Geneva, November 10, 2020 MSCI GLOBAL SMALL CAP INDEXES

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Full Portfolio Holdings

Hartford Multifactor International Fund Full Portfolio Holdings* as of August 31, 2021 % of Security Coupon Maturity Shares/Par Market Value Net Assets Merck KGaA 0.000 152 36,115 0.982 Kuehne + Nagel International AG 0.000 96 35,085 0.954 Novo Nordisk A/S 0.000 333 33,337 0.906 Koninklijke Ahold Delhaize N.V. 0.000 938 31,646 0.860 Investor AB 0.000 1,268 30,329 0.824 Roche Holding AG 0.000 74 29,715 0.808 WM Morrison Supermarkets plc 0.000 6,781 26,972 0.733 Wesfarmers Ltd. 0.000 577 25,201 0.685 Bouygues S.A. 0.000 595 24,915 0.677 Swisscom AG 0.000 42 24,651 0.670 Loblaw Cos., Ltd. 0.000 347 24,448 0.665 Mineral Resources Ltd. 0.000 596 23,709 0.644 Royal Bank of Canada 0.000 228 23,421 0.637 Bridgestone Corp. 0.000 500 23,017 0.626 BlueScope Steel Ltd. 0.000 1,255 22,944 0.624 Yangzijiang Shipbuilding Holdings Ltd. 0.000 18,600 22,650 0.616 BCE, Inc. 0.000 427 22,270 0.605 Fortescue Metals Group Ltd. 0.000 1,440 21,953 0.597 NN Group N.V. 0.000 411 21,320 0.579 Electricite de France S.A. 0.000 1,560 21,157 0.575 Royal Mail plc 0.000 3,051 20,780 0.565 Sonic Healthcare Ltd. 0.000 643 20,357 0.553 Rio Tinto plc 0.000 271 20,050 0.545 Coloplast A/S 0.000 113 19,578 0.532 Admiral Group plc 0.000 394 19,576 0.532 Swiss Life Holding AG 0.000 37 19,285 0.524 Dexus 0.000 2,432 18,926 0.514 Kesko Oyj 0.000 457 18,910 0.514 Woolworths Group Ltd. -

Cyient Ltd Cyient Ltd Bloomberg Code: CYL in India Research - Stock Broking BUY

Aug 03, 2016 Information Technology-Technology Services Cyient Ltd Cyient Ltd Bloomberg Code: CYL IN India Research - Stock Broking BUY Moderate Capex Leads to Healthy Free Cash Flow Generation Recommendation (Rs.) CMP (as on Aug 02, 2016) 513 During FY16, Cyient has recorded a cash balance of Rs.7741Mn (cash balance Target Price 589 including the liquid investments) after the four acquisitions made during Upside (%) 15 FY15-FY16. Operating cash flow after adjusting the working capital changes, has Stock Information picked up to 60.0% levels of EBITDA; it has witnessed 90.2% of EBITDA during FY15. Cash per share has grown by 12.5% CAGR during FY12-FY16. Moderate Mkt Cap (Rs.mn/US$ mn) 57713 / 865 capex (Capex/EBITDA multiple of 3.2x, 5.0x and 5.1x during FY16, FY17E and 52-wk High/Low (Rs.) 643 / 369 FY18E respectively) behind the healthy free cash flow generation. 3M Avg. daily volume (mn) 0.07 Revival in business growth, besides healthy deal pipeline and strong Beta (x) 0.68 backlog orders. Rangsons and Softential business performance to be Sensex/Nifty 27982 / 8623 O/S Shares(mn) 112.50 watched: Cyient has recorded a deal pipeline of around US$1021Mn at the end Face Value (Rs.) 5.0 of FY16, a growth of 27.6% from US$799 Mn (during FY15). FY16 has witnessed a Shareholding Pattern (%) weak revenue growth, due to headwinds from the business investments (Softential and Rangsons) and few client specific issues. However, strong orders intake Promoters 22.2 during FY16, besides pickup in orders execution during FY16 displays the revival FIIs 41.4 in business growth. -

