River Lift Irrigation. Scheme . in Kolhapur District ·Maharashtra

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Join Director Technical Education Pune

0819 N3 IE -9 lOZILl8 8 --- 9 I OZILIS lndeqlox '3!uq3adlod ~e~epoq~)Lerueg s~3~)ag~I 189 a OE 9 I OZILIX (

SHIVAJI UNIVERSITY, KOLHAPUR Provisional Electoral Roll of Registered Graduates

SHIVAJI UNIVERSITY, KOLHAPUR Provisional Electoral Roll of Registered Graduates Polling Center : 1 Kolhapur District - Chh.Shahu Central Institute of Business Education & Research, Kolhapur Faculty - ARTS AND FINE ARTS Sr. No. Name and Address 1 ADAKE VASANT SAKKAPPA uchgaon kolhapur 416005, 2 ADNAIK DEVRAJ KRISHNAT s/o krishnat adnaik ,891,gaalwada ,yevluj,kolhapur., 3 ADNAIK DEVRAJ KRUSHANT Yevluj Panhala, 4 ADNAIK KRISHNAT SHANKAR A/P-KUDITRE,TAL-KARVEER, City- KUDITRE Tal - KARVEER Dist- KOLHAPUR Pin- 416204 5 AIWALE PRAVIN PRAKASH NEAR YASHWANT KILLA KAGAL TAL - KAGAL. DIST - KOLHAPUR PIN - 416216, 6 AJAGEKAR SEEMA SHANTARAM 35/36 Flat No.103, S J Park Apartment, B Ward Jawahar Nagar, Vishwkarma Hsg. Society, Kolhapur, 7 AJINKYA BHARAT MALI Swapnanjali Building Geetanjali Colony, Nigave, Karvir kolhapur, 8 AJREKAR AASHQIN GANI 709 C WARD BAGAWAN GALLI BINDU CHOUK KOLHAPUR., 9 AKULWAR NARAYAN MALLAYA R S NO. 514/4 E ward Shobha-Shanti Residency Kolhapur, 10 ALAVEKAR SONAL SURESH 2420/27 E ward Chavan Galli, Purv Pavellion Ground Shejari Kasb bavda, kolhapur, 11 ALWAD SANGEETA PRADEEP Plot No 1981/6 Surna E Ward Rajarampuri 9th Lane kolhapur, 12 AMANGI ROHIT RAVINDRA UJALAIWADI,KOLHAPUR, 13 AMBI SAVITA NAMDEV 2362 E WARD AMBE GALLI, KASABA BAWADA KOLHPAUR, 14 ANGAJ TEJASVINI TANAJI 591A/2 E word plot no1 Krushnad colony javal kasaba bavada, 15 ANURE SHABIR GUJBAR AP CHIKHALI,TAL KAGAL, City- CHIKALI Tal - KAGAL Dist- KOLHPUR Pin- 416235 16 APARADH DHANANJAY ASHOK E WARD, ULAPE GALLI, KASABA BAWADA, KOLHAPUR., 17 APUGADE RAJENDRA BAJARANG -

Distribution and Morphodiversity Analysis of Genus Dioscorea from India with Special Reference to Satpura Hilly Ranges and Western Ghat of Maharashtra State, India

