Housing Research

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Water Bus Loch Lomond 2013

Cabs – 01877 382587. 01877 – Cabs £56.00 £40.00 Family Contact J. Morgan Taxis – 01877 330496 and Crescent Crescent and 330496 01877 – Taxis Morgan J. Contact £14.00 £10.00 under & 16 Children allander C and Pier rossachs T . between available is £18.00 £13.00 Adult berfoyle A and tronachlachar S . In the Trossachs it it Trossachs the In . ay D Full hours CES U I 3 R P to p Inversnaid, Inversnaid, between available is service the or call us 01389 756251 01389 us call or direct regular bus service. In the Strathard area area Strathard the In service. bus regular direct www.canyouexperience.com/canoe_hire.php Strathard and Trossachs areas that have no no have that areas Trossachs and Strathard from hired be can canoes and boats Bicycles, This service is provided by Stirling Council for for Council Stirling by provided is service This OCH LL A B AT RE I H E L C Y C BI (has to be booked 24 hours in advance) in hours 24 booked be to (has ORT P TRANS E IV ONS P RES DEMAND £8.00 £6.00 under & 16 Children £18.00 £12.00 Adult next bus times. bus next ay D Full hours CES U I 4 R P to p txt2traveline for service SMS use also can You 01877 376366. 01877 m.trafficscotland.org websites. and cannot be accommodated. be cannot www.katrinewheelz.co.uk calling by or at mobile.travelinescotland.com mobile-friendly due to Health & Safety reasons, electric wheelchairs wheelchairs electric reasons, Safety & Health to due Cycle hire information and prices can be obtained obtained be can prices and information hire Cycle access public transport and traffic info on the the on info traffic and transport public access • weekend break weekend A discuss your particular requirements. -

Weekly Planning Schedule

Weekly Planning Schedule Week Commencing: 14 June 2021 Week Number: 24 CONTENTS 1 Valid Planning Applications Received 2 Delegated Officer Decisions 3 Committee Decisions 4 DPEA Appeal Decisions 5 Local Review Body (LRB) Appeal Decisions 6 Enforcement Matters 7 Land Reform (Scotland) Act Section 11 Access Exemption Applications 8 Other Planning Issues 9 Byelaw Exemption Applications 10 Byelaw Authorisation Applications In light of ongoing Covid-19 restrictions, we have continued to adapt how we deliver our planning service while our staff are still working remotely. Please see our planning services webpage for full details (https://www.lochlomond-trossachs.org/planning/coronavirus-covid-19-planning-services/) and follow @ourlivepark for future updates. Our offices remain closed to the public. All staff are continuing to work from home, with restricted access to some of our systems at times. In terms of phone calls, we would ask that you either email the case officer direct or [email protected] and we will call you back. We are now able to accept hard copy correspondence via post, however this remains under review depending on national and local restrictions. We would prefer all correspondence to be electronic where possible. Please email [email protected] National Park Authority Planning Staff If you have enquiries about new applications or recent decisions made by the National Park Authority you should contact the relevant member of staff as shown below. If they are not available, you may wish to leave -

Pretty Lochside Cottage with Beautiful Views Letter Layo Shore Road, by Cove, Argyll & Bute, G84 0Nz

PRETTY LOCHSIDE COTTAGE WITH BEAUTIFUL VIEWS letter layo shore road, by cove, argyll & bute, g84 0nz PRETTY LOCHSIDE COTTAGE WITH BEAUTIFUL VIEWS letter layo shore road, by cove, argyll & bute, g84 0nz Entrance porch w reception hallway w drawing room w dining kitchen w 3 double bedrooms w bathroom w cloakroom/WC w gardens w outbuilding w communal courtyard Helensburgh: 13.5 miles, Glasgow Airport: 36 miles, Glasgow city centre: 46 miles Directions From Glasgow travel west on the M8 and exit at junction 30 for Erskine Bridge. Cross the bridge and filter left signposted A82 and Crianlarich. Beyond Loch Lomond continue through the Arden roundabout along the A82 taking the second left onto the A817 signposted Garelochhead. Proceed to the top of Glen Fruin, and at the next roundabout turn right. Continue straight over the next roundabout following signs for Coulport. On reaching Coulport turn left on the A833 onto Shore Road and Letter Layo is on the left hand side. Situation Letter Layo is set amidst mature, carefully tended gardens with wonderful southerly open aspects over Loch Long and the Firth of Clyde. Nearby Cove, Killcreggan and Peaton were established around the mid 19th century and initially were used mainly as destinations for summer houses, but as time went on permanent occupation took place. Originally there were ferries to Cove and Killcreggan, but today Killcreggan Pier remains the only traditional pier on the Clyde still in daily use. The peninsula has rich architectural heritage with Victorian mansions, castles and cottages with famous architects such as Alexander ‘Greek’ Thomson, William Lever and John Honeyman among the many to build impressive homes for wealthy clients. -

