November 2008

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Announcement February 22, 2019

Announcement February 22, 2019 Indxx USA Regional Banking Index will be reconstituted after the close of trading hours on February 28, 2019. Listed below are the constituents that will be added to the existing index: S.No ISIN Company Name 1 US5116561003 Lakeland Financial Corporation 2 US42234Q1022 Heartland Financial USA, Inc. 3 US3369011032 1st Source Corporation 4 US89214P1093 TowneBank 5 US4461501045 Huntington Bancshares Incorporated 6 US1637311028 Chemical Financial Corporation 7 US2298991090 Cullen/Frost Bankers, Inc. 8 US1176651099 Bryn Mawr Bank Corporation 9 US72346Q1040 Pinnacle Financial Partners, Inc. 10 US90539J1097 Union Bankshares Corporation 11 US81768T1088 ServisFirst Bancshares Inc 12 US06652K1034 BankUnited, Inc. 13 US6952631033 PacWest Bancorp 14 US9897011071 Zions Bancorporation, N.A. 15 US05945F1030 BancFirst Corporation 16 US15201P1093 CenterState Bank Corporation Listed below are the constituents that will be deleted from the existing index: S.No ISIN Company Name 1 US03076K1088 Ameris Bancorp 2 US05561Q2012 BOK Financial Corporation 3 US1011191053 Boston Private Financial Holdings, Inc. 4 US1547604090 Central Pacific Financial Corp. 5 US1972361026 Columbia Banking System, Inc. 6 US2937121059 Enterprise Financial Services Corp 7 US3198291078 First Commonwealth Financial Corporation 8 US3202091092 First Financial Bancorp. 9 US3205171057 First Horizon National Corporation 10 US52471Y1064 LegacyTexas Financial Group, Inc. 11 US7838591011 S&T Bancorp, Inc. 12 US8404411097 South State Corporation 13 US84470P1093 Southside Bancshares, Inc. 14 US9027881088 UMB Financial Corporation 15 US9197941076 Valley National Bancorp Listed below are the new index constituents that will be effective at the close of trading hours on February 28, 2019. Weights as of S.No ISIN Company Name Feb 21, 2019 1 US1491501045 Cathay General Bancorp 2.00% 2 US8984021027 Trustmark Corporation 2.00% 3 US4590441030 International Bancshares Corporation 2.00% 4 US1266001056 CVB Financial Corp. -

O'neil Elected CEO, First Financial Cleburne Morris Is Chairman In

April 9, 2012 www.bankersdigest.com Volume 140, No. 14 O’Neil Elected CEO, Morris Is Chairman in McCaskill Tapped Sabine First Financial Cleburne Mountain Home, AR Reg President, MidSouth First Financial Bankshares Inc., Mountain Home Bancshares Inc. has an- MidSouth Bank, N. A., Lafayette, LA, Abilene, TX, has announced the elec- nounced the election of Cynthia Morris has combined its West Louisiana Re- tion of Tom O’Neil as chairman of the gion with portions as CEO of subsid- board following of its East Texas iary First Finan- the retirement of Region, including cial Bank, N. A., Chairman Denny the Beaumont and Cleburne. He will Smith, who will Vidor markets, to join the existing continue to serve create the Sabine management team as member of the Region. The bank of Matt Reynolds, board of directors. has named Blake president, and Mountain Home McCaskill as the Craig Beskow, ex- O’Neil Bancshares is the Morris Sabine Region- McCaskill ecutive vice presi- parent company al President. He dent. of First National Bank & Trust, Moun- joined MidSouth in 2010 and was O’Neil has served as president of tain Home, AR; Bank of Pocahontas, previously president of the West Loui- subsidiary First Financial Bank, N. Pocahontas, AR; and Integrity First siana Region. A., Eastland, since 2009. He entered Bank, Jonesboro, AR. McCaskill has two decades of bank- banking in 1980 with the OCC and Morris, a cum laude graduate of Wil- ing experience. Before joining Mid- joined First Financial in 1998 as a se- liam Woods University, Fulton, MO, South, he worked for Capital One as nior vice president and commercial began her banking career in 1976 and a vice president for business banking lender in Abilene. -

