Remodelling Knowing Receipt As a Gains-Based Wrong

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Equitable Allowances Or Restitutionary Measures for Dishonest Assistance and Knowing Receipt

Whayman D. Equitable allowances or restitutionary measures for dishonest assistance and knowing receipt. Northern Ireland Legal Quarterly 2017, 68(2), 181–202. Copyright: © Queen's University School of Law. This is the final version of an article published in Northern Ireland Legal Quarterly by Queen's University School of Law. DOI link to article: https://nilq.qub.ac.uk/index.php/nilq/article/view/34 Date deposited: 10/08/2017 Newcastle University ePrints - eprint.ncl.ac.uk NILQ 68(2): 181–202 Equitable allowances or restitutionary measures for dishonest assistance and knowing receipt DEREK WHAYMAN * Lecturer in Law, Newcastle University Abstract This article considers the credit given to dishonest assistants and knowing recipients in claims for disgorgement, with greater focus on dishonest assistance. Traditionally, equity has awarded a parsimonious ‘just allowance’ for work and skill. The language of causation in Novoship (UK) Ltd v Mikhaylyuk [2014] EWCA Civ 908 suggests a more generous restitutionary approach which is at odds with the justification given: prophylaxis. This tension makes the law incoherent. Moreover, the bar to full disgorgement has been set too high, such that the remedy is unavailable in practice. Therefore, even if the restitutionary approach is affirmed, it must be revised. Keywords: disgorgement; equitable allowances; remoteness of gain; dishonest assistance; knowing receipt. isgorgement in equity has become more widely available. It is familiar as against a fiduciary where the profits of the defaulting fiduciary’s efforts are appropriated to the pDrincipal, seen in cases such as Boardman v Phipps .1 In Novoship (UK) Ltd v Mikhaylyuk , the Court of Appeal held that disgorgement is available in principle against accessories (meaning dishonest assistants and knowing recipients) to a breach of fiduciary duty. -

III. KNOWING Assistance .. ·I·

WHEN IS A STRANGERA CONSTRUCTIVETRUSTEE? 453 WHEN IS A STRANGER A CONSTRUCTIVE TRUSTEE? A CRITIQUE OF RECENT DECISIONS SUSAN BARKEHALL THOMAS• 1his articleexplores the conceptualdevelopment of Cet article explore le developpementconceptuel de third party liabilityfor participation in a breach of responsabilite civile dans la participation a fiduciary duty. 1he authorprovides a criticalanalysis l'inexecution d'une obligationfiduciaire. L 'auteur of thefoundations of third party liability in Canada fournit une analyse critique des fondations de la and chronicles the evolution of context-specific responsabilitecivile au Canada et decrit /'evolution liability tests. In particular, the testsfor the liability d'essais de responsabilites particulieres a une of banks and directorsare developed in their specific situation.Les essais de responsabilitedes banques el contexts. 1he author then provides a reasoned des adminislrateurssont particulierementdeveloppes critique of the Supreme Court of Canada's recent dans leur contexte precis. L 'auteurfournit ensulte trend towards context-independenttests. 1he author une critique raisonnee de la recente tendance de la concludes by arguing that the current approach is Cour supreme du Canada pour /es essais inadequateand results in an incoherentframework independantset particuliersa une situation.L 'auteur for the law of third party liability in Canada. conclut en pretendant que la demarche actuelle est inadequateet entraine un cadre incoherentpour la loi sur la responsabilitecivile au Canada. TABLE OF CONTENTS I. IN1R0DUCTION . • • • • . • . • . 453 II. KNOWING PARTICIPATION ......••...........•....•..... 457 A. BANKCASES . 457 B. APPLICATIONOF TIIE "PuT ON INQUIRY" TEST .....•...... 459 C. CONCEPTUALPROBLEMS Wl11I THE "PuT ON INQUIRY" TEST • . • . • • • . • . • . • . 463 D. CONCLUSIONSFROM PART II . 467 III. KNOWING AsSISTANCE .. ·I·............................ 467 A. THEAIR CANADA DECISION . • • • . • . 468 IV. -

Overview of the Constructive Trust

Overview of the constructive trust A paper presented to the Society of Trust and Estates Practitioners – QLD Branch Tuesday 6 June 2017 Denis Barlin Barrister 13 Wentworth Selborne Chambers 180 Phillip Street Sydney, New South Wales [email protected] (02) 9231 6646 Contents 1. Overview of the constructive trust .................................................................................................. 3 2. “Remedial” and “institutional” constructive trusts ......................................................................... 5 3. Fairness is not the criteria for the imposition of a constructive trust ............................................. 7 4. Remedial Constructive Trust and Presumed Resulting Trust .......................................................... 7 5. Recipients of trust property – constructive trusts ........................................................................... 8 6. Subsequent awareness of the receipt of trust property ................................................................. 8 7. Tracing .............................................................................................................................................. 9 8. Mutual wills and constructive trusts................................................................................................ 9 9. Trustee de son tort.........................................................................................................................11 10. Threshold questions to be considered for there to be constructive -

