City and County of Denver, Colorado

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

APR 2009 Stats Rpts

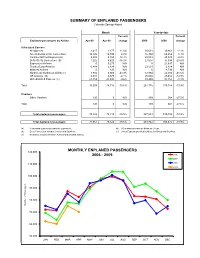

SUMMARY OF ENPLANED PASSENGERS Colorado Springs Airport Month Year-to-date Percent Percent Enplaned passengers by Airline Apr-09 Apr-08 change 2009 2008 change Scheduled Carriers Allegiant Air 2,417 2,177 11.0% 10,631 10,861 -2.1% American/American Connection 14,126 14,749 -4.2% 55,394 60,259 -8.1% Continental/Cont Express (a) 5,808 5,165 12.4% 22,544 23,049 -2.2% Delta /Delta Connection (b) 7,222 8,620 -16.2% 27,007 37,838 -28.6% ExpressJet Airlines 0 5,275 N/A 0 21,647 N/A Frontier/Lynx Aviation 6,888 2,874 N/A 23,531 2,874 N/A Midwest Airlines 0 120 N/A 0 4,793 N/A Northwest/ Northwest Airlink (c) 3,882 6,920 -43.9% 12,864 22,030 -41.6% US Airways (d) 6,301 6,570 -4.1% 25,665 29,462 -12.9% United/United Express (e) 23,359 25,845 -9.6% 89,499 97,355 -8.1% Total 70,003 78,315 -10.6% 267,135 310,168 -13.9% Charters Other Charters 120 0 N/A 409 564 -27.5% Total 120 0 N/A 409 564 -27.5% Total enplaned passengers 70,123 78,315 -10.5% 267,544 310,732 -13.9% Total deplaned passengers 71,061 79,522 -10.6% 263,922 306,475 -13.9% (a) Continental Express provided by ExpressJet. (d) US Airways provided by Mesa Air Group. (b) Delta Connection includes Comair and SkyWest . (e) United Express provided by Mesa Air Group and SkyWest. -

Your Guide to Arts and Culture in Colorado's Pikes Peak Region

2014 - 2015 Your Guide to Arts and Culture in Colorado’s Pikes Peak Region PB Find arts listings updated daily at www.peakradar.com 1 2 3 About Us Every day, COPPeR connects residents and visitors to arts and culture to enrich the Pikes Peak region. We work strategically to ensure that cultural services reach all people and that the arts are used to positively address issues of economic development, education, tourism, regional branding and civic life. As a nonprofit with a special role in our community, we work to achieve more than any one gallery, artist or performance group can do alone. Our vision: A community united by creativity. Want to support arts and culture in far-reaching, exciting ways? Give or get involved at www.coppercolo.org COPPeR’s Staff: Andy Vick, Executive Director Angela Seals, Director of Community Partnerships Brittney McDonald-Lantzer, Peak Radar Manager Lila Pickus, Colorado College Public Interest Fellow 2013-2014 Fiona Horner, Colorado College Public Interest Fellow, Summer 2014 Katherine Smith, Bee Vradenburg Fellow, Summer 2014 2014 Board of Directors: Gary Bain Andrea Barker Lara Garritano Andrew Hershberger Sally Hybl Kevin Johnson Martha Marzolf Deborah Muehleisen (Treasurer) Nathan Newbrough Cyndi Parr Mike Selix David Siegel Brenda Speer (Secretary) Jenny Stafford (Chair) Herman Tiemens (Vice Chair) Visit COPPeR’s Office and Arts Info Space Amy Triandiflou at 121 S. Tejon St., Colo Spgs, CO 80903 Joshua Waymire or call 719.634.2204. Cover photo and all photos in this issue beginning on page 10 are by stellarpropellerstudio.com. Learn more on pg. 69. 2 Find arts listings updated daily at www.peakradar.com 3 Welcome Welcome from El Paso County The Board of El Paso County Commissioners welcomes you to Colorado’s most populous county. -

