I TABLE of CONTENTS Paragraph Page (S) Preface V Overview Virviii

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

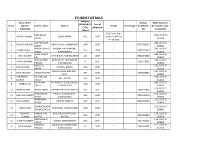

STUDENT DETAILS Category Name of the Contact Addmission Fee (GEN/OBC/S Year of Sl

STUDENT DETAILS Category Name of the Contact Addmission Fee (GEN/OBC/S Year of Sl. No. Student Father's Name Address Result Percentage No./Mobile (Reciept No. Date C/ST/ Admission Addmitted No. & Amount) Others) B.Ed Exam. Sem- RAM BALAK 1701, 03.07.17 1 SARITA KUMARI BADH, PATNA OBC 2017 I,will be Held From SINGH (50000) 12 Feb 2018 GUPTESHWAR 1702, 03.07.17 2 RENUKA KUMARI BIRA NAGAR, JAMSHEDPUR GEN 2017 " 8797935349 MEHTA (50000) NAWAL KISHOR ANCHHA, DAUDNAGAR, 1703, 03.07.17 3 SUMAN SINGH Gen 2017 " 9934727600 SINGH AURANGABAD (50000) NAND KISHOR 1704, 03.07.17 4 NISHI KUMARI DANI BIGHA, AURANGABAD gen 2017 " 8002831802 RAY (50000) SHEO KUMAR AFIM KOTHI, DAUDNAGAR 1705, 03.07.17 5 SUNITA KUMARI SC 2017 " 9525342002 PRASAD AURANGABAD (50000) BACHCHU 1706, 03.07.17 6 PINKI KUMARI KURTHA, ARWAL OBC 2017 " YADAV (50000) CHURCH ROAD GALI NO 1, 1707, 03.07.17 7 PUJA PRAKASH SANJAY KUMAR Gen 2017 " 9973855552 GAYA (50000) SHRIMANTI RAJ NANDAN 1708, 03.07.17 8 PALI, PATNA OBC 2017 " KUMARI YADAV (50000) DINANATH IN FRONT OF GATE SCHOOL, 1709, 03.07.17 9 PRERNA RAJ GEN 2017 " SINGH AURANGABAD (50000) 1710, 03.07.17 10 ABHA KUMARI ASHOK SINGH KARHASI NATWAR, ROHTAS Gen 2017 " 9006743803 (50000) NARESHWAR PILCHHI, DAUDNAGAR, 1711, 03.07.17 11 RADHIKA KUMARI OBC 2017 " 9631012310 SINGH AURANGABAD (50000) MAHENDRA 1712, 03.07.17 12 NITU KUMARI RAJPUR, ROHTAS OBC 2017 " 8002492356 SINGH (50000) CHANDESHWAR 1713, 03.07.17 13 LATIKA SINHA CLUB ROAD, AURANGABAD GEN 2017 " PRASAD SINGH (50000) POONAM RAMLAKHAN DUDHAR, SUNDARGANJ, 1714, 03.07.17 14 -

Of India 100935 Parampara Foundation Hanumant Nagar ,Ward No

AO AO Name Address Block District Mobile Email Code Number 97634 Chandra Rekha Shivpuri Shiv Mandir Road Ward No 09 Araria Araria 9661056042 [email protected] Development Foundation Araria Araria 97500 Divya Dristi Bharat Divya Dristi Bharat Chitragupt Araria Araria 9304004533 [email protected] Nagar,Ward No-21,Near Subhash Stadium,Araria 854311 Bihar Araria 100340 Maxwell Computer Centre Hanumant Nagar, Ward No 15, Ashram Araria Araria 9934606071 [email protected] Road Araria 98667 National Harmony Work & Hanumant Nagar, Ward No.-15, Po+Ps- Araria Araria 9973299101 [email protected] Welfare Development Araria, Bihar Araria Organisation Of India 100935 Parampara Foundation Hanumant Nagar ,Ward No. 16,Near Araria Araria 7644088124 [email protected] Durga Mandir Araria 97613 Sarthak Foundation C/O - Taranand Mishra , Shivpuri Ward Araria Araria 8757872102 [email protected] No. 09 P.O + P.S - Araria Araria 98590 Vivekanand Institute Of 1st Floor Milan Market Infront Of Canara Araria Araria 9955312121 [email protected] Information Technology Bank Near Adb Chowk Bus Stand Road Araria Araria 100610 Ambedkar Seva Sansthan, Joyprakashnagar Wardno-7 Shivpuri Araria Araria 8863024705 [email protected] C/O-Krishnamaya Institute Joyprakash Nagar Ward No -7 Araria Of Higher Education 99468 Prerna Society Of Khajuri Bazar Araria Bharga Araria 7835050423 [email protected] Technical Education And ma Research 100101 Youth Forum Forbesganj Bharga Araria 7764868759 [email protected] -

