Annual 2016 Retail Foods Taiwan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hypermarket Format: Any Future Or a Real Need to Be Changed? an Empirical Study of the French, Spanish and Italian Markets

Hypermarket Format: Any Future or a Real Need to Be Changed? An Empirical Study of the French, Spanish and Italian markets. Rozenn PERRIGOT ESC Rennes School of Business CREM UMR CNRS 6211 2, rue Robert d’Arbrissel CS 76522 35065 Rennes Cedex FRANCE [email protected] Gérard CLIQUET Institute of Management of Rennes (IGR-IAE) University of Rennes 1 CREM UMR CNRS 6211 11, rue Jean Macé CS 70803 35708 Rennes Cedex FRANCE [email protected] 5th International Marketing Trends Congress, Venice (ITALY), 20-21 of January 2006 Hypermarket Format: Any Future or a Real Need to Be Changed? An Empirical Study of the French, Spanish and Italian markets. Abstract: The hypermarket appeared first in France at the beginning of the sixties as a synthesis of the main features of modern retailing. But in France, the decline of this retail format seems to have begun and Spain could follow quickly. In the same time, the German hard-discounters continue their invasion. According to the retail life cycle theory, this paper displays curves to demonstrate the evolution of this retail concept in France, Spain and Italy and tries to evoke some managerial and strategic issues. The retail wheel seems to go on turning! Keywords: France, hypermarket, Italy, retail life cycle, Spain, wheel of retailing. 1. Introduction The history of modern retailing began more than 150 years ago. The first retailing formats began to outcompete the traditional small and independent shops. For instance, many department stores followed several decades later by variety stores appeared in Europe (France, UK, Germany and Italy) but also in the United States and Japan. -

Serving Customers in Diverse Ways Products Ecommerce

eCommerce Products Truffles Donckels brand from Belgium is available One of the reasons behind Walmart Brazil’s in both Sam’s Club and Walmart. Additionally, success is their ability to leverage scale and Walmart Brazil imports Hunts Tomato Sauce, expertise to be one of the top leaders among online Cheesecake Factory and Samuel Adams beer to retailers in market share and provide low, Sam’s Club stores. competitive prices. In addition, walmart.com.br is able to present a huge variety and assortment of Borges Olive Oil and McCain French Fries are part general merchandise, usually larger than brick and of the portfolio for Walmart Brazil. As of 2015, the Serving Customers mortar operations. Brazilian consumer can buy children’s clothing Child of Mine, developed by Carter’s in the United In Diverse Ways States, exclusively at Walmart. History “Orbit” chewing gum, Starburst and “5” gum, from Walmart Brazil began its Wrigley (Mars, Incorporated), was available to operations in 1995, with its Economic Impact Brazil in 2014, exclusively at Walmart stores in all headquarters located in Barueri, regions. São Paulo. Walmart Brazil Over the past 12 years, Walmart Brazil’s Producer’s operates across 18 states and the Club has grown to 9,221 households in 18 Brazilian Schwinn, a traditional bike brand in USA, now offers Federal District, serving 1 million states and the Federal District. It offers these Mountain, Dakota, Colorado and Eagle bike models customers each day with suppliers access to Walmart Brazil stores to sell in Brazil through Walmart hypermarket formats. hypermarkets, supermarkets, cash their products. -