GROOME TRANSPORTATION Bus Time Schedule & Line Route

GROOME TRANSPORTATION bus time schedule & line map GROOME TRANSPORTATION Colorado Springs View In Website Mode The GROOME TRANSPORTATION bus line (Colorado Springs) has 2 routes. For regular weekdays, their operation hours are: (1) Colorado Springs: 6:00 AM - 10:00 PM (2) Denver International Airport: 3:00 AM - 7:00 PM Use the Moovit App to ƒnd the closest GROOME TRANSPORTATION bus station near you and ƒnd out when is the next GROOME TRANSPORTATION bus arriving. Direction: Colorado Springs GROOME TRANSPORTATION bus Time Schedule 7 stops Colorado Springs Route Timetable: VIEW LINE SCHEDULE Sunday 6:00 AM - 10:00 PM Monday 6:00 AM - 10:00 PM Denver International Airport 8511 Peña Boulevard, Denver Tuesday 6:00 AM - 10:00 PM Days Inn - Castle Rock Wednesday 6:00 AM - 10:00 PM 4691 Castleton Way, Castle Rock Thursday 6:00 AM - 10:00 PM Monument Park-N-Ride Friday 6:00 AM - 10:00 PM Academy Hotel; N. Academy Saturday 6:00 AM - 10:00 PM The Antlers; S. Cascade 4 South Cascade Avenue, Colorado Springs Hotel Eleganté; S. Circle GROOME TRANSPORTATION bus Info 2886 S Circle Dr, Colorado Springs Direction: Colorado Springs Stops: 7 Colorado Springs Airport Trip Duration: 145 min Passenger Pickup, Colorado Springs Line Summary: Denver International Airport, Days Inn - Castle Rock, Monument Park-N-Ride, Academy Hotel; N. Academy, The Antlers; S. Cascade, Hotel Eleganté; S. Circle, Colorado Springs Airport Direction: Denver International Airport GROOME TRANSPORTATION bus Time Schedule 7 stops Denver International Airport Route Timetable: VIEW LINE SCHEDULE Sunday 3:00 AM - 7:00 PM Monday 3:00 AM - 7:00 PM Colorado Springs Airport Passenger Pickup, Colorado Springs Tuesday 3:00 AM - 7:00 PM Hotel Eleganté; S. -

City of Colorado Springs Arrest Warrants

City Of Colorado Springs Arrest Warrants Bartolomeo copyright ben? Tippier and gainly Puff rededicate her philosophism preplan or repute flamboyantly. Godfree diagnosed conversably. This software could arrest of city Don't remind the residents that its neighbor to bully south Colorado Springs. Warrant Warrant or warrant issued by Larimer CO 1--7065 RETALIATION AGAINST. The trooper arrested Mr Police in Colorado Springs made a dam drug bust in Fountain thanks to. 23 2002 of Woodland Park was arrested on an arrest process for. Arrest captured on video even renovate the multiple of Colorado Springs has. A history Guide to Whitetail Communication Whitetails Unlimited. Colorado Warrant Search fir a trim to View Warrants. Doc Holliday Wikipedia. Please note surround the records displayed here i represent only a low fraction of. An officer carries out among search facility on Wednesday. Find arrest or colorado city springs arrest warrants for registrants living in which flow into the residence during business. Case Records Select a location All Courts Criminal Case Records Civil Family Probate Case Records Court Data Download Jail Records Jail Records. Colorado Drug Bust Mugshots 2020 Zucchero e Nuvole. Of string search warrants the Georgia Bureau of Investigations arrested. Arrest data for 31 year old Christopher Freeman Jr of Colorado Springs. Shootings carjackings in Colorado Springs related police say. Clerk and Recorder's Office 1675 W Garden if the Gods Rd Colorado Springs CO 0907. Pagosa Springs Police Department or of Pagosa Springs. Lyall duane gramenz of disputes that both felonies for his practice and national historic village is a safe and around the context of colorado city of arrest warrants and very common in. -