Cambridge University Press 978-1-316-62194-3 — Equity and Trusts in Australia Michael Bryan , Vicki Vann , Susan Barkehall Thomas Index More Information INDEX

Cambridge University Press 978-1-316-62194-3 — Equity and Trusts in Australia Michael Bryan , Vicki Vann , Susan Barkehall Thomas Index More Information INDEX accounts of profits, 54–5, 169 limitation statutes, 84–5 remedies for. See remedies allowances, 57–8 unclean hands, 86–8, 168 for breach of trust breach of confidence, 197 beneficiaries, 206 ‘but for’ test, 65–6, 333 calculation of, 55–7 administration of trust and, acquiescence, 85–6 207 calculation of equitable as equitable defence to creditors’ rights and, 313–14 compensation, 60–1 breach of trust, 329–30 differences between fixed breach of fiduciary duty, overlap with laches, 85–6 and discretionary trusts 63–5 advancement for, 207 breach of trust, 61–3 presumption of, 357–9 ‘gift-over’ right, 208–9 calculation of equitable agency indemnification of trustees, damages trusts and, 210–11 311–13 causation standard, 65–6 aggravated damages, 68 interest, trustees’ right to common law adjustments to Anton Piller order, 39 impound, 314 quantum, 66–8 Aristotle, 4 investment of trust funds, categories of constructive trusts, assessment of equitable 297, 299 371 damages, 51 ‘list certainty’, 227 as remedy to proprietary in addition to injunction or sui juris, 278, 312 estoppel, 380–2 specific performance, 51 trust property and, 208 as restitutionary remedy in substitution for injunction trustees’ right to recover for unjust enrichment, or specific performance, overpayment from, 315 380–2 51–2 breach of confidence, 17–18, 47, Baumgartner constructive assignments 50, 68 trusts, 375–9 equitable property, 138–9 defences to. See defences to common intention, family future property, 137–8 breach of confidence property disputes and, gifts, 133–6 remedies for. -

Remedies for Breach of Contract

Remedies for Breach of Contract: The Jimi Hendrix Experience a presentation by SIMON EDWARDS at 39 Essex Street on 2nd December 2003 1. In Ruxley Electronics and Construction Limited v Forsyth [1996] AC 344 Lord Bridge started his speech with these words, “My Lords, damages for breach of contract must reflect, as accurately as the circumstances allow, the loss which the Claimant has sustained because he did not get what he bargained for. There is no question of punishing the contract breaker”. In Attorney General v Blake (2001) 1 AC 268, the House of Lords introduced a substantial departure from that principle. 2. The majority (Lord Hobhouse dissenting) held that in “exceptional circumstances” a contract breaker could be ordered to account to a Claimant for the benefits he received from the breach of contract. The breach of contract in the Blake case was that of a member of the Secret Intelligence Service who had spied for the Soviet Union. Later he wrote a book about his exploits and the Attorney General took action, amongst other things, to “expropriate” the royalties that he was to receive from the publication of the book. 3. Ultimately that action was successful. The House of Lords based its decision on a breach of the contractual undertaking that Blake had given not to divulge any official information that he had gained during the course of his employment. The House of Lords held that in the exceptional circumstances of the case the courts could afford to the Crown the remedy, described by Lord Hobhouse as being “essentially punitive”, of ordering an account of profits. -

CLAIMS AGAINST THIRD PARTIES Jeremy Bamford & Simon Passfield, Guildhall Chambers

CLAIMS AGAINST THIRD PARTIES Jeremy Bamford & Simon Passfield, Guildhall Chambers A. Introduction 1. This paper supports and provides the references for the Wonderland Ltd case study1 which will be considered during the seminar. 2. The aim of the case study is to explore claims which go beyond the usual fare of the office- holder’s statutory remedies by way of transactions at an undervalue, preference, s. 212 misfeasance claims, wrongful or fraudulent trading or transactions defrauding creditors. Instead we explore claims against third parties, where there has been a breach of the Companies Act and/or breach of fiduciary duty by directors, unlawful dividends being used as an example. B. Dividends 3. There are usually 3 potential grounds for challenging dividend payments: 3.1. the conventional technical claim made under the Companies legislation that dividends have not been paid out of profits available for that purpose and that the dividends have been paid in breach of the Companies legislation; 3.2. that the internal regulations of the company were breached and/or 3.3. breach of the common law maintenance of capital rule. We consider these in turn. B1 Part VIII CA 1985 4. In the case study the dividends were paid between 1 Sep 2007 and 1 March 2008. The relevant law is therefore Part VIII Companies Act 1985 (ss. 263 – 281 CA 1985)2. 5. A distribution of a company’s assets (which includes a dividend) can only be made out of profits available for the purpose (s. 263(1) CA 1985)3 being its accumulated, realised profits, so far as not previously utilised by distribution or capitalisation, less its accumulated, realised losses, so far as not previously written off in a reduction or reorganisation of capital duly made (s. -

