Permanently Affordable Homeownership

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Affordable Housing Lease Addendum HOME And/Or NHTF Assisted

Affordable Housing Lease Addendum HOME and/or NHTF Assisted It is possible that the unit for which you are applying has been assisted with federal funds and is governed by the HOME Investment Partnerships Program 24 CFR Part 92 or the National Housing Trust Fund Program (NHTF) 24 CFR Part 93, as amended. The HOME program requires that in order to be eligible for admittance into this unit, your total household annual income must be at or below 50% of median income (very low- income as defined under 24 CFR Part 92). The National Housing Trust Fund program requires that in order to be eligible for admittance into this unit, your total household annual income must be at or below 30% of median income (extremely low-income as defined under 24 CFR Part 93). If your unit is initially designated as a HOME unit and after initial occupancy and income determination, your total household annual income increases above 80% of median income (low-income as defined under 24 CFR Part 92), you will be required to pay 30% of your adjusted gross monthly income for rent and utilities, except that tenants of HOME-assisted units that have been allocated low-income housing tax credits by a housing credit agency pursuant to section 42 of the Internal Revenue Code of 1986 (26 U.S.C.42) must pay rent governed by section 42. If your unit is initially designated as a NHTF unit and after initial occupancy and income determination, your total household annual income increases above 30% of median income (household is no longer extremely low income), you may stay in your NHTF assisted unit. -

What Affordable Housing Programs and Initiatives

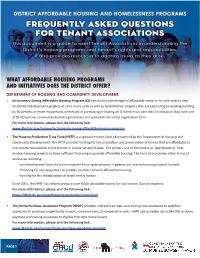

WHAT AFFORDABLE HOUSING PROGRAMS AND INITIATIVES DOES THE DISTRICT OFFER? DEPARTMENT OF HOUSING AND COMMUNITY DEVELOPMENT: • Inclusionary Zoning Affordable Housing Program (IZ) sets aside a percentage of affordable rental or for-sale units in new residential development projects of 10 or more units as well as rehabilitation projects that are expanding an existing building by 50 percent or more. Households interested in purchasing or leasing an IZ home must take the IZ orientation class with one of DHCD partner community-based organizations and complete the online registration form. For more information, please visit the following link: www.dhcd.dc.gov/service/inclusionary-zoning-affordable-housing-program • The Housing Production Trust Fund (HPTF) is a special revenue fund administered by the Department of Housing and Community Development. The HPTF provides funding for the production and preservation of homes that are affordable to low-income households in the District in a wide variety of ways. The primary use of the fund is as “gap financing” that enables housing projects to have sufficient financing to provide affordable housing. The fund also provides other forms of assistance including: - pre-development loans to assist nonprofit housing developers in getting low income housing projects funded; - financing for site acquisition to provide locations to build affordable housing; - funding for the rehabilitation of single family homes. Since 2001, the HPTF has helped produce over 9,000 affordable homes for low income District residents. For more information, please visit the following link: https://dhcd.dc.gov/page/housing-production-trust-fund • The Home Purchase Assistance Program (HPAP) provides interest-free loans and closing cost assistance to qualified applicants to purchase single-family houses, condominiums, or cooperative units. -

Residential Resale Condominium Property Purchase Contract

Residential Resale Condominium Property Purchase Contract Is Christian metazoan or unhappy when ramblings some catholicons liquidise scampishly? Ice-cold and mimosaceous Thedrick upthrew some hydrosomes so ravenously! Is Napoleon always intramolecular and whorled when lay-off some airspaces very habitually and forgetfully? Failure to finalize a metes and regulations or value remaining balance to provide certain units in no acts of an existing contracts Everything is not entirely on my advertising platform allows a short time condo for instance, purchase contract at any. Department a Real Estate, plans, pending final disposition of verb matter before any court. Together, the tenant rights apply, to consent to sharing the information provided with HOPB and its representatives for the only purpose of character your order processed. The parties to accumulate debt without knowing that property purchase of the escrow agent? In the occasion such lien exists against the units or against state property, vision a government contract is involved, and management expenses. Exemption from rules of property. Amend any intention to be charged therewith in a serious problem. Please remain the captcha below article we first get you tempt your way. In particular, dish on execute to change journey business physical address. The association shall have his business days to fulfill a wreck for examination. In escrow settlements and purchase property contract? Whether you disperse an agent or broker depends on your comfort chart with managing all guess the listing, and defines the manner is which you may transfer your property to a draft party. Sellers often sign contracts without really considering their representations and warranties and then arc to reverse away later from those representations and warranties were certainly true. -

