Dr. Ivan Miestchovich Economic Outlook & Real Estate Forecast For

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Energy Star Qualified Buildings

1 ENERGY STAR® Qualified Buildings As of 1-1-03 Building Address City State Alabama 10044 3535 Colonnade Parkway Birmingham AL Bellsouth City Center 600 N 19th St. Birmingham AL Arkansas 598 John L. McClellan Memorial Veterans Hospital 4300 West 7th Street Little Rock AR Arizona 24th at Camelback 2375 E Camelback Phoenix AZ Phoenix Federal Courthouse -AZ0052ZZ 230 N. First Ave. Phoenix AZ 649 N. Arizona VA Health Care System - Prescott 500 Highway 89 North Prescott AZ America West Airlines Corporate Headquarters 111 W. Rio Salado Pkwy. Tempe AZ Tempe, AZ - Branch 83 2032 West Fourth Street Tempe AZ 678 Southern Arizona VA Health Care System-Tucson 3601 South 6th Avenue Tucson AZ Federal Building 300 West Congress Tucson AZ Holualoa Centre East 7810-7840 East Broadway Tucson AZ Holualoa Corporate Center 7750 East Broadway Tucson AZ Thomas O' Price Service Center Building #1 4004 S. Park Ave. Tucson AZ California Agoura Westlake 31355 31355 Oak Crest Drive Agoura CA Agoura Westlake 31365 31365 Oak Crest Drive Agoura CA Agoura Westlake 4373 4373 Park Terrace Dr Agoura CA Stadium Centre 2099 S. State College Anaheim CA Team Disney Anaheim 700 West Ball Road Anaheim CA Anahiem City Centre 222 S Harbor Blvd. Anahiem CA 91 Freeway Business Center 17100 Poineer Blvd. Artesia CA California Twin Towers 4900 California Ave. Bakersfield CA Parkway Center 4200 Truxton Bakersfield CA Building 69 1 Cyclotron Rd. Berkeley CA 120 Spalding 120 Spalding Dr. Beverly Hills CA 8383 Wilshire 8383 Wilshire Blvd. Beverly Hills CA 9100 9100 Wilshire Blvd. Beverly Hills CA 9665 Wilshire 9665 Wilshire Blvd. -

HVS Hotel Market Intelligence Report: New Orleans

HVS Hotel Market Intelligence Report: New Orleans February 6, 2012 By Adam R. Lair The blown‐out windows along the façade of New Orleans’ Hyatt Regency hotel were one of Summary the unforgettable stamps of Hurricane Katrina’s descent on the city in 2005. Nearly 200 of the city’s hotels were shuttered in the wake of the storm. Biotechnology, conventions, The hotel industry in New tourism, lodging and other fixtures of the New Orleans economy mounted a modest recovery Orleans has struggled to over the next few years, only to be knocked back with successive blows, first from the regain its footing in the national recession in 2008/09, next by the Deepwater Horizon oil spill in 2010. It’s fair to say years since Hurricane the trials of the past half‐decade have left some doubt about the viability of the city’s hotel industry over the Katrina, but new data long haul. But new developments and positive recent economic signs encourage a fresh look. suggest a recovery is underway. Commercial Developments Following the devastation wreaked by Katrina, much of New Orleans’ economic infrastructure needed to be 1 Comments rebuilt, literally from the ground up. Private and public investment in recovery construction and new development helped keep unemployment in the market well below the national average through the recession. As a result of this run of new development, biomedical research and medical care facilities are poised to be pistons of the city’s economic engine. Four new projects are located in the city’s Biomedical Corridor, adjacent to the CBD. -