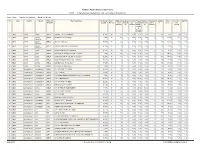

State District Name of Bank Bank Branch/ Financial Literacy Centre

State District Name of Bank Branch/ Address ITI Code ITI Name ITI Address State District Phone Email Bank Financial Category Number Literacy Centre Bihar Araria State Araria Lead Bank Office, PR10000055 Al-Sahaba Industrial P Alamtala Forbesganj Bihar Araria NULL Bank of ADB Building, Training Institute India Araria, Pin- 854311 Bihar Arwal PNB ARWAL ARWAL PR10000083 Adarsh ITC P Umerabad Bihar Arwal NULL Bihar Arwal PNB ARWAL ARWAL PR10000284 Shakuntalam ITC P Prasadi English Bihar Arwal NULL Bihar Arwal PNB ARWAL ARWAL PR10000346 Aditya ITC P At. Wasilpur, Main Road, Bihar Arwal NULL P.O. Arwal, Bihar Arwal PNB ARWAL ARWAL PR10000396 Vikramshila Private P At. Rojapar, P.O. Arwal Bihar Arwal NULL ITI Bihar Arwal PNB ARWAL ARWAL PR10000652 Ram Bhaman Singh P At-Purani Bazar P.o+P.S- Bihar Arwal NULL Private ITI Arwal Bihar Arwal PNB ARWAL ARWAL PR10000677 Sukhdeo Institute Of P Kurtha, Arwal Bihar Arwal NULL Tecnology Private ITI, Bihar Arwal PNB ARWAL ARWAL PR10000707 Dr. Rajendra Prasad P Mubarkpur, Kurtha Arwal Bihar Arwal NULL Private ITI, Bihar Aurangabad PUNJAB DAUDNAGAR DAUDNAGAR PR10000027 New Sai Private ITI- P Aurangabad Road, Bihar Aurangabad NULL NATIONA Bhakharuan More, , Tehsil- L BANK Daudnagar , , Aurangabad - 824113 Bihar Aurangabad PUNJAB AURANGABAD AURANGABAD PR10000064 Adharsh Industrial P Josai More Udyog Bihar Aurangabad NULL NATIONA Training Centre Pradhikar Campus L BANK Bihar Aurangabad MADHYA DAUDNAGAR DAUDNAGAR PR10000108 Sardar Vallabh Bhai P Daudnagar Bihar Aurangabad NULL BIHAR Patel ITC, Daudnagar GRAMIN BANK Bihar Aurangabad MADHYA DAUDNAGAR DAUDNAGAR PR10000142 Adarsh ITC, P AT-,Growth centre ,Jasoia Bihar Aurangabad NULL BIHAR Daudnagar More Daudnagar GRAMIN BANK Bihar Aurangabad PUNJAB RATANUA RATANUA PR10000196 Progresive ITC P At-Growth Center Josia Bihar Aurangabad NULL NATIONA More L BANK Bihar Aurangabad MADHYA DAUDNAGAR DAUDNAGAR PR10000199 Arya Bhatt ITC P Patel Nagar, Daud Nagar Bihar Aurangabad NULL BIHAR GRAMIN BANK Bihar Aurangabad PUNJAB OLD GT RD. -