SJIF IMPACT FACTOR: 4.110 CRDEEPJournals International Journal of Basic and Applied Sciences Gawande et.al., Vol. 4 No. 3 ISSN: 2277-1921 International Journal of Basic and Applied Sciences Vol. 4. No. 3 2015. Pp. 146-150 ©Copyright by CRDEEP. All Rights Reserved. Full Length Research Paper Distribution and Morphodiversity Analysis of Genus Dioscorea from India with special reference to Satpura Hilly Ranges and Western Ghat of Maharashtra State, India. Prashant Ashokrao Gawande1, Neha V. Nimbhorkar2 and Prashant Vinayakrao Thakare2 1Department of Botany, Sant Gadge Baba Amravati University, Amravati- 444602, Maharashtra State, India. 2Department of Biotechnology, Sant Gadge Baba Amravati University, Amravati- 444602, Maharashtra State, India. Corresponding Author: Prashant Ashokrao Gawande Abstract The genus Dioscorea is commonly known as yam, and the family Dioscoreaceae popularly called the yam family. Seven species, two variety of Dioscorea were investigated for establishment of phylogenetic relationships based on a morphological analysis by using NTSYSPC. Morphological dendrogram reveals two clusters in which species under section Enantiophyllum distributed distantly in the dendrogram. However, section Botryosicyos and Lasiophyton exhibit morphological affinity. The section Opsophyton maintains separate entity and was found to be outgrouped. Key words: Dioscorea, Distribution, Morphology, Phylogenetic analysis. Introduction The state of Maharashtra has 307,713 km2 total geographic area, of which 50,632 km2 (16.45%) is covered by forest (FSI, 2013). In order to conserve biodiversified flora and fauna the government of India has established 29 tiger reserves covering an area of 58,620 km2; 508 wild life sanctuaries covering 1,18,400.76 km2 area and 97 national parks extended over 38,223.89 km2 area. -

09 Chapter 3.Pdf

CHAPTER ID IDENTIFICATION OF THE TOURIST SPOT 3.1The Kolhapur City 3.2 Geographical Location 3.3 History 3.4 Significance of Kolhapur for the Study [A] Aspects and Outlying belts [B] Hill top konkan and the plain [C] Hills [D] Rive [E] Ponds and lakesrs [F] Geology [G] Climate [H] Forests [I] Flora of Kolhapur District [J] Vegetation [K] Grassland [L] Economically important plants [P] Wild Animals [Q] Fishers 3.5 Places of Interest in the selected area and their Ecological Importance. 1. New Palace 2. Rankala Lake 3. The Shalini Palace 4. Town Hall 5. Shivaji University 6. Panctiaganga Ghat 7. Mahalaxmi Temple 8. Temblai Hill Temple Garden 9. Gangawesh Dudh Katta 3.6 Place of Interest around the Kolhapur / Selected area and their ecological importance. 1. Panhala Fort 2. Pawankhind and Masai pathar 3. Vishalgad 4. Gaganbavada / Gagangad 5. Shri Narsobachi Wadi 6. Khirdrapnr: Shri Kopeshwar t«pk 7. Wadi Ratnagh-i: Shri Jyotiba Tmepie 8. Shri BahobaM Temple 9. RaAaatgiii and Dajqror Forest Reserves 10. Dob wade falls 11. Barld Water Fails 12. Forts 13. Ramteeth: 14. Katyayani: 15 The Kaneri Math: 16 Amba Pass 3.7 misceieneoas information. CHAPTER -HI IDENTIFICATION OF THE TOURIST SPOT. The concept of Eco-Tourism means making as little environmental impact as possible and helping to sustain the indigenous populace thereby encouraging, the preservation of wild life and habitats when visiting a place. This is responsible form of tourism and tourism development, which encourages going back to natural products in every aspects of life. It is also the key to sustainable ecological development. -