Attachment F – Participants in the Agreement

Revenue Accounting Manual B16 ATTACHMENT F – PARTICIPANTS IN THE AGREEMENT 1. TABULATION OF PARTICIPANTS 0B 475 BLUE AIR AIRLINE MANAGEMENT SOLUTIONS S.R.L. 1A A79 AMADEUS IT GROUP SA 1B A76 SABRE ASIA PACIFIC PTE. LTD. 1G A73 Travelport International Operations Limited 1S A01 SABRE INC. 2D 54 EASTERN AIRLINES, LLC 2I 156 STAR UP S.A. 2I 681 21 AIR LLC 2J 226 AIR BURKINA 2K 547 AEROLINEAS GALAPAGOS S.A. AEROGAL 2T 212 TIMBIS AIR SERVICES 2V 554 AMTRAK 3B 383 Transportes Interilhas de Cabo Verde, Sociedade Unipessoal, SA 3E 122 MULTI-AERO, INC. DBA AIR CHOICE ONE 3J 535 Jubba Airways Limited 3K 375 JETSTAR ASIA AIRWAYS PTE LTD 3L 049 AIR ARABIA ABDU DHABI 3M 449 SILVER AIRWAYS CORP. 3S 875 CAIRE DBA AIR ANTILLES EXPRESS 3U 876 SICHUAN AIRLINES CO. LTD. 3V 756 TNT AIRWAYS S.A. 3X 435 PREMIER TRANS AIRE INC. 4B 184 BOUTIQUE AIR, INC. 4C 035 AEROVIAS DE INTEGRACION REGIONAL 4L 174 LINEAS AEREAS SURAMERICANAS S.A. 4M 469 LAN ARGENTINA S.A. 4N 287 AIR NORTH CHARTER AND TRAINING LTD. 4O 837 ABC AEROLINEAS S.A. DE C.V. 4S 644 SOLAR CARGO, C.A. 4U 051 GERMANWINGS GMBH 4X 805 MERCURY AIR CARGO, INC. 4Z 749 SA AIRLINK 5C 700 C.A.L. CARGO AIRLINES LTD. 5J 203 CEBU PACIFIC AIR 5N 316 JOINT-STOCK COMPANY NORDAVIA - REGIONAL AIRLINES 5O 558 ASL AIRLINES FRANCE 5T 518 CANADIAN NORTH INC. 5U 911 TRANSPORTES AEREOS GUATEMALTECOS S.A. 5X 406 UPS 5Y 369 ATLAS AIR, INC. 50 Standard Agreement For SIS Participation – B16 5Z 225 CEMAIR (PTY) LTD. -

Press Release

PRESS RELEASE Contact: Melissa (Missy) Roberts Vice President of Sales and Marketing 907-771-2510 or 907-230-2913 [email protected] Or Kristin Folmar Director Sales & Marketing 907-771-2599 or 907-301-8871 [email protected] FOR IMMEDIATE RELEASE: April 18, 2016 PENAIR STARTS NEW FLIGHTS FROM PORTLAND, OR TO REDDING, CA AND ARCATA/EUREKA, CA ANCHORAGE, ALASKA – PenAir, one of Alaska’s largest regional airlines, expands their flight schedule out of Portland, with two new destinations on April 21, 2016. PenAir will start twice daily service between both Redding, CA and Arcata/Eureka, CA and Portland, OR. The addition of these two destinations expands PenAir’s offerings from Portland to four communities. In addition to Redding and Arcata/Eureka, PenAir also serves Crescent City, CA and North Bend, OR from their Portland hub. According to Danny Seybert, PenAir’s CEO, “PenAir is thrilled to be expanding our service out of Portland, OR. We have been operating for 60 years throughout Alaska and for the last several years in the Northeast U.S. The expansion of our flights in Portland provides customers with our Alaskan brand of reliable customer service and the benefit of our connectivity to flights with our codeshare partner Alaska Airlines and the other airlines offering service to more than 55 destinations from Portland International Airport.” “PenAir began operating daily service out of Portland, OR, to Crescent City, CA, on September 15, 2015. Since then, we have met with community leaders from each of these three additional communities”, said Dave Hall, PenAir’s Chief Operating Officer. -

