Display's the Thing: the Real Stakes in the Conflict Over High Resolution Displays

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Depthq HD 3D Projector 2009 Lightspeed PDF WEB

Affordable HD3D3D From the originators of portable 3D projection. The New DepthQ® HD 3D Video Projector The world’s rst portable WXGA stereoscopic 3D projector. DepthQ® HD 3D projectors oer rock-solid, 120Hz stereo 3D at 1280x720 resolution. These bright, professional-level 3D projectors can easily display 10 ft (3.0m) diagonal 3D high-denition images using the latest Texas Instruments DLP® and BrilliantColor™ technologies - for stunning colors, a 2000:1 contrast ratio, and a truly unprecedented level of price-performance. Aordable – A fraction of the cost of other single- lens 3D projectors Flicker-free, 120 Hz HD 3D with DLP ® Quality – ® DepthQ HD 3D Projector depthQ.com BrilliantColor TM technology Portable – At 6.9 pounds it ts under your arm and takes less than 5 minutes to set up First in its class: Lightspeed Design presents the portable stereo 3D solution. The DepthQ® HD 3D video projector is a revolutionary lightweight single lens Versatile – Work live in 3D-enabled applications; quality projector capable of achieving frame rates of 120 Hz. When used with a control 3D lm or video game development; stereoscopic 3D image source and liquid crystal shutter glasses, DepthQ® HD bring immersive 3D games into your home 3D projectors will provide a rock-solid high-denition stereo 3D experience. Product Design, Engineering and Research The new DepthQ® HD 3D projector (patent-pending) is a product of Stereo 3D is scientically proven as the most eective way to communicate visual ideas. The Lightspeed Design Inc., co-developed new DepthQ® HD 3D projectors make stereo viewing an aordable choice for anyone working with InFocus Corporation. -

Screen Size Selection

Screen Size Selection One of the most important decisions in screen selection is to determine the correct size of screen based upon the dimensions of the audience area and the projection format(s) to be used. In some situations, these two questions yield the same answer; in • Ceiling Height—The bottom of the screen should be approximately others they do not and compromises must be made. Here are the key 40–48" above the floor in a room with a level floor and several rows considerations— of seats. In rooms with theatre seating or only one or two rows, • Audience Area—In determining the correct screen size in relation to such as a home theatre, the bottom of the screen should usually be the audience area, the goal is to make the screen large enough so 24–36" above the floor. Try to make sure that the lower part of the those in the rear of the audience area can read the subject matter screen will be visible from all seats. Extra drop may be required to easily, but not so large that those in the front of the audience area position the screen at a comfortable viewing level in a room with a have difficulty seeing the full width of the projected image. high ceiling. • Height—Use the following formulas for calculating screen height for • Projection Format—Once you have determined the correct size of maximum legibility. For 4:3 moving video and entertainment, screen screen for the audience area, that size may be modified height should be at least 1/6 the distance from the screen to the based upon the type(s) of projection equipment to be used. -

How to Wire Motorized Projection Screens Cinemasource , 18 Denbow Rd., Durham, NH 03824

How To Wire Motorized Projection Screens CinemaSource , 18 Denbow Rd., Durham, NH 03824 www.cinemasource.com CinemaSource Technical Bulletins. Copyright 2002 by CinemaSource, Inc. All rights reserved. Printed in the United States of America. No part of this bulletin may be used or reproduced in any manner whatsoever without written permission, except in brief quotations embodied in critical reviews. CinemaSource is a registered federal trademark. For information contact: The CinemaSource Press, 18 Denbow Rd. Durham, NH 03824 How to Wire Motorized Projection Screens Motorized Screen Wiring • Using up/down wall switches ----------------------------------------------------- Page5 • Screen control using relays ------------------------------------------------------- Page 6 • IR wireless screen control --------------------------------------------------------- Page 8 • RF wireless screen control -------------------------------------------------------- Page 9 • Screen control via current sensing devices ----------------------------------- Page 10 • X-10 screen control ------------------------------------------------------------------ Page 12 Glossary • A collection of projection screen-related terminology ----------------------- Page 14 SCREEN MANUFACTURERS PROFILED IN THIS GUIDE: DA-LITE SCREEN, 3100 North Detroit St., Warsaw, IN 46581 800-622-3737, www.da-lite.com DRAPER, 411 S. Pearl St., Spiceland, IN 47385 800-238-7999, www.draperinc.com VUTEC Corporation, 5900 Stirling Road, Hollywood, FL 33021 800-770-4700, www.vutec.com STEWART FILMSCREEN, -