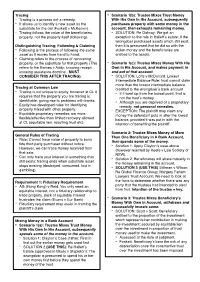

Tracing Is a Process Not a Remedy

Tracing - Scenario 1(b): Trustee Mixes Trust Money - Tracing is a process not a remedy. With His Own In His Account, subsequently - It allows us to identify a new asset as the purchases property with some money in the substitute for the old (Foskett v McKeown). account, then exhausts remaining money. - Tracing follows the value of the beneficiaries - SOLUTION: Re Oatway: We get an property, not the property itself (following). exception to the rule in Hallett’s estate: if the wrongdoer purchased assets which still exist, Distinguishing Tracing; Following & Claiming then it is presumed that he did so with the - Following is the process of following the same stolen money and the beneficiaries are asset as it moves from hand to hand. entitled to the assets. - Claiming refers to the process of recovering property, or the substitute for that property (This - Scenario 1(c): Trustee Mixes Money With His refers to the Barnes v Addy; knowing receipt, Own In His Account, and makes payment in knowing assistance doctrine - MUST and out of that account. CONSIDER THIS AFTER TRACING). - SOLUTION: Lofts v McDonald: Lowest Intermediate Balance Rule: trust cannot claim more than the lowest intermediate balance Tracing at Common Law - credited to the wrongdoer’s bank account Tracing is not unique to equity, however at CL it - If it went up from the lowest point, that is requires that the property you are tracing is not the trust’s money. identifiable, giving rise to problems with banks. - - Although you are deprived of a proprietary Equity has developed rules for identifying remedy, not personal remedies. -

2019 Review Succession & Probate

AYCHT 27/7/2019 2019 review Succession & Probate Au‐Yeung Cheng Ho Tin solicitors –CPD 28 July 2019 Tak Wong 1 遺囑效力 Date Neutral Citation No Pltf Remarks 2019-04-11 [2019] CFI 925 CHU PONG Limited will 08, LA. Consent Rv LA YUEN probate Proof due execution: sol fail Irrational will (to stranger) 2019-02-01 [2019] CFI 238 TAI PUI SHAN Proof due execution: subpoena. DONNA Normal pattern. sol pass §21 presumption of revocation §26 late amend pleading revocation §34 2019-01-28 [2019] CFI 103 CHEUNG TAI 2 informal wills of same date. s.5(2) SHING Cumulative, not inconsistent. All interested : parties & not oppose. Both admitted to probate. 2 1 AYCHT 27/7/2019 遺囑效力 Date Neutral Citation No Pltf Remarks 2018-12-19 [2018] CFA 61 CHOY PO B v G evidence 3 limbs T/C.gap§11 CHUN fact-specific. No proper basis will instruction §18. will invalid 2019-04-18 [2019] CA 452 MOK HING Same B v G 3 limbs T/C. CHUNG fact-specific Yes proper basis. Choy Po Chun distinguished. Will instruction direct / rational Sol > sol firm. Will valid. 3 親屬關係 Date Neutral Citation No Pltf Remarks 2018-08-08 [2018] CA 491 LI CHEONG Natural dau, 1. DNA 2. copy B/C, rolled-up hearing directions 2018-10-18 [2018] CA 719 LI CHEONG Probate action in rem nature, O.15 r.13A, intended intervener, dismiss 2014-07-03 MOK HING CCL:spinster 1.no adopt §89 2.yes CHUNG i-tze 3.yes IEO s2(2)(c) 4.DWAE案 2018-10-19 [2018] CA 713 MOK HING CCL adoption v i-tze, apply to file CHUNG obituary notice, Ladd, dismiss 2019-04-18 [2019] CA 452 MOK HING CCL no formalities (adoption/i-tze) CHUNG §52, all 7 appeal grounds no merit. -

A Commonwealth of Perspective on Restitutionary Disgorgement for Breach of Contract