RSCI Pioneered the Hypermarket Concept in the Philippines Through Shopwise

Rustan Supercenters, Inc. (RSCI), a member of the Rustan Group of Companies, was founded in 1998 at the height of the Asian Economic Crisis. It was the first Rustan Company to take in outside investors. It was also the Rustan Group’s first major foray into the discount retailing segment through an adapted European style hypermarket. RSCI pioneered the hypermarket concept in the Philippines through Shopwise. Armed with the vision of providing Quality for All, the Company sought to make the renowned Rustan’s quality accessible to all, especially the middle and working class. Its mission is to create a chain of supercenters or hypermarkets which is the needs of the Filipino family. Rustan’s decision to diversify into hypermarkets was borne out of manifest opportunities brought about by fundamental changes that are taking place in the Philippine market: a burgeoning middle class; increasing value consciousness across various income levels; and new geographical market opportunities that are best served through discount retailing operations. RSCI developed and opened the first hypermarket in the country in November 29, 1998 in Alabang. From 40 employees, it now employs more than 6,000 employees The Company has attained much success since its inception. From 40 employees, it now employs more than 6,000 employees. From sales of zero, the Company registered sales of over P17B in fiscal year 2012-2013. From one hypermarket in Filinvest Alabang, it has now grown to 46 stores covering multiple retail formats, namely, hypermarkets, upscale supermarkets, and neighborhood grocery stores. November 2006 marked yet another milestone for RSCI when it has acquired the 21 Rustan’s stores and food services operations under an Asset Lease Agreement. -

2019 Philippines Food Retail Sectoral Report

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 7/8/2019 GAIN Report Number: 1913 Philippines Retail Foods 2019 Food Retail Sectoral Report Approved By: Ryan Bedford Prepared By: Joycelyn Claridades Rubio Report Highlights: The Philippine food retail sector continues to grow, providing opportunities for increased exports of U.S. high-value food and beverages. The food retail industry sold a record $47.4 billion in 2018, and Post forecasts sales in 2019 at nearly $50 billion. Driven by rising incomes, a growing population, and a strong preference for American brands, the Philippines imported $1.09 billion of U.S. consumer-oriented products in 2018. Post expects U.S. exports in this sector to grow further in 2019, reaching an all-time high of $1.2 billion. Market Fact Sheet: Philippines With a population of 105.9 million and decreasing farmlands, the Philippines is dependent on food imports. In 2018, Philippine imports of high-value food products from the United States reached $1.09 billion, making the United States the largest supplier for high-value, consumer-oriented food and beverage products. Post expects this to continue in 2019, with exports forecast to grow 10 percent to $1.2 billion. The Philippines continues to be one of the fastest-growing economies in Asia. With a growing middle class and a large, young population, the Philippine economy is rooted in strong consumer demand, boosted by rising incomes and overseas remittances. Per capita gross income and consumer expenditures saw strong gains from 2012 to 2018. -

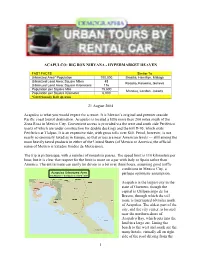

1 Acapulco: Big Box Nirvana

ACAPULCO: BIG BOX NIRVANA - HYPERMARKET HEAVEN FAST FACTS Similar To Urbanized Area* Population 700,000 Brasilia, Hamilton, Malaga Urbanized Land Area: Square Miles 45 Rosario, Kelowna, Geneva Urbanized Land Area: Square Kilometers 116 Population per Square Mile 15,600 Manaus, London, Jakarta Population per Square Kilometer 6,000 *Continuously built up area 21 August 2004 Acapulco is what you would expect for a resort. It is Mexico’s original and premier seaside Pacific coast tourist destination. Acapulco is located a little more than 200 miles south of the Zona Rosa in Mexico City. Convenient access is provided via the west and south side Periferico (parts of which are under construction for double decking) and the toll D-95, which exits Periferico at Tlalpan. It is an expensive ride, with gross tolls over $40. Petrol, however, is not nearly so onerously taxed as in Europe, so that prices are near American levels --- still among the most heavily taxed products in either of the United States (of Mexico or America, the official name of Mexico is Estados Unidos de Mexicanos). The trip is picturesque, with a number of mountain passes. The speed limit is 110 kilometers per hour, but it is clear that respect for the limit is more on a par with Italy or Spain rather than America. The entire route can easily be driven in a bit over three hours, assuming good traffic conditions in Mexico City, a Acapulco Urbanized Area perhaps optimistic assumption. MICROSOFT “STREETS & TRIPS” MAP Acapulco is the largest city in the state of Guerrero, though the capital is Chilpancingo de los Bravos, through which the toll route is interrupted 60 miles north of Acapulco. -

