Food Security Conditions Remain Generally Favorable Except In

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

51 Younoussi Tillabéri 2

1 LASDEL Laboratoire d’études et recherches sur les dynamiques sociales et le développement local _________ BP 12901, Niamey, Niger – tél. (227) 72 37 80 BP 1383, Parakou, Bénin – tél. (229) 61 16 58 Observatoire de la décentralisation au Niger (enquête de suivi 2004-2005) Les pouvoirs locaux dans la commune de Tillabéri (2) Younoussi Issa Assistants de recherche : Abdoutan Harouna, Oumarou Issaka Etudes et Travaux n° 51 Financement : Kfw (FICOD) Janvier 07 2 Table des matières INTRODUCTION ___________________________________________________________________ 4 Méthodologie de la recherche ____________________________________________ 4 COMPLEMENTS DES ENQUETES DE REFERENCE ___________________________________________ 6 L’Etat local __________________________________________________________ 6 L’environnement associatif ____________________________________________ 10 Les partis politiques __________________________________________________ 16 Les projets et ONG ___________________________________________________ 19 DES CAMPAGNES ELECTORALES A LA MISE EN PLACE DU CONSEIL COMMUNAL _________________ 21 La mise en place de l’exécutif communal et profil des membres du conseil _______ 23 LE CONSEIL MUNICIPAL ET SON FONCTIONNEMENT ______________________________________ 26 La composition du conseil communal ____________________________________ 26 Le fonctionnement du conseil ___________________________________________ 27 La mairie ___________________________________________________________ 31 Les ressources financières de la commune _________________________________ -

32 Mohamadou Tchinta

1 LASDEL Laboratoire d’études et recherches sur les dynamiques sociales et le développement local _________ BP 12901, Niamey, Niger – tél. (227) 72 37 80 BP 1383, Parakou, Bénin – tél. (229) 61 16 58 Observatoire de la décentralisation au Niger (enquête de référence 2004) Les pouvoirs locaux dans la commune de Tchintabaraden Abdoulaye Mohamadou Enquêteurs : Afélane Alfarouk et Ahmoudou Rhissa février 05 Etudes et Travaux n° 32 Financement FICOD (KfW) 2 Sommaire Introduction 3 Les Kel Dinnig : de la confédération aux communes 3 Objectifs de l’étude et méthodologie 4 1. Le pouvoir local et ses acteurs 6 1.1. Histoire administrative de l’arrondissement et naissance d’un centre urbain 6 1.2. Les acteurs de l’arène politique locale 7 2. Le découpage de l’arrondissement de Tchintabaraden 19 2.1. Logiques territoriale et logiques sociales 19 2.2. Le choix des bureaux de vote 22 2.3. Les stratégies des partis politiques pour le choix des conseillers 23 2.4. La décentralisation vue par les acteurs 23 3. L’organisation actuelle des finances locales 25 3.1. Les projets de développement 25 3. 2. Le budget de l’arrondissement 26 Conclusion 33 3 Introduction Les Kel Dinnig : de la confédération aux communes L’arrondisssement de Tchintabaraden correspondait avant la création de celui d’Abalak en 1992 à l’espace géographique et social des Touareg Iwillimenden ou Kel Dinnig. Après la révolte de Kaocen en 1916-1917 et son anéantissement par les troupes coloniales françaises, l’aménokalat des Iwilimenden fut disloqué et réparti en plusieurs groupements. Cette technique de diviser pour mieux régner, largement utilisée par l’administration coloniale, constitue le point de départ du découpage administratif pour les populations de cette région. -

Final Narrative Report

01/01/2019-31/12/2019 Agro-pastoral mediation in the Sahel region NARRATIVE REPORT 1 January to 31 December 2019 Centre for Humanitarian Dialogue 114 rue de Lausanne CH 1202 Geneva Tél : +41 22 908 11 30 www.hdcentre.org June 2020 Page 1 out of 8 01/01/2019-31/12/2019 1. Evaluation of the implementation of the activities of the action and of the results In the Sahel, agropastoral activities are highly dependent on climate variability. As a result, agropastoralists are constantly looking for strategies to enable them to effectively adapt their production systems to climate change. In recent years, politico-military crises and the occupation of certain areas by violent extremist groups have greatly disrupted traditional animal movements and caused a crisis of confidence between pastoral and agro-pastoral communities sharing the same geographical spaces and resources and have resulted in an increase in violence By the end of 2019, the Centre for Humanitarian Dialogue (HD) was supporting a network of 961 community mediators spread across 58 border communities in Burkina Faso, Chad, Mali, Mauritania and Niger in their efforts to resolve conflicts over access to natural resources. This network of mediators resolved 105 micro-conflicts and facilitated the return of 229 head of cattle, two plots of land and two motorcycles to their owners. This work reflects the project's objective to prevent the transformation of micro-conflicts into inter-community conflicts that could be triggered by armed groups operating in the Sahel region. Denmark and the European Union also fund the agro-pastoral mediation programme implemented by HD with the support of the Netherlands. -