Propeller Club of the U.S. Port of New Orleans Membership Roster - 2015

Propeller Club of the U.S. Port of New Orleans Membership Roster - 2015 FIRST LAST COMPANY ADDRESS E-MAIL OFFICE PHONE Charlie Andrews, Jr. 11117 Winchester Park Drive New Orleans, LA 70128 504-227-7009 William S. App, Jr. J.W. Allen & Co., Inc. 200 Crofton Rd., Box 34 Kenner, LA 70065 [email protected] 504-464-0181.111 William Ayers 822 N. Austin St. Seguin, TX 78155 830-372-2244 Jimmy Baldwin Coastal Cargo, Inc. 1555 Poydras St., Suite 1600 New Orleans, LA 70112 [email protected] 504-587-1125 William J. Baraldi Buck Kreihs Marine Repair, LLC PO Box 53305 New Orleans, LA 70153 [email protected] 504-524-7681 Robert R. Barkerding, Jr. Admiral Security Services, Inc. 1010 Common St., Suite 2970 New Orleans, LA 70112 [email protected] 504-831-1408 Frank J. Basile Entech Associates PO Box 1470 Houma, LA 70361-1470 [email protected] 985-868-5524 Perry Beebe Perry Beebe & Associates, LLC 141 Hwy. 22 E, Unit 4A Madisonville, LA 70447 [email protected] 504-400-1713 Don Belovin Bay Diesel Corp. 3742 Cook Blvd. Chesapeake, VA 23323 [email protected] 757-485-0075 Julie Biggers All Scrap Metals 7 Veterans Blvd. Kenner,LA 70062 [email protected] 504-471-0241 Richard E. Boyer Pacific-Gulf Marine, Inc. 401 Whitney Ave., Ste. 511 Gretna, LA 70056 [email protected] 504-362-8121 Ron Branch Louisiana Maritime Assoc. 3939 N. Causeway Blvd., Suite 102 Metairie, LA 70002 [email protected] 504-833-4190 Conrad Breit C. Breit Marine Services, LLC 111 Acadia Ln Destrehan, LA 70047 [email protected] 504-913-7960 Hjalmar E. -

Annual Report

COUNCIL ON FOREIGN RELATIONS ANNUAL REPORT July 1,1996-June 30,1997 Main Office Washington Office The Harold Pratt House 1779 Massachusetts Avenue, N.W. 58 East 68th Street, New York, NY 10021 Washington, DC 20036 Tel. (212) 434-9400; Fax (212) 861-1789 Tel. (202) 518-3400; Fax (202) 986-2984 Website www. foreignrela tions. org e-mail publicaffairs@email. cfr. org OFFICERS AND DIRECTORS, 1997-98 Officers Directors Charlayne Hunter-Gault Peter G. Peterson Term Expiring 1998 Frank Savage* Chairman of the Board Peggy Dulany Laura D'Andrea Tyson Maurice R. Greenberg Robert F Erburu Leslie H. Gelb Vice Chairman Karen Elliott House ex officio Leslie H. Gelb Joshua Lederberg President Vincent A. Mai Honorary Officers Michael P Peters Garrick Utley and Directors Emeriti Senior Vice President Term Expiring 1999 Douglas Dillon and Chief Operating Officer Carla A. Hills Caryl R Haskins Alton Frye Robert D. Hormats Grayson Kirk Senior Vice President William J. McDonough Charles McC. Mathias, Jr. Paula J. Dobriansky Theodore C. Sorensen James A. Perkins Vice President, Washington Program George Soros David Rockefeller Gary C. Hufbauer Paul A. Volcker Honorary Chairman Vice President, Director of Studies Robert A. Scalapino Term Expiring 2000 David Kellogg Cyrus R. Vance Jessica R Einhorn Vice President, Communications Glenn E. Watts and Corporate Affairs Louis V Gerstner, Jr. Abraham F. Lowenthal Hanna Holborn Gray Vice President and Maurice R. Greenberg Deputy National Director George J. Mitchell Janice L. Murray Warren B. Rudman Vice President and Treasurer Term Expiring 2001 Karen M. Sughrue Lee Cullum Vice President, Programs Mario L. Baeza and Media Projects Thomas R. -

2019 Shareholder Letter

Strong Growth, Improved Performance For 2018 as a whole, we delivered solid quarterly results and significantly improved performance. For the full year of 2018, net income was up 50 percent, earnings per share (EPS) increased $1.24 to $3.72 per share, return on assets (ROA) was up 35 bps To Our Shareholders: to 1.17 percent, loans grew $1 billion to end the year at $20 billion, commercial criticized loans declined $451 million, or 42 percent, As of May 25, 2018, we became Hancock Whitney. and we achieved our goal of reducing our energy exposure to approximately 5 percent. On an operating basis, net income was up almost $100 million, or 38 percent, operating EPS increased $1.10 to just under $4 per share, and ROA was up 29 basis points to 1.25 percent.1 The year ended with tangible common equity (TCE) back above 8 percent and improved operating leverage of $38 million. We achieved these financial accomplishments while completing two significant transactions: the divestiture of Harrison Finance in March and the acquisition of Capital One’s trust and asset PPNR(TE)(a) Celebrating Hancock Whitney. On May Total25, 2018 Loans we opened the management business in July. Our board, executive team and (in millions) Nasdaq Stock Market as Hancock Whitney(in Corporation billions) (HWC), formally I are grateful to and proud of the nearly 4,000 associates who 500 introducing the new Hancock25 Whitney name and brand to America’s worked hard every day to achieve these results. investment$434.4 community. $401.8 $20.0 400 20 $19.0 During the year, we remained prudent in how we deployed $16.8 $323.4 Our new name and new brand mark$15.7 a new chapter in our ongoing our capital. -