FOCUS Mini Video Projector

Quick Start Guide AKASO FOCUS Mini Video Projector V1.3 CONTENTS English 01 - 13 Español 14 - 26 日本語 27 - 39 English PROJECTOR BUTTONS & FUNCTIONS 1 2 3 4 5 6 7 8 9 10 11 12 13 1 Focusing Wheel 8 Power Bank Mode 2 Return 9 DC 3 Forward 10 USB 4 Backward 11 HDMI 5 OK 12 Earphone 6 Projection Mode 13 Memory Card Port 7 Power Button Note: When in the EZWire/EZCast/HDMI interface, the button function is changed. Forward: Change to volume + Backward: Change to volume - 1 INFRARED REMOTE CONTROL On/Off Mute EZCast Operation No Function HDMI Operation Directions OK Menu Return Home Vol +/- Note: When using the IR remote control, you should aim at the projector rather than screen. POWER ON/OFF 1. Pull the power button to the left and hold it for about four seconds until the green indicator on the projector bottom is lit up, then the projector starts to work. 2. Turn the power button to the left again and hold it for about two seconds to shut down the projector. 3. Turn the power button to the right to lock the button, then the projector can be used as a power bank. 2 POWER BANK MODE AND CHARGING METHOD 1. When the projector is in power bank mode/ projection mode, the projector can charge other devices via USB port. 2. In order to improve charging efficiency, please charge the projector with the original power adapter in power bank mode. 3. The number of indicators represent remaining capacity of battery. -

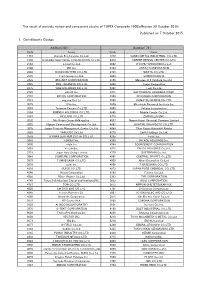

Published on 7 October 2016 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 31 October 2016) Published on 7 October 2016 1. Constituents Change Addition( 70 ) Deletion( 60 ) Code Issue Code Issue 1810 MATSUI CONSTRUCTION CO.,LTD. 1868 Mitsui Home Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 2196 ESCRIT INC. 2117 Nissin Sugar Co.,Ltd. 2198 IKK Inc. 2124 JAC Recruitment Co.,Ltd. 2418 TSUKADA GLOBAL HOLDINGS Inc. 2170 Link and Motivation Inc. 3079 DVx Inc. 2337 Ichigo Inc. 3093 Treasure Factory Co.,LTD. 2359 CORE CORPORATION 3194 KIRINDO HOLDINGS CO.,LTD. 2429 WORLD HOLDINGS CO.,LTD. 3205 DAIDOH LIMITED 2462 J-COM Holdings Co.,Ltd. 3667 enish,inc. 2485 TEAR Corporation 3834 ASAHI Net,Inc. 2492 Infomart Corporation 3946 TOMOKU CO.,LTD. 2915 KENKO Mayonnaise Co.,Ltd. 4221 Okura Industrial Co.,Ltd. 3179 Syuppin Co.,Ltd. 4238 Miraial Co.,Ltd. 3193 Torikizoku co.,ltd. 4331 TAKE AND GIVE. NEEDS Co.,Ltd. 3196 HOTLAND Co.,Ltd. 4406 New Japan Chemical Co.,Ltd. 3199 Watahan & Co.,Ltd. 4538 Fuso Pharmaceutical Industries,Ltd. 3244 Samty Co.,Ltd. 4550 Nissui Pharmaceutical Co.,Ltd. 3250 A.D.Works Co.,Ltd. 4636 T&K TOKA CO.,LTD. 3543 KOMEDA Holdings Co.,Ltd. 4651 SANIX INCORPORATED 3636 Mitsubishi Research Institute,Inc. 4809 Paraca Inc. 3654 HITO-Communications,Inc. 5204 ISHIZUKA GLASS CO.,LTD. 3666 TECNOS JAPAN INCORPORATED 5998 Advanex Inc. 3678 MEDIA DO Co.,Ltd. 6203 Howa Machinery,Ltd. 3688 VOYAGE GROUP,INC. 6319 SNT CORPORATION 3694 OPTiM CORPORATION 6362 Ishii Iron Works Co.,Ltd. 3724 VeriServe Corporation 6373 DAIDO KOGYO CO.,LTD. 3765 GungHo Online Entertainment,Inc. -