TARP Capital Purchase Program Recipients

TARP Capital Purchase Program Recipients Date Name of Institution City State Investment Type Investment 2/6/2009 Alaska Pacific Bancshares, Inc. Juneau AK Preferred Stock w/Warrants 4,781,000 Alaska Total: 1 12/19/2008 BancTrust Financial Group, Inc. Mobile AL Preferred Stock w/Warrants $50,000,000 11/14/2008 Regions Financial Corp. Birmingham AL Preferred Stock w/Warrants $3,500,000,000 12/5/2008 Superior Bancorp Inc. Birmingham AL Preferred Stock w/Warrants $69,000,000 12/23/2008 United Bancorporation of Alabama, Inc. Atmore AL Preferred Stock w/ Warrants $10,300,000 Alabama Total: 4 12/12/2008 Bank of the Ozarks, Inc. Little Rock AR Preferred Stock w/Warrants $75,000,000 1/16/2009 Home Bancshares, Inc. Conway AR Preferred Stock w/ Warrants 50,000,000 2/ 1/23/2009 Liberty Bancshares, Inc. Jonesboro AR Preferred Stock w/ Exercised Warrants 57,500,000 2/ 1/30/2009 Rogers Bancshares, Inc. Little Rock AR Preferred Stock w/ Exercised Warrants 25,000,000 3/ 1/16/2009 Southern Bancorp, Inc. Arkadelphia AR Preferred Stock 11,000,000 Arkansas Total: 5 2/ 1/30/2009 Goldwater Bank, N.A. Scottsdale AZ Preferred Stock w/ Exercised Warrants 2,568,000 Arizona Total: 1 11/14/2008 Bank of Commerce Holdings Redding CA Preferred Stock w/Warrants $17,000,000 12/5/2008 Bank of Marin Bancorp Novato CA Preferred Stock w/Warrants $28,000,000 2/ 1/30/2009 Beach Business Bank Manhattan Beach CA Preferred Stock w/ Exercised Warrants 6,000,000 12/23/2008 Bridge Capital Holdings San Jose CA Preferred Stock w/ Warrants $23,864,000 11/14/2008 Broadway Financial Corporation -

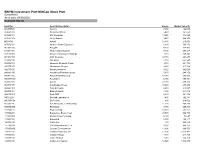

BNYM Investment Port:Midcap Stock Port (Unaudited) As of Date: 09/30/2020 Common Stocks

BNYM Investment Port:MidCap Stock Port (Unaudited) As of date: 09/30/2020 Common Stocks Identifier Security Description Shares Market Value ($) 002535300 Aaron's 7,450 422,043 00404A109 Acadia Healthcare 5,480 161,550 004498101 ACI Worldwide 13,250 346,223 00508Y102 Acuity Brands 9,470 969,255 BD845X2 Adient 12,480 216,278 00737L103 Adtalem Global Education 6,800 166,872 00766T100 AECOM 4,170 174,473 018581108 Alliance Data Systems 7,130 299,317 01973R101 Allison Transmission Holdings 7,110 249,845 00164V103 AMC Networks 10,710 264,644 023436108 Amedisys 2,760 652,547 025932104 American Financial Group 3,310 221,704 03073E105 AmerisourceBergen 2,220 215,162 042735100 Arrow Electronics 5,620 442,069 04280A100 Arrowhead Pharmaceuticals 5,670 244,150 045487105 Associated Banc-Corp 47,940 605,003 05329W102 Autonation 6,980 369,451 05368V106 Avient 23,030 609,374 053774105 Avis Budget Group 10,600 278,992 05464C101 Axon Enterprise 2,410 218,587 062540109 Bank of Hawaii 4,830 244,012 06417N103 Bank OZK 6,630 141,352 090572207 Bio-Rad Laboratories 1,480 762,881 09073M104 Bio-Techne 880 218,002 05550J101 BJs Wholesale Club Holdings 11,270 468,269 09227Q100 Blackbaud 3,750 209,363 103304101 Boyd Gaming 18,350 563,162 105368203 Brandywine Realty Trust 93,500 966,790 11120U105 Brixmor Property Group 6,300 73,647 117043109 Brunswick 8,150 480,117 12685J105 Cable One 300 565,629 127190304 CACI International, Cl. A 3,980 848,377 12769G100 Caesars Entertainment 11,890 666,553 133131102 Camden Property Trust 11,390 1,013,482 134429109 Campbell Soup 4,440 -

