Pasco Iii Appraisers Manual

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cebu 1(Mun to City)

TABLE OF CONTENTS Map of Cebu Province i Map of Cebu City ii - iii Map of Mactan Island iv Map of Cebu v A. Overview I. Brief History................................................................... 1 - 2 II. Geography...................................................................... 3 III. Topography..................................................................... 3 IV. Climate........................................................................... 3 V. Population....................................................................... 3 VI. Dialect............................................................................. 4 VII. Political Subdivision: Cebu Province........................................................... 4 - 8 Cebu City ................................................................. 8 - 9 Bogo City.................................................................. 9 - 10 Carcar City............................................................... 10 - 11 Danao City................................................................ 11 - 12 Lapu-lapu City........................................................... 13 - 14 Mandaue City............................................................ 14 - 15 City of Naga............................................................. 15 Talisay City............................................................... 16 Toledo City................................................................. 16 - 17 B. Tourist Attractions I. Historical........................................................................ -

Trailword.Pdf

NPS Form 10-900-b OMB No. 1024-0018 (March 1992) United States Department of the Interior National Park Service National Register of Historic Places Multiple Property Documentation Form This form is used for documenting multiple property groups relating to one or several historic contexts. See instructions in How to Complete the Multiple Property Documentation Form (National Register Bulletin 16B). Complete each item by entering the requested information. For additional space, use continuation sheets (Form 10-900-a). Use a typewriter, word processor, or computer to complete all items. _X___ New Submission ____ Amended Submission ======================================================================================================= A. Name of Multiple Property Listing ======================================================================================================= Historic and Historical Archaeological Resources of the Cherokee Trail of Tears ======================================================================================================= B. Associated Historic Contexts ======================================================================================================= (Name each associated historic context, identifying theme, geographical area, and chronological period for each.) See Continuation Sheet ======================================================================================================= C. Form Prepared by ======================================================================================================= -

Cabinology with Dale Mulfinger Ologies Podcast June 25, 2019

Cabinology with Dale Mulfinger Ologies Podcast June 25, 2019 Oh Hey! It’s that friend who can’t sit at a diner table without making modular sculptures with the half & half creamers, can’t not do it! Alie Ward, back with another episode of Ologies. Great news, kiddos! I got some news for you. You ready? This episode is not about ticks. Yesss! Are you stoked? Now that we have covered some basic health and safety, i.e. me just reminding you, check those crevices, kind of like a flight attendant demonstrating an inflatable vest. But now you know, let’s get this summer show on the road. There are sprinklers to run through, there’s campfire smoke to dodge, some sandal tans to get, barbeques, reunions. Before we hit the road, let’s make a pit stop at ThankYouVille, to say thanks to all the folks supporting this podcast on Patreon. I literally could not make the show without you. Thank you to all the folks wearing Ologies merch on your actual physical bodies and talking up the show to your fam while you make pies. Thank you to everyone who, for zero dollars, rate, and subscribes, and leaves the reviews for me to read, because you know I do, like a lady creep. And then I read you one aloud, such as this fresh one from CrazyDogMom1227 who compared me to a, “gently excited Richard Simmons but for science instead of high kicks.” And said that I’ll, “Teach about all sorts of things, especially things that you didn’t think you’d find interesting. -

Like a Ton of Bricks Here’S a Ton of 7-Letter Bingos About BUILDINGS, STRUCTURES, COMPONENTS Compiled by Jacob Cohen, Asheville Scrabble Club