Directory Establishment

DIRECTORY ESTABLISHMENT SECTOR :URBAN STATE : BIHAR DISTRICT : Araria Year of start of Employment Sl No Name of Establishment Address / Telephone / Fax / E-mail Operation Class (1) (2) (3) (4) (5) NIC 2004 : 2021-Manufacture of veneer sheets; manufacture of plywood, laminboard, particle board and other panels and boards 1 PLYWOOD COMPANY P.O.- BHAGATVENEER DIST: ARARIA PIN CODE: 854311, STD CODE: NA , TEL NO: NA , FAX NO: 2000 10 - 50 NA, E-MAIL : N.A. NIC 2004 : 5020-Maintenance and repair of motor vehicles 2 AGARWAL MOTAR GARAGE, P.O.- FORBESGANJ, WARDNO. 11 DIST: ARARIA PIN CODE: 854318, STD CODE: 06455, TEL NO: 1954 10 - 50 FORBESGANJ NA , FAX NO: NA, E-MAIL : N.A. NIC 2004 : 6010-Transport via railways 3 RAILWAY STATION, FORBESGANJ P.O.- FORBISGANJ DIST: ARARIA PIN CODE: 854318, STD CODE: 06455, TEL NO: 0222545, FAX 1963 51 - 100 NO: NA, E-MAIL : N.A. 4 P.W.I.S.E.OFFICE, N.F.RAILWAY, P.O.- FPRBESGANJ DIST: ARARIA PIN CODE: 854318, STD CODE: NA , TEL NO: NA , FAX NO: 1963 101 - 500 FORBESGANJ NA, E-MAIL : N.A. NIC 2004 : 6302-Storage and warehousing 5 SEEMA COLD STORAGE, FORBESGANJ P.O.- FORBESGANJ, WARD NO. 1, LOHIA PATH DIST: ARARIA PIN CODE: 854318, STD CODE: 1961 10 - 50 06455, TEL NO: 222773, FAX NO: NA, E-MAIL : N.A. NIC 2004 : 6511-Central banking_relates to the functions and working of the Reserve Bank of India 6 STATE BANK O FINDIA, S.K.ROAD, P.O.- FORBESGANJ DIST: ARARIA PIN CODE: 854318, STD CODE: 06455, TEL NO: 222540, FAX 1942 10 - 50 FORBESGANJ NO: NA, E-MAIL : N.A. -

Pradhan Mantri Gram Sadak Yojana CUCPL - Comprehensive Up-Gradation Cum Consolidation Priority List

Pradhan Mantri Gram Sadak Yojana CUCPL - Comprehensive Up-gradation cum Consolidation Priority List State : Bihar District : All Districts Block : All Blocks Sr.No. State District Block Plan CN Plan Road Name Plan Road Route Educati Medical Veterin Transp Market Administ Populatio Total Score Per Avg PCI Road No. Length Priority onal Faciliti ary ort and Faciliti rative n Score Unit Services es Facilitie Commu es Centres Length s nicatio n Infrastr ucture 1 Bihar Arwal Arwal MRL01 Walidad, T01 To Khamhaini 10.835 M 12 0 0.00 0.00 0.00 1 68 81.00 7.48 1.00 2 Bihar Arwal Banshi MRL02 Manjhiyama to Khatangi 9.465 M 16 8 0.00 9.00 0.00 1 77 111.00 11.73 1.00 Surajpur 3 Bihar Arwal Banshi MRL03 Kharasi to Belaura 14.943 M 22 8 0.00 3.00 0.00 1 89 123.00 8.23 1.00 Surajpur 4 Bihar Arwal Banshi MRL01 Khatangi senari RD to Mobarakpur 10.860 M 9 4 0.00 3.00 0.00 1 42 59.00 5.43 1.00 Surajpur 5 Bihar Arwal Kaler MRL01 Sohasa Road L037 To Masadpur 21.676 M 10 6 0.00 6.00 0.00 1 54 77.00 3.55 1.00 6 Bihar Arwal Karpi MRL02 Imamganj Deokund Road,T04 To Jonha 7.365 M 22 8 3.00 11.00 9.00 2 91 146.00 19.82 1.00 7 Bihar Arwal Karpi MRL01 Karpi Barahmile Road, T03 To Salarpur 12.365 M 18 6 0.00 9.00 7.00 2 104 146.00 11.81 1.00 8 Bihar Arwal Karpi MRL03 Arwal Jehanabad Road, T02 To Aiyara 16.787 M 7 0 0.00 0.00 7.00 1 52 67.00 3.99 1.00 9 Bihar Arwal Kurtha MRL02 Salarpur L042, To Dhamaul 15.238 M 9 4 0.00 3.00 7.00 2 88 113.00 7.42 1.00 10 Bihar Arwal Kurtha MRL01 Pinjrawan to Manepaker 9.456 M 8 2 0.00 0.00 0.00 1 55 66.00 6.98 1.00 11 Bihar Aurangabad -

