Pacific Brands Board Unanimously Recommends Acquisition Proposal from Hanesbrands

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hanesbrands Inc. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended January 3, 2015 or TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number: 001-32891 Hanesbrands Inc. (Exact name of registrant as specified in its charter) Maryland 20-3552316 (State of incorporation) (I.R.S. employer identification no.) 1000 East Hanes Mill Road Winston-Salem, North Carolina 27105 (Address of principal executive office) (Zip code) (336) 519-8080 (Registrant’s telephone number including area code) Securities registered pursuant to Section 12(b) of the Act: Common Stock, par value $0.01 per share and related Preferred Stock Purchase Rights Name of each exchange on which registered: New York Stock Exchange Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes No Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes No Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Hbi Letterhead

news release FOR IMMEDIATE RELEASE News Media: Kirk Saville, (336) 519-6192 Analysts and Investors: T.C. Robillard, (336) 519-2115 HANESBRANDS AND BELLE INTERNATIONAL ENTER LICENSING AGREEMENT TO INTRODUCE CHAMPION FOOTWEAR AND ACCESSORIES IN CHINA Partnership combines the power of the Champion brand with Belle’s extensive retail network, e-commerce expertise and supply chain capabilities WINSTON-SALEM, N.C. – (Feb. 26, 2021) – HanesBrands and Belle International today announced a licensing agreement that will introduce a line of Champion footwear and accessories to consumers in China next year. Under the agreement, Belle will distribute the new collection designed specifically for consumers in China through its countrywide retail network and e-commerce platform. The Champion product range will tap into the brand’s aesthetic and be available by June 2021. “We’re thrilled to expand our long-term distribution relationship with Belle to include a license for footwear and accessories in China, said Jon Ram, group president of global activewear for HanesBrands. “Belle has demonstrated vast capabilities across brick-and- mortar retail, e-commerce, consumer insights and supply chain – and we’re confident the partnership will further accelerate the global growth of the Champion brand.” Fashion Clothing, a Belle International company based in Shanghai, has been a strategic partner for the Champion brand since June 2019. The company operates hundreds of Champion-branded brick-and-mortar and official online stores on leading e-commerce platforms, including Alibaba Group’s TMALL, JD.com and VIP.com. “We see outstanding potential for Champion in the large, growing market in China, and Belle International’s long history of serving consumers in the country, extensive nationwide store network and cross-category supply chain capabilities make us complementary partners,” said Fang Sheng, executive director and president of the footwear and new ventures business group for Belle International. -

Hanesbrands CDP Water 2017 Report

Water 2017 - Hanesbrands Inc. CDP Module: Introduction Page: W0. Introduction W0.1 Introduction Please give a general description and introduction to your organization HanesBrands, based in Winston-Salem, N.C., is a socially responsible leading marketer of everyday basic innerwear and activewear apparel in the Americas, Europe, Australia and Asia-Pacific. The company sells its products under some of the world’s strongest apparel brands, including Hanes, Champion, Maidenform, DIM, Bali, Playtex, Bonds, JMS/Just My Size, Nur Die/Nur Der, L’eggs, Lovable, Wonderbra, Berlei, and Gear for Sports. The company sells T-shirts, bras, panties, shapewear, underwear, socks, hosiery, and activewear produced in the company’s low-cost global supply chain. A member of the S&P 500 stock index, Hanes has approximately 68,000 employees in more than 40 countries and is ranked No. 432 on the Fortune 500 list of America’s largest companies by sales. Hanes takes pride in its strong reputation for ethical business practices. The company is the only apparel producer to ever be honored by the Great Place to Work Institute for its workplace practices in Central America and the Caribbean, and is ranked No. 110 on the Forbes magazine list of America’s Best Large Employers. For eight consecutive years, Hanes has won the U.S. Environmental Protection Agency Energy Star sustained excellence/partner of the year award – the only apparel company to earn sustained excellence honors. The company ranks No. 172 on Newsweek magazine’s green list of 500 largest U.S. companies for environmental achievement. More information about the company and its corporate social responsibility initiatives, including environmental, social compliance and community improvement achievements, may be found at www.Hanes.com/corporate. -

Annual Report

Annual Report Form 10-K for the Fiscal Year Ended December 31, 2016 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2016 or TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number: 001-32891 Hanesbrands Inc. (Exact name of registrant as specified in its charter) Maryland 20-3552316 (State of incorporation) (I.R.S. employer identification no.) 1000 East Hanes Mill Road Winston-Salem, North Carolina 27105 (Address of principal executive office) (Zip code) (336) 519-8080 (Registrant’s telephone number including area code) Securities registered pursuant to Section 12(b) of the Act: Common Stock, par value $0.01 per share Name of each exchange on which registered: New York Stock Exchange Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes No Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes No Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Hanes Australasia

