Mergers & Acquisitions

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Integration of International Financial Regulatory Standards for the Chinese Economic Area: the Challenge for China, Hong Kong, and Taiwan Lawrence L.C

Northwestern Journal of International Law & Business Volume 20 Issue 1 Fall Fall 1999 Integration of International Financial Regulatory Standards for the Chinese Economic Area: The Challenge for China, Hong Kong, and Taiwan Lawrence L.C. Lee Follow this and additional works at: http://scholarlycommons.law.northwestern.edu/njilb Part of the International Law Commons, International Trade Commons, Law and Economics Commons, and the Securities Law Commons Recommended Citation Lawrence L.C. Lee, Integration of International Financial Regulatory Standards for the Chinese Economic Area: The hC allenge for China, Hong Kong, and Taiwan, 20 Nw. J. Int'l L. & Bus. 1 (1999-2000) This Article is brought to you for free and open access by Northwestern University School of Law Scholarly Commons. It has been accepted for inclusion in Northwestern Journal of International Law & Business by an authorized administrator of Northwestern University School of Law Scholarly Commons. ARTICLES Integration of International Financial Regulatory Standards for the Chinese Economic Area: The Challenge for China, Hong Kong, and Taiwan Lawrence L. C. Lee* I. INTRODUCTION ................................................................................... 2 II. ORIGINS OF THE CURRENT FINANCIAL AND BANKING SYSTEMS IN THE CHINESE ECONOMIC AREA ............................................................ 11 * Lawrence L. C. Lee is Assistant Professor at Ming Chung University School of Law (Taiwan) and Research Fellow at Columbia University School of Law. S.J.D. 1998, Univer- sity of Wisconsin-Madison Law School; LL.M. 1996, American University Washington College of Law; LL.M. 1993, Boston University School of Law; and LL.B. 1991, Soochow University School of Law (Taiwan). Portions of this article were presented at the 1999 Con- ference of American Association of Chinese Studies and the 1997 University of Wisconsin Law School Symposium in Legal Regulation of Cross-Straits Commercial Activities among Taiwan, Hong Kong, and China. -

REAL ESTATE TEAM of the YEAR Sponsored by Edwards Gibson CLIFFORD CHANCE/EVERSHEDS SUTHERLAND/NETWORK RAIL NICHOLAS BARTLETT, CATHY CRICK, ANGELA KEARNS

The Project Condor legal team with Jon Vivian of Edwards Gibson REAL ESTATE TEAM OF THE YEAR Sponsored by Edwards Gibson CLIFFORD CHANCE/EVERSHEDS SUTHERLAND/NETWORK RAIL NICHOLAS BARTLETT, CATHY CRICK, ANGELA KEARNS SEAMLESS COLLABORATION ON A GAME-CHANGING TRANSACTION Described by the FT as ‘one of the largest ever UK real estate deals’, lease seen in the real estate market’. Clifford Chance joined in March this trio of legal teams combined seamlessly on Project Condor – 2018 ‘given the complexity of the transaction and the number Network Rail’s sale of its commercial real estate, comprising 5,200 and calibre of bidders interested in the portfolio’ – and led on properties, for £1.45bn to Blackstone and Telereal Trillium. negotiations with bidders, financing and regulatory issues. Cathy Eversheds advised Network Rail, working on Condor for three Crick, general counsel (property) for Network Rail said: ‘Eversheds years designing the structure and template: managing the bidding Sutherland and Clifford Chance proved to be the perfect combination process from 130 interested parties down to one; using AI for of advisers to deliver the most complex real estate transaction in the exchange and completion; and ‘drafting possibly the most complex history of the railway.’ HIGHLY COMMENDED issues surrounding privacy and security TAYLOR WESSING BURGES SALMON/ specific to the PRC. MARK RAJBENBACH TRANSPORT FOR LONDON Advising InTown Group on the acquisition PHILIP BEER, KATIE SULLIVAN FLADGATE of 20 UK hotels and the associated Law firm and in-house team collaborated NICK MUMBY management platform from Apollo fully on the Albert Island regeneration in Advising Hodson Developments on the Global Management for more than The Royal Docks, one of the last big GLA acquisition, financing and development £700m – InTown’s first venture into sites awaiting transformative regeneration. -