List of Bio Gas Plant Installed in Bihar During 2007-08

List of Bio Gas Plant Installed in Bihar During 2007-08 SI District Name of Village Post Block Category Model Sizecum Date of Subsidy Sup. Self/bank R.E.T. Technical Paid by ch./ No. Benefeciary/ S/o functioning Ch. finance staff DD no & date 1. Aurangabad Nagendra Singhm Amba Amba Kutumba Gen. DB 2 05.03.08 2700 700 Turnkey N. K. Md. 165087 Dt. Ugrah Singh Singh Rustam 07/05/08 2. Aurangabad Binay Pande Amba Dhamni Simri Nabinagar SMF DB 2 14.02.08 3500 700 Turnkey N. K. Md. 165085 Dt. Lt. Faujdar Pande Dhamni Singh Rustam 28/03/08 3. Aurangabad Perna Pandey Amba Dhamni Simri Nabinagar SMF DB 2 14.02.08 3500 700 Turnkey N. K. Md. 165085 Dt. Lt. Rekha Pande Dhamni Singh Rustam 28/03/08 4. Aurangabad Raj Kishore Singh Amilauna Amilauna Obra Gen. DB 2 28.02.08 2700 700 Turnkey N. K. Prashant 165085 Dt. Shri Jagdish Singh Singh Mishra 28/03/08 5. Aurangabad Yugal Pandey Amilauna Amilauna Obra Gen. DB 2 25.02.08 2700 700 Turnkey N. K. Prashant 165085 Dt. Lt. Doodheshwer Singh Mishra 28/03/08 Pande 6. Aurangabad Mahendra Kr. Amilauna Amilauna Obra Gen. DB 2 03.03.08 2700 700 Turnkey N. K. Prashant 165085 Dt. Singh Shri Ram Singh Mishra 28/03/08 Awatar Singh 7. Aurangabad Lalu Kishore Anugrah Nagar Aurangabad Aurangabad Gen. DB 3 19.03.08 2700 700 Turnkey N. K. Md. 165090 Dt. Prasad Lt. Singh Rustam 30/05/08 Dev nandan Prasad 8. Aurangabad Mahraj Mehta Bahera Ankuppa Kutumba Gen. -

