Bankislami Annual 2013.FH10

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

S# BRANCH CODE BRANCH NAME CITY ADDRESS 1 24 Abbottabad

BRANCH S# BRANCH NAME CITY ADDRESS CODE 1 24 Abbottabad Abbottabad Mansera Road Abbottabad 2 312 Sarwar Mall Abbottabad Sarwar Mall, Mansehra Road Abbottabad 3 345 Jinnahabad Abbottabad PMA Link Road, Jinnahabad Abbottabad 4 131 Kamra Attock Cantonment Board Mini Plaza G. T. Road Kamra. 5 197 Attock City Branch Attock Ahmad Plaza Opposite Railway Park Pleader Lane Attock City 6 25 Bahawalpur Bahawalpur 1 - Noor Mahal Road Bahawalpur 7 261 Bahawalpur Cantt Bahawalpur Al-Mohafiz Shopping Complex, Pelican Road, Opposite CMH, Bahawalpur Cantt 8 251 Bhakkar Bhakkar Al-Qaim Plaza, Chisti Chowk, Jhang Road, Bhakkar 9 161 D.G Khan Dera Ghazi Khan Jampur Road Dera Ghazi Khan 10 69 D.I.Khan Dera Ismail Khan Kaif Gulbahar Building A. Q. Khan. Chowk Circular Road D. I. Khan 11 9 Faisalabad Main Faisalabad Mezan Executive Tower 4 Liaqat Road Faisalabad 12 50 Peoples Colony Faisalabad Peoples Colony Faisalabad 13 142 Satyana Road Faisalabad 585-I Block B People's Colony #1 Satayana Road Faisalabad 14 244 Susan Road Faisalabad Plot # 291, East Susan Road, Faisalabad 15 241 Ghari Habibullah Ghari Habibullah Kashmir Road, Ghari Habibullah, Tehsil Balakot, District Mansehra 16 12 G.T. Road Gujranwala Opposite General Bus Stand G.T. Road Gujranwala 17 172 Gujranwala Cantt Gujranwala Kent Plaza Quide-e-Azam Avenue Gujranwala Cantt. 18 123 Kharian Gujrat Raza Building Main G.T. Road Kharian 19 125 Haripur Haripur G. T. Road Shahrah-e-Hazara Haripur 20 344 Hassan abdal Hassan Abdal Near Lari Adda, Hassanabdal, District Attock 21 216 Hattar Hattar -

List of Branches Authorized for Overnight Clearing (Annexure - II) Branch Sr

List of Branches Authorized for Overnight Clearing (Annexure - II) Branch Sr. # Branch Name City Name Branch Address Code Show Room No. 1, Business & Finance Centre, Plot No. 7/3, Sheet No. S.R. 1, Serai 1 0001 Karachi Main Branch Karachi Quarters, I.I. Chundrigar Road, Karachi 2 0002 Jodia Bazar Karachi Karachi Jodia Bazar, Waqar Centre, Rambharti Street, Karachi 3 0003 Zaibunnisa Street Karachi Karachi Zaibunnisa Street, Near Singer Show Room, Karachi 4 0004 Saddar Karachi Karachi Near English Boot House, Main Zaib un Nisa Street, Saddar, Karachi 5 0005 S.I.T.E. Karachi Karachi Shop No. 48-50, SITE Area, Karachi 6 0006 Timber Market Karachi Karachi Timber Market, Siddique Wahab Road, Old Haji Camp, Karachi 7 0007 New Challi Karachi Karachi Rehmani Chamber, New Challi, Altaf Hussain Road, Karachi 8 0008 Plaza Quarters Karachi Karachi 1-Rehman Court, Greigh Street, Plaza Quarters, Karachi 9 0009 New Naham Road Karachi Karachi B.R. 641, New Naham Road, Karachi 10 0010 Pakistan Chowk Karachi Karachi Pakistan Chowk, Dr. Ziauddin Ahmed Road, Karachi 11 0011 Mithadar Karachi Karachi Sarafa Bazar, Mithadar, Karachi Shop No. G-3, Ground Floor, Plot No. RB-3/1-CIII-A-18, Shiveram Bhatia Building, 12 0013 Burns Road Karachi Karachi Opposite Fresco Chowk, Rambagh Quarters, Karachi 13 0014 Tariq Road Karachi Karachi 124-P, Block-2, P.E.C.H.S. Tariq Road, Karachi 14 0015 North Napier Road Karachi Karachi 34-C, Kassam Chamber's, North Napier Road, Karachi 15 0016 Eid Gah Karachi Karachi Eid Gah, Opp. Khaliq Dina Hall, M.A. -