For Enquiries on This Agenda Please Contact

MINUTES of MEETING of MID ARGYLL, KINTYRE AND THE ISLANDS AREA COMMUNITY PLANNING GROUP held by SKYPE on WEDNESDAY, 3 FEBRUARY 2021 Present: Ian Brodie, East Kintyre Community Council (Chair) Councillor John Armour Councillor Anne Horn Shona Barton, Committee Manager, Argyll and Bute Council Samantha Somers, Community Planning Officer, Argyll and Bute Council Antonia Baird, Community Development Officer, Argyll and Bute Council Brian Smith, Community Learning Team Leader, Argyll and Bute Council Cristie Moore, Gaelic Development Worker, Argyll and Bute Council Sergeant Iain MacNicol, Police Scotland James Sullivan, Scottish Fire and Rescue Service Mark Benton, Scottish Ambulance Service David Graham, Maritime and Coastguard Agency Rachel Whyte, Islay Community Council Neil MacFarlane, Transport Scotland Lynn Campbell, Department for Work and Pensions Susan MacRae, Skills Development Scotland Sandra MacIntyre, Living Well Network (Islay and Jura) and Addaction 1. WELCOME AND APOLOGIES The Chair welcomed everyone to the meeting and introductions were made. The Committee Manager outlined the procedure for the meeting. Apologies for absence were intimated on behalf of: Councillor Donald MacMillan BEM Councillor Sandy Taylor Fergus Murray, Argyll and Bute Council Joanna MacDonald, Argyll and Bute HSCP Donald Watt, Argyll and Bute HSCP Alison McGrory, Argyll and Bute HSCP Robert Judge, Live Argyll Inspector Julie McLeish, Police Scotland PC Laura Evans, Police Scotland Lucy Sumsion, NFU Scotland Samantha Stubbs, Third Sector Interface Valerie Nimmo, Campbeltown Community Council Catherine Anne MacAulay, Campbeltown Community Council Linda Divers, Inveraray Community Council Jane Cowen, Tarbert and Skipness Community Trust Eric Spence, South Kintyre Development Trust Phil Dickinson, Craignish Community Council Fred Bruce, West Loch Fyne Community Council Alyson MacGillivray, South Islay Development Trust 2. -

Luss Car Park – Temporary Portaloo Facilities

ARGYLL AND BUTE COUNCIL HELENSBURGH AND LOMOND AREA COMMITTEE ROADS AND INFRASTRUCTURE 17 SEPTEMBER 2020 SERVICES LUSS CAR PARK – TEMPORARY PORTALOO FACILITIES 1.0 EXECUTIVE SUMMARY 1.1 The Scottish Government Route Map began relaxing COVID-19 measures across Scotland in May 2020. One of the measures was the opening of car parks and National Parks. As part of this, Loch Lomond and The Trossachs National Park had risk assessed their public conveniences sited at Luss and found they were not fit for purpose under the Return from Lockdown Health and Safety conditions being imposed. 1.2 Several partnership meetings were held with Argyll and Bute Council where it was suggested that 10 portaloos be sited within the current Luss Car Park. Appropriate checks were made in respect of physical distancing as well as risk assessments regarding queuing within the car park with moving vehicles and it was agreed the safest place for 10 portaloos was within 8 parking spaces at the north section of the car park behind the old visitor centre. 1.3 As part of the Argyll and Bute Council Fees and Charges, set by Full Council, the Council charge for the use of any parking bays within our car parks. This was raised with the Chief Executive and forwarded to the Council Leadership meeting where a decision was made on 2 July 2020, due to the exceptional circumstances, to suspend charging for the bays from 4 July 2020 until the end of September where a report would be brought back to the September Helensburgh and Lomond Area Committee. -