Like a Ton of Bricks Here’s a ton of 7-letter bingos about BUILDINGS, STRUCTURES, COMPONENTS compiled by Jacob Cohen, Asheville Scrabble Club A 7s ABATTIS AABISTT abatis (barrier made of felled trees) [n -ES] ACADEME AACDEEM place of instruction [n -S] ACADEMY AACDEMY secondary school [n -MIES] AGOROTH AGHOORT AGORA, marketplace in ancient Greece [n] AIRPARK AAIKPRR small airport (tract of land maintained for landing and takeoff of aircraft) [n -S] AIRPORT AIOPRRT tract of land maintained for landing and takeoff of aircraft [n -S] ALAMEDA AAADELM shaded walkway [n -S] ALCAZAR AAACLRZ Spanish fortress or palace [n -S] ALCOVES ACELOSV ALCOVE, recessed section of room [n] ALMEMAR AAELMMR bema (platform in synagogue) [n -S] ALMONRY ALMNORY place where alms are distributed [n -RIES] AMBONES ABEMNOS AMBO, pulpit in early Christian church [n] AMBRIES ABEIMRS AMBRY, recess in church wall for sacred vessels [n] ANDIRON ADINNOR metal support for holding wood in fireplace [n -S] ANNEXED ADEENNX ANNEX, to add or attach [v] ANNEXES AEENNSX ANNEXE, something added or attached [n] ANTEFIX AEFINTX upright ornament at eaves of tiled roof [n -ES, -, -AE] ANTENNA AAENNNT metallic device for sending or receiving radio waves [n -S, -E] ANTHILL AHILLNT mound formed by ants in building their nest [n -S] APSIDAL AADILPS APSE, domed, semicircular projection of building [adj] APSIDES ADEIPSS APSIS, apse (domed, semicircular projection of building) [n] ARBOURS ABORRSU ARBOUR, shady garden shelter [n] ARCADED AACDDER ARCADE, to provide arcade (series of arches) -

2014 Trail News

Trail of Tears National Historic Trail Trail News Downtown Memphis to Host TOTA Conference in October On the afternoon of Tuesday, October 7, 2014, following a wayside unveiling, conference participants will board a Mississippi riverboat for a cruise narrated by celebrated Memphis historian and tour guide Jimmy Ogle. The following afternoon’s activities, sponsored by the Choctaw Nation, include a tour of the museum and grounds of Chucalissa Archaeological site, followed by a traditional Choctaw meal prepared by a team of cooks under the direction of TOTA Vice President Sue Folsom. Storyteller Lori Robins, representing the Chickasaw Nation, will cap off that evenings events. Featured speakers for the conference include Dr. Dan Littlefi eld, University of Arkansas at Little Rock; Kirk Perry, Chickasaw Nation culture and humanities department, who will speak on Chickasaw image courtesy of the NPS History; and Dr. Brett Riggs, who will do The 19th Annual TOTA Conference in Memphis will include a dedication of a new Trail of Tears National presentations on Muscogee Creek history Historic Trail wayside exhibit about early removal and the water route in the Memphis area. The wayside is and the Natchez Tribe. on the waterfront in Tom Lee Park. Missouri City to Receive 7 Wayside Exhibits The City of Waynesville, Missouri, and INSIDE THIS ISSUE NTIR are working with contractors to produce seven wayside exhibits for Laughlin Park. One upright orientation exhibit and • Executive Director Report................. 2 six low-profi le site specifi c exhibits will • Missouri KMZ File Project................. 2 cover many aspects of the Trail of Tears, including the known encampment along • TOTA Chapter News................... -

2013 Trail News

Trail of Tears National Historic Trail Trail News Enthusiastic Groups Attend Preservation Workshops Large groups and enthusiastic properties, to seek help in identifying valuable preservation expertise from participation characterized two recently- previously unknown historic buildings representatives of three State Historic held Trail of Tears National Historic Trail along the trail routes, and to set priorities Preservation Ofces (SHPOs). Mark (NHT) preservation workshops. The among chapter members for actions Christ and Tony Feaster spoke on behalf frst took place in Cleveland, Tennessee, to be taken related toward historic site of the Arkansas Historic Preservation on July 8 and 9, while the second took identifcation and preservation. Program, and Lynda Ozan—who also place on July 12 and 13 in Fayetteville, attended the Fayetteville meeting— Arkansas. More than 80 Trail of Tears To assist association members in represented the Oklahoma SHPO. At Association (TOTA) members and expanding the number of known historic the Cleveland meeting, Peggy Nickell friends attended the workshops, which sites along the trail, the NPS has been represented the Tennessee SHPO. TOTA took place as a result of the combined working for the past year with the Center President Jack Baker, recently elected to eforts of the Trail of Tears Association, for Historic Preservation at Middle the Cherokee Nation’s Tribal Council, the National Park Service (NPS), and Tennessee State University. Two staf played a key leadership role at both Middle Tennessee State University in members from the center, Amy Kostine workshops. Murphreesboro. and Katie Randall, were on hand at both workshops, and each shared information Representatives of both the Choctaw The workshops had several purposes: to on what had been learned about newly- and Chickasaw nations were also in provide information about historic sites discovered trail properties. -

