Standing Committee on Defence (2003) (Thirteenth Lok Sabha)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LOK SABHA ___ BULLETIN-PART II (General Information Relating To

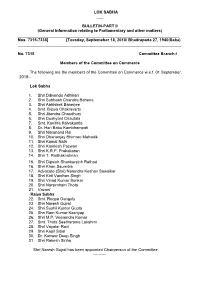

LOK SABHA ___ BULLETIN-PART II (General Information relating to Parliamentary and other matters) ________________________________________________________________________ Nos. 7315-7338] [Tuesday, Septemeber 18, 2018/ Bhadrapada 27, 1940(Saka) _________________________________________________________________________ No. 7315 Committee Branch-I Members of the Committee on Commerce The following are the members of the Committee on Commerce w.e.f. 01 September, 2018:- Lok Sabha 1. Shri Dibyendu Adhikari 2. Shri Subhash Chandra Baheria 3. Shri Abhishek Banerjee 4. Smt. Bijoya Chakravarty 5. Shri Jitendra Chaudhury 6. Shri Dushyant Chautala 7. Smt. Kavitha Kalvakuntla 8. Dr. Hari Babu Kambhampati 9. Shri Nityanand Rai 10. Shri Dhananjay Bhimrao Mahadik 11. Shri Kamal Nath 12. Shri Kamlesh Paswan 13. Shri K.R.P. Prabakaran 14. Shri T. Radhakrishnan 15. Shri Dipsinh Shankarsinh Rathod 16. Shri Khan Saumitra 17. Advocate (Shri) Narendra Keshav Sawaikar 18. Shri Kirti Vardhan Singh 19. Shri Vinod Kumar Sonkar 20. Shri Narsimham Thota 21. Vacant Rajya Sabha 22. Smt. Roopa Ganguly 23. Shri Naresh Gujral 24. Shri Sushil Kumar Gupta 25. Shri Ram Kumar Kashyap 26. Shri M.P. Veerendra Kumar 27. Smt. Thota Seetharama Lakshmi 28. Shri Vayalar Ravi 29. Shri Kapil Sibal 30. Dr. Kanwar Deep Singh 31. Shri Rakesh Sinha Shri Naresh Gujral has been appointed Chairperson of the Committee. ---------- No.7316 Committee Branch-I Members of the Committee on Home Affairs The following are the members of the Committee on Home Affairs w.e.f. 01 September, 2018:- Lok Sabha 1. Dr. Sanjeev Kumar Balyan 2. Shri Prem Singh Chandumajra 3. Shri Adhir Ranjan Chowdhury 4. Dr. (Smt.) Kakoli Ghosh Dastidar 5. Shri Ramen Deka 6. -

Uncorrected – Not for Publication LSS-D-I

Uncorrected – Not for Publication LSS-D-I LOK SABHA DEBATES (Part I -- Proceedings with Questions and Answers) Tuesday, March 6, 2018/ Phalguna 15, 1939 (Saka) LOK SABHA DEBATES PART I – QUESTIONS AND ANSWERS Tuesday, March 6, 2018/Phalguna 15, 1939 (Saka) CONTENTS PAGES …. 1 WRITTEN ANSWERS TO STARRED QUESTIONS 1A-21 (S.Q. NO. 141-160) WRITTEN ANSWERS TO UNSTARRED QUESTIONS 22-251 (U.S.Q. NO. 1611-1840) Uncorrected – Not for Publication LSS-D-II LOK SABHA DEBATES (Part II - Proceedings other than Questions and Answers) Tuesday, March 6, 2018/ Phalguna 15, 1939 (Saka) LOK SABHA DEBATES PART II –PROCEEDINGS OTHER THAN QUESTIONS AND ANSWERS Tuesday, March 6, 2018/Phalguna 15, 1939 (Saka) C ON T E N T S P A G E S RULING RE: NOTICES OF ADJOURNMENT MOTION 252 PAPERS LAID ON THE TABLE 253-55 STANDING COMMITTEE ON AGRICULTURE 256 th th 47 to 50 Reports STANDING COMMITTEE ON RAILWAYS 257 th 19 Report STANDING COMMITTEE ON RURAL DEVELOPMENT 257-58 nd th 42 to 45 Reports STANDING COMMITTEE ON TRANSPORT, TOURISM AND 258-59 CULTURE th st 257 to 261 Reports MOTION RE: 51st REPORT OF BUSINESS ADVISORY 260 COMMITTEE MATTERS UNDER RULE 377 – LAID 261-95 Shri Bharat Singh 262 Shri Harish Meena 263 Shri Devendra Singh Bhole 264 Dr. Manoj Rajoria 265 Shrimati Rakshatai Khadse 266 Shri Jugal Kishore 267 Dr. Kirit P. Solanki 268 Shri Jagdambika Pal 269 Shri Arjun Lal Meena 270 Shri Om Birla 271 Col. Sona Ram Choudhary 272 Dr. Udit Raj 273 Shrimati Rama Devi 274 Shri Laxmi Narayan Yadav 275 Shri Gaurav Gogoi 276 Shri Rajeev Satav 277 Shri Anto Antony 278 Shri P. -