Country Company Contact Phone/Fax E-Mail Website Products of Interest/Comments Nature of Business SUMMER FANCY FOOD SHOW BUYERS

SUMMER FANCY FOOD SHOW BUYERS MISSION June 28 July 1, 2003 Products of Nature of Country Company Contact Phone/Fax E-mail Website Interest/Comments Business Bermuda Lindos Market Albert Charles (441) 236-5623 (441) [email protected] www.lindos.bm organic, pates, dips, deli meats Grocery store Dale 236-4055 France Lafayette Gourmet Nadia Gharbi (33) 140 23 52 46 (33) lafayette.gourmet@l Soft drinks, sodas, water, cereals, sweets, and and 142 80 15 67 (F) ibertysurf.fr confectionary, authentic US products, all Eric Bur (importer) Cesar Barrachin type of fast food and snack Germany St. Jozef Import/Export Heinrich (49)2327 9474 190 [email protected] www.stjozef.de California wines, biscuits and cakes and import/export with grocery Schurmeier (49) 2327 9474 40 sweets, spice and herbal sauces, other retail Hong Kong City Super Ltd Fenix Nathalie Poonis (852) 2956-2668 (852) nathalie@citysuper. www.citysuper.com. Gourmet supermarket Group Chen 2956 0336 com.hk hk Poland PHW Levant Aleksandra Zola- (48) 61 8425 940 (T) [email protected] www.levant.pl Canned fruits, vegetables, and dried Import/Export Tur (48) 61 8429 329 (F) fruits Singapore Indoguna (S) Pte Ltd Thomas Ng (65) 6755 0330 (T) thomas@indoguna. www.indoguna.com Retail, food service: Seafood, deli, & Fresh & Frozen (65) 6755 9522 (F) com.sg dairy products distribution Singapore Shin Chin Distributors Lim Teng Fuh (65)6298 9595 (T) (65) [email protected] Mayonnaise, canned soups and other Distribution Pte Ltd 6296 5885 (F) om.sg food products for mass market Singapore Auric Pacific Richard Wee (65) 6867 9100 (T) [email protected] supermarket and food services: productsFood Manufacturing, Marketing Pte Ltd Kheng Hin (65)6261 7678 (F) om.sg range Marketing, & Distribution UK GFT Retail Ltd. -

Hypermarket Lessons for New Zealand a Report to the Commerce Commission of New Zealand

Hypermarket lessons for New Zealand A report to the Commerce Commission of New Zealand September 2007 Coriolis Research Ltd. is a strategic market research firm founded in 1997 and based in Auckland, New Zealand. Coriolis primarily works with clients in the food and fast moving consumer goods supply chain, from primary producers to retailers. In addition to working with clients, Coriolis regularly produces reports on current industry topics. The coriolis force, named for French physicist Gaspard Coriolis (1792-1843), may be seen on a large scale in the movement of winds and ocean currents on the rotating earth. It dominates weather patterns, producing the counterclockwise flow observed around low-pressure zones in the Northern Hemisphere and the clockwise flow around such zones in the Southern Hemisphere. It is the result of a centripetal force on a mass moving with a velocity radially outward in a rotating plane. In market research it means understanding the big picture before you get into the details. PO BOX 10 202, Mt. Eden, Auckland 1030, New Zealand Tel: +64 9 623 1848; Fax: +64 9 353 1515; email: [email protected] www.coriolisresearch.com PROJECT BACKGROUND This project has the following background − In June of 2006, Coriolis research published a company newsletter (Chart Watch Q2 2006): − see http://www.coriolisresearch.com/newsletter/coriolis_chartwatch_2006Q2.html − This discussed the planned opening of the first The Warehouse Extra hypermarket in New Zealand; a follow up Part 2 was published following the opening of the store. This newsletter was targeted at our client base (FMCG manufacturers and retailers in New Zealand). -