Recreational Buildings and Facilities

Agricultural Research Service • U.S. Department of Agriculture • Agriculture Handbook No.438 RECREATIONAL BUILDINGS AND FACILITIES Agriculture Handbook No. 438 Prepared by Agricultural Research Service United States Department of Agriculture Washington, D.C. ^ issued September 1972 For sale by the Superintendent of Documents, U.S. Government Printing Office Washington, D.C. 20402 - Price 70 cents Stock Number 0100-02663 CONTENTS Plan No. Page Introduction 1 Cabins 2 Vacation cabin for two 5184 2 Three-room cabin 5185 3 Vacation cabin for four 5I86 4 Cabin 5928 5 Cabin, masonry construction 5968 6 Cabin with dormitory loft 6013 9 A-frame cabins 5954 11 5965 11 A-frame cabin 6003 15 Log cabin 55O6 17 Log cabin 5507 I8 Log cabin 7013 18 Pole-frame cabin 6002 20 Pole-frame cabin 6004 22 Vacation house, frame construction 5997 24 Tenant house 7010 27 Farm cottage 7137 28 Adirondack-type shelter 5998 30 Barns and Equipment for Horses 32 Expansible barn for riding horses 5838 32 Two-horse trailer 5943 33 Saddle horse barn 5994 35 Eight-stall horse barn 6010 36 Seventeen-stall horse barn 6011 38 One-and-a-half-story horse barn 6024 40 Portable stable for a horse 6082 42 Horse equipment 6014 44 Horse show rings 6015 46 Greenhouses 48 Plastic-covered greenhouse 594I 48 Plastic-covered greenhouse 5946 50 Greenhouse framing for plastic covering 6029 52 Hotbed and propagating frame 597I 54 Mini-hotbed and propagating frame 6080 57 Recreation Facilities 59 Outdoor fireplace 5188 59 Boat landing 5975 51 Picnic shelter of wood construction 5995 62 Concrete block incinerator 5996 64 Sheltered barbeque pits 6020 66 6022 66 Recreational pavilion with kitchen 6079 68 Comfort station for campgrounds 6083 70 Storage sheds 6086 72 6093 72 Utility sheds 6100 73 RECREATIONAL BUILDINGS AND FACILITIES Agricultural Research Service INTRODUCTION This illustrated list of currently available building Economy of material and labor has been given plans was compiled by the Cooperative Farm Building particular emphasis. -

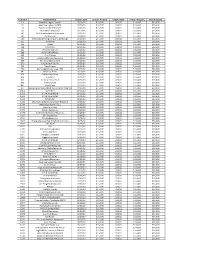

2021-02-09 Final Disbursement Spreadsheet

License # Establishment Check 1 Date Check 1 Amount Check 2 Date Check 2 Amount Total Awarded 51 American Legion Post #1 10/23/20 $15,000 1/20/21 $15,000 $30,000 59 American Legion Post #28 10/23/20 $15,000 1/20/21 $15,000 $30,000 74 Pancho's Villa Restaurant 11/05/20 $15,000 1/20/21 $15,000 $30,000 83 Asia GarDens/BranDy's 11/19/20 $15,000 1/20/21 $15,000 $30,000 107 Bella Vista Pizzaria & Restaurant 10/23/20 $15,000 1/20/21 $15,000 $30,000 140 The Blue Fox 10/29/20 $15,000 1/20/21 $15,000 $30,000 200 Matanuska Brewing ComPany, Anchorage 10/23/20 $15,000 1/20/21 $15,000 $30,000 217 Williwaw 10/23/20 $15,000 1/20/21 $15,000 $30,000 225 Koots 10/23/20 $15,000 1/20/21 $15,000 $30,000 258 Club Paris 10/23/20 $15,000 1/20/21 $15,000 $30,000 321 Chili's Bar anD Grill 10/23/20 $15,000 1/20/21 $15,000 $30,000 398 Buffalo WilD Wings 10/23/20 $15,000 1/20/21 $15,000 $30,000 434 Fiori D'Italia 10/23/20 $15,000 1/20/21 $15,000 $30,000 629 La Cabana Mexican Restaurant 11/05/20 $15,000 1/20/21 $15,000 $30,000 635 Serrano's Mexican Grill 11/12/20 $15,000 1/20/21 $15,000 $30,000 670 Long Branch Saloon 10/23/20 $15,000 1/20/21 $15,000 $30,000 733 Twin Dragon 10/23/20 $15,000 1/20/21 $15,000 $30,000 750 Anchorage Moose LoDge 1534 10/29/20 $15,000 1/20/21 $15,000 $30,000 761 MulDoon Pizza 11/19/20 $15,000 1/20/21 $15,000 $30,000 814 The BraDley House 10/23/20 $15,000 1/20/21 $15,000 $30,000 826 Tequila 61 10/23/20 $15,000 1/20/21 $15,000 $30,000 842 The New Peanut Farm 10/29/20 $15,000 1/20/21 $15,000 $30,000 888 Pizza OlymPia 12/11/20 $15,000 1/20/21 $15,000 $30,000 891 Pizza Plaza 12/11/20 $15,000 1/20/21 $15,000 $30,000 Anchorage977 Brewing ComPany (NeeD sPecial email if aPPlieD for Tier11/05/20 A) $15,000 1/20/21 $15,000 $30,000 1064 Sorrento's 10/23/20 $15,000 1/20/21 $15,000 $30,000 1203 V.F.W. -

