How to Add Wells Fargo Cards to a Digital Wallet Tour the Guided Demos for Androidtm and Apple® Devices at Featuredemos.Wf.Com/En/Home

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Public Bank Unionpay Lifestyle Debit Card Product Disclosure Sheet

PRODUCT DISCLOSURE SHEET Public Bank Berhad (6463-H) Read this Product Disclosure Sheet before you PB Visa/MasterCard Lifestyle Debit – Generic decide to take up the PB Visa/MasterCard/Union Pay Lifestyle Debit. Be sure to also read the PB Visa/MasterCard Lifestyle Debit – Basic general terms and conditions. Savings Account/Basic Current Account PB UnionPay Lifestyle Debit – PB UnionPay Savings Account Date: 1. What is this product about? PB Visa/MasterCard/UnionPay Lifestyle Debit is a two-in-one card combining Visa/MasterCard/ UnionPay debit card and ATM functions. The card is linked to the Savings Account/Current Account/Basic Savings Account/Basic Current Account/PB UnionPay Savings Account (“Banking Account”) of the individual and any expenditure will be deducted directly from the Banking Account. This is a PB Visa/MasterCard/UnionPay Lifestyle Debit, a payment instrument which allows you to pay via a direct deduction of the cost for goods and services from your Banking Account at participating retail and service outlets. You are required to maintain a Banking Account with us, to be linked to your PB Visa/MasterCard/UnionPay Lifestyle Debit. If you close your Banking Account maintained with us, your PB Visa/MasterCard/UnionPay Lifestyle Debit will be automatically cancelled. 2. What are the fees and charges I have to pay? (i) Annual Fee x Generic/PB UnionPay Savings Account: RM8.00 x Basic Savings Account/Basic Current Account: Waived (subject to eight (8) ATM cash withdrawals and six (6) over-the-counter withdrawals per month*) *Note: Fee for exceeding the threshold will be RM1.00 per transaction. -

Chinese Online Payment Platforms for Their Individual Needs

SNAPSHOT GUIDE TO ONLINE PAYMENT PLATFORMS FOR CHINESE VISITORS JULY 2017 OVERVIEW The use of online payment platforms has reshaped the way people pay for goods and services in China. Over the past five years, financial transactions are increasingly being handled through the use of advanced technology in a smartphone device, creating a fast and easy way for customers to pay for goods and services. While there are over 700 million registered users of online payment platforms in China – who complete approximately 380 million transactions a day – use of these platforms in Australia is relatively limited. In the year ending March 2017, 1.2 million Chinese visited Australia (up 12% from the previous year). Chinese visitors to Australia are the highest spending ($9.2 billion in 2016, or around $8,000 per visitor). Integrating online payment platforms recognised by Chinese visitors into business operations provides Australian businesses significant revenue yield opportunities and options better aligned to customer expectations. ONLINE PAYMENT PLATFORMS Also known as a digital wallet or e-wallet, these platforms are linked to a bank account, where transactions are processed without the use of a bank card i.e. similar to the way PayPal works. Online payment platforms can be used for purchases online or in-person. How an online payment platform works: Using a payment platform app, the customer generates a one- time QR code on their smartphone. The merchant uses a small device to scan the QR code given by the customer to process payment for the purchase of goods or services. In Australia, funds are in the merchant’s account within two business days after the date of transaction. -

(Automated Teller Machine) and Debit Cards Is Rising. ATM Cards Have A

Consumer Decision Making Contest 2001-2002 Study Guide ATM/Debit Cards The popularity of ATM (automated teller machine) and debit cards is rising. ATM cards have a longer history than debit cards, but the National Consumers League estimates that two-thirds of American households are likely to have debit cards by the end of 2000. It is expected that debit cards will rival cash and checks as a form of payment. In the future, “smart cards” with embedded computer chips may replace ATM, debit and credit cards. Single-purpose smart cards can be used for one purpose, like making a phone call, or riding mass transit. The smart card keeps track of how much value is left on your card. Other smart cards have multiple functions - serve as an ATM card, a debit card, a credit card and an electronic cash card. While this Study Guide will not discuss smart cards, they are on the horizon. Future consumers who understand how to select and use ATM and debit cards will know how to evaluate the features and costs of smart cards. ATM and Debit Cards and How They Work Electronic banking transactions are now a part of the American landscape. ATM cards and debit cards play a major role in these transactions. While ATM cards allow us to withdraw cash to meet our needs, debit cards allow us to by-pass the use of cash in point-of-sale (POS) purchases. Debit cards can also be used to withdraw cash from ATM machines. Both types of plastic cards are tied to a basic transaction account, either a checking account or a savings account. -

