To See the Evolution of Exchange Rates Regime

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

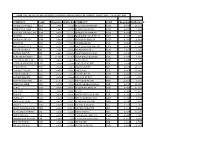

Valūtas Kods Valūtas Nosaukums Vienības Par EUR EUR Par Vienību

Valūtas kods Valūtas nosaukums Vienības par EUR EUR par vienību USD US Dollar 1,185395 0,843601 EUR Euro 1,000000 1,000000 GBP British Pound 0,908506 1,100708 INR Indian Rupee 87,231666 0,011464 AUD Australian Dollar 1,674026 0,597362 CAD Canadian Dollar 1,553944 0,643524 SGD Singapore Dollar 1,606170 0,622599 CHF Swiss Franc 1,072154 0,932702 MYR Malaysian Ringgit 4,913417 0,203524 JPY Japanese Yen 124,400574 0,008039 Chinese Yuan CNY 7,890496 0,126735 Renminbi NZD New Zealand Dollar 1,791828 0,558089 THB Thai Baht 37,020943 0,027012 HUF Hungarian Forint 363,032464 0,002755 AED Emirati Dirham 4,353362 0,229708 HKD Hong Kong Dollar 9,186936 0,108850 MXN Mexican Peso 24,987903 0,040019 ZAR South African Rand 19,467073 0,051369 PHP Philippine Peso 57,599396 0,017361 SEK Swedish Krona 10,351009 0,096609 IDR Indonesian Rupiah 17356,035415 0,000058 SAR Saudi Arabian Riyal 4,445230 0,224960 BRL Brazilian Real 6,644766 0,150494 TRY Turkish Lira 9,286164 0,107687 KES Kenyan Shilling 128,913350 0,007757 KRW South Korean Won 1342,974259 0,000745 EGP Egyptian Pound 18,626384 0,053687 IQD Iraqi Dinar 1413,981158 0,000707 NOK Norwegian Krone 10,925023 0,091533 KWD Kuwaiti Dinar 0,362319 2,759999 RUB Russian Ruble 91,339545 0,010948 DKK Danish Krone 7,442917 0,134356 PKR Pakistani Rupee 192,176964 0,005204 ILS Israeli Shekel 4,009399 0,249414 PLN Polish Zloty 4,576445 0,218510 QAR Qatari Riyal 4,314837 0,231758 XAU Gold Ounce 0,000618 1618,929841 OMR Omani Rial 0,455784 2,194020 COP Colombian Peso 4533,946955 0,000221 CLP Chilean Peso 931,726512 0,001073 -

France À Fric: the CFA Zone in Africa and Neocolonialism

France à fric: the CFA zone in Africa and neocolonialism Ian Taylor Date of deposit 18 04 2019 Document version Author’s accepted manuscript Access rights Copyright © Global South Ltd. This work is made available online in accordance with the publisher’s policies. This is the author created, accepted version manuscript following peer review and may differ slightly from the final published version. Citation for Taylor, I. C. (2019). France à fric: the CFA Zone in Africa and published version neocolonialism. Third World Quarterly, Latest Articles. Link to published https://doi.org/10.1080/01436597.2019.1585183 version Full metadata for this item is available in St Andrews Research Repository at: https://research-repository.st-andrews.ac.uk/ FRANCE À FRIC: THE CFA ZONE IN AFRICA AND NEOCOLONIALISM Over fifty years after 1960’s “Year of Africa,” most of Francophone Africa continues to be embedded in a set of associations that fit very well with Kwame Nkrumah’s description of neocolonialism, where postcolonial states are de jure independent but in reality constrained through their economic systems so that policy is directed from outside. This article scrutinizes the functioning of the CFA, considering the role the currency has in persistent underdevelopment in most of Francophone Africa. In doing so, the article identifies the CFA as the most blatant example of functioning neocolonialism in Africa today and a critical device that promotes dependency in large parts of the continent. Mainstream analyses of the technical aspects of the CFA have generally focused on the exchange rate and other related matters. However, while important, the real importance of the CFA franc should not be seen as purely economic, but also political. -