Digital Experiences in Banking 2019

ANALYSIS REPORT Digital Experiences in Banking 2019 Table of Contents 01 Introduction 3 About Us 02 Trends and Insights 5 Extractable is the digital strategy and experience design partner for 03 Results and Findings 7 financial services firms committed Our Approach 8 to delivering exceptional customer User Experience 10 experience. We plan, design, build, and optimize digital channels to Analytics and SEO 12 drive increased brand awareness, Visual Design and Branding 14 acquisition, and share of wallet Key Functionality 16 while reducing support costs and Content 18 churn. Our experience working Digital Marketing 20 with over 100 banks, credit unions, investment management firms, 04 Future of Digital Banking 23 retirement services providers, Digitally. Intelligently. Forward. 23 brokerages, and transaction Conclusion 23 servicers gives us rare insight into the challenges you face and how to solve for them, while generating positive ROI. EXTRACTABLE | 1 Extractable takes a deep dive 1 Home BancShares $14 B FORBES 2018 into the first 20 “Forbes 2018 2 Western Alliance Bancorp $20 B Top 100 Best Banks in America”1 3 Bank OZK $21 B 4 First Merchants $9 B BEST BANKS to analyze digital experiences 5 East West Bancorp $36 B across the industry. Find out 6 Community Bank System $11 B IN AMERICA what we learned. 7 Prosperity Bancshares $22 B 8 FCB Financial Holdings $10 B 9 First Hawaiian $21 B 10 Glacier Bancorp $10 B 11 Columbia Banking System $10 B 12 Cathay General Bancorp $16 B 13 Cullen/Frost Bankers $31 B 14 South State Bank $11 B 15 First Republic Bank $84 B 16 Bank of Hawaii $17 B 17 WesBanco $10 B 18 International Bancshares $12 B 19 Independent Bank Group $9 B 20 Hope Bancorp $14 B 1 The order of the list varies from what Forbes published originally. -

PORTFOLIO of INVESTMENTS – As of December 31, 2020 (Unaudited)

PORTFOLIO OF INVESTMENTS – as of December 31, 2020 (Unaudited) Loomis Sayles Small Cap Value Fund ________________________________Shares Description ____________________________________________________________ Value (†) Common Stocks – 98.9% of Net Assets Aerospace & Defense – 1.0% 64,870 Aerojet Rocketdyne Holdings, Inc.(a) $ 3,428,379 36,809 BWX Technologies, Inc. ______________2,218,847 ______________5,647,226 Auto Components – 3.2% 134,171 Cooper Tire & Rubber Co. 5,433,925 288,336 Dana, Inc. 5,628,319 20,928 Fox Factory Holding Corp.(a) 2,212,299 38,655 LCI Industries ______________5,012,780 ______________18,287,323 Banks – 13.5% 158,448 Ameris Bancorp 6,032,115 185,530 Atlantic Union Bankshares Corp. 6,111,358 172,148 BancorpSouth Bank 4,723,741 147,547 Bryn Mawr Bank Corp. 4,514,200 215,661 CVB Financial Corp. 4,205,390 271,568 Home BancShares, Inc. 5,290,145 234,144 OceanFirst Financial Corp. 4,362,103 95,010 Pinnacle Financial Partners, Inc. 6,118,644 132,588 Popular, Inc. 7,467,356 76,931 Prosperity Bancshares, Inc. 5,335,934 62,945 South State Corp. 4,550,924 133,304 TCF Financial Corp. 4,934,914 146,089 Triumph Bancorp, Inc.(a) 7,092,621 113,313 Wintrust Financial Corp. ______________6,922,291 ______________77,661,736 Beverages – 1.0% 364,847 Primo Water Corp. ______________5,720,801 Biotechnology – 1.6% 45,738 Emergent BioSolutions, Inc.(a) 4,098,125 31,964 United Therapeutics Corp.(a) ______________4,851,815 ______________8,949,940 Building Products – 2.6% 45,224 American Woodmark Corp.(a) 4,244,273 52,093 Armstrong World Industries, Inc. -