Past Policy Updates

Past Policy Updates This page shows important changes that were made to the PayPal service, its User Agreement, or other policies. Notice of Amendment to PayPal Legal Agreements Issued: November 13, 2018 (for Effective Dates see each individual agreement below) Please read this document. We’re making changes to the legal agreements that govern your relationship with PayPal. We encourage you to carefully review this notice to familiarise yourself with the changes that are being made. You do not need to do anything to accept the changes as they will automatically come into effect on the Effective Dates shown below. Should you decide you do not wish to accept them you can notify us before the above date to close your account immediately without incurring any additional charges. Please review the current Legal Agreements in effect. Notice of amendment to the PayPal User Agreement. Effective Date: November 13, 2018 1. Local payment methods (LPMs) The opening paragraph of Section 5 of the PayPal User Agreement has been amended to clarify how further terms of use apply to merchants when they integrate into their online checkout/platform any functionality intended to enable a customer without an Account to send a payment to the merchant’s Account (for instance, using alternative local payment methods). This includes the PayPal Local Payment Methods Agreement. The opening paragraph of Section 5 now reads as follows: “5. Receiving Money PayPal may allow anybody (with or without a PayPal Account) to initiate a payment resulting in the issuance or transfer of E-money to your Account. By integrating into your online checkout/platform any functionality intended to enable a payer without an Account to send a payment to your Account, you agree to all further terms of use of that functionality which PayPal will make available to you on any page on the PayPal or Braintree website (including any page for developers and our Legal Agreements page) or online platform. -

NEW CARD MOBILE APP Soon, You Can Manage Your Hawaii Central Credit Card Anytime, Anywhere with Our New Mobile App

APRIL 2021 COMING SOON NEW CARD MOBILE APP Soon, you can manage your Hawaii Central credit card anytime, anywhere with our new mobile app. • View credit card transactions Look for our NEW HCFCU Cards App • View current card balance in the upcoming months! • View minimum payment due & next due date • Setup card controls & alert notifications for your credit card DOWNLOAD ON: • Lock & unlock your credit card on-the-go • Make a payment • Report a lost or stolen credit card VIEW CARD OVERVIEW Check Balances View Payment Due Dates CONTROL Lock Cards YOUR SPENDING Set up Card Controls and Alerts based on your chosen criteria. FOR ATTENDING OUR 2021 ANNUAL MEETING Mahalo Our 83nd Annual Meeting was held virtually on Saturday, March 13, 2021. Hawaii Central Board Chairman Neil Shimogawa highlighted our successes in 2020 and Alan Yasuda, Sam Aucoin, and Ariel Chun were re-elected to serve on the Board of Directors. Download a copy of the 2020 Annual Report on our website. HawaiiCentral.org/2020-annual-report NOTICE TO OUR MEMBERS MARCH As of March 31, 2021, American Express has discontinued travelers checks; therefore, we will no longer be issuing travelers checks after March 31st. Members who still have travelers checks after 3/31/21 will 31 still be able to use them as normal. HawaiiCentral.org | Routing #321378990 FEDERALLY INSURED BY NCUA Simplify Your Life with One Card. As a Central Checking member, you’re able to get our FREE VISA® Debit Card! With our VISA Debit Card, you can access your Central Checking Account how you wish and whenever you want. -

Encrypted Traffic Management for Dummies®, Blue Coat Systems Special Edition Published by John Wiley & Sons, Inc