NIGER - DIFFA : Les Incidents Liés Au Groupe Boko Haram* (1 Janvier Au 31 Août 2018)

NIGER - DIFFA : Les incidents liés au groupe Boko Haram* (1 janvier au 31 août 2018) De janvier à août 2018, la situation sécuritaire dans la région de Diffa a été marquée par une augmentation des exactions des éléments du groupe armé non étatique Boko Haram (BH) et une baisse des victimes civiles liées à ces incidents comparativement à la même période l’année dernière (2017). Les mois de janvier et août 2018 ont enregistré le plus d’incidents (47/94 soit 50%). Les communes de Gueskerou, Bosso, Maine Soroa et Chetimari sont les plus touchées par les attaques du groupe BH (73/94 incidents soit 78%). Des attaques terroristes majeures ont été rapportées dans les localités bordant les berges de la Komadougou et les localités proches des îles du Lac Tchad. Le 4 juin, 3 kamikazes ont fait exploser leurs charges dans un quartier de la ville de Diffa tuant 6 civils. Trois (3) bases militaires ont été attaquées par les éléments du groupe BH respectivement les 17 janvier, 23 janvier et 1 juillet dans les localités de Toumour, Chétima Wangou (Chetimari) et Bilabrin (N’Guigmi) faisant des victimes dans les deux camps. Ces incidents et d’autres de nature criminelle (enlèvements, extorsions et menaces) sont à l’origine de mouvements de populations entre les différents sites et/ou villages. Bilan des incidents Les incidents par commune en 2018 Les incidents par mois 94 incidents de janv. à août 2018 Pertes en vies 38 humaines 60 incidents de janv. à août 2017 (janv. à août 2018) 30 24 23 Pertes en vies 25 56 humaines 20 15 15 (2017) 10 0 5 0 1-5 Enlèvements Ngourti Jui Jul Avr Oct Déc. -

Rapport D'analyse Mensuelle Des Donnees Du Monitoring

RAPPORT D’ANALYSE MENSUELLE DES DONNEES DU MONITORING DE PROTECTION septembre 2018 Tillabéri, Niger Discussion de groupe avec les femmes déplacées internes sur le site de Sarayé (commune Abala) 1 # TOTAL DES PDI DANS LA RE- I. APERCU DE L’ENVIRONNEMENT SECURITAIRE ET GION DE TILLABERI DE PROTECTION DANS LA REGION DE TILLABERI La situation sécuritaire dans la région de Tillaberi reste volatile et im- prévisible. Au cours du mois de septembre 2018, il a été signalé une re- 31,703 crudescence des attaques des campements à la frontière avec le Mali ayant un lien probable avec des affiliations ethniques avec les differents groupes armés non étatiques dans le cercle de Menaka au nord du Mali. Suite aux multiples opérations militaires en cours dans la zone, les élé- ments des groupes armés non étatiques connaitraient une débandade et # TOTAL DES PDI PAR DEPARTE- seraient disséminés au sein de la population dans l’espoir de changer de MENT mode de vie. Certains se convertissent en commerçant en utilisant les butins volés à des éleveurs. 15,918 Dans la même période, il a été observé une détérioration de la situation 13,920 sécuritaire le long de la frontière avec le Burkina, en particulier dans la région de l’est et du nord-est du Burkina Faso avec une série d’enlève- ments, d’attaques contre les populations civiles et les FDS. Ces attaques enregistrées le long de la frontière avec le Niger (partie est et sahel) seraient attribuées à des militants affiliés à l’organisation « Etat islamique dans le Grand Sahara » (EIGS), initialement active dans le nord du Mali (régions de Gao et Menaka). -