Country, Capital, Currency

List of all Countries, Capitals & Currencies of the World Country Capital Currency Afghanistan Kabul Afghan afghani Albania Tirana Albanian lek Algeria Agiers Algerian dinar Andorra Andorra la Vella Euro Angola Luanda Kwanza Antigua and Barbuda St. John’s East Caribbean dollar Argentina Buenos Aires Argentine peso Armenia Yerevan Armenian dram Australia Canberra Australian dollar Austria Vienna Euro Azerbaijan Baku Azerbaijani manat Bahamas Nassau Bahamian dollar Bahrain Manama Bahraini dinar Bangladesh Dhaka Bangladeshi taka Barbados Bridgetown Barbadian dollar Belarus Minsk Belarusian ruble Belgium Brussels Euro Belize Belmopan Belize dollar Benin Porto-Novo (official) West African CFA franc Bhutan Thimpu Bhutanese ngultrum Bolivia Sucre Bolivian boliviano Bosnia and Herzegovina Sarajevo Bosnia and Herzegovina convertible mark Botswana Gaborone Pula Brazil Brasília Brazilian real Brunei Bandar Seri Begawan Brunei dollar Bulgaria Sofia Bulgarian lev Burkina Faso Ouagadougou West African CFA franc Burundi Bujumbura Burundian franc Cambodia Phnom Penh Cambodian riel Cameroon Yaoundé Central African CFA franc Canada Ottawa Canadian dollar Cape Verde Praia Cape Verdean escudo Central African Republic Bangui Central African CFA franc Chad N’Djamena Central African CFA franc Chile Santiago Chilean peso China Beijing Chinese Yuan Renminbi Colombia Bogotá Colombian peso Comoros Moroni Comorian franc Costa Rica San José Costa Rican colon Côte d’Ivoire (Ivory Coast) Yamoussoukro (official),Abidjan West African CFA franc (seat of government) Croatia -

ZIMRA Rates of Exchange for Customs Purposes for Period 24 Dec 2020 To

ZIMRA RATES OF EXCHANGE FOR CUSTOMS PURPOSES FOR THE PERIOD 24 DEC 2020 - 13 JAN 2021 ZWL CURRENCY CODE CROSS RATEZIMRA RATECURRENCY CODE CROSS RATEZIMRA RATE ANGOLA KWANZA AOA 7.9981 0.1250 MALAYSIAN RINGGIT MYR 0.0497 20.1410 ARGENTINE PESO ARS 1.0092 0.9909 MAURITIAN RUPEE MUR 0.4819 2.0753 AUSTRALIAN DOLLAR AUD 0.0162 61.7367 MOROCCAN DIRHAM MAD 0.8994 1.1119 AUSTRIA EUR 0.0100 99.6612 MOZAMBICAN METICAL MZN 0.9115 1.0972 BAHRAINI DINAR BHD 0.0046 217.5176 NAMIBIAN DOLLAR NAD 0.1792 5.5819 BELGIUM EUR 0.0100 99.6612 NETHERLANDS EUR 0.0100 99.6612 BOTSWANA PULA BWP 0.1322 7.5356 NEW ZEALAND DOLLAR NZD 0.0173 57.6680 BRAZILIAN REAL BRL 0.0631 15.8604 NIGERIAN NAIRA NGN 4.7885 0.2088 BRITISH POUND GBP 0.0091 109.5983 NORTH KOREAN WON KPW 11.0048 0.0909 BURUNDIAN FRANC BIF 23.8027 0.0420 NORWEGIAN KRONER NOK 0.1068 9.3633 CANADIAN DOLLAR CAD 0.0158 63.4921 OMANI RIAL OMR 0.0047 212.7090 CHINESE RENMINBI YUANCNY 0.0800 12.5000 PAKISTANI RUPEE PKR 1.9648 0.5090 CUBAN PESO CUP 0.3240 3.0863 POLISH ZLOTY PLN 0.0452 22.1111 CYPRIOT POUND EUR 0.0100 99.6612 PORTUGAL EUR 0.0100 99.6612 CZECH KORUNA CZK 0.2641 3.7860 QATARI RIYAL QAR 0.0445 22.4688 DANISH KRONER DKK 0.0746 13.4048 RUSSIAN RUBLE RUB 0.9287 1.0768 EGYPTIAN POUND EGP 0.1916 5.2192 RWANDAN FRANC RWF 12.0004 0.0833 ETHOPIAN BIRR ETB 0.4792 2.0868 SAUDI ARABIAN RIYAL SAR 0.0459 21.8098 EURO EUR 0.0100 99.6612 SINGAPORE DOLLAR SGD 0.0163 61.2728 FINLAND EUR 0.0100 99.6612 SPAIN EUR 0.0100 99.6612 FRANCE EUR 0.0100 99.6612 SOUTH AFRICAN RAND ZAR 0.1792 5.5819 GERMANY EUR 0.0100 99.6612 -