Wilmington Funds Holdings Template DRAFT

Wilmington Global Alpha Equities Fund as of 5/31/2021 (Portfolio composition is subject to change) ISSUER NAME % OF ASSETS USD/CAD FWD 20210616 00050 3.16% DREYFUS GOVT CASH MGMT-I 2.91% MORGAN STANLEY FUTURE USD SECURED - TOTAL EQUITY 2.81% USD/EUR FWD 20210616 00050 1.69% MICROSOFT CORP 1.62% USD/GBP FWD 20210616 49 1.40% USD/JPY FWD 20210616 00050 1.34% APPLE INC 1.25% AMAZON.COM INC 1.20% ALPHABET INC 1.03% CANADIAN NATIONAL RAILWAY CO 0.99% AIA GROUP LTD 0.98% NOVARTIS AG 0.98% TENCENT HOLDINGS LTD 0.91% INTACT FINANCIAL CORP 0.91% CHARLES SCHWAB CORP/THE 0.91% FACEBOOK INC 0.84% FORTIVE CORP 0.81% BRENNTAG SE 0.77% COPART INC 0.75% CONSTELLATION SOFTWARE INC/CANADA 0.70% UNITEDHEALTH GROUP INC 0.70% AXA SA 0.63% FIDELITY NATIONAL INFORMATION SERVICES INC 0.63% BERKSHIRE HATHAWAY INC 0.62% PFIZER INC 0.62% TOTAL SE 0.61% MEDICAL PROPERTIES TRUST INC 0.61% VINCI SA 0.60% COMPASS GROUP PLC 0.60% KDDI CORP 0.60% BAE SYSTEMS PLC 0.57% MOTOROLA SOLUTIONS INC 0.57% NATIONAL GRID PLC 0.56% PUBLIC STORAGE 0.56% NVR INC 0.53% AMERICAN TOWER CORP 0.53% MEDTRONIC PLC 0.51% PROGRESSIVE CORP/THE 0.50% DANAHER CORP 0.50% MARKEL CORP 0.49% JOHNSON & JOHNSON 0.48% BUREAU VERITAS SA 0.48% NESTLE SA 0.47% MARSH & MCLENNAN COS INC 0.46% ALIBABA GROUP HOLDING LTD 0.45% LOCKHEED MARTIN CORP 0.45% ALPHABET INC 0.44% MERCK & CO INC 0.43% CINTAS CORP 0.42% EXPEDITORS INTERNATIONAL OF WASHINGTON INC 0.41% MCDONALD'S CORP 0.41% RIO TINTO PLC 0.41% IDEX CORP 0.40% DIAGEO PLC 0.40% LENNOX INTERNATIONAL INC 0.40% PNC FINANCIAL SERVICES GROUP INC/THE 0.40% ACCENTURE -

The Mineral Industry of Japan in 1998

THE MINERAL INDUSTRY OF JAPAN By John C. Wu Japan’s reserves of limestone, pyrophyllite, and silica are important role in supplying the ferrous and nonferrous metals, quite large. Japan has considerable reserves of coal and iodine, fabricated metal products, and industrial mineral products to but its reserves of natural gas and crude petroleum are very the construction and manufacturing industries of China, small. As a result of exploration conducted in the past 5 years including Hong Kong, Indonesia, the Republic of Korea, by the Metal Mining Agency of Japan (MMAJ), a Malaysia, Singapore, Thailand, and Taiwan. semigovernment agency under the Ministry of International For the first time since the end of World War II, the Japanese Trade and Industry (MITI), reserves of gold, lead, and zinc had economy went into a severe recession in 1998 after 5 years of been extended (Metal Mining Agency of Japan, 1998a), but slow growth in the 1990’s. According to the Economic Japan’s reserves of ferrous and nonferrous minerals are small. Planning Agency and MITI, Japan’s economy, as measured by Japan relied on imports to meet more than 95% of its raw GDP in 1990 constant yen, contracted 2.8% in 1998. material requirements for energy, ferrous metals, and Restructuring in the financial, manufacturing, and other sectors nonferrous metals for its mineral-processing and mineral- had resulted in a substantial increase in unemployment, which related manufacturing sectors. Japan also relied on imports to reached a record rate of 4.1% in 1998. The depressed real meet between 10% and 25% of its requirements for refined estate and stock markets had caused the major banks to carry a nonferrous metal products, industrial mineral products, and heavy load of bad loans, with limited funds available for refined petroleum products. -