Aurangabad, Bihar

DISTRICT HEALTH SOCIETY AURANGABAD , B IHAR District Health Action Plan 2012-2013 Prepared By: Sagar (District Programme Manager) Ashwini Kumar (District Accounts Manager) Rajeev Ranjan (District Monitoring & Evaluation Officer) B.B. Vikrant (District Planning Coordinator) Rahul Kumar Singh (District Community Mobilizer, ASHA) Under the able Guidance of: Dr. Parshuram Bharti Mr. Abhay Kumar Singh (IAS) Civil Surgeon cum Member Secretary District Magistrate cum Chairman District Health Society, Aurangabad District Health Society, Aurangabad District Health Society, Aurangabad Page -1- Table of contents Foreword Table of Contents Topics Page CHAPTER 1 INTRODUCTION 01-05 CHAPTER 2 DISTRICT PROFILE 06-14 Introduction 06 Geography 06 Demography 07 Physiography 07 History 08 Administrative Setup 09-11 Communication Map of the district 12 Health Facilities Map of the district 13 Population Details 14 CHAPTER 3 SITUATIONAL ANALYSIS 15-29 Gaps in Infrastructure 15-18 Aurangabad at a Glance 19 Health Facilities 20 Human Resource 21-22 ASHA Status 23 MAMTA Status 24 Bed Availability 25 Basic Facilities at Rural Institutions 26 District Hospital 27 Indicators of RCH 28 CHAPTER 4 SETTING OBJECTIVES AND SUGGESTED 30-36 PLAN OF ACTION Introduction 30 Targeted Objectives and Suggested Strategies 30-36 (Maternal Health, FRUs, RCH Services, VHSND, JBSY, IMNCI, Caesarean, JSY, Institutional Delivery, NPSGK, NRC) CHAPTER 5 BUDGET 37 -48 District Health Society, Aurangabad Page -2- Foreword It is very rightly said that Health is Wealth. The Importance of Health in the process of economic and social development and improving the quality of life of our citizens, cannot be denied. Recognizing the importance of Health, the Government of India has launched the National Rural Health Mission on 12 th April 2005 in India. -

Bihar Power 13Th Plan BSPTCL & BGCL

83°30'0"E 84°0'0"E 84°30'0"E 85°0'0"E 85°30'0"E 86°0'0"E 86°30'0"E 87°0'0"E 87°30'0"E 88°0'0"E 27°30'0"N Surajpura Hydel P.S 27°30'0"N BIHAR MAP (Nepal) BHPC Valmikinagar (BSPTCL & BGCL WITH 13th PLAN) ± WEST CHAMPARAN Harinagar Sugar Mill Harinagar Narkatiaganj TSS Narkatiaganj Sugar Mill 132 kV Ramnagar (Parwanipur - Nepal) 27°0'0"N 33 kV 33kV Jaleshwar 27°0'0"N HPCL (Nepal) Raxaul (Birganj - Nepal) Lauriya TSS Raxaul Sugarmill Majhaulia NEPAL TSS Raxaul (New) Jivdhara TSS Dhanaha Bettiah Sugauli 33 KV Bettiah TSS Sugar Mill Dhaka Bairgania Biratnagar 132 KV TSS Duhabi Motihari SITAMARHI Pupri 33 KV EAST CHAMPARAN Rajbiraj Motihari Sitamarhi Sheohar Jainagar GOPALGANJ (DMTCL) Pakridayal Sitamarhi 26°30'0"N Hathua Areraj (New) MADHUBANI Kataiya 26°30'0"N SHEOHAR Bajpatti Laukahi TSS Benipatti Bharat Chakia Belsand Thakurganj Gopalganj Sugar Mill Mahwal Runnisaidpur TSS Madhubani Phulparas SUPAUL ARARIA Motipur Shiso TSS Pandaul UTTAR Maharajganj KISHANGANJ Kishanganj (PG) Siwan Ramdayalu Forbesganj TSS MTPS Raghopur Kishanganj SIWAN Gangwara Sakari TSS Pachrukhi Rajapatti SKMCH (New) PRADESH TSS Triveniganj TSS Darbhanga Nirmali Supaul Mashrakh Muzaarpur Mushahari Araria Darbhanga Jhanjharpur DLF MUZAFFARPUR Benipur Kishanganj 132/33 kV Marhowrah (Railway) MADHEPURA 26°0'0"N GSS Siwan Muzaarpur-PG Turki DARBHANGA TSS 26°0'0"N Madhepura SARAN Vaishali Saharsa Amnor-BGCL Shahpurpatori Darbhanga Saharsa Ekma Bela Rail Tajpur (DMTCL) (New) Factory Goraul Samastipur Kusheshwarsthan Banmankhi Purnea Chapra (New) Rosera Baisi Hajipur VAISHALI -

