOOL Adoni H.O 518301 3 Andhra Pradesh ANDHRA PRADESH VISAKHAPATNAM AMALAPURAM Amalapuram H.O 533201 4 Andhra Pradesh ANDHRA PRADESH KURNOOL ANANTAPUR Anantapur H.O 515001 5 Andhra Pradesh ANDHRA PRADESH Vijayawada Machilipatnam Avanigadda H.O 521121 6 Andhra Pradesh ANDHRA PRADESH VIJAYAWADA TENALI Bapatla H.O 522101 7 Andhra Pradesh ANDHRA PRADESH Vijayawada Bhimavaram Bhimavaram H.O 534201 8 Andhra Pradesh ANDHRA PRADESH VIJAYAWADA VIJAYAWADA Buckinghampet H.O 520002 9 Andhra Pradesh ANDHRA PRADESH KURNOOL TIRUPATI Chandragiri H.O 517101 10 Andhra Pradesh ANDHRA PRADESH Vijayawada Prakasam Chirala H.O 523155 11 Andhra Pradesh ANDHRA PRADESH KURNOOL CHITTOOR Chittoor H.O 517001 12 Andhra Pradesh ANDHRA PRADESH KURNOOL CUDDAPAH Cuddapah H.O 516001 13 Andhra Pradesh ANDHRA PRADESH VISAKHAPATNAM VISAKHAPATNAM Dabagardens S.O 530020 14 Andhra Pradesh ANDHRA PRADESH KURNOOL HINDUPUR Dharmavaram H.O 515671 15 Andhra Pradesh ANDHRA PRADESH VIJAYAWADA ELURU Eluru H.O 534001 16 Andhra Pradesh ANDHRA PRADESH Vijayawada Gudivada Gudivada H.O 521301 17 Andhra Pradesh ANDHRA PRADESH Vijayawada Gudur Gudur H.O 524101 18 Andhra Pradesh ANDHRA PRADESH KURNOOL ANANTAPUR Guntakal H.O 515801 19 Andhra Pradesh ANDHRA PRADESH VIJAYAWADA -

9 1 2019 10 20 40 Tender2

From Downloaded www.upsrtc.com From Downloaded www.upsrtc.com From Downloaded www.upsrtc.com SAHARANPUR REGION GENERAL CANDIDATES NO. S.NO NAME FATHER TOTAL OBT %DOB CASTE REGI. AMO ADDRESS Adh INETE NCC ITI A Ex Ard MAR RETIR O . MARKS AINE NO. UNT ar R & LEVE Arm h ATK E LEV D 10TH L y Sani ASH EMPL EL Man k RIT OYEE Bal 1 584 SACHIN NATH HANSRAJ 1000 707 70.7 02-Jul-94 General SRE- 200 VILL AND POST- AZAMPUR, DISTT- YES YES YES GOND GOND 26548 AZAMGARH, PIN- 276125 2 585 AMARNATH RAJENDRA 2240 158370.67 09-Dec-89 General SRE- 200 OLD HAAT ROAD NEAR NAHAR TCP YES YES YES PRASAD 30268 TEKANPUR GWALIOR MP , PINCODE -475005 3 586 SACHIN RAMVEER 1100 777 70.64 10-Jul-98 General SRE- 200 Village asdharmai post marauri distt budaun YES YES YES KUMAR SINGH 12356 243631 4 587 MUKESH RAM PAL 1000 706 70.6 14-Sep-94 General SRE- 200 VILL DANIYARPUR POST KOTWA THANA YES YES YES SINGH SINGH 13566 PHARDHAN DISTT LAKHIMPUR KHERI PIFromN 262805 5 588 Ankit Kumar Rakesh Kumar500 353 70.6 14-Jan-95 General SRE- 200 h-63 Amarpur Ghari Basoud Baghpat Pin YES YES YES 11104 Code- 20601 6 589 AMAN PRATEEK 1000 706 70.6 02-Jul-95 General SRE- 200 VILLAGE ADHYANA POST NAKUR DISTT YES YES YES KUMAR KUMAR 9176 SAHARANPUR UP 247342 7 590 KUMAR SHYAM 500 353 70.6 25-Jan-96 General SRE- 200 37/31/28 mahaviran lane mutthiganj YES YES YES PRATEEK KUMAR 9821 allahabad SRIVASTAVA 8 591 NIRMAL JAY CHAND 500 353 70.6 08-Apr-97 General SRE- 200 VILL GHAGHPUR POST DADEVRA DIST YES YES YES KUMAR 27302 SITAPUR PIN 261404 YADAV 9 592 SATYAM RAJENDRA 500 353 70.6 17-Jul-97 -