Zimra Rates of Exchange for Customs Purposes for the Period 08 to 14 July

ZIMRA RATES OF EXCHANGE FOR CUSTOMS PURPOSES FOR THE PERIOD 08 TO 14 JULY 2021 USD BASE CURRENCY - USD DOLLAR CURRENCY CODE CROSS RATE ZIMRA RATE CURRENCY CODE CROSS RATE ZIMRA RATE ANGOLA KWANZA AOA 650.4178 0.0015 MALAYSIAN RINGGIT MYR 4.1598 0.2404 ARGENTINE PESO ARS 95.9150 0.0104 MAURITIAN RUPEE MUR 42.8000 0.0234 AUSTRALIAN DOLLAR AUD 1.3329 0.7503 MOROCCAN DIRHAM MAD 8.9490 0.1117 AUSTRIA EUR 0.8454 1.1829 MOZAMBICAN METICAL MZN 63.9250 0.0156 BAHRAINI DINAR BHD 0.3760 2.6596 NAMIBIAN DOLLAR NAD 14.3346 0.0698 BELGIUM EUR 0.8454 1.1829 NETHERLANDS EUR 0.8454 1.1829 BOTSWANA PULA BWP 10.9709 0.0912 NEW ZEALAND DOLLAR NZD 1.4232 0.7027 BRAZILIAN REAL BRL 5.1970 0.1924 NIGERIAN NAIRA NGN 410.9200 0.0024 BRITISH POUND GBP 0.7241 1.3810 NORTH KOREAN WON KPW 900.0228 0.0011 BURUNDIAN FRANC BIF 1983.5620 0.0005 NORWEGIAN KRONER NOK 8.7064 0.1149 CANADIAN DOLLAR CAD 1.2459 0.8026 OMANI RIAL OMR 0.3845 2.6008 CHINESE RENMINBI YUAN CNY 6.4690 0.1546 PAKISTANI RUPEE PKR 158.3558 0.0063 CUBAN PESO CUP 24.0957 0.0415 POLISH ZLOTY PLN 3.8154 0.2621 CYPRIOT POUND EUR 0.8454 1.1829 PORTUGAL EUR 0.8454 1.1829 CZECH KORUNA CZK 21.6920 0.0461 QATARI RIYAL QAR 3.6400 0.2747 DANISH KRONER DKK 6.2866 0.1591 RUSSIAN RUBLE RUB 74.2305 0.0135 EGYPTIAN POUND EGP 15.6900 0.0637 RWANDAN FRANC RWF 1001.5019 0.0010 ETHOPIAN BIRR ETB 43.9164 0.0228 SAUDI ARABIAN RIYAL SAR 3.7500 0.2667 EURO EUR 0.8454 1.1829 SINGAPORE DOLLAR SGD 1.3478 0.7419 FINLAND EUR 0.8454 1.1829 SPAIN EUR 0.8454 1.1829 FRANCE EUR 0.8454 1.1829 SOUTH AFRICAN RAND ZAR 14.3346 0.0698 GERMANY -