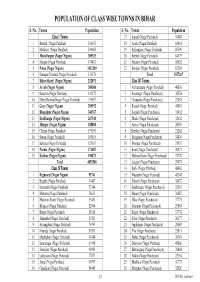

Population of Class Wise Towns in Bihar

POPULATION OF CLASS WISE TOWNS IN BIHAR S. No. Towns Population S. No. Towns Population Class I Towns 17 Supaul (Nagar Parishad) 54085 1 Bettiah (Nagar Parishad) 116670 18 Araria (Nagar Parishad) 60861 2 Motihari (Nagar Parishad) 100683 19 Kishanganj (Nagar Parishad) 85590 3 Muzaffarpur (Nagar Nigam) 305525 20 Beehat (Nagar Parishad) 64579 4 Hajipur (Nagar Parishad) 119412 21 Barauni (Nagar Parishad) 58628 5 Patna (Nagar Nigam) 1432209 22 Benipur (Nagar Parishad) 62203 6 Danapur Nizamat (Nagar Parishad) 131176 Total 1557267 7 Bihar Sharif (Nagar Nigam) 232071 Class III Towns 8 Arrah (Nagar Nigam) 203380 1 Narkatiaganj (Nagar Parishad) 40830 9 Sasaram (Nagar Parishad) 131172 2 Ramnagar (Nagar Panchayat) 38554 10 Dehri DalmiyaNagar (Nagar Parishad) 119057 3 Chanpatia (Nagar Panchayat) 22038 11 Gaya (Nagar Nigam) 389192 4 Raxaul (Nagar Parishad) 41610 12 Bhagalpur (Nagar Nigam) 340767 5 Sugauli (Nagar Panchayat) 31432 13 Darbhanga (Nagar Nigam) 267348 6 Dhaka (Nagar Panchayat) 32632 14 Munger (Nagar Nigam) 188050 7 Areraj (Nagar Panchayat) 20356 15 Chapra (Nagar Parishad) 179190 8 Sheohar (Nagar Panchayat) 21262 16 Siwan (Nagar Parishad) 109919 9 Bairgania (Nagar Panchayat) 34836 17 Saharsa (Nagar Parishad) 125167 10 Motipur (Nagar Panchayat) 21957 18 Purnia (Nagar Nigam) 171687 11 Kanti (Nagar Panchayat) 20871 19 Katihar (Nagar Nigam) 190873 12 Mahnar Bazar (Nagar Panchayat) 37370 Total 4853548 13 Lalganj (Nagar Panchayat) 29873 Class II Towns 14 Barh (Nagar Parishad) 48442 1 Begusarai (Nagar Nigam) 93741 15 Masaurhi (Nagar Parishad) 45248 -