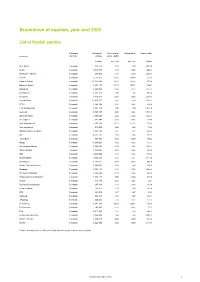

Breakdown of Equities, Year-End 2020

Breakdown of equities, year-end 2020 Listed Danish equities Company Number of Ownership of Voting rights Market value Company domicile equities share capital number per cent per cent DKKm ALK-Abello Denmark 830,794 7.46 4.10 2,077.0 Ambu Denmark 4,818,951 1.91 0.86 1,268.3 AP Moller - Maersk Denmark 253,690 1.27 0.90 3,358.9 Asetek Denmark 2,722,415 10.30 10.30 210.3 Bang & Olufsen Denmark 17,092,036 13.92 13.92 573.6 Bavarian Nordic Denmark 5,904,171 10.11 10.11 1,104.1 Carlsberg Denmark 1,227,664 0.84 0.27 1,197.2 Chr Hansen Denmark 1,381,570 1.06 1.06 865.4 Coloplast Denmark 1,310,347 0.61 0.35 1,218.1 Danske Bank Denmark 13,693,257 1.60 1.60 1,378.2 DFDS Denmark 1,949,162 3.32 3.32 536.4 DSV PANALPINA Denmark 2,281,956 1.00 1.00 2,327.6 Genmab Denmark 1,166,965 0.09 0.09 1,544.8 GN Store Nord Denmark 3,166,046 2.24 2.24 1,542.5 H Lundbeck Denmark 931,964 0.47 0.47 194.6 H+H International Denmark 2,107,893 11.72 11.72 278.2 Huscompagniet Denmark 615,000 3.08 3.08 76.9 INVISIO Communications Denmark 3,183,701 7.22 7.22 589.2 ISS Denmark 4,551,135 2.46 2.46 479.7 Jyske Bank 1 Denmark 455,709 0.63 0.00 106.2 Matas Denmark 1,846,027 4.82 4.82 159.5 Netcompany Group Denmark 1,660,500 3.33 3.33 1,033.7 Nilfisk Holding Denmark 1,436,062 5.29 5.29 189.0 NKT Denmark 2,637,690 6.14 6.14 715.3 Novo Nordisk Denmark 7,546,288 0.32 0.11 3,219.6 Novozymes Denmark 1,724,215 0.61 0.23 602.6 Nordic Transport Group Denmark 1,086,064 4.80 4.80 278.0 Pandora Denmark 2,153,187 2.16 2.16 1,466.3 Per Aarsleff Holding Denmark 2,064,304 10.13 6.34 636.8 Ringkjoebing -