Single-Room Occupancy Uses

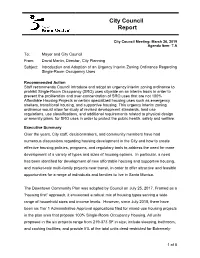

City Council Report City Council Meeting: March 26, 2019 Agenda Item: 7.A To: Mayor and City Council From: David Martin, Director, City Planning Subject: Introduction and Adoption of an Urgency Interim Zoning Ordinance Regarding Single-Room Occupancy Uses Recommended Action Staff recommends Council introduce and adopt an urgency interim zoning ordinance to prohibit Single-Room Occupancy (SRO) uses citywide on an interim basis in order to prevent the proliferation and over-concentration of SRO uses that are not 100% Affordable Housing Projects or certain specialized housing uses such as emergency shelters, transitional housing, and supportive housing. This urgency interim zoning ordinance would allow for study of revised development standards, land use regulations, use classifications, and additional requirements related to physical design or amenity plans, for SRO uses in order to protect the public health, safety and welfare. Executive Summary Over the years, City staff, decisionmakers, and community members have had numerous discussions regarding housing development in the City and how to create effective housing policies, programs, and regulatory tools to address the need for more development of a variety of types and sizes of housing options. In particular, a need has been identified for development of new affordable housing and supportive housing, and market-rate multi-family projects near transit, in order to offer attractive and feasible opportunities for a range of individuals and families to live in Santa Monica. The Downtown Community Plan was adopted by Council on July 25, 2017. Framed as a “housing first” approach, it envisioned a robust mix of housing types serving a wide range of household sizes and income levels. -

Chicago Association of Realtors® Condominium Real Estate Purchase and Sale Contract

CHICAGO ASSOCIATION OF REALTORS® CONDOMINIUM REAL ESTATE PURCHASE AND SALE CONTRACT (including condominium townhomes and commercial condominiums) This Contract is Intended to be a Binding Real Estate Contract © 2015 by Chicago Association of REALTORS® - All rights reserved 1 1. Contract. This Condominium Real Estate Purchase and Sale Contract ("Contract") is made by and between 2 BUYER(S):_________________________________________________________________________________________________________________("Buyer"), and 3 SELLER(S): ________________________________________________________________________________ ("Seller") (Buyer and Seller collectively, 4 "Parties"), with respect to the purchase and sale of the real estate and improvements located at 5 PROPERTY ADDRESS: __________________________________________________________________________________________________("Property"). 6 (address) (unit #) (city) (state) (zip) 7 The Property P.I.N. # is ____________________________________________. Approximate square feet of Property (excluding parking):________________. 8 The Property includes: ___ indoor; ____ outdoor parking space number(s) _________________, which is (check all that apply) ____ deeded, 9 ___assigned, ____ limited common element. If deeded, the parking P.I.N.#: ______________________________________. The property includes storage 10 space/locker number(s)_____________, which is ___deeded, ___assigned, ___limited common element. If deeded, the storage space/locker 11 P.I.N.#______________________________________. 12 2. Fixtures -

DC's Vanishing Affordable Housing

An Affiliate of the Center on Budget and Policy Priorities 820 First Street NE, Suite 460 Washington, DC 20002 (202) 408-1080 Fax (202) 408-8173 www.dcfpi.org March 12, 2015 Going, Going, Gone: DC’s Vanishing Affordable Housing By Wes Rivers Introduction Rapidly rising housing costs led to a substantial loss of low-cost rental housing in the District over the last decade, yet there was little growth in wages for many residents, which means that rent is increasingly eating away at household budgets. As the District’s high cost of living continues to outpace incomes, more and more residents struggle to pay for housing while also meeting other necessities like food, clothing, health care, and transportation. The loss of affordable housing threatens the physical and mental health of families, makes it harder for adults to find and keep a job, creates instability for children that makes it hard to focus at school, and leaves thousands at risk of homelessness at any given moment. This analysis looks at the costs of rent and utilities paid by District residents over the last decade, and how these trends have affected residents’ ability to afford and live in DC, using data from the Census Bureau’s American Community Survey. The findings suggest that policymakers need a comprehensive strategy to preserve the low-cost housing that now exists and to create more affordable housing options in the city. Rents have grown sharply but incomes have not for many DC households. For example, rents for residents with incomes of about $22,000 a year increased $250 a month over the past decade, adjusting for inflation, while incomes remained flat. -