Membersofparliament(Xvehloksabha)Nominatedaschairman/Co-Chairmantothe Committtee (DISHA) District Development Coordination & Monitoring

MembersofParliament(XVEhLokSabha)NominatedasChairman/Co-Chairmantothe Committtee (DISHA) District Development Coordination & Monitoring ANDAMAN & NICOBAR ISLANDS Member of Parliament Members of Parliament (XVlth Lok Sabha) Nominated as Chairman/Co- chairman to the District Development coordination & Monitoring committtee ANDHRA PRADESH District Member of Parliament Chairman/Co-Chairman Chairman Anantapur Shri Kristappa Nimmala Shri J-C. Divaka r Reddy Co-Chairman chairman Chittoor Dr. Naramalli SivaPrasad Shri Midhun Reddy Co-chairman Dr. Vara Prasadarao Velaga Palli Co-Chairman East Godavari Shri Murali Mohan Maganti Chdimon Co-Choirmon Sh ri Narasimham Thota Dr. Ravindra Babu Pandula Co-choirmon Smt. Geetha KothaPa lli Co-choirmon chairman Guntur Shri Rayapati Samb!9!Yq leo Co-Chairman Shri Jayadev Galla Co-Chairman Shri Sriram MalYadri chairman Kadapa Shri Y. S. Avinash ReddY chri Mi.lhunn Reddv Co-Chairman Rao Chairman Krishna Shri Konakalla Narayana Co-Chairman Shri Srinivas Kesineni qhri Vankateswa ra Rao Masantti Co-Chairman Chairman Kurnool chrisPY-Reddev cmt Rpnllka Blltta Co-Chairman ReddY Chairman Nellore shri MekaDati Raiamohan nr \/era Prasadarao Velaea Palli Co-Chairman Subbareddy chairman Prakasam Shri Yerram Venkata cl-.,i C.iram l\rrl\/arlri Co-Chairman Co-Chairman Shri Mekpati Raiamohan ReddY Chairman Srikakulam Shri Ashok GajaPati Raju Pusapati Shri Kiniarapu Ram Mohan Naidu Co-Chairman Smt. Geetha KothaPalli Co-Chairperson Chairperson Vishakhapatnam Smt. Geetha KothaPalli Shri Muthamsetti Srinivasa Rao (Avnth Co-Chairman -

January, 2019/Pausa, 1940(Saka)