Published on 7 October 2016 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 31 October 2016) Published on 7 October 2016 1. Constituents Change Addition( 70 ) Deletion( 60 ) Code Issue Code Issue 1810 MATSUI CONSTRUCTION CO.,LTD. 1868 Mitsui Home Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 2196 ESCRIT INC. 2117 Nissin Sugar Co.,Ltd. 2198 IKK Inc. 2124 JAC Recruitment Co.,Ltd. 2418 TSUKADA GLOBAL HOLDINGS Inc. 2170 Link and Motivation Inc. 3079 DVx Inc. 2337 Ichigo Inc. 3093 Treasure Factory Co.,LTD. 2359 CORE CORPORATION 3194 KIRINDO HOLDINGS CO.,LTD. 2429 WORLD HOLDINGS CO.,LTD. 3205 DAIDOH LIMITED 2462 J-COM Holdings Co.,Ltd. 3667 enish,inc. 2485 TEAR Corporation 3834 ASAHI Net,Inc. 2492 Infomart Corporation 3946 TOMOKU CO.,LTD. 2915 KENKO Mayonnaise Co.,Ltd. 4221 Okura Industrial Co.,Ltd. 3179 Syuppin Co.,Ltd. 4238 Miraial Co.,Ltd. 3193 Torikizoku co.,ltd. 4331 TAKE AND GIVE. NEEDS Co.,Ltd. 3196 HOTLAND Co.,Ltd. 4406 New Japan Chemical Co.,Ltd. 3199 Watahan & Co.,Ltd. 4538 Fuso Pharmaceutical Industries,Ltd. 3244 Samty Co.,Ltd. 4550 Nissui Pharmaceutical Co.,Ltd. 3250 A.D.Works Co.,Ltd. 4636 T&K TOKA CO.,LTD. 3543 KOMEDA Holdings Co.,Ltd. 4651 SANIX INCORPORATED 3636 Mitsubishi Research Institute,Inc. 4809 Paraca Inc. 3654 HITO-Communications,Inc. 5204 ISHIZUKA GLASS CO.,LTD. 3666 TECNOS JAPAN INCORPORATED 5998 Advanex Inc. 3678 MEDIA DO Co.,Ltd. 6203 Howa Machinery,Ltd. 3688 VOYAGE GROUP,INC. 6319 SNT CORPORATION 3694 OPTiM CORPORATION 6362 Ishii Iron Works Co.,Ltd. 3724 VeriServe Corporation 6373 DAIDO KOGYO CO.,LTD. 3765 GungHo Online Entertainment,Inc. -

Msci Kokunai Japan Equity Indices November 2005 Semi-Annual Index Review

MSCI KOKUNAI JAPAN EQUITY INDICES NOVEMBER 2005 SEMI-ANNUAL INDEX REVIEW Geneva, November 16, 2005. MSCI Barra, a leading provider of benchmark indices and risk management analytics products, announced today changes to the MSCI KOKUNAI Japan Equity Indices that will be effective as of the close of November 30, 2005. These changes result from the November 2005 Semi-Annual Index Review. The full list of additions to and deletions from the MSCI KOKUNAI Japan Equity Indices as well as an updated methodology book have been posted on MSCI’s web site at http://www.msci.com/japan. The additions to the MSCI KOKUNAI Large Cap 200 Index are Ibiden Co and TBS Tokyo Broadcasting. There will be no deletions from the MSCI KOKUNAI Large Cap 200 Index. For the MSCI KOKUNAI Mid Cap 400 Index, there will be 11 additions and five deletions. The five largest additions are Daikyo, Sumitomo Warehouse Co, Okuma Holdings, Japan Steel Works and Amano Corp. There will be 29 additions to the MSCI KOKUNAI Small Cap 900 Index. The largest five additions are Fintech Global, Advanced Media, Link Theory Holdings Co, Mie Bank and Cima Co. 21 securities will be deleted from the MSCI KOKUNAI Small Cap 900 Index. There will be 121 additions to the MSCI KOKUNAI Micro Cap Index. The five largest additions are Aeon Kyushu Co, Yondenko Corp, Dynapac Co, Chuo Warehouse Co and Chuo Kagaku Co. There will be eight deletions from the MSCI KOKUNAI Micro Cap Index. For the MSCI KOKUNAI Investable Market Value Index, there will be 232 additions or upward changes in Value Inclusion Factors (VIFs) and 165 deletions or downward changes in VIFs. -