Hang Seng Mainland China Companies High Dividend Yield Index

Hang Seng Mainland China Companies High Dividend Yield Index August 2021 The Hang Seng Mainland China Companies High Dividend Yield Index ("HSMCHYI") reflects the overall performance of Hong Kong listed Mainland companies with high dividend yield. FEATURES ■ The index comprises the 50 highest dividend yielding stocks among sizable Mainland companies that have demonstrated relatively lower price volatility and a persistent dividend payment record for the latest three fiscal years. ■ The index is net dividend yield- weighted with 10% cap on individual constituents. Data has been rebased at 100.00. All information for an index prior to its launch date is back-tested, back-tested performance INFORMATION reflects hypothetical historical performance. Launch Date 9 Sep 2019 INDEX PERFORMANCE Backdated To 31 Dec 2014 % Change Index Index Level Base Date 31 Dec 2014 1 - Mth 3 - Mth 6 - Mth 1 - Yr 3 - Yr 5 - Yr YTD Base Index 3,000 HSMCHYI 3,191.64 +7.42 -11.33 -7.46 +5.16 -7.37 +21.68 +2.40 Review Half-yearly HSMCHYI TRI 4,541.18 +7.76 -7.28 -2.51 +12.13 +10.20 +57.98 +7.87 Dissemination Every 2 sec INDEX FUNDAMENTALS Currency HKD Index Dividend Yield (%) PE Ratio (Times) Annual Volatility*(%) Total Return Index Available HSMCHYI 7.01 5.91 17.47 No. of Constituents 49 *Annual Volatility was calculated based on daily return for the past 12-month period. HSIDVP 602.10 VENDOR CODES All data as at 31 Aug 2021 Bloomberg HSMCHYI Refinitiv .HSMCHYI CONTACT US Email [email protected] Disclaimer All information contained herein is provided for reference only. -

The Charter – a Short History

The Charter – a short history The Mindful Business Charter was born out of discussions between the in house legal team at Barclays and two of their panel law firms, Pinsent Masons and Addleshaw Goddard, along the following lines: The people working in their businesses are highly driven professionals; We do pressured, often complex, work which requires high levels of cognitive functioning; We thrive on that hard work and pressure; In amongst that pressure and hard work there is stress, some of which is unnecessary; When we are stressed we work less productively, and it is not good for our health; and If we could remove that unnecessary stress, we would enable people to work more effectively and efficiently, as well as be happier and healthier. They also recognised that the pressure and stress come from multiple sources, often because of unspoken expectations of what the other requires or demands. Too often lawyers will respond to requests for work from a client with an assumption that the client requires the work as quickly as possible, whatever the demands that may make on the individuals involved, and whatever the impact upon their wellbeing, their families and much else besides. The bigger and more important the client, the greater the risk of that happening. The development of IT has contributed to this. As our connectivity has increased, there has been an inexorable drift towards an assumption that simply because we can be contactable and on demand and working 24/7, wherever we may be, that we should be. No-one stopped to think about this, to challenge it, to ask if it was what we wanted, or what we should do, or needed to do or if it was a good idea, we just went with the drift, perhaps fearful of speaking out, perhaps fearful that if we took a stand, the client would find another law firm down the road who was prepared to do whatever was required. -

General Counsel Career Track an Eversheds Sutherland Research Report General Counsel Career Track an Eversheds Sutherland Research Report

General Counsel Career Track An Eversheds Sutherland research report General Counsel Career Track An Eversheds Sutherland research report Contents Foreword 3 Introduction 4 Characteristics of existing General Counsel 5 What the GCs said: advice to succeed 8 The views of aspiring General Counsel 14 The way forward: some suggestions 17 In-house legal competencies framework 18 Profiles illustrating different in-house career paths 20 Acknowledgements 28 General Counsel Career Track An Eversheds Sutherland research report Foreword In the last twenty years the role of General Counsel has become more prevalent and at the same time, it has increased in influence and scope. Much has been written about this pivotal role - the independent voice on, or close to, a company’s board and yet very little has been written about how to reach what some may consider their ultimate career goal. As the role has expanded from managing a legal team As a former General Counsel I have long been an to encompassing secretariat, governance, risk, advocate for the position, recognising the great compliance and potentially a range of other central breadth and variety that the role offers and the functions, the experience and skills required to opportunity to become involved in a broad range of succeed have changed. Identifying the attributes of strategic and commercial activity. However, I have also some of the country’s most successful General witnessed highly competent in-house counsel Counsel will be helpful, but as the role expands to become too specialised either by sector or role and meet a changing work and regulatory environment, miss out on management positions by not being skills and attributes that have been valued and effective sufficiently prepared for their next promotion. -