45 STANDING COMMITTEE ON DEFENCE (2018-19) (SIXTEENTH LOK SABHA) MINISTRY OF DEFENCE [ACTION TAKEN BY THE GOVERNMENT ON THE OBSERVATIONS/RECOMMENDATIONS CONTAINED IN THIRTY-THIRD REPORT OF STANDING COMMITTEE ON DEFENCE (16TH LOK SABHA) ON ‘RESETTLEMENT OF EX-SERVICEMEN'] FORTY- FIFTH REPORT LOK SABHA SECRETARIAT NEW DELHI January, 2019/Pausa, 1940(Saka) FORTY- FIFTH REPORT STANDING COMMITTEE ON DEFENCE (2018-19) (SIXTEENTH LOK SABHA) MINISTRY OF DEFENCE [ACTION TAKEN BY THE GOVERNMENT ON THE OBSERVATIONS/RECOMMENDATIONS CONTAINED IN THIRTY-THIRD REPORT OF STANDING COMMITTEE ON DEFENCE (16TH LOK SABHA) ON ‘RESETTLEMENT OF EX-SERVICEMEN'] Presented to Lok Sabha on 7.1.2019 Laid in Rajya Sabha on 7.1.2019 LOK SABHA SECRETARIAT NEW DELHI January, 2019/Pausa, 1940(Saka) CONTENTS PAGE. COMPOSITION OF THE COMMITTEE (2018-19).……………………….....……............. (iii) INTRODUCTION..…………………………………………………….….……….................... (v) CHAPTER I Report…………………………………………………………………..... CHAPTER II Recommendations/Observations which have been accepted by the Government………………………………………....... CHAPTER III Recommendations/Observations which the Committee do not desire to pursue in view of the replies of the Government ………………………………….................................... CHAPTER IV Recommendations/Observations in respect of which Replies of the Government have not been accepted by The Committee and which require reiteration………………….…....... CHAPTER V Recommendations/Observations in respect of which Government have furnished interim replies………………………........ APPENDICES I Minutes of the Second sitting of the Standing Committee on Defence (2018-19) held on 14.11.2018.………………................. II Analysis of Action Taken by the Government on the Observations/Recommendations contained in the Thirty-third Report (16th Lok Sabha) of the Standing Committee on Defence (2018-19)................................................. COMPOSITION OF THE STANDING COMMITTEE ON DEFENCE (2018-19) SHRI KALRAJ MISHRA - CHAIRPERSON Lok Sabha 2. -

Panel of Chairpersons Cabinet Ministers

an> Title: Newly elected members of 16th Lok Sabha took the oath or made the affirmation, signed the Roll of members and took their seats in the House. HON.SPEAKER: Now I call hon. Members to make oath orsubscribe affirmation. Shri Narendra Damodardas Modi (Varanasi) - Oath - Hindi Shri L.K. Advani (Gandhinagar) - Oath - Hindi Shrimati Sonia Gandhi (Rae Bareli) - Affirmation - Hindi HON. SPEAKER : Now I request the Secretary-General to call the names. SECRETARY GENERAL: Now panel of Chairpersons. PANEL OF CHAIRPERSONS 1. Shri Arjun Charan Sethi (Bhadrak) - Oath - English 2. Shri Purno Agitok Sangma (Tura) - Oath - English 3. Shri Biren Singh Engti (Autonomous - Oath - English District) CABINET MINISTERS 4. Shri Raj Nath Singh (Lucknow) - Oath - Hindi 5. Shrimati Sushma Swaraj (Vidisha) - Oath - Sanskrit 6. Shri Nitin Jairam Gadkari (Nagpur) - Oath - Hindi 7. Shri D.V. Sadananda Gowda - Oath - Kannada (Bangalore North ) 8. Ms. Uma Bharti (Jhansi) - Oath - Sanskrit 9. Shri Ramvilas Paswan (Hajipur) - Affirmation - Hindi 10. Shri Kalraj Mishra (Deoria) - Oath - Hindi 11. 12. Shrimati Maneka Sanjay Gandhi - Oath - English (Pilibhit) Shri Ananth Kumar (Bangalore South) - Oath - Kannada 13. Shri Ashok Gajapathi Raju Pusapati - Oath - Hindi (Vizianagaram) 14. Shri Anant Geete (Raigad) - Oath - Hindi 15. Shrimati Harsimrat Kaur Badal - Oath - Punjabi (Bathinda) 16. Shri Narendra Singh Tomar (Gwalior) - Oath - Hindi 17. Shri Jual Oram (Sundargarh) - Oath - Odia 18. Shri Radha Mohan Singh (Purvi - Oath - Hindi Champaran) 19. Dr. Harsh Vardhan (Chandni Chowk) - Oath - Sanskrit MINISTERS OF STATES (Independent Charge) 20. General (Retd.) Vijay Kumar Singh - Oath - Hindi (Ghaziabad) 21. Shri Rao Inderjit Singh (Gurgaon) - Oath - Hindi 22. Shri Santosh Kumar Gangwar (Bareilly) - Oath - Hindi 23. -