Usef-I Q2 2021

Units Cost Market Value U.S. EQUITY FUND-I U.S. Equities 88.35% Domestic Common Stocks 10X GENOMICS INC 5,585 868,056 1,093,655 1ST SOURCE CORP 249 9,322 11,569 2U INC 301 10,632 12,543 3D SYSTEMS CORP 128 1,079 5,116 3M CO 11,516 2,040,779 2,287,423 A O SMITH CORP 6,897 407,294 496,998 AARON'S CO INC/THE 472 8,022 15,099 ABBOTT LABORATORIES 24,799 2,007,619 2,874,948 ABBVIE INC 17,604 1,588,697 1,982,915 ABERCROMBIE & FITCH CO 1,021 19,690 47,405 ABIOMED INC 9,158 2,800,138 2,858,303 ABM INDUSTRIES INC 1,126 40,076 49,938 ACACIA RESEARCH CORP 1,223 7,498 8,267 ACADEMY SPORTS & OUTDOORS INC 1,036 35,982 42,725 ACADIA HEALTHCARE CO INC 2,181 67,154 136,858 ACADIA REALTY TRUST 1,390 24,572 30,524 ACCO BRANDS CORP 1,709 11,329 14,749 ACI WORLDWIDE INC 6,138 169,838 227,965 ACTIVISION BLIZZARD INC 13,175 839,968 1,257,422 ACUITY BRANDS INC 1,404 132,535 262,590 ACUSHNET HOLDINGS CORP 466 15,677 23,020 ADAPTHEALTH CORP 1,320 39,475 36,181 ADAPTIVE BIOTECHNOLOGIES CORP 18,687 644,897 763,551 ADDUS HOMECARE CORP 148 13,034 12,912 ADOBE INC 5,047 1,447,216 2,955,725 ADT INC 3,049 22,268 32,899 ADTALEM GLOBAL EDUCATION INC 846 31,161 30,151 ADTRAN INC 892 10,257 18,420 ADVANCE AUTO PARTS INC 216 34,544 44,310 ADVANCED DRAINAGE SYSTEMS INC 12,295 298,154 1,433,228 ADVANCED MICRO DEVICES INC 14,280 895,664 1,341,320 ADVANSIX INC 674 15,459 20,126 ADVANTAGE SOLUTIONS INC 1,279 14,497 13,800 ADVERUM BIOTECHNOLOGIES INC 1,840 7,030 6,440 AECOM 5,145 227,453 325,781 AEGLEA BIOTHERAPEUTICS INC 287 1,770 1,998 AEMETIS INC 498 6,023 5,563 AERSALE CORP -

Stephens Bank Research Team

Stephens Bank Research Team – Upcoming Investor Events August 22, 2018 Non-Deal Roadshow 2018 Stephens Bank CEO Forum August, 2018 Company Name (Ticker) Company Name (Ticker) Company Name Day Location Allegiance Bancshares, Inc. (ABTX) LegacyTexas Financial Group (LTXB) BancorpSouth Bank (BXS) 22 Boston Ameris Bancorp (ABCB) Merchants Bancorp (MBIN) Banner Corp. (BANR) 28-29 New York, Boston Bank OZK, Inc. (OZK) Midland States Bancorp, Inc. (MSBI) September, 2018 BofI Holding, Inc. (BOFI) National Bank Holdings (NBHC) Company Name Day Location BOK Financial Corporation (BOKF) National Commerce Corp. (NCOM) F.N.B. Corporation (FNB) 11-12 Dallas, Houston Business First Bancshares (BFST) Old Line Bancshares (OLBK) Sterling Bancorp (STL) 19 Boston Byline Bancorp (BY) Old National Bancorp (ONB) November, 2018 Cadence Bancorporation (CADE) Origin Bancorp, Inc. (OBNK) Company Name Day Location CBTX, Inc. (CBTX) Pacific Premier Bancorp, Inc. (PPBI) Carolina Financial Corp. (CARO) 1-2 Kansas City, St. Louis, Dallas CenterState Banks (CSFL) PacWest Bancorp (PACW) Analyst Marketing Chemical Financial (CHFC) Pinnacle Financial (PNFP) August, 2018 City Holding Co (CHCO) Preferred Bank (PFBC) Analyst(s) Day Location County Bancorp (ICBK) Prosperity Bancshares (PB) Terry McEvoy / Austin Nicholas 22-24 New York Stephens 8th Annual Bank Eagle Bancorp (EGBN) RBB Bancorp, Inc. (RBB) Tyler Stafford, CFA 27 New York CEO Forum will take Equity Bancshares (EQBK) Renasant Corp (RNST) th Matt Olney, CFA / Austin Nicholas 28 San Francisco place September 24 – FB Financial Corporation (FBK) Simmons First National Corp (SFNC) 26th in Little Rock – See September, 2018 here for further details. Fidelity Southern Corporation (LION) SmartFinancial (SMBK) Analyst(s) Day Location First Bancshares (FBMS) South State Corporation (SSB) Tyler Stafford, CFA / Matt Olney, CFA 4-5 Kansas City, St. -