The Franc Under Pressure

January 3 . 1959 THE ECONOMIC WEEKLY The Franc under Pressure (From Our London Correspondent) "MARKET pressures against the ports fell off in 1958 to about the been expected from such a devalua French frane and rumours level of the import programme laid tion operation about Impending devaluation are down for that period. However, Large Scale Borrowing not unusual Ever .so often some French exports suffered sharply The continued weakness in the event triggers off feverish activity due to the recession in world trade. French balance of trade is made on the Paris gold market and a In fact, exports fell short of the considerably worse by the trade flight of short-term capital from programme by nearly ten per cent. balance of the overseas French France occurs. Because of the In these conditions, and in spite of franc area. Metropolitan France frequency of these episodes these a favourable movement in the is responsible for settling the deficit rumours and currency movements terms of trade, the French deficit in of her overseas Empire with all seldom constitute news; the weak the balance of trade, running at an countries. In 1957 the deficit of ness of the French franc is chronic annual rate of about $1,300 mn in the overseas French franc area and has become a persistent phe the first half of 1958. remains with all non-franc countries, am nomenon in Europe's post-war substantial. ounted to $160 mn, after taking ' currency markets. The present Infructuous Measures into account a $48 mn foreign ca plight of the French franc. -

C381 Official Journal

Official Journal C 381 of the European Union Volume 63 English edition Information and Notices 12 November 2020 Contents II Information INFORMATION FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES European Commission 2020/C 381/01 Non-opposition to a notified concentration (Case M.9954 — Sumitomo/AAR/JV) (1) . 1 IV Notices NOTICES FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES European Commission 2020/C 381/02 Euro exchange rates — 11 November 2020 . 2 2020/C 381/03 New national side of euro coins intended for circulation . 3 Court of Auditors 2020/C 381/04 Report on the performance of the EU budget – Status at the end of 2019 . 4 NOTICES FROM MEMBER STATES 2020/C 381/05 Value added tax (VAT) Exempt investment gold List of gold coins meeting the criteria established in Article 344(1), point (2) of Council Directive 2006/112/EC (special scheme for investment gold) Valid for the year 2021 . 5 EN (1) Text with EEA relevance. NOTICES CONCERNING THE EUROPEAN ECONOMIC AREA EFTA Surveillance Authority 2020/C 381/06 State aid – Decision to raise no objections . 24 2020/C 381/07 State aid – Decision to raise no objections . 25 2020/C 381/08 State aid – Decision to raise no objections . 26 2020/C 381/09 State aid – Decision to raise no objections . 27 2020/C 381/10 State aid – Decision to raise no objections . 28 2020/C 381/11 State aid – Decision to raise no objections . 29 2020/C 381/12 State aid – Decision to raise no objections . 30 V Announcements PROCEDURES RELATING TO THE IMPLEMENTATION OF COMPETITION POLICY European Commission 2020/C 381/13 Prior notification of a concentration (Case M.9907 – Exclusive Networks/Veracomp Business) Candidate case for simplified procedure (1) . -