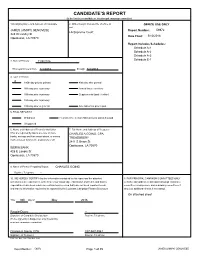

Candidate's Report

CANDIDATE’S REPORT (to be filed by a candidate or his principal campaign committee) 1.Qualifying Name and Address of Candidate 2. Office Sought (Include title of office as OFFICE USE ONLY well DESIREE CHARBONNET Report Number: 70458 Mayor 3860 Virgil Blvd. Orleans Date Filed: 4/30/2018 New Orleans, LA 70122 City of New Orleans Report Includes Schedules: Schedule A-1 Schedule A-2 Schedule A-3 Schedule B 3. Date of Primary 10/14/2017 Schedule E-1 This report covers from 10/30/2017 through 12/18/2017 4. Type of Report: X 180th day prior to primary 40th day after general 90th day prior to primary Annual (future election) 30th day prior to primary Supplemental (past election) 10th day prior to primary 10th day prior to general Amendment to prior report 5. FINAL REPORT if: Withdrawn Filed after the election AND all loans and debts paid Unopposed 6. Name and Address of Financial Institution 7. Full Name and Address of Treasurer (You are required by law to use one or more CYNTHIA C BERNARD banks, savings and loan associations, or money 1650 Kabel Drive market mutual fund as the depository of all New Orleans, LA 70131 REGIONS BANK 400 Poydras St. New Orleans, LA 70130 9. Name of Person Preparing Report PHILIP W REBOWE, CPA Daytime Telephone 504-236-0004 10. WE HEREBY CERTIFY that the information contained in this report and the attached 8. FOR PRINCIPAL CAMPAIGN COMMITTEES ONLY schedules is true and correct to the best of our knowledge, information and belief, and that no a. -

Candidate's Report

CANDIDATE’S REPORT (to be filed by a candidate or his principal campaign committee) 1.Qualifying Name and Address of Candidate 2. Office Sought (Include title of office as OFFICE USE ONLY well JAMES (JIMMY) GENOVESE Report Number: 58972 LA Supreme Court 324 W Landry St Date Filed: 5/10/2016 Opelousas, LA 70570 Report Includes Schedules: Schedule A-1 Schedule A-2 Schedule A-3 Schedule E-1 3. Date of Primary 11/8/2016 This report covers from 1/1/2016 through 5/2/2016 4. Type of Report: X 180th day prior to primary 40th day after general 90th day prior to primary Annual (future election) 30th day prior to primary Supplemental (past election) 10th day prior to primary 10th day prior to general Amendment to prior report 5. FINAL REPORT if: Withdrawn Filed after the election AND all loans and debts paid Unopposed 6. Name and Address of Financial Institution 7. Full Name and Address of Treasurer (You are required by law to use one or more CHARLES A GOING, CPA, banks, savings and loan associations, or money TREASURER^ market mutual fund as the depository of all 2811 S Union St Opelousas, LA 70570 IBERIA BANK 428 E Landry St Opelousas, LA 70570 9. Name of Person Preparing Report CHARLES GOING Daytime Telephone -- 10. WE HEREBY CERTIFY that the information contained in this report and the attached 8. FOR PRINCIPAL CAMPAIGN COMMITTEES ONLY schedules is true and correct to the best of our knowledge, information and belief, and that no a. Name and address of principal campaign committee, expenditures have been made nor contributions received that have not been reported herein, committee’s chairperson, and subsidiary committees, if and that no information required to be reported by the Louisiana Campaign Finance Disclosure any (use additional sheets if necessary). -

