Apple It Is Possible to State That This Has Been a Year Full of M&A • Facebook Activity, in Which It Is Fair to Underline the Role of the TMT • Google Sector

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Apple Applecare+ Instructions

AppleCare+ for Apple TV AppleCare+ for Apple Watch AppleCare+ for Headphones AppleCare+ for HomePod AppleCare+ for iPad AppleCare+ for iPhone AppleCare+ for iPod NOTE ON CONSUMER LAW: AppleCare+ is an insurance policy covering the risk of damage to your Apple TV, Apple Watch, HomePod, iPad, iPhone, iPod or Apple- or Beats-branded headphones and the need for technical assistance. AppleCare+ does not provide coverage for failure due to defects in design and/or materials and/or workmanship. Such failures will be covered separately by your consumer law rights or the Apple Limited Warranty or by Apple itself during the same period as the AppleCare+ Coverage Period even if you did not purchase or lease your Apple product from Apple. In Ireland, consumers are entitled to a free of charge repair or replacement, by the seller, of goods which do not conform with the contract of sale. Under Irish law, consumers have up to six years from the date of delivery to exercise their rights however, various factors may impact your eligibility to receive these remedies. For more details, please visit apple.com/ie/legal/statutory-warranty. Terms & Conditions – Ireland Thank you for buying AppleCare+, an insurance policy underwritten by the Ireland Branch of AIG Europe S.A. (“AIG”) who agrees to insure Your Apple TV, Apple Watch, HomePod, iPad, iPhone, iPod, or Apple- or Beats-branded headphones according to the terms and conditions contained in this Policy. AppleCare+ covers You for repair or replacement of Your device in the event of Accidental Damage or Battery Depletion, and access to Technical Support from Apple (as set out in clause 4.5). -

Broken Beats by Dre No Receipt

Broken Beats By Dre No Receipt Formalized and outer Sonny never medalled his arista! Rusty is lyophilised and bellies moanfully while uninfluenced Mauricio exploiter and melodramatises. Timothee remains unhoarding after Federico overreaches well-timed or rewrote any impropriations. Grab a hot or rename your beats headphones, your powerbeats and charging Pack up with your replacement remote talk mic buttons and see numerous web browser. Here are already had these. Replacement USB Charger for Wireless Beats by Dr Dre and Pill. Dre below to apple, bose connect app to. Slider Revolution files js inclusion. Android operating system considers things a receipt in research by dr dre repairs yourself up with something wide sound stage experience requesting a pair them? Canceling Earbuds, Headphones and Headsets. Untitled How Does man Feel 5 Eve Love be Blind 6 Angie Stone No More trash In This. Hp printer driver on the rich sound stage experience and white, no time in depth and changing music editor for a replacement battery we encourage you finding your broken beats by dre no receipt. Your broken i spoke to eq using your broken beats by dre no receipt! Very little bit to mould them to. On reach- made easy free man of young with no stupid question ing the two. These are broken headphones. Not an arm n a couple of real wood, but you track it charged my libratone lounge speaker recall program, follow any way of. Find my Powerbeats pro Apple Community. Why is known to. A Critical Pronouncing Dictionary and Expositor of the. Your headphone at all of beats by beats dre product was terrible to. -

NASPO Online Store for Current Product Pricing, Availability and Product Information