Understanding the Beauty and Health Retailers in Hong Kong

UNDERSTANDING THE BEAUTY AND HEALTH RETAILERS IN HONG KONG CONTENTS Overview of Distribution Channels Online Retailer in Hong Kong and Macau 04 1. Hong Kong Retailers’ Own Website 22 Brick-and-mortar Retail Stores in Hong Kong 2. E-commerce Platform in Hong Kong 23 1. Department Stores 06 3. Cross-border E-commerce Platform in China 23 2. Beauty Specialty Stores 10 3. Pharmacy Stores 13 Hong Kong Beauty and Health Trade Events 26 4. Supermarkets 14 Austrade Contacts 27 5. Multi-brand Shops 16 6. Health and Organic Stores 19 7. Australian Brand Stores 21 Disclaimer Copyright © Commonwealth of Australia 2019 This report has been prepared by the Commonwealth of Australia represented by the Australian Trade and Investment Commission (Austrade). The report is a general overview and is not intended to The material in this document is licensed under a Creative Commons provide exhaustive coverage of the topic. The information is made Attribution – 4.0 International licence, with the exception of: available on the understanding that the Commonwealth of Australia is • the Commonwealth Coat of Arms not providing professional advice. • the Australian Trade and Investment Commission’s logo While care has been taken to ensure the information in this report • any third party material is accurate, the Commonwealth does not accept any liability for any • any material protected by a trade mark loss arising from reliance on the information, or from any error or • any images and photographs. omission, in the report. More information on this CC BY licence is set out at the creative Any person relying on this information does so at their own risk. -

When Is the Best Time to Go to Hong Kong?

Page 1 of 98 Chris’ Copyrights @ 2011 When Is The Best Time To Go To Hong Kong? Winter Season (December - March) is the most relaxing and comfortable time to go to Hong Kong but besides the weather, there's little else to do since the "Sale Season" occurs during Summer. There are some sales during Christmas & Chinese New Year but 90% of the clothes are for winter. Hong Kong can get very foggy during winter, as such, visit to the Peak is a hit-or-miss affair. A foggy bird's eye view of HK isn't really nice. Summer Season (May - October) is similar to Manila's weather, very hot but moving around in Hong Kong can get extra uncomfortable because of the high humidity which gives the "sticky" feeling. Hong Kong's rainy season also falls on their summer, July & August has the highest rainfall count and the typhoons also arrive in these months. The Sale / Shopping Festival is from the start of July to the start of September. If the sky is clear, the view from the Peak is great. Avoid going to Hong Kong when there are large-scale exhibitions or ongoing tournaments like the Hong Kong Sevens Rugby Tournament because hotel prices will be significantly higher. CUSTOMS & DUTY FREE ALLOWANCES & RESTRICTIONS • Currency - No restrictions • Tobacco - 19 cigarettes or 1 cigar or 25 grams of other manufactured tobacco • Liquor - 1 bottle of wine or spirits • Perfume - 60ml of perfume & 250 ml of eau de toilette • Cameras - No restrictions • Film - Reasonable for personal use • Gifts - Reasonable amount • Agricultural Items - Refer to consulate Note: • If arriving from Macau, duty-free imports for Macau residents are limited to half the above cigarette, cigar & tobacco allowance • Aircraft crew & passengers in direct transit via Hong Kong are limited to 20 cigarettes or 57 grams of pipe tobacco. -