These materials are © 2015 John Wiley & Sons, Inc. Any dissemination, distribution, or unauthorized use is strictly prohibited. Encrypted Traffic Management Blue Coat Systems Special Edition by Steve Piper, CISSP These materials are © 2015 John Wiley & Sons, Inc. Any dissemination, distribution, or unauthorized use is strictly prohibited. Encrypted Traffic Management For Dummies®, Blue Coat Systems Special Edition Published by John Wiley & Sons, Inc. 111 River St. Hoboken, NJ 07030‐5774 www.wiley.com Copyright © 2015 by John Wiley & Sons, Inc., Hoboken, New Jersey No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning or otherwise, except as permitted under Sections 107 or 108 of the 1976 United States Copyright Act, without the prior written permission of the Publisher. Requests to the Publisher for permission should be addressed to the Permissions Department, John Wiley & Sons, Inc., 111 River Street, Hoboken, NJ 07030, (201) 748‐6011, fax (201) 748‐6008, or online at http://www.wiley.com/go/permissions. Trademarks: Wiley, For Dummies, the Dummies Man logo, The Dummies Way, Dummies.com, Making Everything Easier, and related trade dress are trademarks or registered trademarks of John Wiley & Sons, Inc. and/or its affiliates in the United States and other countries, and may not be used without written permission. Blue Coat Systems and the Blue Coat logo are trademarks or registered trade- marks of Blue Coat Systems, Inc. All other trademarks are the property of their respective owners. John Wiley & Sons, Inc., is not associated with any product or vendor mentioned in this book. -

Discovery Issues. (Gaudreau, Holly) (Filed on 2/18/2011)

Sony Computer Entertainment America LLC v. Hotz et al Doc. 85 February 18, 2011 VIA HAND DELIVERY AND EMAIL AT JCSpo~and. uscourts.gov Magistrate Judge Joseph C. Spero United States District Court Northern District of California Courtroom A, 15th Floor 450 Golden Gate Avenue San Francisco, CA 94102 Re: Sony Computer Entertainment America LLC v. Hotz, et a!., Case No. C-L 1-00167 SI (N.D. Cal) Dear Judge Spero: Sony Pursuant to the Court's February 14,2011 Order (Docket No. 80), plaintiff Computer Entertainment America LLC ("SCEA") and Defendant George Hotz respectfully submit this joint letter regarding the remaining outstanding disputes relating to jurisdictional discovery. Á. Case Background On January 11,2011, SCEA filed a complaint against Mr. Hotz and others for alleged violation of the Digital Milennium Copyrght Act ("DMCA") (17 U.S.c. §1201), the Computer Fraud and Abuse Act ("CFAA") (18 U.S.C. § 1030), the Copyright Act (17 U.S.C. §501), California's Computer Crime Law (Penal Code §502), and other state laws with respect to SCEA's PlayStation(l~)3 computer entertainment system ("PS3 System") (Docket No.1). SCEA also moved for a Temporary Restraining Order against Mr. Hotz based on its claims under the DMCA and CFAA. (Docket No.2). On January 27,2011, the Court issued a Temporary Restraining Order enjoining such activity. (Docket No. 50). The parties also submitted limited briefing on the question of whether the Court has personal jurisdiction over Mr. Hotz. (Docket Personal Nos. 32,46,47) On February 2,2011, Mr. Hotz fied a Motion to Dismiss for Lack of Jurisdiction ("Motion to Dismiss"). -

CONSUMER DEBIT CARD ATM CARD Look for These Logos at ATM

CONSUMER DEBIT CARD ATM CARD Make purchases plus get cash fast at ATMs Get cash fast at ATMs Applicant Name: New Student _____________________________________________________________ Card Type: Sunset Eagle Your card and PIN will be sent to the address on your account statement. Please speak to an Account Representative for special mailing __________________________________ CHECKING ACCOUNT NUMBER accommodations. (Required for Debit Card __________________________________ Last 4 digits of Applicant’s Social Security Number: ___________________ SECONDARY CHECKING ACCOUNT NUMBER __________________________________ Daytime Phone: Evening or Message Phone: SAVINGS ACCOUNT NUMBER __________________________ __________________________ __________________________________ Reason for new card (lost, damage, etc.) I hereby request that I be issued a First Bank Consumer Debit card or a ATM card and Personal Identification Number for use at merchant locations, point-of-sale terminals (Consumer Debit Card only) and automated teller machines (ATMs) to access my account(s) at First Bank. I understand that I may use my card to access my savings account through an ATM only. I also acknowledge receipt of an Electronic Funds Transfer Disclosure and a Cardholder Agreement, and understand that use of my Consumer Debit Card or ATM card shall governed by the terms and conditions applicable to my account(s), to the terms of the Cardholder Agreement, by laws, rules, regulations or applicable law, and such terms, conditions, and/or amendments as may be established from time to time and communicated to me in writing. ________ As the parent/guardian on this account, I understand that I am responsible for the Please Initial transactions conducted by the minor owner. Applicant’s Signature Date If applicable, Parent Signature Date In order to expedite the processing of your application form, please remember: 1. -