Karachi Central 2000 (Old Photocopy)

ARCHIVES DAP‐NEDUET 12‐Jan‐15 REPORT CATALOGUE Call No. Author / Editor Title RO‐0001 District Municipal Corporation (DMC) Proposed Karachi (Uniform) Advertisement Signage Bye Laws Karachi Central 2000 (Old Photocopy) RO‐0002 Australian Social & Economic Rights Community Perspectives Australia’s Compliance with the Un Project (ASERP) Covenant on Economic Social & Cultural Rights RO‐0003 Governor of Sindh's "Panel of Experts" Karachi Building & Town Planning Regulations‐2000 RO‐0004 Governor of Sindh's "Panel of Experts" Karachi Building & Town Planning Regulations‐2000 (Book 2 Forms) RO‐0005 PCATP PCATP: Handbook RO‐0006 Philip Lall Economic Impact of Constitutional & Political Crisis, 1993 RO‐0007 Edward Mcfarlan III Shelter & Working Class Communities: Community Initiated Housing Development in the North End RO‐0008 India‐Pakistan Conference on the Environment December 13‐15, 1989 at Lahore, Pakistan (Vol 1) RO‐0009 India‐Pakistan Conference on the Environment December 13‐15, 1989 at Lahore, Pakistan (Vol 2) RO‐0010 Larkana Package Schemes; Project Breif RO‐0011 Kenneth Fernandes Forced Evictions & Housing Right Abuses in Asia (2nd Report 1996‐97) RO‐0012 Research Centre for Islamic History, Mostar 2004 Workshop Report 1997 Art & Culture (IRCICA) Istanbul RO‐0013 Noman Ahmed Socio‐Economic Profile of the Rural Environs of Madinat‐Al‐ Hikmah Deh Bund Murd Khan Karachi RO‐0014 Monsoon Tree Planting Compaign 2010 RO‐0015 State Bank of Pakistan Annual Report 2000‐2001 RO‐0016 Technical Sanction: NWFP Urban Development Project (NUDP) Page 1 of 55 ARCHIVES DAP‐NEDUET 12‐Jan‐15 REPORT CATALOGUE Call No. Author / Editor Title RO‐0017 Akbar Zaidi From The Lane to the City: The Impact of the Orangi Pilot Project's Low Cost Sanitation Model (A Water Aid Report) RO‐0018 Delft University of Technology Annual Report 1999 Dut Management Centre for International Cooperation RO‐0019 (ICMA) International City/County IQ Service Report Vol. -

Branch Directory

Dubai Islamic Bank - Branch Directory Abbottabad S.No Branch Code Branch Name Address Province PABX Number Khyber 1 31 Abbottabad CB 306/4, Lala Rukh Plaza, Mansehra Road, Abbottabad, Pakhtunkhwa 0992-342239-41 Ground Floor, Shop Nos.12 & 13, Mamu Jee Market, Opp GPO, Cantt Khyber 2 161 Abbottabad 2 Bazaar, Abbottabad, Pakhtunkhwa 0992-342394 Attock S.No Branch Code Branch Name Address Province PABX Number Plot No B-1-63, A Block, Khan Plaza, Fawara Chowk, Civil Bazaar, Attock. 3 73 Attock Punjab. Punjab 057-2702054-6 Mehria Town Housing Scheme, Phase 1, Shop No. 25 + 39, Block - A, Kamra 4 187 Mehria Road - Attock Punjab Bahawalpur S.No Branch Code Branch Name Address Province PABX Number Model Town Plot No 12.B, Khewat No 148,Khatooni No.246,General Officer Colony, 062-2889951-3, 5 71 Bahawalpur Model Town B, Bahawalpur,Punjab. Punjab 2889961-3 Burewala S.No Branch Code Branch Name Address Province PABX Number 439/EB, Block C, Al-Aziz Super Market, College Road, Burewala. Vehari 6 95 Burewala District, Punjab. Punjab 067-3772388 Chakwal S.No Branch Code Branch Name Address Province PABX Number Ground Floor, No. 1636, Khewat 323, Opposite Main PTCL Office Main 7 172 Chakwal Talagang Road, Chakwal District, Punjab. Punjab 054-3544115 Chaman S.No Branch Code Branch Name Address Province PABX Number Ground Floor, Haji Ayub Plaza, Plot No. Mall Road, Chaman.Killa Abdullah 8 122 Chaman District, Balochistan . Balochistan 0826-61806-61812 Dadyal S.No Branch Code Branch Name Address Province PABX Number Ground Floor, Khasra No. 552, Moza Mandi, Kacheri Road, Dadyal, District Azad Jammu & 9 120 Dadyal Mirpur Azad Jammu Kashmir. -