PENDING POSITION of MATTERS RAISED UNDER RULE 377 in SIXTEENTH LOK SABHA AS on 10.01.2017 Sl. No. Ministries Pending Matter

PENDING POSITION OF MATTERS RAISED UNDER RULE 377 IN SIXTEENTH LOK SABHA AS ON 10.01.2017 Sl. Ministries Pending No. matters 1. Ministry of Agriculture and Farmers Welfare 39 2. Ministry of Ayush 06 3. Ministry of Chemicals and Fertilizers 20 4. Ministry of Civil Aviation 07 5. Ministry of Coal 09 6. Ministry of Commerce and Industry 15 7. Ministry of Communications and Information Technology 23 8. Ministry of Consumer Affairs, Food and Public Distribution 11 9. Ministry of Corporate Affairs 01 10. Ministry of Culture 15 11. Ministry of Defence 10 12. Ministry of Development of North Eastern Region 00 13. Ministry Drinking Water Supply and Sanitation 53 14. Ministry of Earth Science 00 15. Ministry of Environment and Forests and Climate Change 97 16. Ministry of External Affairs 02 17. Ministry of Finance 49 18. Ministry of Food Processing Industries 01 19. Ministry Health and Family Welfare 85 20. Ministry of Heavy industries and Public Enterprises 08 21. Ministry of Home Affairs 35 22. Ministry of Housing and Urban and Poverty Alleviation 01 23. Ministry of Human Resources Development 120 24. Ministry of Information and Broadcasting 04 25. Ministry of Labour and Employment 26 26. Ministry of Law and Justice 18 27. Ministry of Micro, Small and Medium Enterprises 04 28. Ministry of Mines 06 29. Ministry of Minority Affairs 01 30. Ministry of New and Renewable Energy 04 31. Ministry of Overseas Indian Affairs 01 32. Ministry of Panchayati Raj 03 33. Ministry of Parliamentary Affairs 01 34. Ministry of Personnel, Public Grievance and Pension 11 35. -

Standing Committee on Defence (2018-2019)

47 STANDING COMMITTEE ON DEFENCE (2018-2019) (SIXTEENTH LOK SABHA) MINISTRY OF DEFENCE [ACTION TAKEN BY THE GOVERNMENT ON THE RECOMMENDATIONS/OBSERVATIONS CONTAINED IN THE FORTY-FIRST REPORT OF STANDING COMMITTEE ON DEFENCE (SIXTEENTH LOK SABHA) ON `DEMANDS FOR GRANTS OF THE MINISTRY OF DEFENCE FOR THE YEAR 2018-19 ON ARMY, NAVY AND AIR FORCE (DEMAND NO. 20)’] FORTY-SEVENTH REPORT LOK SABHA SECRETARIAT NEW DELHI January, 2019/ Pausa, 1940 (Saka) FORTY-SEVENTH REPORT STANDING COMMITTEE ON DEFENCE (2018-2019) (SIXTEENTH LOK SABHA) MINISTRY OF DEFENCE [ACTION TAKEN BY THE GOVERNMENT ON THE RECOMMENDATIONS/OBSERVATIONS CONTAINED IN THE FORTY-FIRST REPORT OF STANDING COMMITTEE ON DEFENCE (SIXTEENTH LOK SABHA) ON `DEMANDS FOR GRANTS OF THE MINISTRY OF DEFENCE FOR THE YEAR 2018-19 ON ARMY, NAVY AND AIR FORCE (DEMAND NO. 20)’] Presented to Lok Sabha on 7.1.2019 Laid in Rajya Sabha on 7.1.2019 LOK SABHA SECRETARIAT NEW DELHI January, 2019/ Pausa, 1940 (Saka) CONTENTS PAGE COMPOSITION OF THE COMMITTEE(2018-19).……………………….....….......... INTRODUCTION..…………………………………………………….….…................... CHAPTER I Report…………………………………………………………………..... CHAPTER II a) Recommendations/Observations which have been accepted by the Government …………………………………….. b) Recommendations/Observations which have been accepted by the Government and commented upon................. CHAPTER III Recommendations/Observations which the Committee do not desire to pursue in view of the replies received from the Government . CHAPTER IV Recommendations/Observations in respect of which replies of Government have not been accepted by the Committee which require reiteration and commented upon ………………….….... CHAPTER V Recommendations/Observations in respect of which Government have furnished interim replies……………………….......... APPENDICES I Minutes of the third Sitting of the Standing Committee on Defence (2018-19) held on 04.01.2019…………….................... -