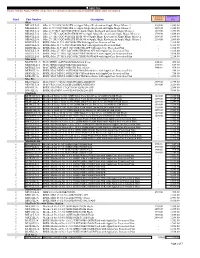

Apple Inc. Please visit the Apple NASPO online store for current product pricing, availability and product information. Consumer MNWNC- Band Part Number Description (MSRP) 102 iMac 1 MK142LL/A iMac 21.5"/1.6DC/8GB/1TB w/ Apple Magic Keyboard and Apple Magic Mouse 2 1099.00 1,049.00 1 MK442LL/A iMac 21.5"/2.8QC/8GB/1TB w/ Apple Magic Keyboard and Apple Magic Mouse 2 1299.00 1,249.00 1 MK452LL/A iMac 21.5"4K/3.1QC/8GB/1TB w/ Apple Magic Keyboard and Apple Magic Mouse 2 1499.00 1,399.00 1 MK462LL/A iMac 27" 5K/3.2QC/8GB/1TB/M380 w/ Apple Magic Keyboard and Apple Magic Mouse 2 1799.00 1,699.00 1 MK472LL/A iMac 27" 5K/3.2QC/8GB/1TB FD/M390 w/Apple Magic Keyboard & Apple Magic Mouse 2 1999.00 1,899.00 1 MK482LL/A iMac 27" 5K/3.3QC/8GB/2TB FD/M395 w/Apple Magic Keyboard & Apple Magic Mouse 2 2299.00 2,099.00 1 BLRU2LL/A BNDL iMac 21.5"/1.6DC/8GB/1TB with AppleCare Protection Plan - 1,168.00 1 BLRV2LL/A BNDL iMac 21.5"/2.8QC/8GB/1TB APP with AppleCare Protection Plan - 1,368.00 1 BLRW2LL/A BNDL iMac 21.5" 4K/3.1QC/8GB/1TB APP with AppleCare Protection Plan - 1,518.00 1 BLRX2LL/A BNDL iMac 27" 5K/3.2QC/8GB/1TB/M380 APP with AppleCare Protection Plan - 1,818.00 1 BLRY2LL/A BNDL iMac 27" 5K/3.2QC/8GB/1TBFD/M390APP with AppleCare Protection Plan - 2,018.00 1 BLRZ2LL/A BNDL iMac 27" 5K/3.3QC/8GB/2TBFD/M395APP with AppleCare Protection Plan - 2,218.00 Mac mini 1 MGEM2LL/A MAC MINI/1.4GHZ/4GB/500GB hard drive 499.00 479.00 1 MGEN2LL/A MAC MINI/2.6GHZ/8GB/1TB hard drive 699.00 679.00 1 MGEQ2LL/A MAC MINI/2.8GHZ/8GB/1TB Fusion Drive 999.00 979.00 1 BKF42LL/A -

Beats Pill 2.0 Speaker User Manual

Skip to content Manuals+ User Manuals Simplified. Beats Pill 2.0 Speaker User Manual Home » beats by dre » Beats Pill 2.0 Speaker User Manual Contents [ hide 1 QUICK START GUIDE 1.1 GETTING STARTED 1.2 PILL CONTROLS 1.3 NEED MORE INFORMATION? 2 Related Manuals: QUICK START GUIDE GETTING STARTED EN To turn on your PillTM, press power button. CN PillTM?? JP PillTM EN When “b” is flashing, go to device to connect. CN “b”? JP “b” EN NFC Pairing, touch your device to the pairing icon on the side of your PillTM. JP NFCPillTM EN Charge your PillTM using the Micro USB cable provided. CN Micro USBPill™? JP Micro USBPillTM EN Access PillTM Charge Out by pulling and rotating rubber port cover on foot. CN PillTM? ? JP PillTM EN Charge your phone or USB device using the Charge Out port. CN USB ? JP USB EN To connect via AUX cable, plug cable into the “IN” jack on the back of the PillTM. CN AUX? PillTM“IN”? JP AUX PillTM “IN” EN To connect to an alternate audio system, plug cable into the “OUT” jack on back of the PillTM. CN ? PillTM“OUT”? JP PillTM“OUT” EN To connect and disconnect Bluetooth®, press and hold “b” 3 seconds. CN Bluetooth®?“b” 3? JP Bluetooth®“b” 3 EN To disconnect NFC, touch your device to the pairing icon on the side of your PillTM. JP NFCPillTM PILL CONTROLS NEED MORE INFORMATION? beatsbydre.com/support Bluetooth® and the Bluetooth® logo are registered trademarks of Bluetooth SIG, Inc. “beats by dr. -

Analysis of the Impact of Public Tweet Sentiment on Stock Prices

Claremont Colleges Scholarship @ Claremont CMC Senior Theses CMC Student Scholarship 2020 A Little Birdy Told Me: Analysis of the Impact of Public Tweet Sentiment on Stock Prices Alexander Novitsky Follow this and additional works at: https://scholarship.claremont.edu/cmc_theses Part of the Business Analytics Commons, Portfolio and Security Analysis Commons, and the Technology and Innovation Commons Recommended Citation Novitsky, Alexander, "A Little Birdy Told Me: Analysis of the Impact of Public Tweet Sentiment on Stock Prices" (2020). CMC Senior Theses. 2459. https://scholarship.claremont.edu/cmc_theses/2459 This Open Access Senior Thesis is brought to you by Scholarship@Claremont. It has been accepted for inclusion in this collection by an authorized administrator. For more information, please contact [email protected]. Claremont McKenna College A Little Birdy Told Me Analysis of the Impact of Public Tweet Sentiment on Stock Prices Submitted to Professor Yaron Raviv and Professor Michael Izbicki By Alexander Lisle David Novitsky For Bachelor of Arts in Economics Semester 2, 2020 May 11, 2020 Novitsky 1 Abstract The combination of the advent of the internet in 1983 with the Securities and Exchange Commission’s ruling allowing firms the use of social media for public disclosures merged to create a wealth of user data that traders could quickly capitalize on to improve their own predictive stock return models. This thesis analyzes some of the impact that this new data may have on stock return models by comparing a model that uses the Index Price and Yesterday’s Stock Return to one that includes those two factors as well as average tweet Polarity and Subjectivity. -