Case Study Cyient Helps Increase Market Share Through Product

Cyient helps Increase Market Share Through Product Innovation 100-ton cross-terrain truck crane developed Customer to arrive at an agreed-upon vehicle definition, incorporating significant Cyient contributions to the crane’s major subsystem designs. A global market leader in the world of heavy These systems included the frame, decking, construction equipment manufacturing, fenders, x-type outriggers, outrigger hub, this Fortune 500 Cyient, Inc. client provides superstructure, suspension systems, lower and diversified mechanical solutions for industrial upper cab and boom hydraulics. In addition, the applications ranging from infrastructure Cyient team helped to develop the crane’s Tier construction to surface mining and IV/RoW engine, powertrain integration, and transportation. Today shipping to more than 170 electrical/pneumatic systems integration. countries, their chief products include cranes, aerial work platforms, material handling and processing systems, digger derricks and auger The final design was then digitally validated drills. using FEA (finite element analysis), CFD (computational fluid dynamics) analysis and hand Business Need calculations in order to assure quality and full compliance with the norms and regulations in place throughout the United States and Canada, In an effort to increase their market share, the including: client selected Cyient as its engineering partner to help develop its first ever 100-ton cross- • Emission regulations and standards terrain truck crane. • Intermodal roadability regulations Client requirements -

ROCKWOOL Koncernen Øger De Forretningsmæssige Resultater

ROCKWOOL International A/S Meddelelse nr. 2 – 2016 Hovedgaden 584, Indgang C Til Nasdaq Copenhagen 2640 Hedehusene Tlf.: 46 56 03 00 www.rockwool.com CVR-nr.: 54879415 Side 1/1 26. februar 2016 ROCKWOOL koncernen øger de forretningsmæssige resultater Bestyrelsen for ROCKWOOL International A/S har i dag godkendt årsrapporten for 1. januar – 31. december 2015. CEO Jens Birgersson udtaler om koncernens resultater: ”Vi fik en god start på vores forandringsprogram og en god afslutning på året. Vi er sikre på at programmet vil give sig udslag i bedre resultater og øget indtjening. De globale markeder for byggeri er ikke upåvirkede af den generelle økonomiske uro men vi fastholder vores ambition om at fortsætte den positive vækst”. Hovedpunkter 2015 Omsætningen steg med 2,2 % i lokal valuta. Omsætningen blev på EUR 2.208 mio., en stigning på 1,3 % i rapporterede tal. Koncernens forandringsprogram forløber som planlagt og fratrædelsesomkostninger relateret til 2015 beløber sig til EUR 15,4 mio. En nedskrivning af forretningerne i Indien og Kina på EUR 21,4 mio. er inkluderet i 2015. Årets driftsresultat uden de ovennævnte poster steg med 6 % til EUR 172 mio. svarende til 7,8 % EBIT ratio – en stigning på 0,4 procent point i forhold til sidste år. Cash flow fra driftsaktiviteter udgjorde EUR 297 mio. – en stigning på 45 % i forhold til 2014. Investeringer og akkvisitioner udgjorde i alt EUR 201 mio. Udbyttet foreslås øget fra DKK 11,30 til DKK 11,50 pr. aktie. Forventninger til 2016 Koncernen forventer en svagt positiv omsætningsstigning i lokal valuta i 2016. -

ROCKWOOL International A/S

ROCKWOOL International A/S Annual General Meeting 7 April 2021 Annual General Meeting 7 April 2021 © ROCKWOOL International A/S 1 Agenda 1. The board of directors’ report on the company’s activities during the past financial year 2. Presentation of annual report with auditors’ report 3. Adoption of the annual report for the past financial year and discharge of liability for the management and the board of directors 4. Presentation of and advisory vote on remuneration report 5. Approval of the remuneration of the board of directors for 2021/2022 6. Allocation of profits according to the adopted accounts 7. Election of members to the board of directors 8. Appointment of auditors 9. Proposals from the board of directors or shareholders Proposals from the board of directors: 9a. Authorization to acquire own shares 9b. Reduction of the company’s share capital for the purpose of cancelling own shares 9c. Proposal for amendments of the Articles of Association (i) Electronic general meeting (ii) Remuneration report Proposals from shareholders: 9d. Assessment of environmental and community impacts from siting of manufacturing facilities 9e. Disclosure of political contributions 10. Any other business Annual General Meeting 7 April 2021 © ROCKWOOL International A/S 2 Agenda item 1 and 2 The board of directors’ report on the company’s activities during the past financial year and presentation of annual report with auditors’ report Annual General Meeting 7 April 2021 © ROCKWOOL International A/S 3 Annual General Meeting 2021 Thomas Kähler Chairman -