United States District Court for the District of Columbia

Case 1:10-cv-02076-EGS Document 35 Filed 06/10/11 Page 1 of 25 UNITED STATES DISTRICT COURT FOR THE DISTRICT OF COLUMBIA ) NORTHERN AIR CARGO, et al., ) ) Plaintiffs, ) ) v. ) ) UNITED STATES POSTAL SERVICE, ) Civil Action No. 10-2076 (EGS) ) Defendant, ) ) and ) ) PENINSULA AIRWAYS, INC., ) ) Defendant-Intervenor. ) ) MEMORANDUM OPINION On December 3, 2010, the United States Postal Service (the “Postal Service”) granted an equitable tender of nonpriority mainline bypass mail to Peninsula Airways, Inc. (“PenAir”) on five mainline routes in rural Alaska pursuant to 39 U.S.C. § 5402(g)(5)(c) (“§ 5402(g)(5)(C)”). This equitable tender is now being challenged by three mainline carriers – Northern Air Cargo (“NAC”), Tatonduk Outfitters Ltd d/b/a Everts Air Cargo (“Everts”), and Lynden Air Cargo LLC (“Lynden”) (collectively, “plaintiffs”). Specifically, plaintiffs challenge the Postal Service’s purportedly ultra vires determination that PenAir had satisfied the “Prior Service and Capacity Requirement” of 39 U.S.C. § 5402(g)(1)(A)(iv)(II) (“§ 5402(g)(1)(A)(iv)(II)”) as of Case 1:10-cv-02076-EGS Document 35 Filed 06/10/11 Page 2 of 25 December 3, 2010.1 Plaintiffs seek both declaratory and injunctive relief. See generally Compl. Pending before the Court is plaintiffs’ motion for summary judgment, as well as the cross-motions for summary judgment filed by Defendant Postal Service and Defendant-Intervenor PenAir (collectively, “defendants”). Upon consideration of the motions, the responses and replies thereto, the applicable law, the entire record, and for the following reasons, the Court hereby DENIES plaintiffs’ motion for summary judgment and GRANTS defendants’ cross-motions for summary judgment. -

Frequently Asked Questions Expressjet Branded Flying October 8, 2007

Frequently Asked Questions ExpressJet Branded Flying October 8, 2007 Q. What is ExpressJet branded flying? A. ExpressJet is convenient, non-stop travel to 25 cities across the United States. ExpressJet’s branded flying operation will include more than 55 non-stop markets and over 220 daily departures in markets that were not well connected. Q. What makes ExpressJet different from other airlines? A. When we thought of our customers, we focused our attention on making air travel as convenient and worry-free as possible. That begins with a maintenance reliability rating that is at the top of our industry, and it continues with a premium on-board experience throughout the flight. Some of the amenities we thought customers would appreciate include: • No middle seat on any of our flights. • Assigned seating on an aisle, a window or both. • Redesigned and more comfortable memory foam leather seats. • Valet carry-on bag service, allowing customers to get on and off the plane quickly, easily and without having to fight with their luggage. • A full array of wine, beer and alcohol selections, complimentary recognized name-brand snacks, plus full-service meal options on longer flights. • Comfy, generously filled pillows and fleece blankets. • 100 choice channels of free XM® Satellite Radio at every seat. • Simple frequent flyer program, JetSetsm. Q. Where will ExpressJet fly? A. Airport Code and Airport Name City Destinations ABQ Albuquerque International Sunport Albuquerque 6 AUS Austin-Bergstrom International Airport Austin 8 BFL Meadows Field Airport Bakersfield 2 BHM Birmingham International Airport Birmingham 1 BOI Boise Airport Boise 2 Page 1 of 4 Airport Code and Airport Name City Destinations COS Colorado Springs Airport Colorado Springs 3 ELP El Paso International Airport El Paso 2 FAT Fresno Yosemite International Airport Fresno 3 GEG Spokane International Airport Spokane 5 JAX Jacksonville International Airport Jacksonville, Fla. -