Emergency Plan of Action (Epoa) Niger: Complex Emergency

Page | 1 Emergency Plan of Action (EPoA) Niger: Complex Emergency Emergency MDRNE021 Glide n°: OT-2014-000126-NER Appeal / n° For Emergency 13 April Expected timeframe: 24 months (extended 12 months) Appeal: Date of 2018 launch: Expected end date: 30 April 2020 Category allocated to the of the disaster or crisis: Orange Emergency Appeal Funding Requirements: Revised to CHF 2,205,000 from CHF 1,680,731 DREF allocated: CHF 168,073 Total number of 461,323 Number of people to be 50,000 people revised from 43,113 people affected: assisted: if the total number of people people targeted is revised, Provinces Three Provinces/Regions targeted: One affected: Project manager: Pierre Danladi, overall responsible for planning, National Society contact: ISSA implementing, reporting and compliances. Mamane, Secretary General Host National Society presence (n° of volunteers, staff, branches): Diffa branch of the Niger Red Cross Society (NRCS) with 800 volunteers and eight staff Red Cross Red Crescent Movement partners actively involved in the operation: International Committee of the Red Cross (ICRC), Luxembourg Red Cross and International Federation of Red Cross and Red Crescent Societies (IFRC) Other partner organizations actively involved in the operation: UNHCR, UNICEF, WFP, WHO, OCHA, CARE, Save the Children, MSF Spain, OXFAM, World Vision, ACTED, UNFPA, DRC, Plan International, ACF, ONG KARKARA, APBE, ONG DIKO, Ministry of Humanitarian Action and Disaster Management, Ministry of Interior A. Situation analysis Description of the crisis The Diffa region of Niger continues to experience violence, inter-community conflicts, abduction and population movement as a result of armed groups activities. The current security situation remains extremely volatile and attacks by armed groups and military operations have kept people on the move, seeking safety and hoping for peace. -

In Mali, Burkina Faso and Niger Situation Overview : Niger – Tillabéri and Tahoua Regions | March 2020

Humanitarian situation monitoring (HSM) in Mali, Burkina Faso and Niger Situation overview : Niger – Tillabéri and Tahoua regions | March 2020 Context Since the outbreak of violence in Mali in 2012, the border area between Niger, Mali and Burkina Faso has been characterized by a climate of insecurity due to the presence of armed groups, crime and rising tensions between communities1. The security situation in Niger has deteriorated sharply since 2018 and has caused the internal displacement of 159,028 people in the Tillabéri and Tahoua regions as of March 20202. In addition, the provision of humanitarian assistance is subject to multiple constraints resulting in limitations to access affected populations due to security, geographic and climatic factors, as well as to measures taken as part of the state of emergency covering parts of the Tillabéri and Tahoua regions1. Limited humanitarian access is one of the factors at the origin of important information gaps about the scope, nature and severity of needs. To fill these information gaps, REACH has been implementing a monitoring of the humanitarian situation, financed by the U.S. Office of Foreign Disaster Assistance (OFDA) since January 2020, following a pilot phase in November 20193. This situation overview presents the main results for data collected in March 2020 in the Tillabéri and Tahoua regions and analyzes the development of main indicators in the Tillabéri region between November 2019 and March 20204. Methodology This assessment adopts a so-called “Area of knowledge” methodology. The aim of this methodology is to collect, analyze and share up-to-date information regarding multi-sectoral humanitarian needs in the region, including in areas that are difficult to access. -

Dynamiques Des Ressources Environnementales Et

Dynamiques des ressources environnementales et mutations des systèmes agro-sylvo-pastoraux en milieu tropical semi aride : le cas de la vallée d’Arewa ( Niger central) François Fauquet To cite this version: François Fauquet. Dynamiques des ressources environnementales et mutations des systèmes agro- sylvo-pastoraux en milieu tropical semi aride : le cas de la vallée d’Arewa ( Niger central). Géographie. Université Joseph-Fourier - Grenoble I, 2005. Français. tel-00010859 HAL Id: tel-00010859 https://tel.archives-ouvertes.fr/tel-00010859 Submitted on 3 Nov 2005 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. RESUME On évoque souvent, à propos de l’agriculture sahélienne, les caprices de la pluviométrie notamment les sécheresses catastrophiques de 1973 et de 1984. Pour autant, en dehors de ces épisodes de crises exceptionnelles et de leurs conséquences dramatiques, les savoir-faire paysans et le dynamisme des communautés rurales, ont permis de surmonter bien des difficultés. Les solidarités entre générations, la cohésion des familles, une économie populaire informelle, sont autant de parades à l’incertitude et aux mauvaises conjonctures. Dans la vallée d’Arewa, le doublement de la population ces vingt cinq dernières années a été accompagné d’un formidable mouvement d’extension des cultures, avec pour corollaire, une saturation des terres cultivables et une diminution sensible de la couverture végétale. -