Reference # Resource Name Address County City Listed Date Multiple

Reference # Resource Name Address County City Listed Date Multiple Name 76001760 Arnwine Cabin TN 61 Anderson Norris 19760316 92000411 Bear Creek Road Checking Station Jct. of S. Illinois Ave. and Bear Creek Rd. Anderson Oak Ridge 19920506 Oak Ridge MPS 92000410 Bethel Valley Road Checking Station Jct. of Bethel Valley and Scarboro Rds. Anderson Oak Ridge 19920506 Oak Ridge MPS 91001108 Brannon, Luther, House 151 Oak Ridge Tpk. Anderson Oak Ridge 19910905 Oak Ridge MPS 03000697 Briceville Community Church and Cemetery TN 116 Anderson Briceville 20030724 06000134 Cross Mountain Miners' Circle Circle Cemetery Ln. Anderson Briceville 20060315 10000936 Daugherty Furniture Building 307 N Main St Anderson Clinton 20101129 Rocky Top (formerly Lake 75001726 Edwards‐‐Fowler House 3.5 mi. S of Lake City on Dutch Valley Rd. Anderson 19750529 City) Rocky Top (formerly Lake 11000830 Fort Anderson on Militia Hill Vowell Mountain Rd. Anderson 20111121 City) Rocky Top (formerly Lake 04001459 Fraterville Miners' Circle Cemetery Leach Cemetery Ln. Anderson 20050105 City) 92000407 Freels Cabin Freels Bend Rd. Anderson Oak Ridge 19920506 Oak Ridge MPS Old Edgemoor Rd. between Bethel Valley Rd. and Melton Hill 91001107 Jones, J. B., House Anderson Oak Ridge 19910905 Oak Ridge MPS Lake 05001218 McAdoo, Green, School 101 School St. Anderson Clinton 20051108 Rocky Top (formerly Lake 14000446 Norris Dam State Park Rustic Cabins Historic District 125 Village Green Cir. Anderson 20140725 City) 75001727 Norris District Town of Norris on U.S. 441 Anderson Norris 19750710 Tennessee Valley Authority Hydroelectric 16000165 Norris Hydrolectric Project 300 Powerhouse Way Anderson Norris 20160412 System, 1933‐1979 MPS Roughly bounded by East Dr., W. -

Newsletter of the Trail of Tears National Historic Trail Partnership • Spring 2018