Weekly List 10 Wc 050318

Weekly Planning Schedule Week Commencing: 5 March 2018 Week Number: 10 CONTENTS 1 Valid Planning Applications Received 2 Delegated Officer Decisions 3 Committee Decisions 4 Planning Appeals 5 Enforcement Matters 6 The Forestry Commission Public Register of New Planting and Felling Applications 7 Forestry Commission Register of EIA Determinations 8 Land Reform (Scotland) Act Section 11 Access Exemption Applications 9 Other Planning Issues 10 Byelaw Exemption Applications 11 Byelaw Authorisation Applications The Public Access site will be unavailable between 08:00 on Monday 12th March and 16:00 on Thursday 15th March 2018 due to a scheduled upgrade. If you wish to view an application during this period, please contact one of our Planning Assistants on 01389 722024. If you wish to comment on a planning application please email us directly at [email protected] quoting the application reference number. We apologise for any inconvenience this may cause. National Park Authority Planning Staff If you have enquiries about new applications or recent decisions made by the National Park Authority you should contact the relevant member of staff as shown below. If they are not available, you may wish to leave a voice mail message or contact our Planning Information Manager on 01389 722024. Telephone Telephone PLANNING SERVICES DEVELOPMENT MANAGEMENT (01389) (01389) Director of Rural Development and Development & Implementation Planning 727760 Manager 722631 Stuart Mearns Bob Cook Performance and Support Manager Vacant DEVELOPMENT PLANNING -

Historic Arts and Crafts House with Separate Cottage and Views Over the Gare Loch

Historic Arts and Crafts house with separate cottage and views over the Gare Loch Ferry Inn, Rosneath, By Helensburgh, G84 0RS Lower ground floor: Sitting room, bedroom/gym, WC. Ground floor: Reception hall, drawing room, dining room, kitchen, study, morning room, pantry First floor: Principal bedroom with en suite bathroom, 3 further bedrooms, 2 further bathrooms. Ferry Inn Cottage: Detached cottage with living room/bedroom/bedroom, kitchen and shower room Garden & Grounds of around 4 acres. Local Information and both local authority and Ferry Inn is set in around 4 acres private schools. of its own grounds on the Rosneath Peninsula. The grounds The accessibility of the Rosneath form the corner of the promontory Peninsula has been greatly on the edge of Rosneath which improved by the opening of the juts out into the sea loch. There new Ministry of Defence road are magnificent views from the over the hills to Loch Lomond. house over the loch and to the The journey time to Loch marina at Rhu on the opposite. Lomond, the Erskine Bridge and Glasgow Airport has been The Rosneath Peninsula lies to significantly reduced by the new the north of the Firth of Clyde. road which bypasses Shandon, The peninsula is reached by the Rhu and Helensburgh on the road from Garelochhead in its A814 on the other side of the neck to the north. The peninsula loch. is bounded by Loch Long to the northwest, Gare Loch to the east About this property and the Firth of Clyde to the south The original Ferry Inn stood next and is connected to the mainland to the main jetty for the ferry by a narrow isthmus at its which ran between Rosneath and northern end. -

Inveraray Jail - Prisoner Records

INVERARAY JAIL - PRISONER RECORDS http://www.inverarayjail.co.uk/ USE THE EDIT / FIND ON TOOLBAR TO SEARCH NAMES and ENTRIES BY TOWN and VILLAGE By tradition and history 'the county town Argyll, Inveraray's courthouse and prisons, designed by James Gillespie Graham in 1813, after original plans by Robert Reid in 1807, opened in 1820 - Whilst Reid's original plans hadd included a courthouse and three prisons - one for males, one for females and one for debtors - The Prison Commissioners, lacking finances, had to be content with building only the courthouse and but one prison, eight cellss contained in its two floors - Following the 1839 Prisons (Scotland) Act, a second prison, separating men and women and designed by Thomas Brown of Edinburgh, was opened at the end of 1848, the new three-storied prison having twelve cells, an exercise gallery and a pair of outdoor exercise yards, the idea of separating male and female prisoners stemming from the somewhat misguided persuasion that such a system gave prisoners time to reflect upon their sins ! After the passing of the 1877 Prisons (Scotland) Act, the responsibility for the running and financing prisons taken away from local authorities, small local prisons were successively closed in favour of large prisons, such as Glasgow's 1882-built Barlinnie Prison and though Inveraray's jail, the last of the small prisons, was closed on August 31, 1889, courts continued to sit in Inveraray's courthouse until around 1954.4. After an extensive programme of restoration was undertaken by The Scottish Office in the 1980's, the building then lying empty for some years, Inveraray Jail was opened to the public as a 'visitor attraction' in May 1989 and the records of more than 4,000 of its Victorian prisoners put online for the interest of family history researchers. -