GIPE-175649-10.Pdf

1: '*"'" GOVERNMENT OF MAIIAitASJRllA OUTLINE· OF · ACTIVITIES For 1977-78 and 1978-79 IRRIGATION DEPARTMENT OUTLINE OF ACTIVITIES 1977-78 AND 1978-79 IRRIGATION DEPARTMENT CONTENTS CHAl'TI!R PAGtiS I. Introduction II. Details of Major and Medium Irrigation Projects 6 Ul. Minor Irrigation Works (State sector) and Lift Irrigation 21 IV. Steps taken to accelerate the pace of Irrigation Development 23 V. Training programme for various Technical and Non-Technical co~ 36 VI. Irrigation Management, Flood Control and ElCiension and Improvement 38 CHAPTER I INTRODUCTION I.· The earstwhile Public Works Department was continued uuaffect~u after Independence in 1947, but on formation of the State ot Maharashtra in 1_960, was divided into two Departments. viz. .(1) Buildings and Communica· ticns Dep4rtment (now named · as ·'Public Works ' and Housing Department) and (ii) Irrigation and Power Department, as it became evident that the Irrigation programme to be t;~ken up would ·need a separate Depart· ment The activities in . both the above Departments have considerably increased since then and have nei:eSllitated expansion of both the Depart ments. Further due t~ increased ·activities of the Irrigation and Power Department the subject <of Power (Hydro only) has since been allotted to Industries,"Energy and· Labour Department. Public Health Engineering wing is transferred to Urban. Development and Public Health Department. ,t2.. The activities o(the Irrigation ·Department can be divided broadly into the following categories :- (i) Major and Medium Irrigation Projects. (u) Minor Irrigation Projects (State Sector). (ii1) Irrigation Management. (iv) Flood Control. tv) Research. .Designs and Training. (vi) Command Area Development. (vii) Lift Irrigation Sc. -

Pre-Feasibility Report

Pre-Feasibility Report Extension of Runway with Blast Pad, RESA, Taxiway, Apron, GSE Area, Isolation Bay, Construction of New Domestic Terminal Building, ATC tower cum Technical Block cum Fire Station and Other Miscellaneous Works at Kolhapur Airport (Maharashtra) Extension of runway with blast pad, RESA, taxiway, Apron, GSE area, isolation bay, construction of new domestic terminal building, ATC tower cum Technical block cum fire station and other Miscellaneous works at Kolhapur Airport (Maharashtra) Chapter - 1 Kolhapur Airport 1.1 Background Kolhapur is an important city in Maharashtra and is known as Dakshin Kashi from ancient time. It is a famous religious place due to Mahalakshmi & Jotiba temples. Kolhapur is seat of Goddess Mahalaxmi and is one of the Shaktipeeths mentioned in India. Kolhapur is world famous for Kolhapuri Chappals as well. The city is situated at a height of 1790 feet above mean sea level and 16-42 North latitude and 74 - 14 East longitude. The city stands on the bank of river Panchaganga, a tributary of the river Krishna. By road, Kolhapur is 228 km south of Pune, 615 km north-west of Bangalore and 530 km west of Hyderabad. The coastal line (western) is only 75 km away from Kolhapur & hence is known as 'Door of Konkan'. The national highway no.4 (Poona-Bangalore Highway) passes through Kolhapur. Kolhapur is having a railway terminal station named "Chhatrapati Shahu Tarminus". 1.1.1 Economy Kolhapur is one of the important economic regions of Maharashtra with its Strong and Historic Heritage, most attractive tourist destinations, well established economic infrastructure, is one of the richest agricultural belt of the country. -