CS Group Buys AIM for £5.3M Earlier This Month the AIM-Listed Computer Software Group Bought Hull-Based Legal Systems Supplier AIM for £5.3 Million in Cash

www.legaltechnology.com CS Group buys AIM for £5.3m Earlier this month the AIM-listed Computer Software Group bought Hull-based legal systems supplier AIM for £5.3 million in cash. AIM’s audited accounts to 30 April 2005 show a pre-tax loss from continuing operations of £107k and gross assets of £7.5 million. Since then AIM has disposed of another division and consequently pre-tax losses for the year to 30 April 2006 are expected to increase. However the CS Group says it is confident that “cost savings and synergies resulting from the acquisition CPL expect £850k IT will result in a significant increase in future profitability”. Currently income from recurring support contracts account payback in year one for approximately 51% of AIM’s annual sales. Europe’s largest conveyancing operation Countrywide Property Lawyers is investing Following the acquisition Jim Chase is to continue as £850,000 in an upgrade of their Visualfiles managing director of AIM’s legal software business unit case management and SOS practice within the CS Group. All other AIM Group directors have management software. CPL, who resigned. Commenting on the deal, CS Group chief originally went with a Visualfiles/SOS executive Vin Murria said she was “confident AIM, with its solution in 1997 but then flirted with and strong and stable client base, will steadily grow in sales subsequently abandoned a bespoke and profits. It will provide a sound base from which CS project called Fusion, say they are Group can develop a significant position in the legal confident the upgrade will pay for itself sector, in which we intend to become a leading supplier.” within the first year of implementation. -

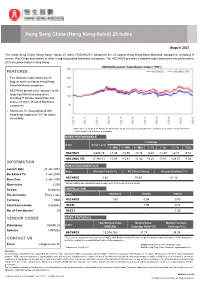

Hang Seng China (Hong Kong-Listed) 25 Index

Hang Seng China (Hong Kong-listed) 25 Index August 2021 The Hang Seng China (Hong Kong- listed) 25 Index ("HSCHK25") comprises the 25 largest Hong Kong-listed Mainland companies, including H shares, Red Chips and shares of other Hong Kong-listed Mainland companies. The HSCHK25 provides a tradable index that tracks the performance of China plays listed in Hong Kong. FEATURES ■ This thematic index tracks the 25 biggest and most liquid Hong Kong- listed Mainland companies ■ HSCHK25 provides an exposure to the large-cap Mainland companies, including H Shares, Red Chips and shares of other HK-listed Mainland companies ■ Stocks are freefloat-adjusted with weightings capped at 10% for higher investibility Data has been rebased at 100.00. All information for an index prior to its launch date is back-tested, back-tested performance reflects hypothetical historical performance. INDEX PERFORMANCE % Change Index Index Level 1 - Mth 3 - Mth 6 - Mth 1 - Yr 3 - Yr 5 - Yr YTD HSCHK25 8,630.19 +1.49 -13.50 -14.18 -0.67 -11.29 +6.71 -9.51 HSCHK25 TRI 17,191.11 +1.80 -11.81 -11.82 +2.47 -0.70 +28.57 -7.02 INFORMATION INDEX FUNDAMENTALS Launch Date 20 Jan 2003 Index Dividend Yield (%) PE Ratio (Times) Annual Volatility*(%) Backdated To 3 Jan 2000 HSCHK25 3.32 10.02 21.12 Base Date 3 Jan 2000 Base Index 2,000 *Annual Volatility was calculated based on daily return for the past 12-month period. Review Quarterly CORRELATION Dissemination Every 2 sec Index HSCHK25 HSCEI HSCCI Currency HKD HSCHK25 1.00 0.98 0.73 Total Return Index Available HSCEI - 1.00 0.73 No. -