Statistical Diary, Uttar Pradesh-2017 (English)

STATISTICAL DIARY UTTAR PRADESH 2017 ECONOMICS AND STATISTICS DIVISION STATE PLANNING INSTITUTE PLANNING DEPARTMENT, UTTAR PRADESH http://updes.up.nic.in OFFICERS & STAFF ASSOCIATED WITH THE PUBLICATION 1. SHRI ASHOK KUMAR PANWAR Director 2. SHRI ARVIND KUMAR PANDEY Addl. Director 3. SHRI RAM AVTAR Addl. Director (ADMIN.) Guidance and Supervision 1. SHRI VIKRAMADITYA PANDEY Jt. Director 2. SHRI JITENDRA YADAV Dy. Director 3. SHRI JAIDEEP SINGH Eco. & Stat. Officer 4. SMT MEENAKSHI SRIVASTAVA Addl. Stat. Officer (In-charge) Scrutiny work 1. SMT BEENA SINGH Addl. Stat. Officer 2. SHRI Y. P. SINGH Addl. Stat. Officer 3. SMT NIDHI RASTOGI Addl. Stat. Officer 4. SHRI RAJBALI Addl. Stat. Officer 5. SMT GEETANJALI Asst. Stat. Officer 6. SHRI NIJANAND SINGH Asst. Stat. Officer 7. SMT KIRAN KUMARI Asst. Stat. Officer Manuscript work . Dr. MANJU DIKSHIT Addl. Stat. Officer CONTENTS S.No. Items Page 1. List of Chapters i 2. List of Tables ii-ix 3. Conversion Factors x 4. Map, Graph/Charts xi-xxiii 5. Tables 1-359 6. Explanatory Notes 360- 367 7. Telephone Numbers 368-375 8. E-mail Address 376-380 Chapters List Chapter Description Page No. 0. U.P. at a glance 1-14 1. Area and Population 15-103 2. State Income 104-118 3. Revenue and Expenditure 119-128 4. Rainfall and Temperature 129-132 5. Agriculture 133-199 6. Animal Husbandry 200-202 7. Fisheries 203 8. State Forest 204-205 9. Institutional Finance 206-213 10.Co-operation 214-217 11.Joint stock companies 218-228 12.Labour,Employment and Training 229-238 13.Industry 239-251 14.Electricity 252-261 15.Education 262-276 16.Public Health 277-287 17.Transport and communication 288-295 18.Prices 296-300 19.National savings 301 20.Economic census 302-310 21.Planning 311-323 22.Entertainment 324 23.Social services 325-329 24.Miscellaneous 330-359 I List of Tables Table No. -

Downloaded from सी�नयर �लट OBC डॉ啍यूम�ट वे�र�फकेशन के �लए �त�थ �नधा셍रण स�हत Letter Number 7201 Date 01-10-2019 S.NO

