Order Execution Policy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TEACHERS' RETIREMENT SYSTEM of the STATE of ILLINOIS 2815 West Washington Street I P.O

Teachers’ Retirement System of the State of Illinois Compliance Examination For the Year Ended June 30, 2020 Performed as Special Assistant Auditors for the Auditor General, State of Illinois Teachers’ Retirement System of the State of Illinois Compliance Examination For the Year Ended June 30, 2020 Table of Contents Schedule Page(s) System Officials 1 Management Assertion Letter 2 Compliance Report Summary 3 Independent Accountant’s Report on State Compliance, on Internal Control over Compliance, and on Supplementary Information for State Compliance Purposes 4 Independent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards 8 Schedule of Findings Current Findings – State Compliance 10 Supplementary Information for State Compliance Purposes Fiscal Schedules and Analysis Schedule of Appropriations, Expenditures and Lapsed Balances 1 13 Comparative Schedules of Net Appropriations, Expenditures and Lapsed Balances 2 15 Comparative Schedule of Revenues and Expenses 3 17 Schedule of Administrative Expenses 4 18 Schedule of Changes in Property and Equipment 5 19 Schedule of Investment Portfolio 6 20 Schedule of Investment Manager and Custodian Fees 7 21 Analysis of Operations (Unaudited) Analysis of Operations (Functions and Planning) 30 Progress in Funding the System 34 Analysis of Significant Variations in Revenues and Expenses 36 Analysis of Significant Variations in Administrative Expenses 37 Analysis -

18 February 2019 Solvency and Diversification in Insurance Remain Key Strengths Despite Change in Structure

FINANCIAL INSTITUTIONS ISSUER IN-DEPTH Lloyds Banking Group plc 18 February 2019 Solvency and diversification in insurance remain key strengths despite change in structure Summary RATINGS In 2018, Lloyds Banking Group plc (LBG) altered its structure to comply with the UK's ring- Lloyds Banking Group plc Baseline Credit a3 fencing legislation, which requires large banks to separate their retail and SME operations, Assessment (BCA) and deposit taking in the European Economic Area (EEA) from their other activities, including Senior unsecured A3 Stable the riskier capital markets and trading business. As part of the change, LBG designated Lloyds Bank plc as the“ring-fenced” entity housing its retail, SME and corporate banking operations. Lloyds Bank plc It also assumed direct ownership of insurer Scottish Widows Limited, previously a subsidiary Baseline Credit A3 Assessment (BCA) of Lloyds Bank. The changes had little impact on the creditworthiness of LBG and Lloyds Adjusted BCA A3 Bank, leading us to affirm the deposit and senior unsecured ratings of both entities. Scottish Deposits Aa3 Stable/Prime-1 Widows' ratings were unaffected. Senior unsecured Aa3 Stable » LBG's reorganisation was less complex than that of most UK peers. The Lloyds Lloyds Bank Corporate Markets plc Banking Group is predominantly focused on retail and corporate banking, and the Baseline Credit baa3 required structural changes were therefore relatively minor. The group created a small Assessment (BCA) separate legal entity, Lloyds Bank Corporate Markets plc (LBCM), to manage its limited Adjusted BCA baa1 Deposits A1 Stable/Prime-1 capital markets and trading operations, and it transferred its offshore subsidiary, Lloyds Issuer rating A1 Stable Bank International Limited (LBIL), to LBCM from Lloyds Bank. -