(2015) Shivaji University, Kolhapur

Shivaji University, Kolhapur Register of Registered Graduate (2015) Faculty of ENGINEERING & TECHNOLOGY Registration No. 89801 Registration No. 89809 1 Shri. ABHYANKAR GANGADHAR LAXMAN 9 Shri. ADHYAPAK ANIL AMRIT SHIVAJI NAGAR 108 KRISHNA NIVAS A/P - KUNDGOL 4TH LANE HINDU COLONY DADAR T.T. MUMBAI - 14 DD Dist. DHARWAR Dist. MUMBAI Registration No. 89802 Registration No. 89810 2 Shri. ABHYANKAR GANGADHAR SHANKAR 10 Shri. ADKAR ARUN RAMACHANDRA 40 PRERANA TILAK NAGAR 382 KASBA BARSI V.P.ROAD MUMBAI - 4 Dist. SOLAPUR Dist. MUMBAI Registration No. 89803 Registration No. 89811 3 Shri. ABHYANKAR HEMANT KESHAV 11 Shri. ADKAR SHASHIKANT GOVIND 977 A SATTIKAR LANE 231 NAVI PETH GAON-BHAG JALGAON SANGLI Dist. SANGLI Dist. JALGAON Registration No. 89804 Registration No. 89812 4 Shri. ABHYANKAR PURUSHOTTAM SITARAM 12 Shri. ADMUTHE SUNIL SHANTINATH PATWARDHAN BLOCKS DEPARTMENT OF INSTRUMENTION NEAR WALCHAND COLLEGE OF ENGINEERING P V P INSTITUTE OF TECHNOLOGY VISHRAM BAUG SANGLI BUDHGAON Dist. SANGLI Dist. SANGLI Registration No. 89805 Registration No. 89813 5 Shri. ABHYANKAR SURESH SHRIDHAR 13 Shri. ADNAIK PRAKASH MOHANRAO C/O - S.W.ABHYANKAR 1877/B FLAT NO 2 AMRAPALI KHAPARDE GARDEN APT RAJARAMPURI 8TH LANE AMARAVATI (VIDARBH) KOLHAPUR Dist. AMARAVATI Dist. KOLHAPUR 416008 Registration No. 89806 Registration No. 89814 6 Shri. ADADANDE AKSHAYKUMAR BALASAHEB 14 Shri. ADSUL AKSHAY RAMCHANDRA KARVEER NAGAR HOUSING SOCIETY, PLOT NO 27 B, 1014/29 SAI COLONY AIRPORT ROAD, UJALAIWADI KOLHAPUR APTE NAGAR, KOLHAPUR 416004 Dist. KOLHAPUR Dist. KOLHAPUR Registration No. 89807 Registration No. 89815 7 Shri. ADANI KRISHNAKUMAR DHARAMSHI 15 Shri. ADURE GAUTAM SURESH R.NO. 96 PL NO 45 B/1 LAYOUT NO 1 GITA GRAHA 4 PICKET ROAD BABA JARAG NAGAR MUMBAI - 2 KOLHAPUR - 416007 Dist. -

WATER QUALITY ANALYSIS and SIMULATION of PANCHAGANGA RIVER USING MATLAB Mr

[Mulla* et al., 5(8): August, 2016] ISSN: 2277-9655 IC™ Value: 3.00 Impact Factor: 4.116 IJESRT INTERNATIONAL JOURNAL OF ENGINEERING SCIENCES & RESEARCH TECHNOLOGY WATER QUALITY ANALYSIS AND SIMULATION OF PANCHAGANGA RIVER USING MATLAB Mr. Riyaj K. Mulla* and Mr. Shrikant M. Bhosale Department of Technology, Shivaji University, Kolhapur, India DOI: 10.5281/zenodo.60106 ABSTRACT Panchaganga River is now facing serious problem of pollution and in present situation continuous analysis is needed to control pollution of Panchaganga River. Pollution of Panchaganga River is observed because of disposal of untreated municipal sewage and industrial effluent through various Streams. Time and money for manpower and chemical is needed for continuous sampling work. MATLAB is an interactive software that allows implementation of algorithm, graphics and creation of user interface with other computer languages. MATLAB helps to predict future water quality using present data and helps to save time, manpower and other cost for continuous analysis. Simulation programming techniques are used for model and virtual based experimentation with the help of collected data from field. The simulation environment of river includes several programming techniques, interactive graphic displays and user friendly interface. Simulation helps in environmental research for understanding research problem and helps find out remedial measures on that. There are several software’s available in market for the prediction of river water quality but MATLAB provides easy and convenient user interface in the form of MATLAB GUI (Graphical User Interface). KEYWORDS: MATLAB Software, Panchaganga River, Pollution Control, Simulation, Graphical User Interface. INTRODUCTION India is the most populated country after china which is also facing problem of clean water shortage. -