How Mpos Helps Food Trucks Keep up with Modern Customers

FEBRUARY 2019 How mPOS Helps Food Trucks Keep Up With Modern Customers How mPOS solutions Fiserv to acquire First Data How mPOS helps drive food truck supermarkets compete (News and Trends) vendors’ businesses (Deep Dive) 7 (Feature Story) 11 16 mPOS Tracker™ © 2019 PYMNTS.com All Rights Reserved TABLEOFCONTENTS 03 07 11 What’s Inside Feature Story News and Trends Customers demand smooth cross- Nhon Ma, co-founder and co-owner The latest mPOS industry headlines channel experiences, providers of Belgian waffle company Zinneken’s, push mPOS solutions in cash-scarce and Frank Sacchetti, CEO of Frosty Ice societies and First Data will be Cream, discuss the mPOS features that acquired power their food truck operations 16 23 181 Deep Dive Scorecard About Faced with fierce eTailer competition, The results are in. See the top Information on PYMNTS.com supermarkets are turning to customer- scorers and a provider directory and Mobeewave facing scan-and-go-apps or equipping featuring 314 players in the space, employees with handheld devices to including four additions. make purchasing more convenient and win new business ACKNOWLEDGMENT The mPOS Tracker™ was done in collaboration with Mobeewave, and PYMNTS is grateful for the company’s support and insight. PYMNTS.com retains full editorial control over the findings presented, as well as the methodology and data analysis. mPOS Tracker™ © 2019 PYMNTS.com All Rights Reserved February 2019 | 2 WHAT’S INSIDE Whether in store or online, catering to modern consumers means providing them with a unified retail experience. Consumers want to smoothly transition from online shopping to browsing a physical retail store, and 56 percent say they would be more likely to patronize a store that offered them a shared cart across channels. -

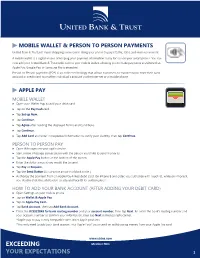

Mobile Wallet Guide

MOBILE WALLET & PERSON TO PERSON PAYMENTS United Bank & Trust just made shopping even easier! Using your phone to pay is faster, safer, and more convenient. A mobile wallet is a digital means of keeping your payment information ready for use on your smart-phone. You can now add your United Bank & Trust debit card to your mobile wallet, allowing you to make payments anywhere that Apple Pay, Google Pay, or Samsung Pay is accepted. Person-to-Person payments (P2P) is an online technology that allows customers to transfer funds from their bank account or credit card to another individual’s account via the Internet or a mobile phone. APPLE PAY MOBILE WALLET ▶ Open your Wallet App to add your debit card. ▶ Tap on the Pay Cash card. ▶ Tap Set up Now. ▶ Tap Continue. ▶ Tap Agree after reading the displayed Terms and Conditions. ▶ Tap Continue. ▶ Tap Add Card and enter in requested information to verify your identity, then tapContinue. PERSON TO PERSON PAY ▶ Open iMessages on your apple device. ▶ Start a new iMessage conversation with the person you’d like to send money to. ▶ Tap the Apple Pay button at the bottom of the screen. ▶ Enter the dollar amount you would like to send. ▶ Tap Pay or Request. ▶ Tap the Send Button (it is a white arrow in a black circle.) ▶ Authorize the payment from an Apple Pay-linked debit card. On iPhone 8 and older, you authorize with Touch ID, while on iPhone X, you double-click the side button to activate Face ID for authorization. HOW TO ADD YOUR BANK ACCOUNT (AFTER ADDING YOUR DEBIT CARD) ▶ Open Settings on your mobile phone. -