RAPPORT ANNUEL DE MONITORING DE PROTECTION 2018 Tillabéri, Niger

RAPPORT ANNUEL DE MONITORING DE PROTECTION 2018 Tillabéri, Niger Discussions de groupe avec les déplacés internes le 28 août à Ayorou - Tillabéri 1 # TOTAL DES PDIs DANS LA RE- I. APERCU DE L’ENVIRONNEMENT SECURITAIRE ET GION DE TILLABERI DE PROTECTION DANS LA REGION DE TILLABERI La région de Tillabéri a connu une instabilité très accentuée durant l’année 2018, du fait de l’insécurité dans les localités des différentes communes frontalières avec le Mali et le Burkina Faso, en proie aux 35,866 attaques des éléments des groupes armés non étatique. A cela s’ajoute la porosité de la frontière nigérienne avec le Mali et l’insuffisance de la couverture des zones par les forces de défense et de sécurité. Cette insécurité a eu comme conséquences collatérales des incidents de protection et des mouvements de populations avec un accroissement # TOTAL DES PDIs PAR DEPARTE- des besoins multisectoriels. Ainsi, au 31 décembre, 419 incidents de MENT protection rapportés soit une moyenne de 35 incidents par mois ainsi que 35,866 personnes déplacées internes enregistrées dans la région 19.030 de Tillaberi. Les communes d’Inates, d’Abala, d’Anzourou et d’Ayorou 14.971 restent les plus touchées au cours de l’année avec plus de 300 incidents de protection et plus de 34 000 PDI dans ces départements. Les interventions militaires de l’opération conjointe Barkhane-G5 Sahel et l’opération de l’armée nigérienne (Dongo) dans le nord d’ Ouallam et l’opération Saki 2 dans les communes de Torodi et Makalondi menées en Octobre dernier ont entrainé la dispersion d’une 665 1,200 grande partie des groupes armés qui se seraient déplacés vers les zones d’ Inates, de Tilloa, au nord de Banibangou et d’Abala, dans la Région de Banibangou Tillaberi et vers la forêt de Kodjoga Beli située à cheval entre le Niger et le Ouallam Ayorou Abala Burkina-Faso. -

Republique Du Niger Region De Diffa Direction Regionale De L'etat Civil Et Des Refugies

REPUBLIQUE DU NIGER REGION DE DIFFA DIRECTION REGIONALE DE L'ETAT CIVIL ET DES REFUGIES Situtation des refugiés et retournés mise à jour 24/11/2015 N° Site RGP/H 2012 Menages Personnes Refugiés Retournés 1 Diffa festibal 508 3 229 1 619 1 610 2 Diffa Affounori 187 1 040 695 345 3 Diffa Administratif 31 173 162 11 4 Diffa Koura 604 3 483 2 442 1 041 5 Diffa Château 554 3 956 2 658 1 298 6 Diffa Sabon Carré 684 5 902 3 661 2 241 7 Adjimeri 419 1 691 1 127 564 8 Bagara 67 478 159 319 9 Grema Artori 99 436 317 119 10 Boulangouri 82 462 395 67 11 Lada 149 703 604 99 12 Guirtia 20 112 84 28 13 Ngueldagoumé 50 382 0 382 14 Boulangou Yakou 31 195 158 37 15 Kayawa 97 507 269 238 16 Koula koura 256 554 332 222 17 Madou Kaouri 61 912 585 327 18 Ligaridi 107 629 337 292 19 Dorikoulo 43 306 158 148 Total Diffa 159 722 4049 25 150 15 762 9 388 20 Mainé Boudji Kolomi 156 1 865 1695 670 21 Mainé Abdouri 25 182 195 109 22 Mainé Djambourou 112 1 574 1049 525 23 Mainé Katiellari 3 16 0 16 24 Mainé Dekouram 1 11 0 11 25 Mainé Angoual Yamma 295 2 066 1 113 953 26 Mainé Château 222 2 824 1 777 1 047 27 Mainé Yabal 16 87 76 11 28 Mainé Alaouri 36 301 92 209 29 Mainé Kaoumaram 26 201 93 108 30 Mainé Goussougourniram 23 136 0 136 31 Mainé Nguibia 19 84 13 71 32 Mainé Gadori 97 559 434 125 33 Mainé Abbasari 57 692 594 98 34 Mainé Kilwadji 20 135 61 74 35 Mainé Baredi 3 28 9 19 36 Mainé Ambouram Ali 174 864 714 150 37 Mainé Issari Bagara 22 129 0 129 38 Mainé Tam 107 957 291 666 39 Mainé Kayetawa 23 120 16 104 40 Cheri 30 140 48 92 41 Ambouram 38 198 68 130 42 -