Dlvmc-Order-New.Pdf

Members of Parliament (16th Lok Sabha) Nominated as Chairman/ Co-chairman to the District Vigilance & Monitoring Committees ANDHRA PRADESH District Member of Parliament Chairman/Co-Chairman Shri Kristappa Nimmala Chairman Anantapur Shri J.C. Divakar Reddy Co-Chairman Dr. Naramalli Sivaprasad Chairman Chittoor Shri Midhun Reddy Co-Chairman Dr. Vara Prasadarao Velagapalli Co-Chairman Shri Murali Mohan Maganti Chairman Shri Narasimham Thota Co-Chairman East Godavari Dr. Ravindra Babu Pandula Co-Chairman Smt. Geetha Kothapalli Co-Chairperson Shri Rayapati Sambasiva Rao Chairman Guntur Shri Jayadev Galla Co-Chairman Shri Sriram Malyadri Co-Chairman Shri Y. S. Avinash Reddy Chairman Kadapa Shri Midhunn Reddy Co-Chairman Shri Konakalla Narayana Rao Chairman Krishna Shri Srinivas Kesineni Co-Chairman Shri Venkateswara Rao Magantti Co-Chairman Shri S.P.Y. Reddey Chairman Kurnool Smt. Renuka Butta Co-Chairperson Shri Mekapati Rajamohan Reddy Chairman Nellore Dr. Vara Prasadarao Velagapalli Co-Chairman Shri Yerram Venkata Subbareddy Chairman Prakasam Shri Sriram Malyadri Co-Chairman Shri Mekpati Rajamohan Reddy Co-Chairman Shri Ashok Gajapati Raju Pusapati Chairman Srikakulam Shri Kinjarapu Ram Mohan Naidu Co-Chairman Smt. Geetha Kothapalli Co-Chairperson Smt. Geetha Kothapalli Chairperson Vishakhapatnam Shri Muthamsetti Srinivasa Rao (Avnthi) Co-Chairman Shri. Hari Babu Kambhampati Co-Chairman Shri Ashok Gajapati Raju Pusapati Chairman Vizianagaram Dr. Hari Babu Kambhampati, Co-Chairman Smt. Geetha Kothapalli Co-Chairperson Shri Venkateswara Rao -