Of 8 S# Branch Code Branch Name Branch Adress City/Town 71 165 Gilgit Branch Main Bazar Airport Road Gilgit Gilgit 72 731 Ranai Road, Chillas Shop No

S# Branch Code Branch Name Branch Adress City/Town 1 24 Abbottabad Branch Mansera Road Abbottabad Abbottabad 2 312 Sarwarabad, Abbottabad Sarwar Mall, Mansehra Road Abbottabad Abbottabad 3 345 Jinnahabad, Abbotabad PMA Link Road, Jinnahabad Abbottabad Abbottabad 4 721 Mansehra Road, Abbotabad Lodhi Golden Tower Supply Bazar Mansehra Road Abbottabad Abbottabad 5 721A PMA Kakul Abbottabad IJ-97, Near IJ Check Post, PMA Kakul, Abbottabad. Abbottabad 6 351 Ali Pur Chatha Near Madina Chowk, Ali Pur Chattha Ali Pur Chattha 7 266 Arifwala Plot # 48, A-Block, Outside Grain Market, Arifwala Arifwala 8 197 Attock City Branch Ahmad Plaza Opposite Railway Park Pleader Lane Attock City Attock 9 318 Khorwah, District Badin survey No 307 Main Road Khurwah District Badin Badin 10 383 Badyana Pasrur Road Badyana, District Sialkot. Badyana 11 298 Bagh, AJ&K Kashmir Palaza Hadari Chowk BAGH, Azad Kashmir BAGH AJK 12 201 Bahawalnagar Branch Grain Market Minchanabad Road Bahawalnagar Bahawalnagar 13 305 Haroonabad Plot No 41-C Ghalla Mandi, Haroonabad District Bahawalnagar Bahawalnagar 14 390 Grain Market, Model Town-B, Bahawalpur Plot No. 112/113-B, Model Town-B, Bahawalpur Bahawalpur 15 134 Channi Goth Bahawalpur Uch Road Channi Goth Tehsil Ahmed Pur East Bahawalpur 16 269 UCH Sharif, District Bahawalpur Building # 68-B, Ahmed Pur East Road, Uch Sharif, Distric Bahawalpur Bahawalpur 17 25 Noor Mahal Bahawalpur 1 - Noor Mahal Road Bahawalpur Bahawalpur 18 261 Bahawalpur Cantt Al-Mohafiz Shopping Complex, Pelican Road, Opposite CMH, Bahawalpur Cantt Bahawalpur 19 750 IBB Circular Rd Bhawalpur Khewat No 38 Ground & First floor Aziz House Rafique Sabir Building Circular Road Bahawalpur Bahawalpur 20 258A Bannu Cantt Shop No. -