Natwest Markets N.V. Annual Report and Accounts 2020 Financial Review

NatWest Markets N.V. Annual Report and Accounts 2020 Financial Review Page Description of business Financial review NWM N.V., a licensed bank, operates as an investment banking firm serving corporates and financial institutions in the European Economic Presentation of information 2 Area (‘EEA’). NWM N.V. offers financing and risk solutions which 2 Description of business includes debt capital markets and risk management, as well as trading 2 Performance overview and flow sales that provides liquidity and risk management in rates, Impact of COVID-19 3 currencies, credit, and securitised products. NWM N.V. is based in Chairman's statement 4 Amsterdam with branches authorised in London, Dublin, Frankfurt, Summary consolidated income statement 5 Madrid, Milan, Paris and Stockholm. Consolidated balance sheet 6 On 1 January 2017, due to the balance sheet reduction, RBSH 7 Top and emerging risks Group’s regulation in the Netherlands, and supervision responsibilities, Climate-related disclosures 8 transferred from the European Central Bank (ECB), under the Single Risk and capital management 11 Supervisory Mechanism. The joint Supervisory Team comprising ECB Corporate governance 43 and De Nederlandsche Bank (DNB) conducted the day-to-day Financial statements prudential supervision oversight, back to DNB. The Netherlands Authority for the Financial Markets, Autoriteit Financiële Markten Consolidated income statement 52 (AFM), is responsible for the conduct supervision. Consolidated statement of comprehensive income 52 Consolidated balance sheet 53 UK ring-fencing legislation Consolidated statement of changes in equity 54 The UK ring-fencing legislation required the separation of essential Consolidated cash flow statement 55 banking services from investment banking services from 1 January Accounting policies 56 2019. -

Fidelity® Emerging Markets Index Fund

Quarterly Holdings Report for Fidelity® Emerging Markets Index Fund January 31, 2021 EMX-QTLY-0321 1.929351.109 Schedule of Investments January 31, 2021 (Unaudited) Showing Percentage of Net Assets Common Stocks – 92.5% Shares Value Shares Value Argentina – 0.0% Lojas Americanas SA rights 2/4/21 (b) 4,427 $ 3,722 Telecom Argentina SA Class B sponsored ADR (a) 48,935 $ 317,099 Lojas Renner SA 444,459 3,368,738 YPF SA Class D sponsored ADR (b) 99,119 361,784 Magazine Luiza SA 1,634,124 7,547,303 Multiplan Empreendimentos Imobiliarios SA 156,958 608,164 TOTAL ARGENTINA 678,883 Natura & Co. Holding SA 499,390 4,477,844 Notre Dame Intermedica Participacoes SA 289,718 5,003,902 Bailiwick of Jersey – 0.1% Petrobras Distribuidora SA 421,700 1,792,730 Polymetal International PLC 131,532 2,850,845 Petroleo Brasileiro SA ‑ Petrobras (ON) 2,103,697 10,508,104 Raia Drogasil SA 602,000 2,741,865 Bermuda – 0.7% Rumo SA (b) 724,700 2,688,783 Alibaba Health Information Technology Ltd. (b) 2,256,000 7,070,686 Sul America SA unit 165,877 1,209,956 Alibaba Pictures Group Ltd. (b) 6,760,000 854,455 Suzano Papel e Celulose SA (b) 418,317 4,744,045 Beijing Enterprises Water Group Ltd. 2,816,000 1,147,720 Telefonica Brasil SA 250,600 2,070,242 Brilliance China Automotive Holdings Ltd. 1,692,000 1,331,209 TIM SA 475,200 1,155,127 China Gas Holdings Ltd. 1,461,000 5,163,177 Totvs SA 274,600 1,425,346 China Resource Gas Group Ltd. -

LATAM and Emerging Markets Conference Calendar 2021 Confirmed Date and Format to Be Confirmed

LATAM and Emerging Markets Conference Calendar 2021 Confirmed Date and format to be confirmed 2021 June From To Location Conference Institution Latin America EMEA Global ESG 3 4 Virtual BofA Securities 2021 Emerging Markets Debt & Equity Conference BofA X X 6 6 Virtual BofA Securities Virtual Energy Credit Conference BofA X 7 11 Virtual 15th Annual Transport and Logistics Conference HSBC X 8 10 Virtual 2021 Global Energy Conference Credit Suisse X 8 9 Virtual 12th BBI London Virtual Conference Bradesco X 8 9 Virtual Global Industrials and Transportation Virtual Conference UBS X 9 9 Virtual Morgan Stanley Sustainable Futures Conferece Morgan Stanley X X 15 15 Virtual Scotiabank Latam Financials Forum Scotiabank X 23 23 Virtual UBS Virtual Latam Conference UBS X 23 23 Virtual 2021 Energy, Power and Renewables Conference JP Morgan X 30 30 Virtual BTG LatAm Opportunities Conference BTG Pactual X 29 1-Aug Virtual HSBC Financials Conference - a path to sustainability HSBC X X 30 1-Aug Virtual 2021 Brazil Transportation & Infrastructure Conference Credit Suisse X July From To Location Conference Institution Latin America EMEA Global ESG 8 8 Virtual 1st Credit Suisse ESG Forum Switzerland Credit Suisse X August From To Location Conference Institution Latin America EMEA Global ESG 11 13 Virtual 4th Annual FinTech Conference Credit Suisse X 25 26 Virtual CITI-SGX-REITAS REITS / SPONSORS FORUM Citi X September From To Location Conference Institution Latin America EMEA Global ESG 9 9 London Sustainability, ESG and Alpha Summit Citi X X 8 10 NYC 15th -