CP-A222WN LCD Projector

CP-A222WN LCD Projector Fully featured ultra short throw LCD projector with network capabilities and a low operating cost all in a portable design. Ultra Short Throw Series Hitachi’s CP-A222WN ultra short throw LCD projector combines an array of advanced features in a compact, portable design perfectly suited for class- rooms of any size. Small in size, but big on performance, the CP-A222WN provides vibrant image quality, cost-effective operation, and long-lasting Key Features reliability. The CP-A222WN incorporates a cloning function which enables you ■ XGA 1024 x 768 resolution to copy setting data from one projector to others of the same model via USB ■ 2,200 ANSI lumens white/color output memory. Plus, Hitachi’s Intelligent Eco Mode with ImageCare combines optimal ■ 4000:1 contrast ratio picture performance with energy savings for a lower total cost of ownership. ■ HDMI 1 input For added peace of mind, Hitachi’s CP-A222WN is also backed by a generous ■ 4,000 hours hybrid filter* ■ 3,000 hours lamp life (Standard mode) warranty and our world-class service and support programs. and 5,000 hours lamp life (Eco mode)** ■ ImageCare technology ■ Wireless compatible CP-A222WN 1.800.HITACHI [email protected] hitachi-america.us/projectors CP-A222WN LCD Projector UNIQUE FEATURES Network Control, Maintenance and Security Drawing Function with Optional Tablet (TB-1) Embedded networking gives you the ability to manage and control multiple projectors The optional Hitachi wireless tablet and pen allows you to over your LAN. Features include scheduling engage your audience by annotating over images shown on of events, centralized reporting, image the projector. -

CORPORATE PROFILE Corporate Philosophy

CORPORATE PROFILE Corporate Philosophy Mission Statement Creating Value for Customers via New Ideas ITO Corporation's mission is to contribute to our customers and to society via the values born from new pairings and findings. We create opportunities that previously did not exist by connecting together objects, people, companies, and ideas. We strive for a virtuous cycle where we provide new opportunities and value to our customers, which in turn contributes to the products and services born into the world. Value Statement An Organization Which Excites All In order for us to provide customers and society with exciting new opportu- nities, we ourselves must be an innovative organization. Additionally, for us to increase our customer's level of satisfaction and to take actions which contrib- ute to the world, it is important that we spend our time in a valuable way. To achieve the above, we value the following as an organization: Respect each other and understand the value that diversity brings. No discrimination based on gender, nationality, age, experience, etc. Cultivate a harmonious and encouraging work culture, and support the efforts of others Strive for a fulfilling life together, not only with work but also by valuing family and society Provide employment, skill development, and opportunities for advance- ment to those with motivation Ensure that our actions are always fair and moral Vision Statement Improve the World via Moving Equipment Throughout the ages, moving components and equipment have freed people from heavy la- bor, enabled transportation to remote locations, and enriched the lives of people everywhere. During the foundation of our company, we played a role in the post-war recovery by providing to people electrical machinery and other moving items that could be used in the burnt fields of Tokyo. -