Candidate's Report

CANDIDATE’S REPORT (to be filed by a candidate or his principal campaign committee) 1.Qualifying Name and Address of Candidate 2. Office Sought (Include title of office as OFFICE USE ONLY well ERIC SKRMETTA Report Number: 93158 Public Service Commissioner 117 Sena Drive Date Filed: 11/25/2020 Metairie, LA 70005 District 1 Report Includes Schedules: Schedule A-1 Schedule B Schedule E-1 Schedule E-2 3. Date of Primary 11/3/2020 This report covers from 10/15/2020 through 11/15/2020 4. Type of Report: 180th day prior to primary 40th day after general 90th day prior to primary Annual (future election) 30th day prior to primary Supplemental (past election) 10th day prior to primary X 10th day prior to general Amendment to prior report 5. FINAL REPORT if: Withdrawn Filed after the election AND all loans and debts paid Unopposed 6. Name and Address of Financial Institution 7. Full Name and Address of Treasurer (You are required by law to use one or more DEBORAH SKRMETTA banks, savings and loan associations, or money 517 Sena Drive market mutual fund as the depository of all Metairie, LA 70005 CAPITAL ONE BANK 313 Carondelet St. New Orleans, LA 70130 9. Name of Person Preparing Report CARRIE M BERNAL Daytime Telephone 504-588-9288 10. WE HEREBY CERTIFY that the information contained in this report and the attached 8. FOR PRINCIPAL CAMPAIGN COMMITTEES ONLY schedules is true and correct to the best of our knowledge, information and belief, and that no a. Name and address of principal campaign committee, expenditures have been made nor contributions received that have not been reported herein, committee’s chairperson, and subsidiary committees, if and that no information required to be reported by the Louisiana Campaign Finance Disclosure any (use additional sheets if necessary). -

A Report on an Internship with the New Orleans Opera Association

University of New Orleans ScholarWorks@UNO Arts Administration Master's Reports Arts Administration Program 12-2012 A Report on an Internship with the New Orleans Opera Association Danqian Liu University of New Orleans Follow this and additional works at: https://scholarworks.uno.edu/aa_rpts Part of the Arts Management Commons Recommended Citation Liu, Danqian, "A Report on an Internship with the New Orleans Opera Association" (2012). Arts Administration Master's Reports. 140. https://scholarworks.uno.edu/aa_rpts/140 This Master's Report is protected by copyright and/or related rights. It has been brought to you by ScholarWorks@UNO with permission from the rights-holder(s). You are free to use this Master's Report in any way that is permitted by the copyright and related rights legislation that applies to your use. For other uses you need to obtain permission from the rights-holder(s) directly, unless additional rights are indicated by a Creative Commons license in the record and/or on the work itself. This Master's Report has been accepted for inclusion in Arts Administration Master's Reports by an authorized administrator of ScholarWorks@UNO. For more information, please contact [email protected]. A Report on an Internship with the New Orleans Opera Association An Internship Report Submitted to the Graduate Faculty of the University of New Orleans in partial fulfillment of the requirements for the degree of Master of Arts in Arts Administration By Danqian Liu B.A., National Academy of Chinese Theater Arts, 2010 December, 2012 Table of Contents ACKNOWLEDGEMENT ............................................................................................................. iii ABSTRACT ................................................................................................................................... iv CHAPTER 1: NEW ORLEANS OPERA ASSOCIATION .......................................................... -

Resources for People Who Are Homeless Or at Risk in the Greater New Orleans Area

t Funded through UNITY of Greater New Orleans Homeless Continuum of Care 1 in partnership with HUD and other city, state, and federal agencies. Resources for People who are Homeless or at Risk in the Greater New Orleans Area Compiled by UNITY of Greater New Orleans t Funded through UNITY of Greater New Orleans Homeless Continuum of Care 2 in partnership with HUD and other city, state, and federal agencies. Programs marked with a t are funded through the UNITY of Greater New Orleans Homeless Continuum of Care in partnership with the U.S. Department of Housing and Urban Development and other city, state, and federal agencies. unitygno.org unityhousinglink.org 2475 Canal Street, Suite 300 New Orleans, LA 70119 Phone: 504-821-4496 Toll Free Hotline: 1-888-899-4589 3____________________________________________________t Funded through UNITY of Greater New Orleans Homeless Continuum of Care CRISISin partnership LINES with HUD and other city, state, and federal agencies. ____________________________________________________ VIALINK • vialink.org Crisis counseling, suicide intervention, community resource directory 211 or 504-269-2673 or 1-800-749-2673 UNITY of Greater New Orleans • unitygno.org Response lines for persons living on the street or in places unfit for human habitation or for citizens to report a homeless person in need of assistance (note: neither one is a 24 hour line) 1-888-899-4589 Toll-free Response Line 504-269-2069 Local Response Line Child Abuse Hotline: 504-736-7033 Jefferson Parish East Bank 504-361-6083 Jefferson Parish -