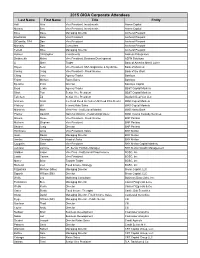

2015 GIOA Corporate Attendees

2015 GIOA Corporate Attendees Last Name First Name Title Entity Hall Wes Vice President, Investments Alamo Capital Mullally Ben Vice President, Investments Alamo Capital Bove Dave Managing Director Amherst Pierpont Brudzinski Beau Vice President Amherst Pierpont DiCamillo, CFA Dan Vice President Amherst Pierpont Markaity Dan Consultant Amherst Pierpont Teifeld Mike Managing Director Amherst Pierpont Holmen Christopher Investments Andress Enterprises Deshmukh Nisha Vice President, Business Development ASPN Solutions Li Shen Trader Bank of America Merrill Lynch Hayes Sean Vice President, SSA Origination & Syndicate Bank of Montreal Conley Craig Vice President - Fixed Income Bank of the West Ching Jerry Agency Trader Barclays Fisher Michael Rates Sales Barclays Bjursten Peter Director Barclays Capital Boyd Lewis Agency Trader BB&T Capital Markets Short Tom Senior Vice President BB&T Capital Markets Tollefsen Ed Senior Vice President Blaylock Beal Van LLC Graham Scott Co-Head Fixed Inc Sales US/Head Prim Dealer BMO Capital Markets Pilsbury Bill Interest Rate Sales BMO Capital Markets Mitrovich Mark Vice Pres - Institutional Market BMO Harris Bank Preiner David B. National Director - Relationship Devel BMO Trust & Custody Services Gavula Steve Vice President - Fixed Income BNP Paribas Mulhern Stephen Vice President BNP Paribas Shubert Craig Director BNP Paribas Hennessy Anna Vice President, Sales BNY Mellon Isaac David Managing Director BNY Mellon Jacobs Christopher Head of Sales BNY Mellon Coughlin Sean Vice President BNY Mellon Capital Markets Jemison Johnnie VP, Senior Portfolio Manager BNY Mellon Wealth Management Glidden Jason Vice Pres - Institutional Fixed Income BOSC, Inc Lewis Camee Vice President BOSC, Inc Maher Brian Taxable Trader BOSC, Inc Rietveld Joel Fixed Income Strategy BOSC, Inc Fitzpatrick Michael (Mike) Managing Director Brean Capital, LLC Sapoch William (Bill) Director Brean Capital, LLC Wells Les Marketing Consultant Business Data Links, Inc. -

Market Monitor

MARKET MONITOR M&A and financing update 1st Quarter 2020 “There are decades where nothing happens; and there are weeks where decades happen” said Vladimir Lenin Indeed for many of us, the last few weeks of “interesting times” seemed undoubtedly like decades. We are hearing “unprecedented” as often as “coronavirus”. An increasingly common sentiment is that “this time is different.” Lately, the comparisons to past events such as the Great Recession, September 11th, and Black Monday have been questioned. But, relatively little attention has been given to the oil price shock that may have more significant long-term economic implications than COVID-19. The lack of precedent, or our ability to recognize precedent where it’s relevant, will test leadership at all levels of the U.S. economy as monetary, fiscal, and regulatory policy levers are being pulled to create a baseline and a path forward. From February 11th to March 12th, the Dow Industrial average dropped 28%, sending the U.S. into a bear market. On March 9th the stock market experienced its first trading halt when the S&P 500 declined 7%. The capital markets took notice and continued forward. On March 12th when the second trading halt occurred the gravity of the situation intensified and the capital markets began to pause. By noon, almost every M&A sale process was stopped due to the very real threat of COVID-19 on the U.S. economy as the hospitality industry closed its doors, social gathering was restricted by local governments, and employers quickly shifted to work from home models. -