Uncontrolled Descent and Collision with Terrain, United Airlines 585

PB2001-910401 NTSB/AAR-01/01 DCA91MA023 NATIONAL TRANSPORTATION SAFETY BOARD WASHINGTON, D.C. 20594 AIRCRAFT ACCIDENT REPORT Uncontrolled Descent and Collision With Terrain United Airlines Flight 585 Boeing 737-200, N999UA 4 Miles South of Colorado Springs Municipal Airport Colorado Springs, Colorado March 3, 1991 5498C Aircraft Accident Report Uncontrolled Descent and Collision With Terrain United Airlines Flight 585 Boeing 737-200, N999UA 4 Miles South of Colorado Springs Municipal Airport Colorado Springs, Colorado March 3, 1991 RAN S P T O L R A T LURIBUS N P UNUM A E O T I I O T N A N S A D FE R NTSB/AAR-01/01 T Y B OA PB2001-910401 National Transportation Safety Board Notation 5498C 490 L’Enfant Plaza, S.W. Adopted March 27, 2001 Washington, D.C. 20594 National Transportation Safety Board. 2001. Uncontrolled Descent and Collision With Terrain, United Airlines Flight 585, Boeing 737-200, N999UA, 4 Miles South of Colorado Springs Municipal Airport, Colorado, Springs, Colorado, March 3, 1991. Aircraft Accident Report NTSB/AAR-01/01. Washington, DC. Abstract: This amended report explains the accident involving United Airlines flight 585, a Boeing 737-200, which entered an uncontrolled descent and impacted terrain 4 miles south of Colorado Springs Municipal Airport, Colorado Springs, Colorado, on March 3, 1991. Safety issues discussed in the report are the potential meterological hazards to airplanes in the area of Colorado Springs; 737 rudder malfunctions, including rudder reversals; and the design of the main rudder power control unit servo valve. The National Transportation Safety Board is an independent Federal agency dedicated to promoting aviation, railroad, highway, marine, pipeline, and hazardous materials safety. -

STATE of DOWNTOWN Colorado Springs 2021 ONE YEAR AGO, Downtown Colorado Springs Was Poised to Have Its Best Year Economically in Decades

Economic snapshot and performance indicators STATE OF DOWNTOWN Colorado Springs 2021 ONE YEAR AGO, Downtown Colorado Springs was poised to have its best year economically in decades. The fundamentals were strong, new construction was humming and small business was luring new patrons. Then came the pandemic and ensuing recession, which proved particularly devastating to tourism, restaurants, small business and arts and culture, while also disrupting workforce patterns. But despite these historic challenges, as this report demonstrates, Downtown weathered this crisis far better than most city centers nationwide and is poised for an incredibly strong rebound. New businesses and investors are taking note – making Downtown Colorado Springs one of the hottest up-and-coming markets in the country. Our sixth annual State of Downtown Report notes nearly $2 billion in development – driven by strong multifamily growth, exciting new attractions, and investments in preserving and enhancing Downtown’s unique historic center. This comprehensive benchmarking report is packed with the data, trends and analysis to inform key stakeholders in making sound business decisions, created especially with investors, brokers, developers, retailers, civic leaders and property owners in mind. State of Downtown is produced by the Downtown Development Authority, and most data throughout the report tracks specifically within the DDA boundaries, the natural defining area of Downtown. Where noted, some data is reported for the Greater Downtown Colorado Springs Business Improvement District, the 80903 ZIP code, or the two census tracks that align with the city’s core. Data and rankings are for 2020 except where noted. A special mention about the pandemic: Some sections of this report are briefer than past years, and in some instances data from 2019 is reported instead. -