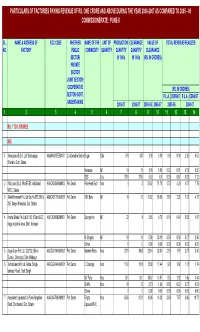

PUNE-II PDF Created with Deskpdf Pdfwriter -Trial:: SL

PARTICULARS OF FACTORIES PAYING REVENUE OF RS. ONE CRORE AND ABOVE DURING THE YEAR 2006-2007 AS COMPARED TO 2005 - 06 COMMISSIONERATE : PUNE-II PDF Created with deskPDF PDFWriter -Trial::http://www.docudesk.com SL. NAME & ADDRESS OF ECC CODE WHETHER NAME OF THE UNIT OF PRODUCTION CLEARANCE VALUE OF TOTAL REVENUE REALIZED NO. FACTORY PUBLIC COMMODITY QUANTITY QUANTITY QUANTITY CLEARANCE SECTOR/ IN '000s IN '000s (RS. IN CRORES) PRIVATE SECTOR JOINT SECTOR/ COOPERATIVE (RS. IN CRORES) SECTOR/ GOVT. P.L.A. CENVAT P.L.A. CENVAT UNDERTAKING 2006-07 2006-07 2005-06 2006-07 2005-06 2006-07 1 2 3 4 5 6 7 8 91011121314 RS. 1 TO 5 CRORES M/S 1 Alinkyatara S.S.K. Ltd. Shahunagar, AAAAA0510EXM001 Co-Operative Sector Sugar Qtls 578 347 0.00 0.00 1.60 0.00 2.35 0.53 Shendre, Distt. Satara Molasses MT 14 15 0.00 0.00 0.72 0.01 0.31 0.83 SDS Ltrs. 3769 3759 5.33 6.8 0.00 0.87 0.00 1.12 2 Alfa Laval (I) Ltd. Plot E7/E8, Additional AAACA5899AXM002 Pvt. Sector Plate Heat Exch. Nos. 4 3 53.62 71.78 4.72 4.20 4.07 7.79 MIDC, Satara 3 Allied Ferromelt Pvt. Ltd Gat No.383,384 & AABCA5179NXM001 Pvt. Sector TMT Bars MT 16 16 31.62 36.09 1.89 3.28 1.73 4.17 385, Sangvi Khandala, Dist. Satara 4 Anshul Steels Pvt. Ltd.B-135, 5 Star MIDC, AAFCA0039BXM001 Pvt. Sector Sponge Iron MT 22 9 3.06 9.75 0.10 0.40 0.52 1.07 Kagal Industrial Area, Distt. -

Panchganga River

REPORT ON ACTION PLAN FOR CLEAN-UP OF POLLUTED STRETCH OF PANCHGANGA RIVER JUNE, 2019 CONTENTS PANCHGANGA RIVER (Shirol to Kolhapur) ................................................................................................. 3 1.1 Executive Summary of Action Plan Restoration of Water Quality of Savitri River .......................... 3 1.2 Background ........................................................................................................................................ 9 1.3 Status of Domestic Sewage Generation and Treatment ................................................................... 12 1.4 Status of Industrial Effluent Generation and Treatment................................................................... 15 1.5 Drains out-falling into River Panchganga ........................................................................................ 19 1.6 Status of Water Quality .................................................................................................................... 22 1.7 Status of Ground Water Quality ....................................................................................................... 24 1.8 Waste Management .......................................................................................................................... 26 1.8.1 Solid Waste Management ......................................................................................................... 26 1.8.2 Bio-medical waste Management ............................................................................................. -