NASDAQ Stock Market LLC (“Nasdaq Exchange”), a Subsidiary of the Nasdaq Stock Market, Inc

July 31, 2006 Nancy M. Morris, Esq. Secretary US Securities and Exchange Commission 100 F Street, NE Washington, DC 20549 RE: Request for Relief from § 12 of the Securities Exchange Act of 1934 Dear Ms. Morris: On January 13, 2006, the Securities and Exchange Commission (“SEC” or “Commission”) approved the application of The NASDAQ Stock Market LLC (“Nasdaq Exchange”), a subsidiary of The Nasdaq Stock Market, Inc. (“Nasdaq”), to register under Section 6 of the Securities Exchange Act of 1934 (“Act” or “Exchange Act”) as a national securities exchange.1 Nasdaq’s transition of its listing and trading activities to the Nasdaq Exchange will further Congress’s instruction to promote “fair competition . between exchange markets.”2 Absent the relief requested herein, however, Nasdaq’s transition to a national securities exchange would require approximately 3,200 Nasdaq Global Market3 and Capital Market issuers with securities registered pursuant to the Act, or exempt from registration under Section 12(g) of the Act,4 to file registration statements5 to register those securities under Section 12(b) of the Act.6 1 Securities Exchange Act Release No. 53128 (January 13, 2006), 71 FR 3550 (January 23, 2006) (the “Exchange Approval Order”). 2 Exchange Act Section 11A(a)(1)(C)(ii). 3 Effective July 1, 2006, Nasdaq renamed the Nasdaq National Market as the Nasdaq Global Market and created a new segment within the Global Market called the Global Select Market. References to the Nasdaq Global Market include those securities listed on the Nasdaq Global Market and the Nasdaq Global Select Market. See Securities Exchange Act Release No. -

Banks Ultrasector Profund :: Schedule of Portfolio Investments :: April 30, 2020 (Unaudited)

Banks UltraSector ProFund :: Schedule of Portfolio Investments :: April 30, 2020 (unaudited) Shares Value Common Stocks (75.2%) Associated Banc-Corp. (Banks) 848 $ 11,991 BancorpSouth Bank (Banks) 509 11,142 Bank of America Corp. (Banks) 36,462 876,910 Bank of Hawaii Corp. (Banks) 217 14,795 Bank OZK (Banks) 643 14,545 BankUnited, Inc. (Banks) 506 10,024 BOK Financial Corp. (Banks) 172 8,908 Capitol Federal Financial, Inc. (Thrifts & Mortgage Finance) 749 8,981 Cathay General Bancorp (Banks) 399 11,140 CIT Group, Inc. (Banks) 506 9,604 Citigroup, Inc. (Banks) 11,598 563,199 Citizens Financial Group, Inc. (Banks) 2,312 51,766 Comerica, Inc. (Banks) 764 26,633 Commerce Bancshares, Inc. (Banks) 550 33,655 Cullen/Frost Bankers, Inc. (Banks) 304 21,845 East West Bancorp, Inc. (Banks) 771 27,039 F.N.B. Corp. (Banks) 1,725 13,955 Fifth Third Bancorp (Banks) 3,771 70,480 First Citizens BancShares, Inc. - Class A (Banks) 47 17,954 First Financial Bankshares, Inc. (Banks) 717 19,968 First Hawaiian, Inc. (Banks) 693 12,190 First Horizon National Corp. (Banks) 1,652 15,004 First Republic Bank (Banks) 898 93,652 Fulton Financial Corp. (Banks) 875 10,229 Glacier Bancorp, Inc. (Banks) 454 17,288 Hancock Whitney Corp. (Banks) 463 9,681 Home BancShares, Inc. (Banks) 822 12,601 Huntington Bancshares, Inc. (Banks) 5,486 50,691 IBERIABANK Corp. (Banks) 276 11,443 International Bancshares Corp. (Banks) 305 8,842 Investors Bancorp, Inc. (Banks) 1,183 11,014 JPMorgan Chase & Co. (Banks) 16,666 1,595,935 KeyCorp (Banks) 5,235 60,988 M&T Bank Corp. -