Fast and Secure Transfers – Fact Sheet

FAST AND SECURE TRANSFERS – FACT SHEET NEW ELECTRONIC FUNDS TRANSFER SERVICE, “FAST” FAST (Fast And Secure Transfers) is an electronic funds transfer service that allows customers to transfer SGD funds almost immediately between accounts of the 24 participating banks and 5 non-financial institutions (NFI) in Singapore. FAST was originally launched on 17 March 2014 and included only bank participants. From 8th February onwards, FAST will also be available to the 5 NFI participants. FAST enables almost immediate receipt of money. You will know the status of the transfer by accessing your bank account via internet banking or via notification service offered by the participating bank or NFI. FAST is available anytime, 24x7, 365 days. Payment Type Receipt of Payments FAST Almost Immediate, 24x7 basis Cheque Up to 2 business days eGIRO Up to 3 business days Types of accounts that you can use to transfer funds via FAST (Updated on 25 Jan 2021) FAST can be used to transfer funds between customer savings accounts, current accounts or e-wallet accounts. For some banks, the service can also be used for other account types (see table below). Other Account types that you can use FAST Participating Bank to transfer funds via FAST Transfer from Transfer to (Receive) (Pay) 1 ANZ Bank MoneyLine MoneyLine 2 Bank of China Credit Card Credit Card MoneyPlus MoneyPlus 3 The Bank of Tokyo-Mitsubishi UFJ - - 4 BNP Paribas - - 5 CIMB Bank - - 6 Citibank NA - - 7 Citibank Singapore Limited - - 8 DBS Bank/POSB Credit Card Credit Card Cashline Cashline 9 Deutsche Bank - - 10 HL Bank - - 11 HSBC - - 12 HSBC Bank (Singapore) Limited - - 13 ICICI Bank Limited Singapore - - 14 Industrial and Commercial Bank of China Limited Debit Card Debit Card Credit Card 15 JPMorgan Chase Bank, N.A. -

17-19 November 2020

17-19 November 2020 https://financeusa.solarenergyevents.com Confirmed Organizations: 38 DEGREES NORTH EC CAPITAL NATURAL POWER CONSULTANTS AB POWER ADVISORS ECOS ENERGY NAUTILUS SOLAR ENERGY, LLC AETHER INVESTMENT PARTNERS EMERGING ENERGY & ENVIRONMENT INVESTMENT GROUP LLC NEW ENERGY EQUITY AGILITAS ENERGY, LLC ENBALANCE STORAGE NJR CLEAN ENERGY VENTURES AMARESCO ENCORE RENEWABLE ENERGY NORD LB AMERICAS ENERGY GROUP ENEL X NUVEEN, A TIAA COMPANY APRICITY RENEWABLES INC. ENERGY STORAGE DEVELOPMENT PARTNERS ONYX RENEWABLE PARTNERS, LP. ASCEND ANALYTICS ENERGY TOOLBASE ORIGIS ENERGY AVANA CAPITAL ENERVEST CAPITAL ORIGIS SERVICES BLACKROCK FTI CONSULTING PEAK POWER BLATTNER ENERGY GINLONG TECHNOLOGIES PIVOT ENERGY BLOOMBURG GLOBUS THENKEN POWER AFRICA-USAID BLUE WAVE SOLAR GRIDSME PV TECH RESEARCH BNRG HECATE ENERGY RABOBANK BORALEX HELIOLYTICS RADIENT REIT BOSTONIA PARTNERS HELIOVAAS RIGUP BRETTS SOLUTIONS HODGSON RUSS ROTH CAPITAL PARTNERS BRIGHTNIGHT INVESTEC HOLDINGS SEMINOLE FINANCIAL SERVICES BVT ITRI SILICON RANCH C2 ENERGY CAPITAL JAVELIN CAPITAL SOLAMERICA ENERGY CALVERT IMPACT CAPITAL JINKO SOLAR SOLAR RANCH DEVELOPMENT CENTROPLAN USA LLC KAISERWETTER ENERGY ASSET MANAGEMEMT SOLAR RANCH DEVELOPMENT COMPANY CIT BANK KEYBANC CAPITAL MARKETS SOLARIS GLOBAL LLC CITADEL LECLANCHE SOLAS ENERGY CONSULTING CLEAN HORIZON LIBERTY RENEWABLES SOLIS INVERTERS CLEANCAPITAL LIGHTSOURCE BP STANDARD SOLAR INC. CLIFFVIEW PARTNERS LIVE OAK BANK STARKPOINT CAPITAL ADVISORS, LLC CNB LONGI SOLAR STEM COMMONWEALTH BANK OF AUSTRALIA LS POWER SUNLIGHT GENERAL CAPITAL COMMUNITY ENERGY M&T BANK SUNTECH CONEDISON MAP ENERGY SUSGEN CPS ENERGY MARATHON CAPITAL SUSTAINABLE WESTCHESTER CUBICO MITSUBISHI HEAVY INDUSTRIES AMERICA, INC. TMEIC CUSTOMIZED ENERGY SOLUTIONS MOMENTUM ENERGY STORAGE PARTNERS TORTOISE ADVISORS DAYMARK ENERGY ADVISORS MONARCH PRIVATE CAPITAL U.S. DEPARTMENT OF ENERGY DLA PIPER MOTT MACDONALD UL DNV-GL MUNICHRE USAID/ POWER AFRICA. -