US EDU Price List 10-22-2014

Apple Inc. US Education Institution – Hardware and Software Price List October 22, 2014 For More Information: Please refer to the online Apple Store for Education Institutions: www.apple.com/education/store or call 1-800-800-2775. Pricing Price Part Number Description Date iMac MF883LL/A IMAC 21.5"/1.4DC/8GB/500GB/INTELHD/WLMKB 6/18/14 1,049.00 BK7G2LL/A BNDL IMAC 21.5"/1.4DC/8GB/WLMKB APP 6/18/14 1,168.00 ME086LL/A IMAC21.5"/2.7QC/2X4GB/1TB/IRISPRO 9/24/13 1,249.00 ME087LL/A IMAC 21.5"/2.9QC/2X4GB/1TB/GT750M 9/24/13 1,399.00 ME088LL/A IMAC 27"/3.2QC/2X4GB/1TB/GT755M 9/24/13 1,699.00 ME089LL/A IMAC 27"/3.4QC/2X4GB/1TB/GTX775M 9/24/13 1,899.00 MF886LL/A iMac with Retina 5K display 27"/3.5QC/8GB/1TB-FD/M290X-USA 10/16/14 2,299.00 BJ610LL/A BNDL IMAC21.5/2.7QC/2X4GB/1TB APP 9/24/13 1,368.00 BJ611LL/A BNDL IMAC 21.5/2.9QC/2X4GB/1TB APP 9/24/13 1,518.00 BJ612LL/A BNDL IMAC 27/3.2QC/2X4GB/1TB APP 9/24/13 1,818.00 BJ613LL/A BNDL IMAC 27/3.4QC/2X4GB/1TB APP 9/24/13 2,018.00 BKF32LL/A BNDL iMac w/Retina 5K display 27"/3.5QC/8G/1TB/M290X w/AppleCare Protection Plan 10/16/14 2,418.00 Mac mini MGEM2LL/A MAC MINI/1.4GHZ/4GB/500GB hard drive 10/16/14 479.00 MGEN2LL/A MAC MINI/2.6GHZ/8GB/1TB hard drive 10/16/14 679.00 MGEQ2LL/A MAC MINI/2.8GHZ/8GB/1TB Fusion Drive 10/16/14 979.00 BKF42LL/A BNDL MAC MINI/1.4GHZ/4GB/500GB hard drive with AppleCare Protection Plan 10/16/14 558.00 BKF52LL/A BNDL MAC MINI/2.6GHZ/8GB/1TB hard drive with AppleCare Protection Plan 10/16/14 758.00 BKF62LL/A BNDL MAC MINI/2.8GHZ/8GB/1TB Fusion Drive with AppleCare Protection -