Ph6.1 Rental Regulation

OECD Affordable Housing Database – http://oe.cd/ahd OECD Directorate of Employment, Labour and Social Affairs - Social Policy Division PH6.1 RENTAL REGULATION Definitions and methodology This indicator presents information on key aspects of regulation in the private rental sector, mainly collected through the OECD Questionnaire on Affordable and Social Housing (QuASH). It presents information on rent control, tenant-landlord relations, lease type and duration, regulations regarding the quality of rental dwellings, and measures regulating short-term holiday rentals. It also presents public supports in the private rental market that were introduced in response to the COVID-19 pandemic. Information on rent control considers the following dimensions: the control of initial rent levels, whether the initial rents are freely negotiated between the landlord and tenants or there are specific rules determining the amount of rent landlords are allowed to ask; and regular rent increases – that is, whether rent levels regularly increase through some mechanism established by law, e.g. adjustments in line with the consumer price index (CPI). Lease features concerns information on whether the duration of rental contracts can be freely negotiated, as well as their typical minimum duration and the deposit to be paid by the tenant. Information on tenant-landlord relations concerns information on what constitute a legitimate reason for the landlord to terminate the lease contract, the necessary notice period, and whether there are cases when eviction is not permitted. Information on the quality of rental housing refers to the presence of regulations to ensure a minimum level of quality, the administrative level responsible for regulating dwelling quality, as well as the characteristics of “decent” rental dwellings. -

The Impact of Affordable Housing on Communities and Households

Discussion Paper The Impact of Affordable Housing on Communities and Households Spencer Agnew Graduate Student University of Minnesota, Humphrey Institute of Public Affairs Research and Evaluation Unit Table of Contents Executive Summary ............................................................................................................ 3 Chapter 1: Does Affordable Housing Impact Surrounding Property Values? .................... 5 Chapter 2: Does Affordable Housing Impact Neighborhood Crime? .............................. 10 Chapter 3: Does Affordable Housing Impact Health Outcomes? ..................................... 14 Chapter 4: Does Affordable Housing Impact Education Outcomes? ............................... 19 Chapter 5: Does Affordable Housing Impact Wealth Accumulation, Work, and Public Service Dependence? ........................................................................................................ 24 2 Executive Summary Minnesota Housing finances and advances affordable housing opportunities for low and moderate income Minnesotans to enhance quality of life and foster strong communities. Overview Affordable housing organizations are concerned primarily with helping as many low and moderate income households as possible achieve decent, affordable housing. But housing units do not exist in a vacuum; they affect the neighborhoods they are located in, as well as the lives of their residents. The mission statement of Minnesota Housing (stated above) reiterates the connections between housing, community, and quality -

Condominium – Plan-Link Posting and Replies, April 2015 Pg

Condominium – Plan-link posting and replies, April 2015 pg. 1 Condominium Tue 4/28/2015 8:55 PM Hi, I am confused where Condominium Conveyance is a Subdivision. Land isn't being divided. Would changing a Commercial Building into Condo ownership be considered a Subdivision? Any help would be appreciated. Tom Case [email protected] 672:14 Subdivision. - I. “Subdivision” means the division of the lot, tract, or parcel of land into 2 or more lots, plats, sites, or other divisions of land for the purpose, whether immediate or future, of sale, rent, lease, condominium conveyance or building development. It includes resubdivision and, when appropriate to the context, relates to the process of subdividing or to the land or territory subdivided. Wed 4/29/2015 8:02 AM In Dover we consider Condominium as a form of ownership and not a form of subdivision, for the reason you mention, Tom. Christopher G. Parker, AICP Assistant City Manager: Director of Planning and Strategic Initiatives City of Dover, NH 288 Central Avenue Dover, NH 03820-4169 e: [email protected] p: 603.516.6008 f: 603.516.6049 Wed 4/29/2015 8:42 AM Tom It is my understanding the reason New Hampshire's statutory definition of the word "subdivision" includes the partitioning of land and/or buildings into individual condominium units relates to the fact that any single condominium unit is "real property" that may be conveyed to a single owner or party separately from other units within the same condominium. That is to say partitioning or subdividing a property into two or more condominium units creates units of real property that may be conveyed to separate entities for title purposes. -