Download IPO Report

Donnelley Financial Solutions US IPO Report - December 2020 Edition Congratulations to the 74 December issuers and their advisors on the ~$159 Billion "2020 - an unforgettable year for IPOs! successful completion of their IPO. As I look back on all the successes we Total Raised in 2020 DFIN was proud to have serviced shared with our clients - perseverance, AbCellera Biologics, Altitude hard work, compassion, and great Acquisition, BioAtla, CBRE partnerships led us to successfully Acquisition, 17 Education & 2020 Priced (count) complete 197 IPOs during a year with Technology Group, 4D Molecular 100 so many challenges. An incredibly Therapeutics, Wish, DoorDash, active pipeline, robust valuations, Far Peak Acquisition, Golden vaccine deployment and newfound Falcon Acquisition, Gores hope brings much optimism for 2021." Holding VI, Marquee Raine CRAIG CLAY, PRESIDENT, DONNELLEY FINANCIAL SOLUTIONS 0 Acquisition, Periphas Capital JAN FEB MAR APR MAY JUNE JULY AUG SEP OCT NOV DE… Partnering, Pharming Group NV, Silverback Therapeutics, Thayer 91 League Table *Top 25 Ventures Acquisition, Upstart Issuer's Counsel Count Holdings, and the largest offering IPOs publicly filed in December Ellenoff Grossman 48 this year Airbnb! bringing total count for 2020 to 621. In Kirkland & Ellis 41 2019, there were 293 total filings and Skadden Arps 38 Latham & Watkins LLP 33 296 in 2018. 156 of 2020 filings are Cooley LLP 30 December Priced (count) pending pricing. Goodwin Procter 27 2017 (15) White & Case 23 Davis Polk 19 Sector Breakdown (non-SPACs) 2018 (17) Loeb & Loeb 16 Wilson Sonsini 16 49.8% Healthcare 2019 (13) Winston & Strawn 15 24.08% Technology Ropes & Gray 14 2020 (74) Weil Gotshal 14 11.42% Consumer 2020 Priced Simpson Thacher 11 7.35% Industrial Graubard Miller 9 Greenberg Traurig 9 7.35% Financial 50% of the priced IPOs in 2020 were Paul Weiss 7 SPACs with a total count for the year Sheppard Mullin 7 WilmerHale 7 248 with a total valuation of ~$76 Healthcare Fenwick & West 6 billion. -

In a Year of Contraction, Asia Feels the Ripple Effect of Mifid II 2016 Greenwich Leaders: Asian Equities