A Commonwealth of Perspective on Restitutionary Disgorgement for Breach of Contract Caprice L. Roberts Table of Contents I. Introduction: Contractual Disgorgement Remedy as Watershed.....................................................................................946 II. Section 39 of the Pending American Restatement of Restitution ....................................................................................950 III. Comparative Roots & Flaws of Section 39’s Proposed Disgorgement Remedy .................................................................953 A. Blake’s Resonance and Other Signposts of Commonwealth Support ........................................................954 B. Section 39’s Adoption of Blake’s Remedial Theory but with Narrow Application .................................................961 C. Lessons of Blake & Practical Flaws of Section 39.................965 1. Section 39’s Potential May Be Lost for Its Cumbersome Nature........................................................965 2. Section 39 Asserts Its Narrowness, but to What End?......................................................................966 IV. Intellectual Godparents to Section 39...........................................967 Professor of Law, West Virginia University. The author is indebted to Andrew Kull for graciously accepting criticism of the pending American Restatement provision on disgorgement, providing substantive feedback, and provoking my continued interest in assisting with the artful navigation of drafting this important contractual -

Unconscionability As an Underlying Concept in Equity

THE DENNING LAW JOURNAL UNCONSCIONABILITY AS A UNIFYING CONCEPT IN EQUITY Mark Pawlowski* ABSTRACT This article seeks to examine the extent to which a unified concept of unconscionability can be used to rationalise related doctrines of equity, in particular, in the areas of (1) unconscionable bargains, undue influence and duress (2) proprietary estoppel (3) knowing receipt liability and (4) relief against forfeitures. The conclusion is that such a process of amalgamation may provide a principled doctrinal basis for equity’s intervention which has already found favour in the English courts. INTRODUCTION A recent discernible trend in equity has been the willingness of the English courts to adopt a broader-based doctrine of unconscionability as underlying proprietary estoppel claims and the personal liability of a stranger to a trust who has knowingly received trust property in breach of trust. The decisions in Gillett v Holt,1 Jennings v Rice2 and Campbell v Griffin3 in the context of proprietary estoppel and Bank of Credit and Commerce International (Overseas) Ltd v Akindele4 on the subject of receipt liability, demonstrate the judiciary’s growing recognition that the concept of unconscionability provides a useful mechanism for affording equitable relief against the strict insistence on legal rights or unfair and oppressive conduct. This, in turn, prompts the question whether there are other areas which would benefit from a rationalisation of principles under the one umbrella of unconscionability. The process of amalgamation, it is submitted, would be particularly useful in areas where there are currently several related (but distinct) doctrines operating together so as to give rise to confusion and overlap in the same field of law. -

Accounting of Profits Calculations in Intellectual Property Cases in Canada.Pdf

ACCOUNTING OF PROFITS IN INTELLECTUAL PROPERTY CASES IN CANADA Norman V. Siebrasse Alexander J. Stack 103543 Cole Article Bookrev 3/26/08 2:39 PM Page 3 INTRODUCTION..............................................................................................................................1 1.0 ACTUAL PROFITS AND DIFFERENTIAL PROFITS .....................................................3 1.1 Take the Infringer as you find him...........................................................................................3 1.2 The Actual Profits Approach....................................................................................................3 1.3 Differential Profits Approach and the “But For” position ........................................................3 2.0 REVENUES ...........................................................................................................................8 2.1 The Sale of Convoyed Products ...............................................................................................8 2.2 Revenue Realized Through the Actions of Third Parties (Other Than Customers) ..................9 2.3 Profits Made in Foreign Jurisdictions.......................................................................................9 2.4 Profits Achieved by Wholly Owned Subsidiaries....................................................................10 2.5 Profits of Less Than a 100 Percent Owned Entity .................................................................10 2.6 Earned But Unrealized Profits................................................................................................10 -

Unit 5 – Equity and Trusts Suggested Answers - January 2013

LEVEL 6 - UNIT 5 – EQUITY AND TRUSTS SUGGESTED ANSWERS - JANUARY 2013 Note to Candidates and Tutors: The purpose of the suggested answers is to provide students and tutors with guidance as to the key points students should have included in their answers to the January 2013 examinations. The suggested answers set out a response that a good (merit/distinction) candidate would have provided. The suggested answers do not for all questions set out all the points which students may have included in their responses to the questions. Students will have received credit, where applicable, for other points not addressed by the suggested answers. Students and tutors should review the suggested answers in conjunction with the question papers and the Chief Examiners’ reports which provide feedback on student performance in the examination. SECTION A Question 1 This essay will examine the general characteristics of equitable remedies before examining each remedy in turn to analyse whether they are in fact strict and of limited flexibility as the question suggests. The best way to examine the general characteristics of equitable remedies is to draw comparisons with the common law. Equitable remedies are, of course discretionary, whereas the common law remedy of damages is available as of right. This does not mean that the court has absolute discretion, there are clear principles which govern the grant of equitable remedies. Equitable remedies are granted where the common law remedies would be inadequate or where the common law remedies are not available because the right is exclusively equitable. One of the key characteristics of equitable remedies is of course that they act in personam.