APCO MEMBER CASE STUDY: HANES AUSTRALASIA Could a single plastic hanger really be a customers hangers with their online orders, but problem? When Hanes Australasia, owner of we decided to invest in a solution.’ market-leading brands Bonds, Berlei, Bras The catalyst for change, she says, was two- N Things, Champion and Sheridan recently fold. First, the company considered it the invested in additional resource to manually right thing to do in reducing its environmental remove plastic hangers on its Bonds garments footprint and by increasing its own internal ordered online, the answer soon became clear. recycling rates. And, second, some customers Within six months, over half a million plastic were getting in touch and asking Hanes not to hangers, or 15 tonnes of plastic, had been send hangers out with their Bonds orders. retrieved instead of ending up in their online customers’ bins and likely headed for landfill. In 2019, at least a million hangers are expected ‘Customers are increasingly to be fed back into the company’s ‘closed loop considering sustainability when hanger recycling program’. This particular waste challenge emerged as they are making brand choices and customers embraced online. In stores, hangers younger consumers, in particular, are are routinely removed at the point of sale, and far more aware of the environmental re-used up to seven times in the company’s closed loop program, before being recycled. By effects of their purchasing decisions.’ retaining the hangers, Hanes could keep track of them across their lifecycle and avoid them being ‘Customers are increasingly considering lost to landfill or leaking into the environment sustainability when they are making brand as waste. -

HANESBRANDS INC GOING COMMANDO September 13, 2016 DISCLAIMER

BRIAN MCGOUGH ALEC RICHARDS JEREMY MCLEAN HANESBRANDS INC GOING COMMANDO September 13, 2016 DISCLAIMER DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment advice for individuals. This research does not constitute an offer to sell, or a solicitation of an offer to buy any security. This research is presented without regard to individual investment preferences or risk parameters; it is general information and does not constitute specific investment advice. This presentation is based on information from sources believed to be reliable. Hedgeye Risk Management is not responsible for errors, inaccuracies or omissions of information. The opinions and conclusions contained in this report are those of Hedgeye Risk Management, and are intended solely for the use of Hedgeye Risk Management’s clients and subscribers. In reaching these opinions and conclusions, Hedgeye Risk Management and its employees have relied upon research conducted by Hedgeye Risk Management’s employees, which is based upon sources considered credible and reliable within the industry. Hedgeye Risk Management is not responsible for the validity or authenticity of the information upon which it has relied. TERMS OF USE This report is intended solely for the use of its recipient. Re-distribution or republication of this report and its contents are prohibited. For more details please refer to the appropriate sections of the Hedgeye Services Agreement and the Terms of Use at www.hedgeye.com © Hedgeye Risk Management LLC, All Rights Reserved. 2 PLEASE SUBMIT QUESTIONS* TO [email protected] *ANSWERED AT THE END OF THE CALL STILL CALLING IT LIKE WE SEE IT 1) Core business weakening. -

Hanes Hosiery Mill

NORTH CAROLINA STATE HISTORIC PRESERVATION OFFICE Office of Archives and History Department of Cultural Resources NATIONAL REGISTER OF HISTORIC PLACES Hanes Hosiery Mill – Ivy Avenue Plant Winston-Salem, Forsyth County, FY8833, Listed 5/31/2016 Nomination by Sunny Townes Stewart Photographs by Sunny Townes Stewart, October 2015 East Elevation, 1925 Hosiery Mill #1 Overall view, 1938 finishing mill NPS Form 10-900 OMB No. 1024-0018 United States Department of the Interior National Park Service National Register of Historic Places Registration Form This form is for use in nominating or requesting determinations for individual properties and districts. See instructions in National Register Bulletin, How to Complete the National Register of Historic Places Registration Form. If any item does not apply to the property being documented, enter "N/A" for "not applicable." For functions, architectural classification, materials, and areas of significance, enter only categories and subcategories from the instructions. 1. Name of Property Historic name: _Hanes Hosiery Mill, Ivy Avenue Plant _______ Other names/site number: _N/A_________________________________ Name of related multiple property listing: _N/A______________________________________________________ (Enter "N/A" if property is not part of a multiple property listing ___________________________________________________________ 2. Location Street & number: _1245 and 1325 Ivy Avenue_____________________ City or town: _Winston-Salem___ State: _NC____ County: _Forsyth_____ Not For Publication: N/A Vicinity: N/A ____________________________________________________________________________ 3. State/Federal Agency Certification As the designated authority under the National Historic Preservation Act, as amended, I hereby certify that this X nomination ___ request for determination of eligibility meets the documentation standards for registering properties in the National Register of Historic Places and meets the procedural and professional requirements set forth in 36 CFR Part 60. -