MEMBERS LIST AS on OCTOBER 17, 2015-Web.Pdf

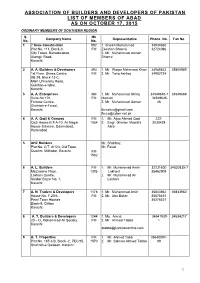

ASSOCIATION OF BUILDERS AND DEVELOPERS OF PAKISTAN LIST OF MEMBERS OF ABAD AS ON OCTOBER 17, 2015 ORDINARY MEMBERS OF SOUTHERN REGION S. Mb Company Name Representative Phone No. Fax No. No. No. 1. 7 Seas Construction 992 1. Sheikh Muhammad 34934660 Plot No. 111, Block-3, FM Zeeshan Shamsi 32724086 City Tower, Bahadurabad, 2. Mr. Muhammad Usman Alamgir Road, Shamsi Karachi. 2. A. A. Builders & Developers 493 1. Mr. Waqar Mehmood Khan 34985842 35800589 1st Floor, Shaes Centre, FM 2. Mr. Tariq Ashfaq 34982724 SB-25, Block-13-C, Main University Road, Gulshan-e-Iqbal, Karachi. 3. A. A. Enterprises 464 1. Mr. Muhammad Ikhlaq 34549645-7 34549669 Suite No.101, FM Memon 34949645- Fortune Centre, 2. Mr. Muhammad Usman 46 Shahrah-e-Faisal, Karachi. [email protected] [email protected] 4. A. A. Qazi & Compay FM 1. Mr. Aijaz Ahmed Qazi 222- Qazi House B # A-10, Ali Nagar 1554 2. Engr. Ghulam Mustafa 2030428 House Scheme, Qasimabad, Abro Hyderabad. 5. AHZ Builders Mr. Shahbaz Plot No. O.T. 8/123, Old Town, Mr. Faisal Quarter, Mithadar, Karachi. FM 1562 6. A. L. Builders FM 1. Mr. Muhammad Amin 32231600 34830835-7 Mezzanine Floor, 1305 Lakhani 35462909 Lakhani Centre, 2. Mr. Muhammad Ali Soldier Bazar No. 1, Lakhani Karachi 7. A. N. Traders & Developers 1178 1. Mr. Muhammad Amin 35833962 35833962 House No. F-20/6, FM 2. Mr. Abu Baker 35875451 Pearl Town Houses 35376521 Block-9, Clifton Karachi. 8. A. T. Builders & Developers 1244 1. Ms. Amna 34541930- 34534217 20 – D, Mohammad Ali Society, FM 2. -

Dubai Islamic Bank (Open Branch List)

Dubai Islamic Bank (Open Branch List) S.No B.Code Open/Close City Branch Name Contact Address 1 031 Open Abbotabad Abbotabad 0992-342239 & 41 Lalarukh Plaza, CB 306/4, Manasehra Road, 2 072 Open AjK North Muzafrabad 05822-921420 & 05822-924136 Main Branch Domail Syedaan Muzaffarabad Azad Jammu & Kashmir 3 120 Open AJK Dadyal Branch 05827-465757-9 DR 05827-465755-56 Ground Floor, Khasra No. 552, Moza Mandi, Kacheri Road, Dadyal, District Mirpur Azad Jammu Kashmir. 4 073 Open Attock Attock 057-2702054 & 5 Plot No B-1-63,A Block,Khan Plaza, Fawara Chowk Civil Bazar, Attock 5 071 Open Bhawalpur Bhawalpur 062-2889961-2 - DR (062-2889951-53) Plot No.12-B,Khewat No. 148,Khatooni No. 246,General Officer Colony, 6 095 Open Burewala Burewala 067-3772386, Al Aziz Super Market College Road - Burewala 7 172 Open Chakwal Chakwal 054-3544117-20 DR- (0543-544115-6) KHASRA# 1536, KHEWAT# 323, OPPOSITE MAIN PTCL OFFICE,TALAGANG ROAD, CHAKWAL 8 041 Open Dalbadin Dalbandin 0825211821-4 Shop No-1, Al Daud Hotel London Road Dalbandin 9 169 Open Dera Gazi Khan Dera Gazi Khan 064-2470981-82 DR (064-2470983) P-7728 ,Block-5 Shop#29,30, Abdullah Center, College Road, Dera Ghazi Khan 10 006 Open Faislabad Kotwali Faislabad 041-2605950,2605945 Plot NO. 05 Liaquat Road, Near State life building, Faisalabad 11 022 Open Faislabad FSD Satiana Road 041-8555601,602 Satiana Road 575-B, People,s Colony Satiana 12 159 Open Faislabad Soson Road 041-8722813-5 PLOT # 27-Z-101, BANK CHOWK, MAIN SUSAN ROAD, FAISALABAD ,PAKISTAN 13 155 Open Gujranwala Faisal Arcade G.T Road Gujranwala 055-4297703 Ground Floor, Faisal Street, Rana Colony, Main G.T. -