In a Year of Contraction, Asia Feels the Ripple Effect of MiFID II 2016 Greenwich Leaders: Asian Equities Q1 2017 Three global brokers are pulling away from the pack in the Asian equity research/advisory business—a break from historical patterns characterized by a more gradual slope among major competitors. Credit Suisse, Bank of America Merrill Lynch and Morgan Stanley are statistically deadlocked atop the list of 2016 Greenwich Leaders in Asian Equity Research/Advisory Vote Share. These three firms have opened a significant lead over UBS, CLSA Asia-Pacific Markets and J.P. Morgan, which are also virtually tied in terms of vote share and round out the list of this year’s winners. In Asian Equity Trading, the same three firms are statistically tied for the top spot in overall share, but in this business, their lead over fellow Greenwich Share Leaders CLSA, UBS and Citi is much narrower. In the growing algorithmic trading business, Bank of America Merrill Lynch widened its lead over the competition. Credit Suisse and Morgan Stanley claim the title of 2016 Greenwich Quality Leaders in Asian Equity Research Product & Analyst Service, and Greenwich Share Leaders — 2016 GREENWICH ASSOCIATES Greenwich Share20 1Leade6r Asian Equity Research/Advisory Vote Share Asian Equity Algorithmic Trading Share Broker Statistical Rank Broker Statistical Rank Credit Suisse 1T Bank of America Merrill Lynch 1 Bank of America Merrill Lynch 1T UBS 2T Morgan Stanley 1T Morgan Stanley 2T UBS 4T Credit Suisse 2T CLSA Asia-Pacific Markets 4T Goldman Sachs 5T J.P. Morgan 4T Citi 5T ITG 5T Asian Equity Trading Share, Options & Volatility Product Important Relationships—Asia Broker Statistical Rank* Broker Statistical Rank Morgan Stanley 1T Morgan Stanley 1T Bank of America Merrill Lynch 1T Goldman Sachs 1T Credit Suisse 1T Bank of America Merrill Lynch 3T CLSA Asia-Pacific Markets 4T Deutsche Bank 3T UBS 4T J.P. -

Td Bank Group Q 2 202 1 Earnings Conference Call May 2 7 , 202 1 Disclaimer

TD BANK GROUP Q 2 202 1 EARNINGS CONFERENCE CALL MAY 2 7 , 202 1 DISCLAIMER THE INFORMATION CONTAINED IN THIS TRANSCRIPT IS A TEXTUAL REPRESENTATION OF THE TORONTO-DOMINION BANK’S (“TD”) Q2 2021 EARNINGS CONFERENCE CALL AND WHILE EFFORTS ARE MADE TO PROVIDE AN ACCURATE TRANSCRIPTION, THERE MAY BE MATERIAL ERRORS, OMISSIONS, OR INACCURACIES IN THE REPORTING OF THE SUBSTANCE OF THE CONFERENCE CALL. IN NO WAY DOES TD ASSUME ANY RESPONSIBILITY FOR ANY INVESTMENT OR OTHER DECISIONS MADE BASED UPON THE INFORMATION PROVIDED ON TD’S WEB SITE OR IN THIS TRANSCRIPT. USERS ARE ADVISED TO REVIEW THE WEBCAST (AVAILABLE AT TD.COM/INVESTOR) ITSELF AND TD’S REGULATORY FILINGS BEFORE MAKING ANY INVESTMENT OR OTHER DECISIONS. FORWARD - LOOKING INFORMATION From time to time, the Bank (as defined in this document) makes written and/or oral forward-looking statements, including in this document, in other filings with Canadian regulators or the United States (U.S.) Securities and Exchange Commission (SEC), and in other communications. In addition, representatives of the Bank may make forward-looking statements orally to analysts, investors, the media and others. All such statements are made pursuant to the “safe harbour” provisions of, and are intended to be forward-looking statements under, applicable Canadian and U.S. securities legislation, including the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements include, but are not limited to, statements made in this document, in the Quarterly Report to Shareholders for the quarter ended April 30, 2021 under the heading “How We Performed”, including under the sub-headings “Economic Summary and Outlook” and “The Bank's Response to COVID-19”, and under the heading “Managing Risk”, and statements made in the Management’s Discussion and Analysis (“2020 MD&A”) in the Bank’s 2020 Annual Report under the headings “Economic Summary and Outlook” and “The Bank’s Response to COVID-19”, for the Canadian Retail, U.S.