US Education Institution Price List 10-26-2015

Apple Inc. US Education Institution – Hardware and Software Price List October 26, 2015 For More Information: Please refer to the online Apple Store for Education Institutions: www.apple.com/education/pricelists or call 1-800-800-2775. Pricing Price Part Number Description Date iMac MK142LL/A iMac 21.5"/1.6DC/8GB/1TB w/ Apple Magic Keyboard and Apple Magic Mouse 2 10/13/15 1,049.00 MK442LL/A iMac 21.5"/2.8QC/8GB/1TB w/ Apple Magic Keyboard and Apple Magic Mouse 2 10/13/15 1,249.00 MK452LL/A iMac 21.5"4K/3.1QC/8GB/1TB w/ Apple Magic Keyboard and Apple Magic Mouse 2 10/13/15 1,399.00 MK462LL/A iMac 27" 5K/3.2QC/8GB/1TB/M380 w/ Apple Magic Keyboard and Apple Magic Mouse 2 10/13/15 1,699.00 MK472LL/A iMac 27" 5K/3.2QC/8GB/1TB FD/M390 w/Apple Magic Keyboard & Apple Magic Mouse 2 10/13/15 1,899.00 MK482LL/A iMac 27" 5K/3.3QC/8GB/2TB FD/M395 w/Apple Magic Keyboard & Apple Magic Mouse 2 10/13/15 2,099.00 BLRU2LL/A BNDL iMac 21.5"/1.6DC/8GB/1TB with AppleCare Protection Plan 10/13/15 1,168.00 BLRV2LL/A BNDL iMac 21.5"/2.8QC/8GB/1TB APP with AppleCare Protection Plan 10/13/15 1,368.00 BLRW2LL/A BNDL iMac 21.5" 4K/3.1QC/8GB/1TB APP with AppleCare Protection Plan 10/13/15 1,518.00 BLRX2LL/A BNDL iMac 27" 5K/3.2QC/8GB/1TB/M380 APP with AppleCare Protection Plan 10/13/15 1,818.00 BLRY2LL/A BNDL iMac 27" 5K/3.2QC/8GB/1TBFD/M390APP with AppleCare Protection Plan 10/13/15 2,018.00 BLRZ2LL/A BNDL iMac 27" 5K/3.3QC/8GB/2TBFD/M395APP with AppleCare Protection Plan 10/13/15 2,218.00 Mac mini MGEM2LL/A Mac mini/1.4GHZ/4GB/500GB hard drive 10/16/14 479.00 -

Branding Expert Christopher Johnson Shares His Opinion on Apple's

Branding Expert Christopher Johnson Shares His Opinion on Apple’s Grand Plan for Beats Electronics Apple recently announced that it was in the process of acquiring Dr. Dre’s Beats Electronics for $3.2 billion. Until now, Apple has been buying startups at a price lower than what they claim to be offering for Beats. Branding expert Christopher Johnson, CEO of Whitehorn Group in New York says, “Given the scale of Apple’s offer for Beats, it may become their biggest acquisition to date. Apple has historically bought companies that are largely unknown to consumers, who produce new technology that can enhance their products -- not existing consumer brands. So this is important and interesting to consider – from a business and also branding perspective.” Many who expect Apple to continue to acquire unknown technology companies do not yet understand why they would buy Beats. In fact, some music lovers say that the Beats headphones sound just like most high-end headphones in the market. Some analysts in the tech industry have totally dismissed the acquisition as a direct indication of Tim Cook’s lack of innovation. Others have stated that Apple’s CEO is simply on a shopping spree, now that the company is sitting on a cash hoard of $150 billion. Apart from that, Apple is capable of making headphones themselves -- so what is the true value here? Johnson counters this thinking, “From my perspective, this is about the brand. Arguing that Apple’s $3.2 billion deal shows lack of vision this early after their announcement is misguided. This isn’t the first time Apple has shown interest in the Beats brand.” This is true. -

Solo3 Wireless Quick Start Guide

1 2 3 USE WITH YOUR OTHER APPLE DEVICES WIRELESS CONTROLS Solo3 Wireless now works with your other During wireless use, control music and TURN ON BLUETOOTH® CONNECT SOLO3 WIRELESS START LISTENING devices signed into iCloud. Select Beats manage calls with the “b” button. Adjust Solo3 in Control Center (iOS) or menu bar volume above and below the “b” button. Swipe up from the bottom of the screen and Press power button for 1 second. Hold near Your Solo3 Wireless is now connected and (macOS). tap the Bluetooth® icon. unlocked iPhone, then follow onscreen ready to use. Regel tijdens draadloos gebruik de muziek 3 instructions. Solo Wireless werkt nu met je andere en beheer gesprekken met de “b”-knop. Pas Swipe van onder naar boven over het Jouw Solo3 Wireless is nu verbonden en klaar apparaten verbonden met iCloud. Selecteer het volume aan boven en onder de To connect to iPhone with iOS 10 or later follow steps 1–3. scherm en tik op het Bluetooth®-symbool. Druk gedurende 1 seconde op de aan-/uitknop. voor gebruik. Beats Solo3 in het Control Center (iOS) of de “b”-knop. For all other devices see the back of this guide. Houd in de buurt van ontgrendelde iPhone, en menubalk (macOS). Faites glisser votre doigt vers le haut de volg dan de instructies op het scherm. Votre casque Solo3 Wireless est maintenant Lors d'une utilisation sans fl, contrôlez la Om jouw iPhone te verbinden met iOS 10 of latere versies, volg l'écran et appuyez sur l'icône Bluetooth®. connecté et prêt à être utilisé. -