EK-120UK/EK-122X WUXGA/XGA Long Life Lamp Portable LCD Projector

EK-120UK/EK-122X WUXGA/XGA Long Life Lamp Portable LCD Projector 4,400 Lumens* WUXGA (1920 x 1200) 4,700 Lumens* XGA (1024 x 768) 3LCD Projector EK-120UK and EK-122XK have a big with Innovative Long Life Lamp advantage for reducing Total Cost of Ownership (TCO) with a long life lamp. Reduction of maintenance by Long Life Lamp This new model can be provided beautiful, high-contrast and clear images Built-in Innovative Long Life Lamp achieves longer life time of 2.5 times at Normal mode and 2 times at Eco mode than conventional models'. It offers a Total Cost of Ownership (TCO) up to the life of the projector come. reduction considerably. 10,000 hours (Normal mode) 20,000 hours Key Features (Eco mode) EK-120 series ・ Long Life Lamp 4,000 hours 2.5 times longer (Normal mode) Conventional model 10,000 hours 2 times longer 20,000 hours (Eco) (Eco mode) 10,000 hours (Normal) 0 10,000 20,000 (hrs) ・ High Contrast Ratio 15,000 : 1 High Contrast Ratio 15,000:1 The realization of high contrast has made it possible to realistically express the three-dimensional ・ Optical Zoom 1.2 x effect and the depth of a dark image. ・ Digital Input HDMI x 2 ・Flexible installation - Keystone Correction Clearer Image H: +/- 15 ° V: +/- 30 ° Recommended Application Corner Correction - Curved Correction (EK-122X only) - Classrooms - Conference Rooms ・Quick Power OFF EK-120UK and EK-122X are suitable for education and corp. market such as classrooms ・Built-in 10-Watt Audio Speaker and Conference rooms since they are compact and easy to install with Auto set up function, Horizontal and Vertical Keystone Correction, and Corner correction. -

Video Processor, Video Upconversion & Signal Switching

81LumagenReprint 3/1/04 1:01 PM Page 1 Equipment Review Lumagen VisionPro™ Video Processor, Video Upconversion & Signal Switching G REG R OGERS Lumagen VisionPro™ Reviewer’s Choice The Lumagen VisionPro™ Video Processor is the type of product that I like to review. First and foremost, it delivers excep- tional performance. Second, it’s an out- standing value. It provides extremely flexi- ble scaling functions and valuable input switching that isn’t included on more expen- sive processors. Third, it works as adver- tised, without frustrating bugs or design errors that compromise video quality or ren- Specifications: der important features inoperable. Inputs: Eight Programmable Inputs (BNC); Composite (Up To 8), S-Video (Up To 8), Manufactured In The U.S.A. By: Component (Up To 4), Pass-Through (Up To 2), “...blends outstanding picture SDI (Optional) Lumagen, Inc. Outputs: YPbPr/RGB (BNC) 15075 SW Koll Parkway, Suite A quality with extremely Video Processing: 3:2 & 2:2 Pulldown Beaverton, Oregon 97006 Reconstruction, Per-Pixel Motion-Adaptive Video Tel: 866 888 3330 flexible scaling functions...” Deinterlacing, Detail-Enhancing Resolution www.lumagen.com Scaling Output Resolutions: 480p To 1080p In Scan Line Product Overview Increments, Plus 1080i Dimensions (WHD Inches): 17 x 3-1/2 x 10-1/4 Price: $1,895; SDI Input Option, $400 The VisionPro ($1,895) provides two important video functions—upconversion and source switching. The versatile video processing algorithms deliver extensive more to upconversion than scaling. Analog rithms to enhance edge sharpness while control over input and output formats. Video source signals must be digitized, and stan- virtually eliminating edge-outlining artifacts. -