FTSE Asia Pacific Ex Japan Australia and NZ Net 20 May 2014

FTSE PUBLICATIONS FTSE Asia Pacific ex Japan Australia 20 May 2014 and NZ Net Indicative Index Weight Data as at Closing on 31 March 2014 Index Index Index Constituent Country Constituent Country Constituent Country weight (%) weight (%) weight (%) AAC Technologies Holdings 0.12 HONG Beijing Capital International Airport (H) 0.03 CHINA China Development Financial Holdings 0.13 TAIWAN KONG Beijing Enterprises Holdings (Red Chip) 0.15 CHINA China Dongxiang Group (P Chip) 0.02 CHINA ABB India 0.02 INDIA Beijing Enterprises Water Group (Red Chip) 0.09 CHINA China Eastern Airlines (H) 0.02 CHINA Aboitiz Equity Ventures 0.09 PHILIPPINES Beijing Jingneng Clean Energy (H) 0.02 CHINA China Everbright (RED CHIP) 0.04 CHINA Aboitiz Power 0.04 PHILIPPINES Beijing North Star (H) 0.01 CHINA China Everbright International (Red Chip) 0.12 CHINA ACC 0.03 INDIA Belle International (P Chip) 0.17 CHINA China Foods (Red Chip) 0.01 CHINA Acer 0.05 TAIWAN Bengang Steel Plates (B) <0.005 CHINA China Galaxy Securities (H) 0.02 CHINA Adani Enterprises 0.05 INDIA Berjaya Sports Toto 0.03 MALAYSIA China Gas Holdings (P Chip) 0.08 CHINA Adani Ports and Special Economic Zone 0.05 INDIA Berli Jucker 0.02 THAILAND China Hongqiao Group (P Chip) 0.02 CHINA Adani Power 0.01 INDIA Bharat Electronics 0.01 INDIA China Huishan Dairy Holdings (P Chip) 0.03 CHINA Adaro Energy PT 0.04 INDONESIA Bharat Forge-A 0.02 INDIA China International Marine Containers (H) 0.04 CHINA Aditya Birla Nuvo 0.02 INDIA Bharat Heavy Elect .LS 0.06 INDIA China Life Insurance (H) 0.67 CHINA Advanced Info Serv 0.27 THAILAND Bharat Petroleum Corp 0.04 INDIA China Longyuan Power Group (H) 0.11 CHINA Advanced Semiconductor Engineering 0.22 TAIWAN Bharti Airtel 0.22 INDIA China Machinery Engineering (H) 0.01 CHINA Advantech 0.06 TAIWAN Bharti Infratel 0.02 INDIA China Mengniu Dairy 0.22 HONG Agile Property Holdings (P Chip) 0.03 CHINA Big C Supercenter 0.04 THAILAND KONG Agricultural Bank of China (H) 0.32 CHINA Biostime International Holdings (P Chip) 0.03 CHINA China Merchant Holdings (Red Chip) 0.13 CHINA AIA Group Ltd. -

Chinese Equities – the Guide March 2021

Chinese equities – the guide March 2021 For professional investors only. In Switzerland for Qualified Investors. In Australia for wholesale clients only. Not for use by retail investors or advisers. Introduction Investors who venture into the Chinese stock universe face an alphabet soup of seemingly random letters. There are A-shares, H-shares and S-chips to name just a few (see Chart 1). These letters represent various attempts to develop the equity market in a country where people traded the first shares as long ago as the 1860s. But something resembling a modern stock market, the Shenzhen Stock Exchange, didn’t start operations until 1 December 1990.1 Shenzhen beat Shanghai as the first exchange of the modern era by some three weeks.2 The Hong Kong Stock Exchange, a forerunner to the city’s current bourse, began operations in 1914 but developed under British colonial rule.3 Investors view Hong Kong as a separate and distinct market. Chart 1: Alphabet soup of Chinese equities Shares Listing Currency Country of Country Examples Index inclusion Comments Can Chinese incorporation where investors buy? company does most business A-share Shanghai + Renminbi China China Shanghai CSI 300 or MSCI Some have dual Y Shenzhen International China A Onshore. listing in H-share Airport Co. MSCI EM since market June 2018 B-share Shanghai + US dollar + China China N/A None Interest has Y Shenzhen Hong Kong collapsed since dollar H-shares H-share Hong Kong Hong Kong China China PetroChina, China MSCI China All Often dual listing Y dollar Construction -