Mobile Payments

Mobile Payments - A study of the emerging payments ecosystem and its inhabitants while building a business case. By: Cherian Abraham Principal Analyst – Mobile Commerce & Payments Practice / Co-Founder - DROP Labs Twitter @ http://twitter.com/cherian abraham LinkedIn @ http://www.linkedin.com/in/cherianabraham For more information on this study and associated research, contact me at EXECUTIVE SUMMARY: The advent of the ubiquitous smart phone has along with it brought dramatic shifts in customer behavior and payment modalities. Banks are finding themselves in an unenviable position of choosing to wait until a secure and safe standard emerges for "Digital", or take the plunge in to these murky payment waters. There is a battle waging for the customer mind-share and emerging revenue streams, between traditional and non-traditional players - who are ever more emboldened by advances in technology and disappearing barriers to entry. The objective of this study is to build a business case for banks evaluating the opportunities and challenges present in building out mobile payment solutions, including direct and indirect revenue generation. This study paints a roadmap of current mobile payment initiatives undertaken by Financial institutions, MNO's and technology upstarts, and to highlight the risks of building payment solutions which are not centered on the payment context. This study summarizes the challenges ahead for mobile payments, including a lack of interoperability, consumer apathy and a general lack of understanding of its merits. It is targeted at financial institutions that may be making first steps, by building out their own mobile wallet initiatives or partnering with others, and seeks clarity. -

Paypal Holdings, Inc

PAYPAL HOLDINGS, INC. (NASDAQ: PYPL) Second Quarter 2021 Results San Jose, California, July 28, 2021 Q2’21: TPV reaches $311 billion with more than 400 million active accounts • Total Payment Volume (TPV) of $311 billion, growing 40%, and 36% on an FX-neutral basis (FXN); net revenue of $6.24 billion, growing 19%, and 17% on an FXN basis • GAAP EPS of $1.00 compared to $1.29 in Q2’20, and non-GAAP EPS of $1.15 compared to $1.07 in Q2’20 • 11.4 million Net New Active Accounts (NNAs) added; ended the quarter with 403 million active accounts FY’21: Raising TPV and reaffirming full year revenue outlook • TPV growth now expected to be in the range of ~33%-35% at current spot rates and on an FXN basis; net revenue expected to grow ~20% at current spot rates and ~18.5% on an FXN basis, to ~$25.75 billion • GAAP EPS expected to be ~$3.49 compared to $3.54 in FY’20; non-GAAP EPS expected to grow ~21% to ~$4.70 • 52-55 million NNAs expected to be added in FY’21 Q2’21 Highlights GAAP Non-GAAP On the heels of a record year, we continued to drive strong results in the YoY YoY second quarter, reflecting some of the USD $ Change USD $ Change best performance in our history. Our platform now supports 403 million Net Revenues $6.24B 17%* $6.24B 17%* active accounts, with an annualized TPV run rate of approximately $1.25 trillion. Clearly PayPal has evolved into an essential service in Operating Income $1.13B 19% $1.65B 11% the emerging digital economy.” Dan Schulman EPS $1.00 (23%) $1.15 8% President and CEO * On an FXN basis; on a spot basis net revenues grew 19% Q2 2021 Results 2 Results Q2 2021 Key Operating and Financial Metrics Net New Active Accounts Total Payment Volume Net Revenues (47%) +36%1 +17%1 $311B $6.24B 21.3M $5.26B $222B 11.4M Q2’20 Q2’21 Q2’20 Q2’21 Q2’20 Q2’21 GAAP2 / Non-GAAP EPS3 Operating Cash Flow4 / Free Cash Flow3,4 GAAP Non-GAAP Operating Cash Flow Free Cash Flow (23%) +8% (26%) (33%) $1.29 $1.77B $1.15 $1.58B $1.07 $1.00 $1.31B $1.06B Q2’20 Q2’21 Q2’20 Q2’21 Q2’20 Q2’21 Q2’20 Q2’21 1.