Pages 1 to 54 New

WORKS SPINNING PROJECT R. S. No. 347, Ambapwadi Phata, NH-4, Vadgaon, Tal. Hatkanangale Dist. Kolhapur - 416 112 Phone : ++91- 230-2471230 Fax : ++91- 230-2471229 e-mail – [email protected] WEAVING PROJECT Khotwadi, Opp Parwati Industrial Estate, Ichalkaranji, Dist. Kolhapur WEAVING PROJECT Plot No. T-7, Metro Hi-Tech Co-Op Textile Park, Five Star M.I.D.C Kagal, Dist. Kolhapur HYDRO POWER PROJECT Hydro Power Project, Dam foot Radhanagari Dam, A/p: - Fejiwade, Tal. Radhanagari, Dist. Kolhapur 2 R M MOHITE TEXTILES LTD. 19th Annual Report 2009-2010 Contents Page No. 3 4 R M MOHITE TEXTILES LTD. 19th Annual Report 2009-2010 For and on behalf of Board of Directors, Vadgaon - 416 112 SHIVAJI MOHITE th Date : 17 August, 2010 MANAGING DIRECTOR 5 6 R M MOHITE TEXTILES LTD. 19th Annual Report 2009-2010 7 8 SCHEDULE-5 - FIXED ASSETS Fixed Assets as on 31.03.2010 Rs. in Lacs GROSS BLOCK DEPRECIATION Name of the Gross Block Additions Deductions Gross Block Rate % Depn Depn on Depreciation Total Net Block Net Block Asset As On As On upto Asset For the Year Depn As On As On 01.04.2009 31.03.2010 01.04.2009 Sold 31.03.2010 31.03.2009 Land 57.55 - . - 57.55 - - . - - . - . 57.55 57.55 Kagal MIDC Land 289.43 - . - 289.43 - - . - - . - . 289.43 289.43 Factory Building 2,493.09 106.58 202.52 2,397.15 3.34% 373.56 13.42 83.36 443.50 1,953.65 2,119.53 Plant & Machinery Imported 6,059.87 7.79 - 6,067.66 5.28% 3,323.67 - 320.10 3,643.77 2,423.89 2,736.20 ndigenous 3,010.87 18.94 - 3,029.81 5.28% 1,104.57 - 159.11 1,263.68 1,766.13 1,906.29 Electrical Installation 250.41 1.83 - 252.24 4.75% 77.03 - 11.91 88.94 163.30 173.37 Office Equipment 66.38 4.57 - 70.95 4.75% 26.82 - 3.29 30.11 40.84 39.56 Laboratory Equip. -

Holy City Development Plan a Presentation to Shri Ashokrao Chavan Honourable Chief Minister, Maharashtra

KOLHAPUR: Holy City Development Plan A Presentation to Shri Ashokrao Chavan Honourable Chief Minister, Maharashtra By Kolhapur Municipal Corporation Fortress Structure of the Presentation A About Kolhapur B Kolhapur as a Tourism Destination C Project Outlay and Details D Financial & Implementation Plan Fortress Kolhapur : Location Overview Distances Mumbai : 390 Pune : 233 Bangalore : 614 Belgaum : 105 Goa : 237 Hyderabad : 551 Tirupati :900 Nashik : 435 Aurangabad : 475 Population 35 Lacs Tourists 40 lacs pa Strategically Located on the CorridorsFortress of NH 4 connecting Mumbai, Pune and Bangalore Kolhapur - one of the important economic regions of Maharashtra Strong Historic & Cultural Heritage Most attractive tourism destination Well established Economic infrastructure One of the richest agricultural belt of the country One of the higgpphest per capita income of the countr y One of the highest literate City Æ 90% Strong Education and Health Infrastructure District Population 35.25 Lacs Æ 30% Urban Fortress Kolhapur City – A Brief Profile City Area - 66 sq.kms Population – 5 Lakhs plus Literacy : >90% Economic Drivers Manufacturing, Tourism, Agriculture and Services Central Business Districts Mahadwar Rd, Laxmiopuri, Sahupuri & Rajarampuri Prime Residential Area Tarabai Park, Ruikar Colony, Nagala Park Rajaram Puri & Takala Connectivity Well connected by Rail, Road and Air Fortress Socio- Economic Infrastructure in Kolhapur Important Education destinations in Maharashtra due to • Presence of Shivaji University EDUCATION • District