London, Washington, and the Management of the Franc, 1936-39

PRINCETON STUDIES IN INTERNATIONAL FINANCE, NO. 45 London, Washington, and the Management of the Franc, 1936-39 Ian M. Drummond INTERNATIONAL FINANCE SECTION DEPARTMENT OF ECONOMICS PRINCETON UNIVERSITY • 1979 - PRINCETON STUDIES , IN INTERNATIONAL. FINANCE This is the forty-fifth nurnber, in the series PRINCETON STUDIES IN IN- TERNATIONAL FINANCE, published from time to time by the .Interna- tional Finance Section of the Department of, Economics at Princeton University. The author, Ian M. Drummond, is a professor in the Department of Political Economy at the University of Toronto. He has also taught at Yale University and, as a visitor, at Princeton University and the Uni- versity of Edinburgh. Among his recent publications are British 'Eco- nomic Policy and the Empire, 1919.-1939, Imperial Economic Policy, 1917=1939, and Economics: Principles and Policies in an Open Econ- omy. / This series is intended to be restricted to meritorious research stud- ies in the general field of international financial problems that are too technical, too specialized, or too long to qualify as ESSAYS. The Section welcomes the submission of manuscripts for the series. While the 'Sec- tion ,sponsors the studies, the writers are free to develop their topics as they will. • PETER B. BENEN Director, International Finance Section PRINCETON STUDIES IN INTERNATIONAL FINANCE NO. 45 London, Washington, and the Management of the Franc, 1936-39 Ian M. Drummond INTERNATIONAL FINANCE SECTION DEPARTMENT OF ECONOMICS PRINCETON UNIVERSITY PRINCETON, NEW JERSEY NOVEMBER 1979 CONTENTS CAST OF CHARACTERS V 1 INTRODUCTION 1 The Tripartite Declarations 1 Historical Backdrop 3 Attitudes toward Cooperation and Mutual Support 4 2 BLUM AND AURIOL 9 3 CHAUTEMPS AND BONNET 16 4 CHAUTEMPS AND MARCHANDEAU 26 5 BLUM ONCE MORE 30 6 DALADIER AND MARCHANDEAU 32 7 TRANQUILLITY WITH DALADIER AND REYNAUD 39 8 MORGENTHAU AND THE FRENCH: CREDIT AND EXCHANGE CONTROL 42 9 SOME CONCLUSIONS 53 REFERENCES 57 INTERNATIONAL FINANCE SECTION EDITORIAL STAFF Peter B. -

Countries Codes and Currencies 2020.Xlsx

World Bank Country Code Country Name WHO Region Currency Name Currency Code Income Group (2018) AFG Afghanistan EMR Low Afghanistan Afghani AFN ALB Albania EUR Upper‐middle Albanian Lek ALL DZA Algeria AFR Upper‐middle Algerian Dinar DZD AND Andorra EUR High Euro EUR AGO Angola AFR Lower‐middle Angolan Kwanza AON ATG Antigua and Barbuda AMR High Eastern Caribbean Dollar XCD ARG Argentina AMR Upper‐middle Argentine Peso ARS ARM Armenia EUR Upper‐middle Dram AMD AUS Australia WPR High Australian Dollar AUD AUT Austria EUR High Euro EUR AZE Azerbaijan EUR Upper‐middle Manat AZN BHS Bahamas AMR High Bahamian Dollar BSD BHR Bahrain EMR High Baharaini Dinar BHD BGD Bangladesh SEAR Lower‐middle Taka BDT BRB Barbados AMR High Barbados Dollar BBD BLR Belarus EUR Upper‐middle Belarusian Ruble BYN BEL Belgium EUR High Euro EUR BLZ Belize AMR Upper‐middle Belize Dollar BZD BEN Benin AFR Low CFA Franc XOF BTN Bhutan SEAR Lower‐middle Ngultrum BTN BOL Bolivia Plurinational States of AMR Lower‐middle Boliviano BOB BIH Bosnia and Herzegovina EUR Upper‐middle Convertible Mark BAM BWA Botswana AFR Upper‐middle Botswana Pula BWP BRA Brazil AMR Upper‐middle Brazilian Real BRL BRN Brunei Darussalam WPR High Brunei Dollar BND BGR Bulgaria EUR Upper‐middle Bulgarian Lev BGL BFA Burkina Faso AFR Low CFA Franc XOF BDI Burundi AFR Low Burundi Franc BIF CPV Cabo Verde Republic of AFR Lower‐middle Cape Verde Escudo CVE KHM Cambodia WPR Lower‐middle Riel KHR CMR Cameroon AFR Lower‐middle CFA Franc XAF CAN Canada AMR High Canadian Dollar CAD CAF Central African Republic -