Guide to Services Links and Resources for Health and Wellbeing

Guide to Services Links and Resources for Health and Wellbeing 2! ! ! ! ! Health!is!a!state!of! complete!physical,! mental!and!social! wellbeing!and!not! merely!the!absence! of!disease!or! infirmity! ! ! ! (World'Health'Organisation)' ! ! ! ! 3! Guide to Services Links and Resources For Health & Wellbeing Contents ! Introduction - Keeping Well 4 - 7 Emergency and Crisis Contacts 8 - 19 Who’s Who in the Community Mental Health Service 20 - 28 'Self Help Resources and Websites 29 - 42 Local Services and Agencies 43 - 68 List of Local Directories 69 - 73 Information on Local Groups and Activities 74 - 86 Index 87 - 94 Survey This is for You - Relaxation CD 4! 1. Eat a balanced diet and drink sensibly: Improving your diet can protect against feelings of anxiety and depression. 2. Maintain friendships: Just listening and talking to friends who are feeling down can make a huge difference. So make sure your devote time to maintaining your friendships both for their sake and your own. 3. Maintain close relationships: Close relationships affect how we feel - so nurture them and if there is a problem within a relationship, try and resolve it. 4. Take exercise: The effects of exercise on mood are immediate. Whether it is a workout in the gym or a simple walk or bike ride, it can be uplifting. Exercise can also be great fun socially. 5. Sleep: Sleep has both physical and mental benefits. Physically it is the time when the body can renew its energy store but sleep also helps us to rebuild our mental energy. 6. Laugh: A good laugh does wonders for the mind and soul. -

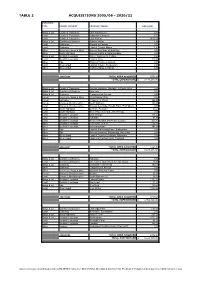

Table 2-Acquisitions (Web Version).Xlsx TABLE 2 ACQUISITIONS 2005/06 - 2020/21

TABLE 2 ACQUISITIONS 2005/06 - 2020/21 PURCHASE TYPE FOREST DISTRICT PROPERTY NAME AREA (HA) Bldgs & Ld Cowal & Trossachs Edra Farmhouse 2.30 Land Cowal & Trossachs Ardgartan Campsite 6.75 Land Cowal & Trossachs Loch Katrine 9613.00 Bldgs & Ld Dumfries & Borders Jufrake House 4.86 Land Galloway Ground at Corwar 0.70 Land Galloway Land at Corwar Mains 2.49 Other Inverness, Ross & Skye Access Servitude at Boblainy 0.00 Other North Highland Access Rights at Strathrusdale 0.00 Bldgs & Ld Scottish Lowlands 3 Keir, Gardener's Cottage 0.26 Land Scottish Lowlands Land at Croy 122.00 Other Tay Rannoch School, Kinloch 0.00 Land West Argyll Land at Killean, By Inverary 0.00 Other West Argyll Visibility Splay at Killean 0.00 2005/2006 TOTAL AREA ACQUIRED 9752.36 TOTAL EXPENDITURE £ 3,143,260.00 Bldgs & Ld Cowal & Trossachs Access Variation, Ormidale & South Otter 0.00 Bldgs & Ld Dumfries & Borders 4 Eshiels 0.18 Bldgs & Ld Galloway Craigencolon Access 0.00 Forest Inverness, Ross & Skye 1 Highlander Way 0.27 Forest Lochaber Chapman's Wood 164.60 Forest Moray & Aberdeenshire South Balnoon 130.00 Land Moray & Aberdeenshire Access Servitude, Raefin Farm, Fochabers 0.00 Land North Highland Auchow, Rumster 16.23 Land North Highland Water Pipe Servitude, No 9 Borgie 0.00 Land Scottish Lowlands East Grange 216.42 Land Scottish Lowlands Tulliallan 81.00 Land Scottish Lowlands Wester Mosshat (Horberry) (Lease) 101.17 Other Scottish Lowlands Cochnohill (1 & 2) 556.31 Other Scottish Lowlands Knockmountain 197.00 Other Tay Land at Blackcraig Farm, Blairgowrie -