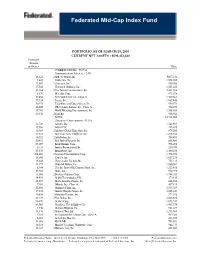

Federated Mid-Cap Index Fund

Federated Mid-Cap Index Fund PORTFOLIO AS OF MARCH 29, 2019 CURRENT NET ASSETS - $593,452,840 Principal Amount or Shares Value COMMON STOCKS - 95.9%1 Communication Services - 2.5% 14,222 2 AMC Networks, Inc. $807,241 1,623 Cable One, Inc. 1,592,780 23,507 2 Cars.com, Inc. 535,960 37,540 Cinemark Holdings, Inc. 1,501,225 51,364 2 Live Nation Entertainment, Inc. 3,263,668 8,570 Meredith Corp. 473,578 39,868 New York Times Co., Class A 1,309,664 77,124 Tegna, Inc. 1,087,448 30,933 Telephone and Data System, Inc. 950,571 16,605 Wiley (John) & Sons, Inc., Class A 734,273 17,961 World Wrestling Entertainment, Inc. 1,558,655 26,636 2 Yelp, Inc. 918,942 TOTAL 14,734,005 Consumer Discretionary - 11.5% 21,728 Aaron's, Inc. 1,142,893 33,566 Adient PLC 435,015 18,981 2 Adtalem Global Education, Inc. 879,200 57,672 American Eagle Outfitters, Inc. 1,278,588 10,932 2 AutoNation, Inc. 390,491 50,411 Bed Bath & Beyond, Inc. 856,483 29,097 Boyd Gaming Corp. 796,094 6,331 Brinker International, Inc. 280,970 29,570 Brunswick Corp. 1,488,258 204,681 2 Caesars Entertainment Corp. 1,778,678 16,046 Carter's, Inc. 1,617,276 15,358 Cheesecake Factory, Inc. 751,313 11,971 Churchill Downs, Inc. 1,080,502 8,184 Cracker Barrel Old Country Store, Inc. 1,322,616 51,764 Dana, Inc. 918,293 11,866 2 Deckers Outdoor Corp. -

Ftse Rafi Us 1000

2 FTSE Russell Publications 19 August 2021 FTSE RAFI US 1000 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3M Company 0.37 UNITED Allison Transmission Holdings 0.02 UNITED Apartment Income REIT Corp 0.02 UNITED STATES STATES STATES Abbott Laboratories 0.26 UNITED Allstate Corp 0.26 UNITED Apollo Commercial Real Estate Finance 0.02 UNITED STATES STATES STATES AbbVie Inc 0.46 UNITED Ally Financial 0.13 UNITED Apollo Global Management Inc 0.02 UNITED STATES STATES STATES Abercrombie & Fitch A 0.02 UNITED Alphabet Class A 0.73 UNITED Apple Hospitality REIT 0.03 UNITED STATES STATES STATES ABM Industries Inc 0.02 UNITED Alphabet Class C 0.73 UNITED Apple Inc. 2.23 UNITED STATES STATES STATES Acadia Healthcare 0.02 UNITED Altice USA 0.05 UNITED Applied Industrial Technology 0.01 UNITED STATES STATES STATES Accenture Cl A 0.29 UNITED Altria Group 0.45 UNITED Applied Materials 0.14 UNITED STATES STATES STATES Activision Blizzard 0.08 UNITED Amazon.Com 0.86 UNITED Aptargroup 0.02 UNITED STATES STATES STATES Acuity Brands Inc 0.03 UNITED AMC Networks 0.02 UNITED Aptiv PLC 0.07 UNITED STATES STATES STATES Adient plc 0.04 UNITED Amdocs 0.03 UNITED Aramark 0.05 UNITED STATES STATES STATES Adobe 0.11 UNITED AMERCO 0.02 UNITED Arch Capital Gp 0.07 UNITED STATES STATES STATES Advance Auto Parts 0.04 UNITED Ameren Corp 0.09 UNITED Archer Daniels Midland 0.17 UNITED STATES STATES STATES Advanced Micro Dev 0.03 UNITED American Airlines Group 0.04 UNITED Arconic Corporation 0.04 UNITED STATES STATES STATES AECOM 0.07 UNITED American Axle & MFG Holdings 0.02 UNITED Arista Networks 0.02 UNITED STATES STATES STATES AerCap Holdings N.V.