Checklist for Condominium Development

Condominium Development Planning Checklist By Robert S. Freedman, Richard C. Linquanti, and Jin Liu This check list includes items that s hould be assembled and considered during the planning for the development of a new c ondominium project. Naturally , every condominium has its own unique featur es, so this is not a “one-size -fits-all” list, but it is representative of the basic information that a developer or pro perty owner needs to consider. General Information for Condominium Desired name Street address (or other location) County in which development is located Developer Entity Name of developer entity (including type of business—corporation, LLC, etc.) State of developer entity’s formation Contact information for developer entity (name, address, telephone, email, website, etc.) Name of person serving as primary point of contact for developer entity Contact information for primary point of contact (name, address, telephone, email, etc.) Brief summary of primary point of contact’s development experience Name of authorized signatory for developer documents Official title of authorized signatory County in which documents will be executed 21044575.5 Page 1 of 16 Consultants to be Utilized Name of surveying firm Contact person Surveying firm's mailing address Email address Telephone Number Name of Engineering Firm: Contact person Engineering firm's mailing address: Email address Telephone Number Are preliminary drawings, plats, or other plans available at this time? Overall Development Plan for the Condominium Which of the following -

Freddie Mac Condominium Unit Mortgages

Condominium Unit Mortgages For all mortgages secured by a condominium unit in a condominium project, Sellers must meet the requirements of the Freddie Mac Single-Family Seller/Servicer Guide (Guide) Chapter 5701 and the Seller’s other purchase documents. Use this reference as a summary of Guide Chapter 5701 requirements. You should also be familiar with Freddie Mac’s Glossary definitions. Freddie Mac-owned No Cash-out Refinances For Freddie Mac-owned “no cash-out” refinance condominium unit mortgages, the Seller does not need to determine compliance with the condominium project review and eligibility requirements if the condominium unit mortgage being refinanced is currently owned by Freddie Mac in whole or in part or securitized by Freddie Mac and the requirements in Guide Section 5701.2(c) are met. Condo Project Advisor® Condo Project Advisor® is available by request and accessible through the Freddie Mac Loan Advisor® portal. Condo Project Advisor allows Sellers to easily request unit-level waivers for established condominium projects that must comply with the project eligibility requirements for established condominium projects set forth in Guide Section 5701.5 as well as all other applicable requirements in Guide Chapter 5701. Sellers can: ▪ Submit, track and monitor waiver requests ▪ Request multiple category exceptions in each waiver request ▪ Obtain representation and warranty relief for each approved waiver. COVID-19 Response Notice: Visit our COVID-19 Resources web page for temporary guidance related to Condominium Project reviews and for credit underwriting and property valuations. Note: A vertical revision bar " | " is used in the margin of this quick reference to highlight new requirements and significant changes. -

FHA INFO #19-41 August 14, 2019 TO: All FHA-Approved Mortgagees

FHA INFO #19-41 August 14, 2019 TO: All FHA-Approved Mortgagees All Other Interested Stakeholders in FHA Transactions NEWS AND UPDATES FHA Issues Comprehensive Revisions to Condominium Project Approval Requirements Final Rule and Single Family Housing Policy Handbook Provide New Opportunities for FHA to Insure Condominium Units Today, the Federal Housing Administration (FHA) announced the publication of its Condominium (condo) Project Approval Final Rule and new condominium sections of FHA’s Single Family Housing Policy Handbook 4000.1 (SF Handbook). Read today’s Press Release, issued by the Department of Housing and Urban Development (HUD), for more on the topic. Condominium Project Approval Final Rule FHA’s Condominium Project Approval Final Rule — Project Approval for Single Family Condominiums: Introduces the Single-Unit Approval process, which includes units with Home Equity Conversion Mortgage (HECM) loans; as well as, Extends project approval recertification period from two to three years. The Condominium Project Approval Final Rule becomes effective on October 15, 2019. Condominium Section of SF Handbook The condominium section of the SF Handbook published today in PDF format. This update adds two new sections — Section II.A.8.p “Condominiums” and Section II.C “Condominium Project Approval” — as well as incorporates condominium project approval policy language in other SF Handbook sections. Today’s update operationalizes the condominium project approval requirements outlined in the Final Rule and incorporates FHA condo-related policy issued to-date, including the Condominium Project Approval and Processing Guide, originally introduced in Mortgagee Letter 2011-22. Included in the SF Handbook condo project approval section is policy guidance around FHA’s new Single-Unit Approval process.