सी�नयर �लट GENERAL डॉ啍यूम�ट वे�र�फकेशन के �लए �त�थ �नधा셍रण स�हत Letter number 7201 date 01-10-2019 S.N Name Fname PAddress i=kad fnukad cqykok frfFk O. GENERAL 1 SUBHAM ARVIND SINGH WARI,HAMIDPUR,KADIPUR,SULTAN 7202 01/10/2019 14-10-2019 SINGH PUR Pin.228145 (UP) 2 Sarvesh shukla raju Chandra Rampur Kotwa lalgopalganj kunda 7203 01/10/2019 14-10-2019 shukla Pratapgarh 3 RISHIKESH PREM KISHORE 4121, Chowk kaseru walan pahar 7204 01/10/2019 14-10-2019 ganj new delhi:110055 4 SHUBHAM RAJENDRA SINGH vill-post- Abhaypur Dist Fatehpur 7205 01/10/2019 14-10-2019 SINGH pin code 212665 5 Vinay tiwari Ram prakash Village/post loyabadshahpur 7206 01/10/2019 14-10-2019 tiwari district etah uttarpradesh 207001 6 SAURABH DIXIT ANIL KUMAR shiv shakti public school durga 7207 01/10/2019 14-10-2019 DIXIT nagar nagla kishan lal tedi bagiya agra 7 MANISH DEV SHIV KUMAR VILL-POST-ABHAYPUR DIST- 7208 01/10/2019 14-10-2019 GAUTAM SINGH DownloadedFATEHPUR UTTAR PRADESH from PIN- 212665 8 KULDIP BRAJESH SHARMA MOH.www.upsrtc.com HANUMAN NAGAR 7209 01/10/2019 14-10-2019 SHARMA FATEHABAD TEHSIL- FATEHABAD DIST- AGRA UP 283111 सी�नयर �लट GENERAL डॉ啍यूम�ट वे�र�फकेशन के �लए �त�थ �नधा셍रण स�हत Letter number 7201 date 01-10-2019 S.N Name Fname PAddress i=kad fnukad cqykok frfFk O. GENERAL 9 SHIVAM HANUMANT VILL GARHI DALEL POST GARHI 7210 01/10/2019 14-10-2019 CHAUHAN SINGH CHAUHAN RAMDHAN DIST ETAWAH PINCODE 206245 10 NISHANT JAGMEHAR Village- Babupura 7211 01/10/2019 14-10-2019 SHARMA SHARMA Post- Nanauta District- Saharanpur Pin- 247452 11 DEEPAK SARVESH KUMAR PURANA -

BK Centers in Saharanpur, India

BK Centers in Saharanpur, India Source: “Centers Finder” service by www.bkgsu.com/centres Centre Area Centre Address Contact Info. Saharanpur Sukh Shanti Dham 0132-2723185 Navin Nagar 6, Navin Nagar 9457047770, 9368298340 Saharanpur-247001 [email protected] Uttar Pradesh Nakur Divya Prakash Bhawan 9258076925 Opp: Block Office [email protected] Banjaran Nakur Saharanpur-247342 Uttar Pradesh Nanauta Khasra No: 1592, Pawan Dham 9457664722, 9411293227 Shiv Mandir, Gangoh Road [email protected] Near Bus Stand, Rampur Nanauta Saharanpur-247452 Uttar Pradesh Rampur Light House 01332- 252912 Maniharan Banjaran Mohalla 9760722711 Khurana Complex rampurmaniharan@bkivv. Rampur Maniharan org Saharanpur-247451 Uttar Pradesh Sarsawa Trimurti Shiv Shakti Dham 9720240840 Near Ambala Road Old Chungi [email protected] Mohan Colony Sarsawa Saharanpur-247232 Uttar Pradesh Deoband Shiv Om Shanti Dham, H.no: 154 01336- 225393 Chowk Near Shiv Chowk 9258076922, 9411079827 Kaysthwada Deoband Saharanpur-247554 Uttar Pradesh Deoband H No: 47 7906809556 Gujjarwada Panchayati Takur Dwara [email protected] Gujjarwda Mohalla Deoband Saharanpur-247554 Uttar Pradesh Nagal Plot No: 832, Anubhuti Dham 9368298340, Gali No:3, Opp: Punjab National Bank 9457047770, 9027848484 Hardev Nagar, Tal: Deoband Nagal Saharanpur-247551 Uttar Pradesh Chhutmalpur Ward No: 2, House Of Subhash Saini 9258076924,9520708004 Kamaalpur Road, Near Sanatan Dharmashala Aryanagar Colony Chhutmalpur Saharanpur-247662 Uttar Pradesh Behat H No:432/24 9368298265 Near Old Water Tank Mahajanan Colony Behat Saharanpur-247121 Uttar Pradesh Gangoh H.no: 210, Near Shiv Chowk 9084589794 Boora Mandi Chhatta Mohalla Gangoh Saharanpur-247341 Uttar Pradesh --------------------------------------------------------------------------------------------------------------------------------------------------------- Source: The “Centres Finder” service by Brahma Kumaris main website Source link ➤ www.brahma-kumaris.com/centres OR www.bkgsu.com/centres OR Scan this QR code with your smartphone camera to visit the link ➤ . -