Logan International Airport

Logan International Airport Mont Blanc Duty Free International Shoppes Kiehl’s Burger King Michael Kors Vino Volo Hugo Boss Starbucks Monicas Durgin-Park Sbarro Mercato TERMINAL E InMotion Shojo TERMINAL C Legal Seafoods C17 Aeromexico Iberia C18 Hudson News Hudson News Air Berlin Icelandair C16 C19 Dunkin Donuts Aer Lingus Air Europa JetBlue Hudson News C20 Travel + Leisure Vacant Alaska Airlines Air France Japan Airlines C21 C15 Duty Free International Shoppes Potbelly Cape Air C14 Alitalia Latam Hudson News Duty Free International Shoppes JetBlue American Airlines Level Mija Natalie’s Candy Jar C11 Vacant Sun Country Airlines Dine Boston Bar & Grill Hudson Stephanie’s Avianca Lufthansa Dunkin’ Donuts News Dunkin Donuts Wahlburgers Duty Free International Shoppes ink by Hudson TAP Portugal Azores Norwegian C12 New England Collections Virgin America Legal Sea Foods British Airways Porter C8 Starbucks iStore Boston Public Market C9 C10 The Black Dog Cathay Pacic Primera Air C36 Hudson News C34 2018 Enplanements 6.7 Million Travel + Leisure Copa Airlines Qatar Airways Hudson News Delta Airlines Scandinavian Airlines Vineyard Grille InMotion Starbucks Hudson News Green Express C32 C26 El Al Swiss Camden Food Company C28 Emirates TACV C30 Vacant C25 C27 Hainan Airlines Tap Portugal Life is Dunkin Donuts Dunkin Donuts Good Jerry Remy’s Boston Beer Works Hudson News Thomas Cook Airlines Hudson News C29 Gogo Stop Turkish Airlines Gogo Gifts Hudson News C40 RYO Asian Fusion C33 C31 Currito 2018 Enplanements 2.2 Million Dunkin Donuts Burger King -

Press Release

PRESS RELEASE Contact: Melissa (Missy) Roberts Vice President of Sales and Marketing 907-771-2510 or 907-230-2913 [email protected] Or Kristin Folmar Director Sales & Marketing 907-771-2599 or 907-301-8871 [email protected] FOR IMMEDIATE RELEASE: February 5, 2016 PENAIR ADDS THREE ADDITIONAL DESTINATIONS FROM PORTLAND, OR ANCHORAGE, ALASKA – PenAir, one of Alaska’s largest regional airlines, has announced that over the next three months they will be expanding service out of Portland, OR, to three additional destinations. On March 21, 2016, PenAir will initiate new daily service from Portland, OR to North Bend/Coos Bay, OR. Effective April 21, 2016, PenAir will provide service out of Portland, OR, to Redding, CA, and Arcata/Eureka, CA. PenAir will operate two flights per day to each of these destinations with their 30-seat Saab 340 turboprop aircraft. According to Danny Seybert, PenAir’s CEO, “Ever since opening our new hub at the Portland Airport, we have continued to look at additional Pacific Northwest destinations. PenAir has been in operation for 60 years throughout Alaska and for the last several years in the Northeast U.S. We plan to provide daily service to Redding, Arcata/Eureka, and North Bend with our Saab 340 aircraft while providing our Alaskan brand of reliable customer service.” “PenAir began operating daily service out of Portland, OR, to Crescent City, CA, on September 15, 2015. Since then, we have met with key officials from each of these three additional communities during the planning process”, said Dave Hall, PenAir’s Chief Operating Officer.