Sch Code School Name Dist Name 11001 Zila School

BIHAR SCHOOL EXAMINATION BOARD PATNA DISTRICTWISE SCHOOL LIST 2013(CLASS X) SCH_CODE SCHOOL_NAME DIST_NAME 11001 ZILA SCHOOL PURNEA PURNEA 11002 URSULINE CONVENT GIRLS HIGH SCHOOL PURNEA PURNEA 11003 B B M HIGH SCHOOL PURNEA PURNEA 11004 GOVT GIRLS HIGH SCHOOL PURNEA PURNEA 11005 MAA KALI HIGH SCHOOL MADHUBANI PURNEA 11006 JLNS HIGH SCHOOL GULAB BAGH PURNEA 11007 PARWATI MANDAL HIGH SCHOOL HARDA PURNEA 11008 ANCHIT SAH HIGH SCHOOL BELOURI PURNEA 11009 HIGH SCHOOL CHANDI RAZIGANJ PURNEA 11010 GOVT HIGH SCHOOL SHRI NAGAR PURNEA 11011 SIYA MOHAN HIGH SCHOOL SAHARA PURNEA 11012 R P C HIGH SCHOOL PURNEA CITY PURNEA 11013 HIGH SCHOOL KASBA PURNEA 11014 K D GIRLS HIGH SCHOOL KASBA PURNEA 11015 PROJECT GIRLS HIGH SCHOOL RANI PATRA PURNEA 11016 K G P H/S BHOGA BHATGAMA PURNEA 11017 N D RUNGTA H/S JALAL GARH PURNEA 11018 KALA NAND H/S GARH BANAILI PURNEA 11019 B N H/S JAGNICHAMPA NAGAR PURNEA 11020 PROJECT GIRLS HIGH SCHOOL GOKUL PUR PURNEA 11021 ST THOMAS H S MUNSHIBARI PURNEA PURNEA 11023 PURNEA H S RAMBAGH,PURNEA PURNEA 11024 HIGH SCHOOL HAFANIA PURNEA 11025 HIGH SCHOOL KANHARIA PURNEA 11026 KANAK LAL H/S SOURA PURNEA 11027 ABUL KALAM HIGH SCHOOL ICHALO PURNEA 11028 PROJECT GIRLS HIGH SCHOOL AMOUR PURNEA 11029 HIGH SCHOOL RAUTA PURNEA 11030 HIGH SCHOOL AMOUR PURNEA 11031 HIGH SCHOOL BAISI PURNEA 11032 HIGH SCHOOL JHOWARI PURNEA 11033 JANTA HIGH SCHOOL BISHNUPUR PURNEA 11034 T N HIGH SCHOOL PIYAZI PURNEA 11035 HIGH SCHOOL KANJIA PURNEA 11036 PROJECT KANYA H S BAISI PURNEA 11037 UGRA NARAYAN H/S VIDYAPURI PURNEA 11038 BALDEVA H/S BHAWANIPUR RAJDHAM -

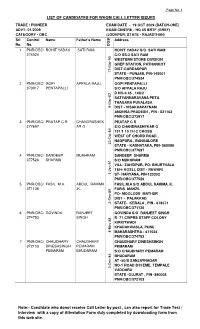

Candidate Who Donot Receive Call Letter by Post , Can Also Report For

Page No. 1 LIST OF CANDIDATES FOR WHOM CALL LETTER ISSUED TRADE : PIONEER EXAM DATE - 19 OCT 2009 (BATCH-ONE) ADVT- 01/2009 EXAM CENTRE - HQ 45 BRTF (GREF) CATEGORY - OBC (JODHPUR, STATE - RAJASTHAN) Srl Control Name Father's Name Address No. No. DOB 1 PNR/OBC/ ROHIT YADAV SATI RAM ROHIT YADAV S/O SATI RAM 374524 C/O SS-2 SATI RAM WESTERN STORE DIVISION GREF STATION, PATHANKOT DIST-GURDASPUR 17-Mar-90 STATE - PUNJAB, PIN-145001 PNR/OBC/374524 2 PNR/OBC/ GOPI APPALA RAJU GOPI PENTAPALLI 373917 PENTAPALLI S/O APPALA RAJU D NO-6 45 , 148/2 SATYANNARAYANA PETA THAGARA PUVALASA 9-Mar-87 DIST - VISAKHAPATNAM ANDHRA PRADESH , PIN - 531162 PNR/OBC/373917 3 PNR/OBC/ PRATAP C R CHANDRASHEK PRATAP C R 377697 AR G S/O CHANDRASHEKAR G 131/1 10 TH C CROSS WEST OF CHORD ROAD , NAGPURA , BANGALORE 23-Oct-84 STATE - KARNATAKA, PIN- 560086 PNR/OBC/377697 4 PNR/OBC/ SANDEEP MUKHRAM SANDEEP SHARMA 377526 SHARMA S/O MUKHRAM VILL- ZAHIDPUR, PO- BHURTHALA TEH- KOSLI, DIST - REWARI 1-Jan-91 ST- HARYANA, PIN-123302 PNR/OBC/377526 5 PNR/OBC/ FASIL M.A. ABDUL RAHIMA FASIL.M.A S/O ABDUL RAHIMA .K. 371136 .K. FARIS MANZIL PO- MOOLODE MATHUR DIST - PALAKKAD 2-Sep-89 STATE- KERALA , PIN - 678571 PNR/OBC/371136 6 PNR/OBC/ GOVINDA RANJEET GOVINDA S/O RANJEET SINGH 374753 SINGH B- 71 CWPRS STAFF COLONY KIRKITWADI KHADAKWASLA, PUNE 8-Nov-88 MAHARASHTRA - 411024 PNR/OBC/374753 7 PNR/OBC/ CHAUDHARY CHAUDHARY CHAUDHARY DINESHSINGH 372103 DINESHSINGH PEMARAM PEMARAM PEMARAM BHUDARAM S/O CHAUDHARY PEMARAM BHUDARAM AT -50/B SANJAYNAGAR NO-1 ROAD B/H EME, TEMPALE 3-Dec-84 VADOARA STATE -GUJRAT , PIN -390008 PNR/OBC/372103 Note:- Candidate who donot receive Call Letter by post , can also report for Trade Test / Interview with a copy of Attestation Form duly completed by downloading form from this web site. -