23 2 2019 11 55 9 Noida 2

from Downloaded www.upsrtc.com From Downloaded www.upsrtc.com GENERAL Father's Obtain Total Date of A EX- ARDH- MRATAK RETIR O SR NO. Name Address Marks% RefNo. Caste NCC ITI Name Marks Marks Birth LEVEL ARMY SAINIK ASHRIT E LEVEL ARVIND RAMCHAN DEEN NAGARIYA TIMANPUR MAINPRUI NOIDA- 802 KUMAR DRA SINGH SHARIFPUR UP 205265 368 500 73.6 26.Mai.97 9534 General YES MATA VILL BIRNAI POST BAIRIBISA THANA VISWAS PRASAD GOPIGANJ DIST S R N BHADOHI PIN NOIDA- 803 UPADHYAY UPADHYAY 221303 368 500 73.6 20.Jun.97 9416 General YES ANKIT SUSHEEL VILLAGE NAGLA CHHATTU POST URESAR NOIDA- 804 KUMAR KUMAR THANA EKA DIST FIROZABAD UP 368 500 73.6 10.Jul.97 4582 General YES RAVINDRA PRATAP JASWANT VILL AND POST AKOHARI THANA NOIDA- 805 SINGH SINGH PARASPUR DISTT GONDA UP PIN 271504 368 500 73.6 20.Jul.97 10142 General YES Girraj Kamalesh Vill- Saray Raj Nagar Post- Jalesar Distt- NOIDA- 806 Kishor Chandra Etah 368 500 73.6 04.Aug.97 9844 General YES RAKESH VILLAGE AND POST SHAHPUR BANGAWA From PRANJAL KUMAR TEHSIL ALAPUR THANA ALAPUR DISTRICT NOIDA- 807 SINGH SINGH AMBEDKAR NAGAR PIN 224181 368 500 73.6 02.Dez.97 5952 General YES ROHAN YOGENDRA VILLAGE MAJURI KHAS POST NEWADA PS NOIDA- 808 SINGH SINGH GAGAHA GORAKHPUR 368 500 73.6 05.Jul.98 2405 General YES PINTOO V.PO DHIKANA BARAUT , BAGHPAT UTTAR NOIDA- 809 KUMAR RAMPAL PRADESH 250611 368 500 73.6 10.Jul.98 12573 General YES SANDEEP GULVIR VPO THORA TEH JEWAR DISTT G B NAGAR NOIDA- 810 SHARMA SHARMA 203155 368 500 73.6 25.Nov.98 11743 General YES LANKESH RAMPURA SIHUA MAMAN HIMATPUR NOIDA- 811 HIMANSHU -

Basic Information of Urban Local Bodies – Uttar Pradesh

BASIC INFORMATION OF URBAN LOCAL BODIES – UTTAR PRADESH As per 2006 As per 2001 Census Election Name of S. Growth Municipality/ Area No. of No. Class House- Total Rate Sex No. of Corporation (Sq. Male Female SC ST (SC+ ST) Women Rate Rate hold Population (1991- Ratio Wards km.) Density Membe rs 2001) Literacy 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 I Saharanpur Division 1 Saharanpur District 1 Saharanpur (NPP) I 25.75 76430 455754 241508 214246 39491 13 39504 21.55 176 99 887 72.31 55 20 2 Deoband (NPP) II 7.90 12174 81641 45511 36130 3515 - 3515 23.31 10334 794 65.20 25 10 3 Gangoh (NPP) II 6.00 7149 53913 29785 24128 3157 - 3157 30.86 8986 810 47.47 25 9 4 Nakur (NPP) III 17.98 3084 20715 10865 9850 2866 - 2866 36.44 1152 907 64.89 25 9 5 Sarsawan (NPP) IV 19.04 2772 16801 9016 7785 2854 26 2880 35.67 882 863 74.91 25 10 6 Rampur Maniharan (NP) III 1.52 3444 24844 13258 11586 5280 - 5280 17.28 16563 874 63.49 15 5 7 Ambehta (NP) IV 1.00 1739 13130 6920 6210 1377 - 1377 27.51 13130 897 51.11 12 4 8 Titron (NP) IV 0.98 1392 10501 5618 4883 2202 - 2202 30.53 10715 869 54.55 11 4 9 Nanauta (NP) IV 4.00 2503 16972 8970 8002 965 - 965 30.62 4243 892 60.68 13 5 10 Behat (NP) IV 1.56 2425 17162 9190 7972 1656 - 1656 17.80 11001 867 60.51 13 5 11 Chilkana Sultanpur (NP) IV 0.37 2380 16115 8615 7500 2237 - 2237 27.42 43554 871 51.74 13 5 86.1 115492 727548 389256 338292 65600 39 65639 23.38 8451 869 67.69 232 28 2 Muzaffarnagar District 12 Muzaffarnagar (NPP) I 12.05 50133 316729 167397 149332 22217 41 22258 27.19 2533 892 72.29 45 16 13 Shamli -