Prospects for a Monetary Union in the East Africa Community: Some Empirical Evidence

Department of Economics and Finance Working Paper No. 18-04 , Guglielmo Maria Caporale, Hector Carcel Luis Gil-Alana Prospects for A Monetary Union in the East Africa Community: Some Empirical Evidence May 2018 Economics and Finance Working Paper Series Paper Working Finance and Economics http://www.brunel.ac.uk/economics PROSPECTS FOR A MONETARY UNION IN THE EAST AFRICA COMMUNITY: SOME EMPIRICAL EVIDENCE Guglielmo Maria Caporale Brunel University London Hector Carcel Bank of Lithuania Luis Gil-Alana University of Navarra May 2018 Abstract This paper examines G-PPP and business cycle synchronization in the East Africa Community with the aim of assessing the prospects for a monetary union. The univariate fractional integration analysis shows that the individual series exhibit unit roots and are highly persistent. The fractional bivariate cointegration tests (see Marinucci and Robinson, 2001) suggest that there exist bivariate fractional cointegrating relationships between the exchange rate of the Tanzanian shilling and those of the other EAC countries, and also between the exchange rates of the Rwandan franc, the Burundian franc and the Ugandan shilling. The FCVAR results (see Johansen and Nielsen, 2012) imply the existence of a single cointegrating relationship between the exchange rates of the EAC countries. On the whole, there is evidence in favour of G-PPP. In addition, there appears to be a high degree of business cycle synchronization between these economies. On both grounds, one can argue that a monetary union should be feasible. JEL Classification: C22, C32, F33 Keywords: East Africa Community, monetary union, optimal currency areas, fractional integration and cointegration, business cycle synchronization, Hodrick-Prescott filter Corresponding author: Professor Guglielmo Maria Caporale, Department of Economics and Finance, Brunel University London, Uxbridge, Middlesex UB8 3PH, UK. -

1 from the Franc to the 'Europe': Great Britain, Germany and the Attempted Transformation of the Latin Monetary Union Into A

From the Franc to the ‘Europe’: Great Britain, Germany and the attempted transformation of the Latin Monetary Union into a European Monetary Union (1865-73)* Luca Einaudi I In 1865 France, Italy, Belgium and Switzerland formed a monetary union based on the franc and motivated by geographic proximity and intense commercial relations.1 The union was called a Latin Monetary Union (LMU) by the British press to stress the impossibility of its extension to northern Europe.2 But according to the French government and many economists of the time, it had a vocation to develop into a European or Universal union. This article discusses the relations between France, which proposed to extend the LMU into a European monetary union in the 1860’s, and the main recipients of the proposal; Great Britain and the German States. It has usually been assumed that the British and the Germans did not show any interest in participating in such a monetary union discussed at an international monetary Conference in Paris in 1867 and that any attempt was doomed from the beginning. For Vanthoor ‘France had failed in its attempt to use the LMU as a lever towards a global monetary system during the international monetary conference... in 1867,’ while for Kindleberger ‘the recommendations of the conference of 1867 were almost universally pigeonholed.’3 With the support of new diplomatic and banking archives, together with a large body of scientific and journalistic literature of the time, I will argue that in fact the French proposals progressed much further and were close to success by the end of 1869, but failed before and independently from the Franco-Prussian war of 1870. -

The Euro and the CFA Franc: Evidence of Sectoral Trade Effects

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Martínez-Zarzoso, Inmaculada Working Paper The Euro and the CFA Franc: Evidence of sectoral trade effects cege Discussion Papers, No. 311 Provided in Cooperation with: Georg August University of Göttingen, cege - Center for European, Governance and Economic Development Research Suggested Citation: Martínez-Zarzoso, Inmaculada (2017) : The Euro and the CFA Franc: Evidence of sectoral trade effects, cege Discussion Papers, No. 311, University of Göttingen, Center for European, Governance and Economic Development Research (cege), Göttingen This Version is available at: http://hdl.handle.net/10419/157628 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available