484 Carrick Castle

484 Carrick Castle - Dunoon Monday to Friday from 1st July 2021 Note: CM CNM NSch CTH NSch CHF CMTW Service: 484 484 484 484 484 484 484 Carrick Castle 0710 0710 0820 1224 1454 1615 1720 Lochgoilhead, Car Park 0727 0727 0837 1241 1511 1632 1737 St Catherines (Arr) 0747 0747 0857 1301 1531 1652 1757 St Catherines (Dep) 0747 0747 0857 1301 1531 1652 1757 Strachur, The Bay 0754 0754 0903 1307 1537 1658 1803 Strachur, The Clachan 0756 0756 0905 1309 1539 1700 1805 Whistlefield Inn 0804 0804 0913 1317 1547 1708 1813 Benmore Gdns 0812 0812 0921 1325 1555 1716 1821 Kilmun 0815 0815 0924 1328 1558 1719 1824 Sandhaven 0817 0817 0926 1330 1600 1721 1826 Sandbank, Holy Loch Inn 0821 0821 0930 1334 1604 1725 1830 Dunoon, Grammar School 0826 0826 - - - - - School Hostel 0830 - - - - - - Ardenslate Road 0831 - - - - - - Marine Parade - 0828 - - - - - Walkers Garage - - 0935 1339 1609 1730 1835 Dunoon, Ferry Terminal 0836 0833 0940 1344 1614 1735 1840 Codes: NSch School Holidays 484 Service 484 is operated on behalf of Argyll and Bute Council. School holiday dates are specified by Argyll and Bute Council. No service operates on 25, 26 December or 01, 02 January. CM Schoolday Mondays Only CNM Schooldays Only, Not Mondays CMTW Schoolday Mondays, Tuesdays and Wednesdays Only CHF Schoolday Thursdays and Fridays Only 484 Dunoon - Carrick Castle Monday to Friday from 1st July 2021 Note: Sch NSch CTH NSch CH CF CMTW Service: 484 484 484 484 484 484 484 Dunoon, Ferry Terminal 0550 0655 1050 1320 1432 1432 1537 Dunoon Grammar School - - - - 1445 1445 1550 School -

Argyll Bird Report with Sstematic List for the Year

ARGYLL BIRD REPORT with Systematic List for the year 1998 Volume 15 (1999) PUBLISHED BY THE ARGYLL BIRD CLUB Cover picture: Barnacle Geese by Margaret Staley The Fifteenth ARGYLL BIRD REPORT with Systematic List for the year 1998 Edited by J.C.A. Craik Assisted by P.C. Daw Systematic List by P.C. Daw Published by the Argyll Bird Club (Scottish Charity Number SC008782) October 1999 Copyright: Argyll Bird Club Printed by Printworks Oban - ABOUT THE ARGYLL BIRD CLUB The Argyll Bird Club was formed in 19x5. Its main purpose is to play an active part in the promotion of ornithology in Argyll. It is recognised by the Inland Revenue as a charity in Scotland. The Club holds two one-day meetings each year, in spring and autumn. The venue of the spring meeting is rotated between different towns, including Dunoon, Oban. LochgilpheadandTarbert.Thc autumn meeting and AGM are usually held in Invenny or another conveniently central location. The Club organises field trips for members. It also publishes the annual Argyll Bird Report and a quarterly members’ newsletter, The Eider, which includes details of club activities, reports from meetings and field trips, and feature articles by members and others, Each year the subscription entitles you to the ArgyZl Bird Report, four issues of The Eider, and free admission to the two annual meetings. There are four kinds of membership: current rates (at 1 October 1999) are: Ordinary E10; Junior (under 17) E3; Family €15; Corporate E25 Subscriptions (by cheque or standing order) are due on 1 January. Anyonejoining after 1 Octoberis covered until the end of the following year.