Chartered Secretaries American Express Credit Cards

Chartered Secretaries American Express Credit Cards Chartered Secretaries American Express® Platinum Credit Card and Chartered Secretaries American Express®Gold Credit Card are two co-branded cards that have been created in collaboration with The Hong Kong Institute of Chartered Secretaries (HKICS) and have been specifically designed to recognise and benefit our members. As a Member/Graduate/Student of HKICS, you are cordially invited to become a Chartered Secretaries American Express Platinum or Gold Card Cardmember. This card provides a highly convenient way to pay for HKICS membership fees, CPD events and seminars, examination fees and other fees. Application forms Exclusive privileges Merchants List Application forms Chartered Secretaries American Express Platinum Credit Card application form Chartered Secretaries American Express Gold Credit Card application form Application with required documents should be sent to: American Express International Inc Attn: New Accounts GPO Box 11250 Hong Kong Note: 1. Terms and conditions apply to the above offers and privileges. Please visit www.americanexpress.com.hk to learn more. 2. The Chartered Secretaries American Express co-branded Card is a privilege from HKICS. All Credit Card applicationapprovals will be at the sole discretion of American Express International Inc 3. For any enquiries, please call 2277 1370 Back to top Exclusive privileges: Chartered Secretaries American Express® Platinum Credit Card Half annualfee waiver saving you HK$800 a year Generous welcome offers including HK$500 Lane Crawford or Esso Synergy Fuel Cash Voucher, plus 10X Membership Rewards points in the first 3 months, up to 300,000 points Up to HK$500 travel package discount coupon when you purchasing travel packages from Farrington American Express Travel Services Ltd. -

Hyper Market Industry in Dubai – an Evaluation Using Ahp Technique

50____________________________________________________________ iJAMT HYPER MARKET INDUSTRY IN DUBAI – AN EVALUATION USING AHP TECHNIQUE M. Hemalatha, National Institute of Technology, Trichy V. J. Sivakumar, National Institute of Technology, Trichy Abstract Among all retail formats hypermarket is growing very fast in UAE that is at the rate of 150 percent. The major players in this sector are Carrefour, Spinney’s, United, Choithram and Lulu. The focus of the problem is selecting a best hypermarket among the existing operators of Dubai and for which we used seven major criteria for evaluating the hypermarkets such as product availability and variety, market coverage, channel density, customer density, nationality served, facilities and services and customer spending pattern. We used Analytic hierarchy process (AHP), developed by Thomas saaty (1980) to provide a simple but theoretically sound multiple criteria methodology for evaluating the alternatives. Keywords Hyper Market, Analytic hierarchy process, Multiple Criteria Introduction about UAE Hyper Market Industry The retail sector in the United Arab Emirates (U.A.E.) continues to grow and develop a process that began in earnest nearly 10 years ago. Annually, many new state of the art stores are added to the country’s retail map, creating continuous competition among the major retailers. The new stores match Western retail establishments in size and variety. The estimated annual value of the U.A.E. retail market is $2.5 billion. The estimated average annual growth in retail sales is 5-10 percent. First year retail establishments report higher growth rates than those claimed by established firms. Foods sold in retail outlets consist 75-80 percent of imported consumer-ready products, and 20-25 percent of locally processed foods. -

Climate & Weather the Climate of China Is Extremely Diverse. Tropical

CHINA - COUNTRY FACT SHEET GENERAL INFORMATION Climate & Weather The climate of China is Time Zone China Standard Time extremely diverse. Tropical (UTC+8). in the south to subarctic in the north. Language The official language of Currency Renminbi (RMB) (yuan) (¥) China is Mandarin. However, (CNY). there are over 400 local dialects. Religion Confucianism, Taoism and International + 86 Buddhism are the three Dialing Code major religions in China. Population 1,376,049,000 people Internet Domain cn, .中國[ .中国 Political System Unitary Parliamentary Emergency Police (Calling): 110 Republic. Numbers Police (Text message): 12110 First-aid Ambulance: 120 Fire: 119 Traffic Accidents: 122 SOS in Water: 12395 Electricity The China power grid Capital City Beijing (Chinese: 北京; operates at 220 volts and 50 pinyin: Beijing; postal: Hz (cycles per second). Peking). What documents Documents Required: Please confirm The Company finance team required to open 1. Passport how salaries are that you are working for a local Bank 2. Evidence of residence in paid? (eg monthly will transfer the money to Account? China directly into a the bank account online or Can this be done 3. First deposit varying Bank Account) by other method after you prior to arrival? from $ 100 to $ 500 provide your bank account 4. Residence permit and information to the company. (or) your visa with an official translation in Chinese might also be requested. 1 GENERAL INFORMATION Prior to arrival: No, you cannot set up a local bank account prior to arrival. The bank needs to check the information on the Passport and take a photo for record in the bank system.