FC EXPO / PV EXPO / PV SYSTEM EXPO / BATTERY JAPAN / INT'l SMART GRID EXPO Dates: : Feb

FC EXPO / PV EXPO / PV SYSTEM EXPO / BATTERY JAPAN / INT'L SMART GRID EXPO Dates: : Feb. 28 (Wed) - Mar. 2 (Fri), 2018 WIND EXPO / BIOMASS EXPO / THERMAL POWER EXPO Venue: Tokyo Big Sight, Japan Organised by: Reed Exhibitions Japan Ltd. Please refer to Exhibitor Directory for the detailed information of each exhibitor. ■ FC EXPO 2018 - 14th Int'l Hydrogen & Fuel Cell Expo ■ ● ABE KOHGYO CO., LTD. ● ACE INC., ● ADVANCED SCIENCE, TECHNOLOGY & MANAGEMENT ● AICHI SCIENCE & TECHNOLOGY FOUNDATION RESEARCH INSTITUTE OF KYOTO ● AIR LIQUIDE JAPAN ● AISINSEIKI CO., LTD. ● AIST ● ALPHASYSTEM INC. ● ANDREAS HOFER HOCHDRUCKTECHNIK GMBH ● APERAM ● ASIA PACIFIC FUEL CELL TECHNOLOGIES, LTD. ● ASTOM CORPORATION ● AVCARB LLC ● AVL LIST GMBH ● BALLARD POWER SYSTEMS INC. ● BECKER AIR TECHNO CO., LTD. ● BEIJING CHINATANK INDUSTRY CO,.LTD ● BEIJING TIANHAI INDUSTRY CO., LTD. ● BLOOM ENERGY JAPAN ● BORIT NV ● BROTHER INDUSTRIES LTD. ● BUSCH CLEAN AIR S.A. ● BUSCH VACUUM (SHANGHAI) CO., LTD. ● CANADIAN HYDROGEN AND FUEL CELL ASSOCIATION (CHFCA) ● CELEROTON AG ● CERPOTECH ● CHINA GREAT WALL INTERNATIONAL EXHIBITION CO., LTD. ● CHINO CORP. ● CHOFU KOSAN CO., LTD. ● CHOSHU INDUSTRY CO., LTD. ● CMR PROTOTECH ● CONVION LTD. ● CORRENS CORP. ● CROWN ADVANCED MATERIAL CO., LTD. ● CS CHEMICAL COMPANY ● CSA GROUP ● DFC CO., LTD. ● DM CARD JAPAN CO., LTD. ● DPOINT TECHNOLOGIES ● EG CORPORATION ● ELCOGEN AS ● ELCOGEN OY ● ELRINGKLINGER AG ● ENAPTER ● ENOAH INC. ● ENOMOTO CO., LTD. ● F-CELL SEPTEMBER 18/19, 2018 ● FRAUNHOFER INSTITUTE FOR MICROENGINEERING AND MICROSYSTEMS IMM ● FUEL CELL AND HYDROGEN, ELECTRIC MOBILITY NETWORK NRW ● FUEL CELL DEVELOPMENT INFORMATION CENTER ● FUJIKIN INC. ● FUJIKOATSU FLEXIBLEHOSE CO., LTD. ● FUJISEIKI ● FUKUDA CO., LTD. ● FUKUOKA INDUSTRIAL TECHNOLOGY CENTER ● FUKUOKA STRATEGY CONFERENCE FOR HYDROGEN ENERGY ● FUMATECH BWT GMBH ● FUTAMURA CHEMICAL CO., LTD. -