Germans .Britain Boosts Income Tax to New Peak^ Harbors, Airports

\ UeilDAr.}T)LTII.tM« ..im r i M L v s '■’Vi flatirftfstnr Etiratno 3SrndIk Average Dally Cirealetlea Far tha Moath at Jama. l$ i . The regular meatlng af Mlaato- Mra Herbert Sargent and tv-f 4 The Weather While working on the new town Dr. Edward F. Krtksclun of Chi Pr. and Mrs. A. A. Friahalt o f M Edward Harris, ■7ST Maary Mrs. Joi^^hina Ptow4k Hills, Elwood street are taking a vaca street, was sersiiaded ftmdey. by noraoh TTlbe No. BB, I. O. ft. M., children, Alice Jeen and Herbert roraeaat af O. S. WaaUur Bmi who U oondudUng a summer art dump several men of the Love cago, ni., one of the successful wUl ha held In the Sports Center Kilby, have left for Weymouth HitTawn Lane W. P. A. project have been tion until August 2, and enjoying tha siOvatlon Army Band. X f. 6,429 course in Rodm 10 of ManehooUr candidates In the state dental sViaon WellsTT vgam ,^ streetv tonight at el^ t Nova Scotia, where they will epenf / affected by^tHrlUtlon of the skin short trips to nsarby places of in HarriA wbo is a member o f thr High school, has changsd the in exams Is a nephew of Peter Staum terest band'haa been confined to bed adth shiu’p. the remainder of the summer. Maatbar af tha Aadit / struction hours, by request, frops from polpcmlng. None of the cases of 89 W. Middle Turnpike. He 1s a heart aliment for the past six BnieM o f Otienlotlono ^ srsji BMtriM AnoM. -

Fully Integrated Marketing Communications Plan for Hanes

The Traditional Family Brand TEAM HANES Andrea Brown Megan Gill Courtney Scott Johnique Smith Table of Contents Executive Summary͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙.4 Situation Analysis SWOT Analysis͙͙͙͙͙͙͙͙͙͙..͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙..͙.5 Price Point͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙..6 The Competition͙͙͙͙͙͙͙͙͙͙͙͙͙..͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙7-8 Industry & Category Analysis͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙....͙͙͙͙͙͙͙͙͙͙͙͙͙9-11 Market Analysis͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙..12-22 Target Analysis͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙..23-28 Problems and Opportunity Summary͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙.......29 Key Problems & Insights͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙30-37 Marketing Communications Objectives͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙..38-41 Marketing Strategies & Rationale͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙..42-48 Advertising, Media & Promotional Tools͙͙͙͙͙..͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙.49-65 Campaign Evaluation͙͙͙͙͙.....͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙.66-69 Budget͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙.70-73 Campaign Conclusion͙͙͙͙͙͙..͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙74 Appendix͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙..͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙75 Research͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙..76-80 References͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙͙.͙͙͙͙͙͙͙͙͙͙͙͙..͙͙͙..81-84 2 Executive Summary: Hanes is the leading manufacturer of intimate apparel, coined the term, ͞apparel essentials.͟ Within this highly competitive sector, Hanes must act now to a capture burgeoning segment of the U.S. market before its competitors. Hanes is the ͞go-to brand͟ for many of its Latino customers, yet has lacked consideration -