Block Teacher Niyojan-2019-20

BLOCK TEACHER NIYOJAN-2019-20 BLOCK: PIRO CLASS-1-5 (GEN) DIST:-BHOJPUR PROVISIONAL MERIT LIST ONLY B.ED APPLICANTS 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 MATRIC INTER TRAINING WEIG FREE BTET/ SUM OF AVG OF TAGE TRAIN APPL.S. NAME OF SE D. FUL CTET TOTAL S.N. FATHER DOB ADDRESS CAT DIS. MARKS MARKS FULL MARKS FULL PERCENT PERCE OF ING REMARKS N. APPLICANT X FIGH L MARK MERIT OBTAI %GE OBTAIN MAR %GE OBTAIN MAR %GE AGE NTAGE BTET/ T. MAR S% TYPE NED ED KS ED KS CTET KS SNEHA ASHOK BANK MORE 1 1768 21/1/1992 F UR NN 451 500 90.2 440 500 88 1079 1300 83 261.2 87.07 73.3 4 91.06667 B.ED KUMARI SHARMA DHANBAD RINKU A K CHURAMANPUR 2 2097 30/06/1994 F EWS NN 475 500 95 415 500 83 867 1000 86.7 264.7 88.23 64 2 90.23333 B.ED KUMARI TIWARI BUXAR KARAMAT BUSHRA RAMNAGAR SEDHA 3 2017 ALI 14/3/1997 F EBC N N 427 500 85.4 394 500 78.8 1065 1300 81.9231 246.123 82.04 70.6 4 86.04103 B.ED SHAMIMA PIRO ANSARI MOHD BUSHRA ARANGI-01, USIA, 4 2389 MONIR 20/04/1994 F UR NN 458 500 91.6 463 600 77.167 1800 2250 80 248.767 82.92 60 2 84.92222 B.ED MONIR DILDARNAGAR, UP ANSARI PRIYANKA SANJAY 5 P/772 13/1/1996 F PARSA BAZAR PATNA EBC N N 441 500 88.2 436 500 87.2 1060 1450 73.1034 248.503 82.83 55.5 2 84.83448 B.ED KUMARI KUMAR MOHD NAZIA ARANGI-01, USIA, 6 2388 MONIR 18/04/1995 F UR NN 457 500 91.4 434 600 72.333 1675 2000 83.75 247.483 82.49 64 2 84.49444 B.ED MONIR DILDARNAGAR, UP ANSARI PUJA RAMESH DHELWAN BEUR 7 1793 KUMARI KUMAR 15/12/1995 F UR N N 465.5 500 93.1 339 500 67.8 1022 1300 78.6154 239.515 79.84 70.7 4 83.83846