UNHCR Niger Operation UNHCR Database

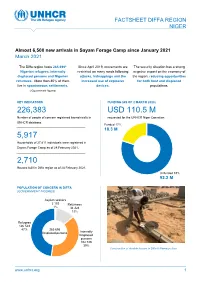

FACTSHEET DIFFA REGION NIGER Almost 6,500 new arrivals in Sayam Forage Camp since January 2021 March 2021 NNNovember The Diffa region hosts 265,696* Since April 2019, movements are The security situation has a strong Nigerian refugees, internally restricted on many roads following negative impact on the economy of displaced persons and Nigerien attacks, kidnappings and the the region, reducing opportunities returnees. More than 80% of them increased use of explosive for both host and displaced live in spontaneous settlements. devices. populations. (*Government figures) KEY INDICATORS FUNDING (AS OF 2 MARCH 2020) 226,383 USD 110.5 M Number of people of concern registered biometrically in requested for the UNHCR Niger Operation UNHCR database. Funded 17% 18.3 M 5,917 Households of 27,811 individuals were registered in Sayam Forage Camp as of 28 February 2021. 2,710 Houses built in Diffa region as of 28 February 2021. Unfunded 83% 92.2 M the UNHCR Niger Operation POPULATION OF CONCERN IN DIFFA (GOVERNMENT FIGURES) Asylum seekers 2 103 Returnees 1% 34 324 13% Refugees 126 543 47% 265 696 Displaced persons Internally Displaced persons 102 726 39% Construction of durable houses in Diffa © Ramatou Issa www.unhcr.org 1 OPERATIONAL UPDATE > Niger - Diffa / March 2021 Operation Strategy The key pillars of the UNHCR strategy for the Diffa region are: ■ Ensure institutional resilience through capacity development and support to the authorities (locally elected and administrative authorities) in the framework of the Niger decentralisation process. ■ Strengthen the out of camp policy around the urbanisation program through sustainable interventions and dynamic partnerships including with the World Bank. -

2.3.2 Niger Border Crossing of Torodi

2.3.2 Niger Border Crossing of Torodi Overview Daily Capacity Customs Clearance Other Relevant Information Overview The crossing at Torodi is set up the same way as the one at Gaya and share the same challenges. Torodi hosts a Customs Office, the CNUT, Soniloga and representatives from the Police Sanitaire that are charged with controlling incoming goods. The processes normally run smoothly and can be expected to be completed within two working days. Delays can arise due to problems with internet connection, and the crossing can in period be congested. A perpetual challenge is the ratio of trucks with Nigerien registration that is enforced by the CNUT and transporters union. The rule is that two thirds (2/3) of trucks for any combined cargo should be registered in Niger. However, there is often not enough Nigerien trucks available at the ports to clear the cargo and Togolese trucks are generally cheaper. Thus the rule is often violated which can lead to problems when crossing. Border Crossing Location and Contact Name of Border Crossing Kantchari – Torodi Province or District Kantchari Department (Benin) / Say Department (Niger) Nearest Town or City with Distance from Border Crossing Torodi 46.4km Kantchari 33.4km Latitude 012.738708 Longitude 001.633797 Managing Authority / Agency Niger Customs Contact Person Commandant Amaber (+227 96 00 70 00) Travel Times Nearest International Airport Diori Hamani International Airport (Niamey) Distance in km: 116km Truck Travel Time: 1 day Car Travel time: 1h43 Nearest Port Port Autonome de Lomé 970km Truck Travel Time: 14 days Car Travel time: 14h14 Nearest location with functioning wholesale markets, or with significant manufacturing or Niamey production capacity 109km Truck Travel Time: 1 day Car Travel time: 1h39 Other Information Fuel stations available en route.