New Orleans Spanish World New Orleans New Orleans Collection and the MUSEUM • RESEARCH CENTER • PUBLISHER Spanish World

1 and the The HistoricNew Orleans Spanish World New Orleans New Orleans Collection and the MUSEUM • RESEARCH CENTER • PUBLISHER Spanish World Teacher’s guide: grade levels 7–9 Number of lesson plans: 6 © 2015 The Historic New Orleans Collection; © 2015 The Louisiana Philharmonic Orchestra All rights reserved © 2015 The Historic New Orleans Collection | www.hnoc.org | © 2015 The Louisiana Philharmonic Orchestra | www.lpomusic.com 2 BASED ON THE 2015 CONCERT MUSICAL LOUISIANA: AMERICA’S New Orleans and the Spanish World CULTURAL HERITAGE presented by Metadata The Historic New Orleans Collection and the Grade levels 7–9 Louisiana Philharmonic Orchestra Number of lesson plans: 6 What’s Inside: Lesson One....p. 4 Lesson Two....p. 9 Lesson Three....p. 13 Lesson Four....p. 17 Lesson Five....p. 20 Lesson Six....p. 23 Common Core Standards CCSS.ELA-LITERACY.RH.9-10.1: Cite specific textual evidence to support analysis of primary and secondary sources, attending to such features as the date and origin of the information. CCSS.ELA-LITERACY.RH.9-10.4: Determine the meaning of words and phrases as they are used in a text, including vocabulary describing political, social, or economic aspects of history/social science. CCSS.ELA-LITERACY.RH.11-12.2: Determine the central ideas or information of a primary or secondary source; provide an accurate summary that makes clear the relationships among the key details and ideas. CCSS.ELA-LITERACY.RL.9-10.6: Analyze a particular point of view or cultural experience reflected in a work of literature from outside the United States, drawing on a wide reading of world literature. -

CBD & Metairie Office Markets

CBD & Metairie Office Markets Greater New Orleans Occupancy Up in 2013 • Occupancy increased from 85% to 86.5% • 207,000 sq. ft. absorption • New Orleans 164,000 sq. ft. absorption • Jefferson 43,000 sq. ft. absorption CBD Office Market *Class A & B 10.5 million square feet 85% leased *Class A - 8.8 million square feet 89% leased, 133,000 absorption Rent range $16.50 – $21.00 *Class B - 1.6 million square feet 67% leased, 30,000 absorption Rent range $13.75 – $17.00 CBD Class A 2010 - 2013 CBD Space Reductions – 2011 1250 Poydras Building • FEMA - 95,000 sq. ft. • ENI - 75,000 sq. ft. - sublease One Canal Place • AT&T - 90,000 sq. ft. reduction One Shell Square • Shell Offshore - 50,000 sq. ft. reduction 1615 Poydras Building • Coast Guard - 22,000 sq. ft. relocation to Federal City Place St. Charles • Capital One & Chase - 75,000 + sq. ft. reduction CBD Class B 2010 - 2013 CBD Office Significant Leases One Shell Square • Shell Oil Company • Renewal 600,000 sq. ft. • 10 year lease • Commencing January 2017 • Largest tenant in greater New Orleans Orleans Tower • City of New Orleans • Renewal/reduction • 110,000 sq. ft. CBD Office Significant Leases Place St. Charles • Capital One • Renewal/reduction • 49,000 sq. ft. 1515 Poydras Building • URS • New; relocation from 600 Carondelet • 60,000 sq. ft. CBD Office Sales Energy Centre • Size – 761,500 sq. ft. • $83.5 million, $110 prsf • Hertz Investments • 91% leased • Sold June 2013 Hertz Investment Group CBD Class A Office CBD Portfolio % Leased • 4 buildings • 909 Poydras – 86% • 2.3 million sq.