Lok Sabha and Rajya Sabha) Serving in NWR Jurisdiction

A List of Hon'ble Member of Parliament (Lok Sabha and Rajya Sabha) serving in NWR Jurisdiction Sr. Name LS/RS/ Party Delhi Address Permanent Address Contact No. Remarks No. Constituency Name AJMER DIVISION 1 Sh. Arjunlal Meena LS/Udaipur BJP Meenakshi Gas Service, 94141-61766 Post Salumbar, Distt 86969-07766 Udaipur 02906-231380 2 Sh. Chandra LS/Chittorgarh BJP 78, Love Kush Nagar, 98296-29541 Prakash Joshi Madhuban, Chittorgarh 94141-11371 94143-11439 3 Sh. Dipsinh LS/Sabarkantha BJP Shankarsinh Rathod 4 Sh. Haribhai LS/ Banaskantha BJP Taluka Palanpur 09426502727 Parthibhai Distt. Banaskantha Chaudhary ACP FTO Jagavana 385001 5 Sh. Hariom Singh LS/Rajsamand BJP C/o Maheshji Paliwal, 94141-72267 Rathore Jila Mahamantri BJP, Hariom Bhawan, Kankroli, Rajsamand 6 Sh. Jayshreeben LS/ Mahesana BJP 2, Shanti Kadam 09426518880 Kanubhai Patel Motera Cross Road Distt Mehsana 7 Sh. Manshankar LS/Banswara BJP Sh. Omji Paliwal, C/o 29, 99281-16783 Ninama Nagar Palika Market, Banswara 8 Sh. Sanwar Lal Jat LS/Ajmer BJP 4/220, FFS Agrawal 94140-07821 Common with Farm, Mansarovar, Jaipur Division also Jaipur 9 Sh. Subhash LS/Bhilwara BJP A-80, Subhash Nagar, 98290-46344 Baheria Bhilwara 01482-239779 10 Sh. Bhupender RS/Ajmer BJP 4, Meena Bagh, 191-C-II, Kundan Nagar, 09013181076, Common with Yadav Maulana Azad Ajmer, Rajasthan - 9811227300 Jaipur Division also Road, New Delhi- 305001 0145-2624854 110001 011-23063117 011-23063092(F) 11 Sh. Madhusudan RS/ Banaskantha Mistry 12 Sh. V.P. Singh RS/ Bhilwara BJP 301, Brahmputra Jalmahal, Badnor, Teh- 9414300400 Common with Badnore Apartments, Dr. B.D. Asind, Dist. -

Nationallistofmpsnominatedasc

Members of Parliament (16th Lok Sabha) Nominated as Chairman/ Co-chairman to the District Vigilance & Monitoring Committees ANDHRA PRADESH District Member of Parliament Chairman/Co-Chairman Shri Kristappa Nimmala Chairman Anantapur Shri J.C. Divakar Reddy Co-Chairman Dr. Naramalli Sivaprasad Chairman Chittoor Shri Midhun Reddy Co-Chairman Dr. Vara Prasadarao Velagapalli Co-Chairman Shri Murali Mohan Maganti Chairman Shri Narasimham Thota Co-Chairman East Godavari Dr. Ravindra Babu Pandula Co-Chairman Smt. Geetha Kothapalli Co-Chairperson Shri Rayapati Sambasiva Rao Chairman Guntur Shri Jayadev Galla Co-Chairman Shri Sriram Malyadri Co-Chairman Shri Y. S. Avinash Reddy Chairman Kadapa Shri Midhunn Reddy Co-Chairman Shri Konakalla Narayana Rao Chairman Krishna Shri Srinivas Kesineni Co-Chairman Shri Venkateswara Rao Magantti Co-Chairman Shri S.P.Y. Reddey Chairman Kurnool Smt. Renuka Butta Co-Chairperson Shri Mekapati Rajamohan Reddy Chairman Nellore Dr. Vara Prasadarao Velagapalli Co-Chairman Shri Yerram Venkata Subbareddy Chairman Prakasam Shri Sriram Malyadri Co-Chairman Shri Mekpati Rajamohan Reddy Co-Chairman Shri Ashok Gajapati Raju Pusapati Chairman Srikakulam Shri Kinjarapu Ram Mohan Naidu Co-Chairman Smt. Geetha Kothapalli Co-Chairperson Smt. Geetha Kothapalli Chairperson Vishakhapatnam Shri Muthamsetti Srinivasa Rao (Avnthi) Co-Chairman Shri. Hari Babu Kambhampati Co-Chairman Shri Ashok Gajapati Raju Pusapati Chairman Vizianagaram Dr. Hari Babu Kambhampati, Co-Chairman Smt. Geetha Kothapalli Co-Chairperson Shri Venkateswara Rao -