Why Firms Still Need to Be Careful in Good Markets 21St September 2015 Authors: Tony Williams; Steve Cottee

Beware of the upturn – why firms still need to be careful in good markets 21st September 2015 Authors: Tony Williams; Steve Cottee As the results for 2014-15 show a sustained if gradual improvement in law firms financial performance, together with the news of Gateley's successful IPO it is tempting to assume that the worst is now behind law firms after a gruelling period following the financial crisis. However, law firms need to be wary of the upturn and ensure that their firm is well placed to weather the storms that will buffet the legal market for many years to come. In our view there are six factors that law firms need to pay particular attention to if they are going to survive and thrive over the next few years. Cash Firms have increased their long term debt (over one year) from £5.75bn in 2010 to £7.35bn in 2014. Conversely short term debt, mostly overdrafts, has reduced from £2.4bn in 2011 to £1.8bn in 2014. Firms have however received a very significant cash infusion by way of the estimated £1bn of capital injected by fixed share partners to meet the recent requirements of HMRC. Banks still see law firms as a relatively good risk but a few high profile failures may see credit committees becoming far less accommodating and the cost of facilities rise. Crucially the capital injection from fixed share partners many firms benefitted from last year will not be available this year, at a time when arguably there will be an even greater need for cash than before. -

RISK MANAGEMENT and PROFESSIONAL INDEMNITY Legal Business May 2014 November 2010 Legal Business 3 RISK MANAGEMENT and PROFESSIONAL INDEMNITY

RISK MANAGEMENT AND PROFESSIONAL INDEMNITY Legal Business May 2014 November 2010 Legal Business 3 RISK MANAGEMENT AND PROFESSIONAL INDEMNITY 50 Legal Business May 2014 Photographs DANIEL THISTLETHWAITE LEGAL BUSINESS AND MARSH UNINTENDED CONSEQUENCES Our annual Legal Business/Marsh risk round table saw law firm risk specialists share their views on the effect that greater scrutiny on financial stability is having on the market MARK McATEER he ghosts of Halliwells, Dewey & placed on firms by insurers and the SRA thing, while the laws applicable to LLPs LeBoeuf and Cobbetts still loom over financial stability? say quite another. large. Our 2014 risk management Sandra Neilson-Moore, Marsh: All of our report, published in March, showed client firms are being asked questions by Nicole Bigby, Berwin Leighton Paisner: A that a significant number of the UK’s the regulator around financial stability, lot of it is to be seen to be regulating what the Ttop 100 law firms have received more than one borrowings and partner compensation. The SRA feels is a public interest issue. If there visit from the Solicitors Regulation Authority SRA is, of course, trying to accomplish two was another significant collapse, it would (SRA) in the last couple of years and financial key things: one, to preserve the reputation of be criticised for not having asked these stability has rapidly moved to the top of its the profession and two, to secure protection questions, or not, at least, demonstrating agenda. In June 2013, the regulator announced for clients. In my view however, (and that it was taking an active interest, so that 160 firms across England and Wales were notwithstanding its best intentions) the there is a measure of self-interest and self- under intensive supervision due to the state of SRA will probably be no more able to spot a protection about it. -

Michael Harvey QC

Michael Harvey QC T: +44 (0)20 7797 8100 [email protected] www.crownofficechambers.com Contents ADR ............................................................................................................................................................ 1 Selected Cases .................................................................................................................................... 1 Commercial ................................................................................................................................................ 2 Selected Cases .................................................................................................................................... 2 Construction & Engineering ....................................................................................................................... 2 Selected Cases .................................................................................................................................... 2 Insurance & Reinsurance ........................................................................................................................... 3 Selected Cases .................................................................................................................................... 3 Product Liability ......................................................................................................................................... 4 Selected Cases ...................................................................................................................................