Published on 7 October 2015 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 30 October 2015) Published on 7 October 2015 1. Constituents Change Addition( 80 ) Deletion( 72 ) Code Issue Code Issue 1712 Daiseki Eco.Solution Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 1930 HOKURIKU ELECTRICAL CONSTRUCTION CO.,LTD. 2410 CAREER DESIGN CENTER CO.,LTD. 2183 Linical Co.,Ltd. 2692 ITOCHU-SHOKUHIN Co.,Ltd. 2198 IKK Inc. 2733 ARATA CORPORATION 2266 ROKKO BUTTER CO.,LTD. 2735 WATTS CO.,LTD. 2372 I'rom Group Co.,Ltd. 3004 SHINYEI KAISHA 2428 WELLNET CORPORATION 3159 Maruzen CHI Holdings Co.,Ltd. 2445 SRG TAKAMIYA CO.,LTD. 3204 Toabo Corporation 2475 WDB HOLDINGS CO.,LTD. 3361 Toell Co.,Ltd. 2729 JALUX Inc. 3371 SOFTCREATE HOLDINGS CORP. 2767 FIELDS CORPORATION 3396 FELISSIMO CORPORATION 2931 euglena Co.,Ltd. 3580 KOMATSU SEIREN CO.,LTD. 3079 DVx Inc. 3636 Mitsubishi Research Institute,Inc. 3093 Treasure Factory Co.,LTD. 3639 Voltage Incorporation 3194 KIRINDO HOLDINGS CO.,LTD. 3669 Mobile Create Co.,Ltd. 3197 SKYLARK CO.,LTD 3770 ZAPPALLAS,INC. 3232 Mie Kotsu Group Holdings,Inc. 4007 Nippon Kasei Chemical Company Limited 3252 Nippon Commercial Development Co.,Ltd. 4097 KOATSU GAS KOGYO CO.,LTD. 3276 Japan Property Management Center Co.,Ltd. 4098 Titan Kogyo Kabushiki Kaisha 3385 YAKUODO.Co.,Ltd. 4275 Carlit Holdings Co.,Ltd. 3553 KYOWA LEATHER CLOTH CO.,LTD. 4295 Faith, Inc. 3649 FINDEX Inc. 4326 INTAGE HOLDINGS Inc. 3660 istyle Inc. 4344 SOURCENEXT CORPORATION 3681 V-cube,Inc. 4671 FALCO HOLDINGS Co.,Ltd. 3751 Japan Asia Group Limited 4779 SOFTBRAIN Co.,Ltd. 3844 COMTURE CORPORATION 4801 CENTRAL SPORTS Co.,LTD. -

Approved Equipment Certification List As at 2019 April 16. the SMA Reserves the Right to Add Or Delete Any Item of Equipment from This List

Spectrum Management Authority of Jamaica (“the SMA”) Approved Equipment Certification List as at 2019 April 16. The SMA reserves the right to add or delete any item of equipment from this list. Manufacturer Model Description DELL C-UAS-DEL1 The transceiver will be used in computers to provide wireless connectivity to DELL computers Licensed Broadcom 802.11 BCM94312MCG Integrated transceiver device for use in 2.4GHz wireless system Licensed Broadcom BCM92046mPCle_FLSH Class 2 Bluetooth device Licensed Broadcom BCM92046MD_GEN Class 2 Bluetooth device Licensed BMW BTCoMB Bluetooth transceiver Licensed Nintendo RVL-021 Bluetooth Accessory Balance Board used with Nintendo Game Licensed Broadcom 802.11g BCM94312HMG PCI-E Half-minicard form factor Wireless LAN module Licensed Manufacturer Model Description Pegatron BT-180 BT-180 is a 2.4 GHz Bluetooth module for use in in a variety of end user product to provide bluetooth connectivity Licensed Ralink Technology RT2700E The RT2700E is an 802.11b/g/n WLAN Mini Card Corporation Licensed Rosemount Inc RM2510 Digital Transmission System Licensed Lite-On Technology Corp WN7600R-A Digital Transmission System 802.11 n/b/g WLAN PCI-e Card Licensed Lite-on Technology Corp WN7600R-MV Digital Transmission System 802.11 n/b/g WLAN PCI-e Card Licensed Lite-On Technology Corp WN7600-N Digital Transmission System 802.11 nb/g WLAN PCI-e Card Licensed Dust Networks XD M2140 Digital Transmission System Smart Mesh Wireless Mote Licensed Symbol Technologies Inc MC7596 Digital Transmission System EDA (Enterprise Digital Assistant) Licensed Manufacturer Model Description Broadcom BCM2045 MC7596 Broadcom BCM2045 Bluetooth reference design Symbol Technologies Inc.