Cyient Ltd January 18, 2018

Cyient Ltd January 18, 2018 Analyst: Mayank Babla (022) 67141412 Initiating Coverage @ Dalal Broacha BUY Cyient provides engineering, manufacturing, geospatial, network, and operations Current Price management services to global industry leaders. The company has a network of more than 590 14,000 associates across 38 global solutions and specializes in Engineering Design, Electronics Target Price 699 Manufacturing & Precision Machining, Aftermarket services, Network Engineering and Upside/Downside 18% Solution Designs, System Development and Integration, Service Assurance & Maintenance, Geospatial Solutions, Big Data Consulting, IOT/MSM and Advanced Analytics. 52 Week Range 605/440 Expect overall Engineering outsourcing market to increase as well as outsourcing to India Key Share Data to grow at 13.7% CAGR between FY17 and FY2021E Market M M Market Cap (Rs.bn) 65.5 Of the $232 Bn spent by G500 companies on ER&D, only $85 Bn is outsourced to ‘offshore rd Market Cap (US$ mn) inhouse R&D centers’ ($34 Bn) and ‘Offshore 3 party engineering service providers’ $51 Bn). 1,023 Industry estimates indicate that the pie of 3rd party engineering providers will increase at a No of o/s shares (mn) 112 CAGR of 9.3% between FY17 and FY21E. Of the $51 Bn outsourced to 3rd party, Indian Face Value 5 companies account for on $8.9 Bn only. This figure is estimated to grow at 14% CAGR Monthly Avg. between FY17 and FY21E. We expect IT engineering service providers such as Cyient, Persistent, KPIT and Tata Elxsi to be major beneficiary of this trend. vol(BSE+NSE) Nos’000 146.4 BSE Code 532175 Expect A&D, Communications, Transportation, Semi-conductor and DLM verticals, which NSE Code CYIENT contribute ~76% of overall revenues to report higher double-digit growth over FY19Eand Bloomberg CYL IN FY20E Cyient’s unique vertical mix ensures benefit from key industry growth drivers. -

3-068-18 Susanne Dyrbol

Working with energy audits in the ROCKWOOL Group Susanne Dyrbøl & Mette Drejstel Abstract No. 3-068-18 The ROCKWOOL Group & 1 SDGs as strategic tool Energy and insulation 2 Audits 3 Learnings The ROCKWOOL Group 45 11,000 Manufacturing Employees with facilities 61 nationalities 39 Countries with sustained presence €2,374m Turnover in 2017 3÷ © ROCKWOOL International A/S Six Group Sustainability Goals Reclaimed waste Health, safety and wellbeing CO2 emissions Our goal: Increase the number of Our goal: Reduce Lost Time Incident Our goal: Reduce CO2 emission (LTI) frequency rate and ensure zero countries where we offer recyclinG intensity from our factories fatalities annually services for our products 10% 0 15 30 10% 20% Fatalities per year reduction in LTI Countries Countries by 2022 by 2030 frequency rate by 2022 by 2030 per year Water consumption Landfill waste Energy efficiency Reduce water consumption intensity Our goal: Reduce landfill waste from Improve this in own (non-renovated) within our factories our factories building stock (kWh/m2) Note: The baseline for five of the six Group Sustainability Goals is 2015. Our safety goal baseline is revised annually. The ROCKWOOL Group & 1 SDGs as strategic tool 2 Energy and insulation Audits 3 Learnings 5÷ © ROCKWOOL International A/S More than just production…. But today we focus on production ÷ © ROCKWOOL International A/S A typical ROCKWOOL factory ÷ © ROCKWOOL International A/S 7 Sustainability Goal Execution Roadmap for Energy MonitorinG tool KPIs: C-level to shop floor on the lines SDG