Appendix-II Pakistani Scheduled Banks Branches

Appendix-II Pakistani Scheduled Banks Branches Al Baraka Bank (Pakistan) Sukkur Kasur Swabi Ltd. (120) Khanewal Talagang Abbottabad Khanpur (R.Y Khan) Timergara Arifwala Kotri Vehari Attock Zhob Badin Lahore (17) Bahawalnagar -Anarkali Allied Bank Ltd. (998) Bahawalpur -Bank Square Market Abbaspur Burewala -Barkat Market, Garden Town Chichawatni -Cavalry Ground Abbottabad (6) Chistian -Circular Road -Supply Bazar Daska -DHA-Phase-II -The Mall Depalpur -DHA-Phase-VI -Bara Towers, Jinnahabad Dera Ghazi Khan -DHA-S-Block -Murree Road Dera Ismail Khan -Faisal Town -Mansehrah Road Dina -Gulshan Block, Allama Iqbal Town -Pine View Road Ellahabad -Hali Road, Gulberg II -M.M. Alam Road, Gulberg-III Adda Farid Nagar Faisalabad (2) -Maclod Road Adda Johal -Civil Line -Shadman Adda Nandi Pur -Chiniot Bazar -Shadman Colony Adda Zakhera -Shaukat Khanum Road Ahmed Pur East Fateh Jhang -Urdu Bazar Akalgarh (AK) Akhora Khatak Gujranwala (2) Larkana Akwal (Talagang) -Anwar Industrial Complex Mailsi Ali Pur -Main G.T. Road Mansehra Alipur Chatha Mardan Arifwala Gilgit Mian Channu Attock Gojra Minawali Bagh (AK) Gujrat Mingora Hafizabad Mirpur (AK) Bahawalnagar (3) Haripur Mirpurkhas -Jail Road, -Main Raod Hyderabad (2) Multan (3) -Minchin Abad Road -Saddar -Abdali Road -Market Area, -Kaswar Gardezi Road Bahawalpur (8) -Mushahid Trade Centre -Model Town B Haroonabad -New Grain Market Muzzaffarabad -Satellite Town Islamabad (4) Okara -Dubai Chowk, Ahmedpur Road -Blue Area, -One Unit Chowk -F-10 Markaz, Peshawar (3) -Circular Road -Jinnah Avenue -Hayatabad -

Company Profile

Table of Contents Introduction ............................................................................................................................................................... 3 Scope of Services ...................................................................................................................................................... 5 Designing Scope: ................................................................................................................................................... 5 Technical Studies & Reports ................................................................................................................................. 5 Project Documentation .......................................................................................................................................... 6 Engineering Estimations & Evaluations ................................................................................................................ 6 Construction Management ..................................................................................................................................... 6 CEO Experience ........................................................................................................................................................ 8 Names of Few Town Houses, Health Centres, Resorts and Commercial Schemes (consulted by IEMA ENGINEERING):................................................................................................................................................... -

98) Noor-E-Rehmat Re

SINDH BUILDING CONTROL AUTHORITY PUBLIC NOTICE Name of the Project: “NOOR-E-REHMAT RESIDENCY” Plot No. 355, BLOCK-7 & 8, C.P. BERAR CHS, KCHS, GULSHAN TOWN, KARACHI The Sindh Building Control Authority hereby informs general public that NOC for Sale & Advertisement of Shops / Residential Flats at above noted project has been issued vide No. SBCA/DD(D-II)/1156/ADV-679/2014, Dated: 25-11-2014 to Mr. Muhammad Hashim Jumani owner of Plot & proprietor of M/s. A.H.S. Builder Builder Lic. No. BL-2868, having its office at Plot No.1/1/1, SR-6, Shahrah-e-Liaquat, Frere Road, Opp. R.K. Square Serai Quarter, Karachi. The Project consists as approved for Basement (Air Raid Shelter + Parking) + Ground (Shops + Building Service Area) + 1st to 8th Floor (Flats) only. As per approved Architectural Concept Plan vide letter No. SBCA/DD-I /Gulshan Town-II/Prop/95/2014/12 Dated: 26-09-2014. The Proposed date of completion: 31-12-2019. License Architect Name: Mr. Ghulam Mohiuddin (Lic. No. AL-01-26) License Engineer Name: Mr. Arif Kassam (Lic. No. SE-06-96) Units offered for sale are as under: - Covered NOS. OF Price in Rs. Flat Category Floors Area in Units “Each Unit” Sq.Ft (Each) A 1st to 7th 07 1475.29 Rs.88,51,740/- A-1 8th 01 1327.17 Rs.79,63,020/- B 1st To 6th 06 881.38 Rs.52,88,280/- B-1 7th & 8th 02 796.38 Rs.47,78,280/- @Rs.15,000/- SHOPS Ground 03 965.00 Per Sq.ft 1 Note: - - Above mentioned prices does not includes documentation / Utilities Connection CE- 1harges/ Floor, Corner, Road Facing Charges etc. -