Newsletter of the Trail of Tears National Historic Trail Partnership • Spring 2018 – Number 29 Leadership from the Cherokee Nation and the National Trail of Tears Association Sign Memorandum of Understanding Tahlequah, OK Principal Chief Bill John Baker expressed Nation’s Historic Preservation Officer appreciation for the work of the Elizabeth Toombs, whereby the Tribe Association and the dedication of its will be kept apprised of upcoming members who volunteer their time and events and activities happening on talent. or around the routes. The Memo encourages TOTA to engage with The agreement establishes a line for govt. and private entities and routine communications between to be an information source on the Trail of Tears Association and the matters pertaining to Trial resource CHEROKEE NATION PRINCIPAL CHIEF BILL JOHN Cherokee Nation through the Cherokee conservation and protection. BAKER AND THE TRAIL OF TEARS PRESIDENT JACK D. BAKER SIGN A MEMORANDUM OF UNDERSTANDING FORMALIZING THE CONTINUED PARTNERSHIP BETWEEN THE TRAIL OF TEARS ASSOCIATION AND THE CHEROKEE NATION TO PROTECT AND PRESERVE THE ROUTES AS WELL AS EDUCATING THE PUBLIC ABOUT THE HISTORY ASSOCIATED WITH THE TRAIL OF TEARS. Cherokee Nation Principal Chief Bill John Baker and Trail of Tears Association President Jack D. Baker, signed a Memorandum of Understanding on March 1st, continuing a long-time partnership between the association and the tribe. Aaron Mahr, Supt. of the National Trails Intermountain Region, the National Park Service office which oversees the Trail of Tears National Historic Trail said “The Trails Of Tears Association is our primary non-profit volunteer organization on the national historic trail, and the partnership the PICTURED ABOVE: (SEATED FROM L TO R) S. -

Tiny House Directory V3

Tiny House Directory Published by the Tiny House Blog By Kent Griswold TinyHouseBlog.com Container Floating Home Log Prefab Houses Container Homes - CR Athens FloLodge - TX Adirondack Lean-to-Company - NY Bungalow in a Box - ME Ecopods - ON Berkeley Engineering - AZ Conestoga Log Cabins - PA Clayton I-House - US Global Portable Building - CA Floating Pods - WA Forest Classics Log Homes - CO Form & Forest Flat Pack Greenleaf Cabins - CO Cabins - BC Jalopy Cabins - CO Gratitude Millworks - AL Lakefront Log Cabins - CA Green Pod Development - WA Lake Louis Lodge - WY Habitaflex - QC LogRV's - CA ideabox - OR Montana Mobile Cabins - MT Joseph Sandy - CA Dome Gypsy Caravan Pine Hollow Log Homes - UT kitHaus - CA Domespace - FR Daphne’s Caravans - ON Tay Log Cabins - Scotland Metro Shed - UK/PA EcoHab - UK Gypsy Caravan Company - UK m-finity - IL Free Spirit Speheres - BC Gypsy Coach - CO MiniHome - ON Igloo Cabin - AU Gypsy Vans by Roth - OR Modern Cabana - CA Monolithic Cabins - TX Gypsy Wagon Workshop - WA Modern-Shed - WA World Shelters - CA Ihgham & Fallon - UK OfficePod - UK The New Gypsy Caravan - PA Narrow Boats Reclaimed Space - TX Windy Smithy - UK Kathlyn - UK Shawnee Structures - PA MetroFloat - UK Shire Cottage - NZ Homeless Shelter Narrow Craft LTD - UK Teak Houses - CA Everyone Deserves a Roof - CA Timber Design - UK The Mad Housers - GA Twelve3 - BC Earth Shelter 2.0 - VA Yardpods - CA CalEarth Ecodomes - CA weeHouse - MN Cob Cottage Company - OR Park Models Cobworks - BC Athens Park Models - TX Econest - NM Breckenridge - IN -

Cleveland, Tennessee …Your Gateway to the Ocoee Region

OZ-ClevelandCOC-Ad-010811.indd 1 1/31/2011 2:11:30 PM Welcome to Cleveland, Tennessee …your gateway to the Ocoee Region. I’m Melissa and it’s my job to TABLE OF CONTENTS Attractions/Adventure ..........................................................................2 invite you to visit our great Attractions/Cherokee Heritage...................................................................4 community! This is my Attractions/Civil War ............................................................................6 Attractions/Farm Fun ..................................................................................8 hometown and I hope you will Attractions/Religious Heritage..................................................................10 see why I love it. Throughout this Outfitters ............................................................................................12 Recreation .......................................................................................... 14 guide, real hometown folks Area Map ............................................................................................ 16 Lodging ..............................................................................................18 welcome you just like when you Dining .................................................................................................20 are here in person. Enjoy your Shopping ............................................................................................22 Events .................................................................................................24