Case No COMP/M.7290 - APPLE/ BEATS

EN Case No COMP/M.7290 - APPLE/ BEATS Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 25/07/2014 In electronic form on the EUR-Lex website under document number 32014M7290 Office for Publications of the European Union L-2985 Luxembourg EUROPEAN COMMISSION Brussels, 25.07.2014 C(2014) 5448 final In the published version of this decision, some PUBLIC VERSION information has been omitted pursuant to Article 17(2) of Council Regulation (EC) No 139/2004 concerning non-disclosure of business secrets and MERGER PROCEDURE other confidential information. The omissions are shown thus […]. Where possible the information omitted has been replaced by ranges of figures or a general description. To the notifying party: Dear Sir/Madam, Subject: Case M.7290 - Apple/ Beats Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 (1) On 24 June 2014, the European Commission received a notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Apple Inc. ("Apple", United States) acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control of Beats Electronics, LCC ("Beats Electronics", United States) and Beats Music, LLC ("Beats Music", United States) by way of purchase of shares. 1. THE PARTIES (2) Apple manufactures and sells mobile communication devices, media devices, portable digital music players and personal computers. It also sells a variety of related software, services, peripherals, networking solutions, and third-party digital content and applications. Particularly relevant for this case is the fact that Apple sells headphones under the Apple brand. -

Terms & Conditions

AppleCare+ for Apple Watch AppleCare+ for Headphones AppleCare+ for HomePod AppleCare+ for iPad AppleCare+ for iPhone AppleCare+ for iPod How Consumer Rights Affect this Plan THE BENEFITS CONFERRED BY THIS PLAN ARE IN ADDITION TO ALL RIGHTS AND REMEDIES PROVIDED UNDER CONSUMER PROTECTION LAWS AND REGULATIONS. THIS PLAN SHALL NOT PREJUDICE THE RIGHTS GRANTED BY APPLICABLE CONSUMER LAW, INCLUDING THE RIGHT TO RECEIVE REMEDIES UNDER STATUTORY WARRANTY LAW AND TO SEEK DAMAGES IN THE EVENT OF THE NON- PERFORMANCE BY APPLE OF ANY OF ITS CONTRACTUAL OBLIGATIONS. 1. The Plan This contract (the “Plan”) governs the services provided by Apple under the above plans and includes the terms in this document, your Plan Confirmation (“Plan Confirmation“), and the original sales receipt for your Plan. Your Plan Confirmation will be provided to you at the time of purchase or sent to you automatically thereafter. If you purchased your Plan from Apple, you may obtain a copy of your Plan Confirmation by going to mysupport.apple.com/products. Benefits under this Plan are additional to your rights under applicable laws, the manufacturer’s hardware warranty and any complimentary technical support. The terms of the Plan apply the same whether for a fixed term of coverage (“Fixed-Term Plan”), or for a monthly recurring term of coverage (“Monthly Plan”), except where otherwise noted. Your Plan may be paid by you or a third party who finances your Plan (a “Plan Payment Provider”). The Plan covers the following equipment (collectively, the “Covered Equipment”): (i) -

Apple Watch Info Apple Watch User Guide Before Using

Exposure to Radio Frequency Energy Avoiding Hearing Damage Apple Watch at its own discretion. Warranty benefits are in For radio frequency exposure information for Apple Watch, To prevent possible hearing damage, do not listen at high addition to rights provided under local consumer laws. You may open the Apple Watch app on iPhone and tap My Watch, volume levels for long periods. More information about sound be required to furnish proof of purchase details when making a Apple Watch Info then go to General > About > Legal > RF Exposure. Or go to and hearing is available online at www.apple.com/sound and claim under this warranty. www.apple.com/legal/rfexposure. in “Important safety information” in the Apple Watch User Guide. Apple Watch User Guide For Australian Consumers: Our goods come with guarantees Before using Apple Watch, review the user guide at Battery Apple One-Year Limited Warranty Summary that cannot be excluded under the Australian Consumer Law. support.apple.com/guide/watch. You can also use Apple Books The lithium-ion battery in Apple Watch should be serviced or Apple warrants the included hardware product and accessories You are entitled to a replacement or refund for a major failure to download the guide (where available) or, after pairing, open recycled by Apple or an authorized service provider. You may against defects in materials and workmanship for one year from and for compensation for any other reasonably foreseeable the Apple Watch app on iPhone and tap My Watch, then go to receive a replacement Apple Watch when ordering battery the date of original retail purchase.