Branchoperational.Pdf

S# Branch Code Branch Name Branch Adress City 1 24 Abbottabad Branch Mansera Road Abbottabad Abbottabad 2 312 Sarwarabad, Abbottabad Sarwar Mall, Mansehra Road Abbottabad Abbottabad 3 345 Jinnahabad, Abbotabad PMA Link Road, Jinnahabad Abbottabad Abbottabad 4 721 Mansehra Road, Abbotabad Lodhi Golden Tower Supply Bazar Mansehra Road Abbottabad Abbottabad 5 721A PMA Kakul Abbottabad IJ-97, Near IJ Check Post, PMA Kakul, Abbottabad. Abbottabad 6 351 Ali Pur Chatha Near Madina Chowk, Ali Pur Chattha Ali Pur Chattha 7 266 Arifwala Plot # 48, A-Block, Outside Grain Market, Arifwala Arifwala 8 197 Attock City Branch Ahmad Plaza Opposite Railway Park Pleader Lane Attock City Attock 9 318 Khorwah, District Badin survey No 307 Main Road Khurwah District Badin Badin 10 383 Badyana Pasrur Road Badyana, District Sialkot. Badyana 11 298 Bagh, AJ&K Kashmir Palaza Hadari Chowk BAGH, Azad Kashmir BAGH AJK 12 201 Bahawalnagar Branch Grain Market Minchanabad Road Bahawalnagar Bahawalnagar 13 305 Haroonabad Plot No 41-C Ghalla Mandi, Haroonabad District Bahawalnagar Bahawalnagar 14 25 Noor Mahal Bahawalpur 1 - Noor Mahal Road Bahawalpur Bahawalpur 15 134 Channi Goth Bahawalpur Uch Road Channi Goth Tehsil Ahmed Pur East Bahawalpur 16 261 Bahawalpur Cantt Al-Mohafiz Shopping Complex, Pelican Road, Opposite CMH, Bahawalpur Cantt Bahawalpur 17 269 UCH Sharif, District Bahawalpur Building # 68-B, Ahmed Pur East Road, Uch Sharif, Distric Bahawalpur Bahawalpur 18 390 Grain Market, Model Town-B, Bahawalpur Plot No. 112/113-B, Model Town-B, Bahawalpur Bahawalpur 19 750 IBB Circular Rd Bhawalpur Khewat No 38 Ground & First floor Aziz House Rafique Sabir Building Circular Road Bahawalpur Bahawalpur 20 258 Bannu Mir Afzal Khan Plaza, Outside Lucky Gate, Bannu Bannu 21 258A Bannu Cantt Shop No. -

Centralized-Clearing-Branches.Pdf

Annexure Centralized Clearing Branches (Processing By CPU) Branch Branch Name City Branch Address Code Karachi Avari Branch 001 Karachi 242 & 243, Avari Tower Plaza, Staff Lines, Fatima Jinnah Road, Karachi II Chundrigar 008 Karachi Show Room # 4, Business & Finance Centre, I.I. Chundrigar Road, Karachi Clifton 009 Karachi Dubai Islamic Bank Pak Ltd. Hassan Chambers Plot DC-7, Block 7, Clifton Karachi Gulshan 016 Karachi Plot No. 7/FL-6, Block 6, Gulshan-e-Iqbal, Karachi Shahbaz 017 Karachi 31-C, Khayaban-e-Shahbaz, DHA, Phase VI, Karachi Haideri 019 Karachi Plot No D-10, Block –F, North Nazimabad, Karachi. Shaheed-e-Millat 020 Karachi Shop # 1, Dolmen Arcade, Bahadurabad, Shaheed-e-Millat Road, Karachi KATI 024 Karachi ST 4/2, KATI Building, Sector 22, Korangi Industrial Area 26th Street 025 Karachi E-14, 26th Street, Phase V, DHA, Karachi Show room # 12, 13 Progressive Centre, Plot # 30-A, Block-6 Pakistan Employees Shahra-e-Faisal 026 Karachi Housing Society, Shahrah-e-Faisal, Karachi University Road 046 Karachi Shop No. SB-2/I & SB-2/II, Block 13/C, University Road, Gulshan-e-Iqbal, Karachi Auto Market Plaza 047 Karachi Plot No. 37/11, Southern Portion, Sheet No. P.R.I, Preedy Quarters, Karachi Shop No.S-10, S-11,S-12, Plot No.118/1, Cassim Complex, Block 18, Gulistan-e- Gulistan-e-Johar 049 Karachi Jauhar,Karachi. SITE Area 052 Karachi Plot No. B-9/B-3, Ground and Mezzanine Floor, SITE Area, Karachi, Pakistan Nazimabad 054 Karachi Plot No. 15, Row No. 1, Sub Block-B, Block- III, Nazimabad F.B.