Final Population Totals, Series-10, Uttar Pradesh

Census of India 2001 Series 10 : Uttar Pradesh FINAL POPULATION TOTALS (St:at:e, Dist:rict:, Tehsil and Town) Ranbir Singh 0' the Indian Administrative Service Direct:or of Census Operat:ions, Uttar Pradesh Lucknow Website: http://www.censusindia.net/ © All rights reserved with Government of India Data Product Number 09-004-Cen-Book Preface The final population data presented in this publication is based on the processing and tabulation of actual data captured from each and every 202 million household schedules. In the past censuses the final population totals and their basic characteristics at the lowest geographical levels popularly known as the village/town Pnmary Census Abstract was compiled manually. The generation of Primary Census Abstract for the Census 2001 is a fully computerized exercise starting from the automatic capture of data from the Household Schedule through scanning to the compilation of Primary Census Abstract. This publication titled "Final Population Totals" IS only a prelude to the Primary Census Abstract. The publication, which has only one table, presents data on the total population, the Scheduled Castes population and the Scheduled Tribes population by sex at the state, district, tehsil and town levels. The village-wise data is being made available in electronic format. It is expected to be a useful ready reference document for data users who are only interested to know the basic population totals. This publication is brought out by Office of the Registrar General, India (ORGI) centrally. I am happy to acknowledge the dedicated efforts of Dr Ranbir Singh, Director of Census Operations, Uttar Pradesh and his team and my colleagues in the ORGI In bringing out this publication. -

State-Wise Length of National Highways (NH) in India As on 30.11.2018 1/31

State-wise length of National Highways (NH) in India as on 30.11.2018 1/31 Sl. NH No. State / U.T. Route Length No. (km) Andhra Pradesh 1 16 5, 6, 60 & 217 Orissa-Anandapuram Pendurthi, Anakapalli, Rajahmundary, Deverapalli, Gondugolanu,Vijayawada, Nellore-Tamil 1,024.1 Nadu Border // Anandapuramu-Visakhapatnam-Anakapalli 2 216 214, 214A Junction with NH-16 near Kathipudi - Kakinada, Machilipatnam - junction with NH-16 near Ongole 391.3 3 216A 16 GQ Rajamahendravaram - tanuku - Tadepalli gudem- Gundugolanu 120.7 4 516C The highway starting from its junction with NH-16 at Sabbavaram bypass connecting Amruthapuram, Narava, 12.7 Sathivani palem, Gopalpatanam rural and terminating near Sheelanagar in the State of Andhra Pradesh. 5 516D Junction with NH 16 near Deverapalli Bypass - Golladgudem, Gopalapuram, Jaganathapuram, Atchyutapuram, 57.7 Koyyalgudem, Bayyanagudem, Seetampeta, Narasannapalem, Jangareddigudam, Vegavaram, Taduvai, Darbhagudem- Jeelugumilli near Andhra Pradesh/Telengana border. 6 516 E junction with NH No. 16 near Rajamundry - Bhupatiapalem Road (connecting SH-38 near Rampachodavaram), 406.2 Koyyuru, Chintapalli, Lambasingi, Paderu, Aruku, Bowadara, Tadipudi - junction of NH-26 at Vizianagaram 7 716 205 Tamil Nadu Border-Reniguta, Mamanduru, Settigunta, Koduru, Pullampeta, Rajampet, Nandalur, Madhavaram, 237.8 Vonimitta, Bhakarapet, Kadapa (Cuddapah), Kuarunipalli, Vellore, Thapetla, Kothapalli, Chidipirala, Pandillapalle, Thiparulu, Yeragunttla, Nidizivve, Chillamakuru , and terminating at its junction with NH-67 near Muddanuru 8 716A Junction with NH-716 near Puttur connecting , Narayana Vanam, Thumburu, Koppedu, Harijan, Vada, Ramagiri, 42.6 Krishnapuram, Utthukottai -Tamil Nadu. 9 716B The highway starting from its junction with NH-16 near Thachur in the state of Tamil Nadu and terminating at its 20.0 junction with NH-40 near Chittoor in the state of Andhra Pradesh.