Hanesbrands Names Tanya Deans President of Hanes Australasia

NEWS RELEASE HanesBrands Names Tanya Deans President of Hanes Australasia 12/18/2020 WINSTON-SALEM, N.C.--(BUSINESS WIRE)-- HanesBrands (NYSE: HBI), a leading global marketer of branded everyday basic apparel, today announced that Tanya Deans has been named president of Hanes Australasia (HAA), eective Feb. 8, 2021. Deans, currently group general manager, Bras N Things, succeeds David Bortolussi, who in August announced his departure for another opportunity. Bortolussi will remain with HAA through January to ensure a smooth transition. “I am thrilled to name Tanya as the new president of our Australasia business,” said Steve Bratspies, CEO of HanesBrands. “She is an outstanding people leader with deep experience building iconic brands. Tanya brings a clear vision for the future, and I look forward to working with her as we apply her experience and learnings to drive growth across our global organization.” Deans will lead 4,400 associates and some of Australia’s most recognized apparel and lifestyle brands, including Bonds, Champion, Bras N Things and Sheridan. She will also be responsible for a rapidly growing e-commerce business and a network of more than 450 stores. Deans has more than 25 years of experience with Hanes Australasia in a range of brand and product leadership roles. She has extensive knowledge of brand strategy, category management, product development and multichannel execution capabilities. Prior to her current role, Deans led the Hanes Australasia Apparel Group brand and marketing eorts. She has also held leadership roles with the Bonds and Berlei brands. 1 “I am honored to have the opportunity to lead Hanes Australasia,” Deans said. -

Hanesbrands Inc. (Hbi) Assessment for Reaccreditation

HANESBRANDS INC. (HBI) ASSESSMENT FOR REACCREDITATION FLA BOARD OF DIRECTORS MEETING OCTOBER 2019 HANESBRANDS, INC.: ASSESSMENT FOR REACCREDITATION TABLE OF CONTENTS TABLE OF CONTENTS .............................................................................................................. 2 INTRODUCTION ........................................................................................................................ 3 SECTION 1: HBI COMPANY AFFILIATE OVERVIEW ............................................................... 4 SECTION 2: HBI SUPPLY CHAIN & FLA DUE DILIGENCE 2010 – 2019 ................................. 6 SECTION 3: HBI SOCIAL COMPLIANCE PROGRAM ANALYSIS ............................................ 7 SECTION 4: RECOMMENDATION TO THE FLA BOARD OF DIRECTORS ........................... 28 APPENDIX A: THE HBI GLOBAL STANDARDS FOR SUPPLIERS (CODE OF CONDUCT) .. 29 APPENDIX B: HBI’s REMEDIATION PROGRESS CHART ..................................................... 32 APPENDIX C: PRINCIPLES OF FAIR LABOR RESPONSIBLE PRODUCTION & SOURCING ................................................................................................................................................. 33 APPENDIX D: HBI’s SAFEGUARDS CHART ............................................................................3 71 Workers at an owned HbI facility in El Salvador. www.fairlabor.org 2 HANESBRANDS, INC.: ASSESSMENT FOR REACCREDITATION INTRODUCTION On October 23, 2019, the FLA Board of Directors approved the reaccreditation of Hanesbrands’ social -

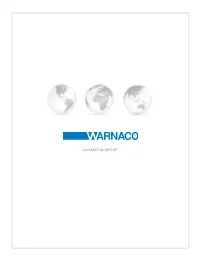

2010 ANNUAL Reportpage 1

2010N AN UAL REPORT 0526_cov.indd 2 4/7/11 10:30 AM COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN* Among The Warnaco Group, Inc., the Russell 2000 index, the S&P Midcap 400 index, the Dow Jones US Clothing & Accessories index $250 and the S&P Apparel, Accessories & Luxury Goods index COMPARISONCOMParisON OF OF 5YEAR 5-YEar CCUMULATIVEUMULatiVE TO TOTALtaL RE TRETURN*Urn* e Warnaco Group, Inc. compared to select indices $250 $200 250 250 $200 $150 200 200 $150 150 150 $100 $100 100 100 $50 $50 50 50 $0 0 0 $0 3/06 6/06 9/06 3/07 6/07 9/07 3/08 6/08 9/08 3/09 6/09 9/09 3/10 6/10 9/10 12/05 12/06 12/07 12/08 12/09 12/10 12/05 3/06 6/06 9/06 12/06 3/07 6/07 9/07 12/07 3/08 6/08 9/08 12/083/096/09 9/09 12/09 3/10 6/10 9/10 12/10 e Warnaco Group, Inc. Russell 2000 S&P MidCap 400 Dow Jones U.S. Clothing & Accessories The Warnaco Group, Inc. Russell 2000 S&P Apparel, Accessories & Luxury Goods *$100 invested on 12/31/05 in stock or index, including reinvestment of dividends. Fiscal year ending December 31. S&P Midcap 400 Dow Jones US Clothing & Accessories Copyright © 2011 S&P, a division of e McGraw-Hill Companies Inc. All rights reserved. Copyright © 2011 Dow Jones & Co. All rights reserved. S&P Apparel, Accessories & Luxury Goods *$100 invested on 12/31/05 in stock or index, including reinvestment of dividends.