Government of India Ministry of Statistics and Programme Implementation

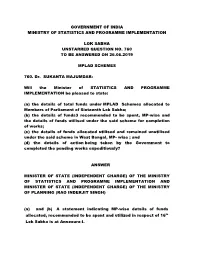

GOVERNMENT OF INDIA MINISTRY OF STATISTICS AND PROGRAMME IMPLEMENTATION LOK SABHA UNSTARRED QUESTION NO. 760 TO BE ANSWERED ON 26.06.2019 MPLAD SCHEMES 760. Dr. SUKANTA MAJUMDAR: Will the Minister of STATISTICS AND PROGRAMME IMPLEMENTATION be pleased to state: (a) the details of total funds under MPLAD Schemes allocated to Members of Parliament of Sixteenth Lok Sabha; (b) the details of funds3 recommended to be spent, MP-wise and the details of funds utilised under the said scheme for completion of works; (c) the details of funds allocated utilised and remained unutilised under the said scheme in West Bengal, MP- wise ; and (d) the details of action being taken by the Government to completed the pending works expeditiously? ANSWER MINISTER OF STATE (INDEPENDENT CHARGE) OF THE MINISTRY OF STATISTICS AND PROGRAMME IMPLEMENTATION AND MINISTER OF STATE (INDEPENDENT CHARGE) OF THE MINISTRY OF PLANNING (RAO INDERJIT SINGH) (a) and (b) A statement indicating MP-wise details of funds allocated, recommended to be spent and utilized in respect of 16th Lok Sabha is at Annexure-I. (c) A statement indicating MP-wise details of funds allocated, utilized and remained unutilized under the MPLAD scheme in West Bengal, is at Annexure- II. (d) The implementation of the MPLADS in the field is undertaken by the District Authorities in accordance with the State Government’s technical, administrative and financial rules. Sanction, rejection and completion of the work are to be done by the District Authorities as per the time line stipulated in MPLADS guidelines. Ministry of Statistics & Programme Implementation holds annual review meeting in addition to regular correspondence with State Government to emphasize timely completion of works and utilization of funds. -

A Case Study of Last Twovidhan Sabha and Lok Sabha Elections in Rajasthan (2013- 2019)

[VOLUME 7 I ISSUE 2 I APRIL- JUNE 2020] e ISSN 2348 –1269, Print ISSN 2349-5138 http://ijrar.com/ Cosmos Impact Factor 4.236 HACKING OF EVMS- A MYTH OR REALITY? A CASE STUDY OF LAST TWOVIDHAN SABHA AND LOK SABHA ELECTIONS IN RAJASTHAN (2013- 2019) Dr. Purnima Singh Assistant Professor in Geography, Government Meera Girls College, Udaipur (Raj.) Received: March 24, 2020 Accepted: May 01, 2020 ABSTRACT: Recently, there has been a controversy surrounding the use of Electronic Voting Machines (EVMs) in elections in India in last 10-15 years. Some of the defeated Candidates and losing parties allege of tempering or hacking of EVMs for their lose and demand the use of ballot papers instead of EVMs for voting in elections. This type of demand has raised confusion in minds of the voters regarding tempering and hacking of EVMs. This suspicion has been taken as hypothesis in this paper and it has been tested by analysing the votes received by winner and nearest rival candidates in last two Lok Sabha and Vidhan Sabha elections in Rajasthan through EVM and through postal ballot papers. The probable results with only postal ballot papers count were compared with the votes received through EVMs. The data was analysed and it was found that there was almost negligible or no difference in results obtained from proportion of votes received through EVMs and those through postal ballot paper and central and state governments were not found to influence the election results. Key Words: Electronic Voting Machines (EVMs), Postal Ballot Paper, Electronic Transfer of Ballot Paper System (ETPBS), Voting, Elections, Lok Sabha, Vidhan Sabha.