THE E-BANKING EXPERIENCE Objectives

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Q. How Do I Enroll for Online Banking? A. You May Access Our Website at and in the Top Right Corner There Is an Orange Box for Online Banking

Q. How do I enroll for Online Banking? A. You may access our website at www.guarantystate.com and in the top right corner there is an orange box for Online Banking. Under the User ID box there is a link that says “Enroll for Online Banking”. Clicking the link will open a new webpage where you will be prompted to confirm your identity which must match what we have on file, create your sign-on and review your information. Should you have any problems, don’t hesitate to contact us at any of our locations. Q. Is there a fee for Online Banking? A. No, Online Banking is available free of charge to all Guaranty State Bank & Trust Company customers. Q. Is Online Banking safe? A. Guaranty State Bank & Trust Company uses state-of-the-art firewalls and security to protect client accounts and identities. We do this by: • Using Secured Socket Layer (SSL) data encryption. • Requiring clients to use a browser with 128-bit encryption. • Never displaying Social Security Numbers over the Internet. • Automatically disconnecting Online Banking sessions after 10 minutes of inactivity. • Requiring a unique Online Banking ID and password to be entered before access is granted to account information. • Utilizing a Password Security System. To keep unauthorized individuals from accessing client accounts by guessing their password, we have instituted a password lockout system. If a password is entered incorrectly three consecutive times, the user is “locked out” of the system. • “Out-of-band Authentication” which manages what computer you access your online banking from and should the IP address change, you will be required to enter a 5 digit code that will either be sent by phone call or text message. -

Electronic Bill Payment and Presentment: a Primer

P Electronic Bill Payment and Presentment: A Primer Ann H. Spiotto Federal Reserve Bank of Chicago Emerging Payments Occasional Paper Series December 2001 (EPS-2001-5) FEDERAL RESERVE BANK OF CHICAGO Electronic Bill Payment and Presentment: A Primer Ann H. Spiotto Ann H. Spiotto is senior research counsel with the Emerging Payments Studies Department of the Federal Reserve Bank of Chicago. She previously spent twenty-five years as an attorney for First Chicago Corporation working with its retail banking and credit card operations – during her last ten years at First Chicago she was responsible for the legal work performed for the credit card business. Special thanks to Brian Mantel for his support in reviewing and critiquing this article. The views expressed in this article are those of the author alone and do not necessarily reflect the views of the Federal Reserve Bank of Chicago or the Board of Governors of the Federal Reserve System. The Occasional Paper Series is part of the Federal Reserve Bank of Chicago’s Public Policy Studies series. Address any correspondence about this paper to Ann H. Spiotto, Federal Reserve Bank of Chicago, 230 S. LaSalle Street, Chicago, Illinois 60604 or e-mail Ann at [email protected]. Requests for additional copies should be directed to the Public Information Center, Federal Reserve Bank of Chicago, P.O. Box 834, Chicago, Illinois 60690-0834 or telephone (312) 322- 5111. This paper is available at http://www.chicagofed.org/publications/publicpolicystudies. This paper first appeared in substantially similar form in the November 2001 edition of The Business Lawyer. -

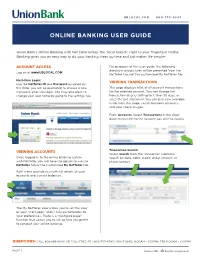

Online Banking User Guide

UBLOCAL.COM 800-753-4343 ONLINE BANKING USER GUIDE Union Bank’s Online Banking with Net Teller brings the “local branch” right to your fi ngertips! Online Banking gives you an easy way to do your banking, frees up time and just makes life simpler. ACCOUNT ACCESS For purposes of this user guide, the following directions and pictures will be presented from the Log on at www.UBLOCAL.COM NetTeller tab, not the customized My NetTeller tab. First-time Login: VIEWING TRANSACTIONS Use the NetTeller ID and Password assigned by the Bank; you will be prompted to choose a new This page displays a list of all account transactions Password after you login. You may also elect to for the selected account. You can change the change your user name by going to the settings tab. transaction display setting to 7, 15 or 30 days, or since the last statement. You can also view available funds from this page, switch between accounts, and view check images. From Accounts, Select Transactions in the drop- down menu next to the account you wish to access. VIEWING ACCOUNTS Transaction Search: Select Search from the Transaction submenu. Once logged-in to the online banking system Search by date, debit, credit, dollar amount, or with NetTeller, you will have the option to use the check number. NetTeller tab or the customized My NetTeller tab. Both views provide you with full details of your accounts and current balances. The My NetTeller view allows you to set this view as your “start page” and is fully customizable to your preferences. -

The Pandemic Is Giving Banks the Opportunity to Create Goodwill With

September 2020 | americanbanker.com Never let a good crisis go to waste — the pandemic is giving banks the opportunity to create goodwill with consumers and our annual survey of bank reputations offers some insight on how to keep the positive momentum going REPUTATION REBOUND ABM0920_Cover_Final.indd 1 8/11/20 2:11 PM Maximize the Value of Your Seniors Housing Loans Welltower (NYSE: WELL), an S&P 500 company, is the largest owner of seniors housing and medical-related real estate assets in the world. Our platform of best-in-class operators, key health care industry relationships, unparalleled data analytics capabilities and access to capital allows us to work alongside and in partnership with you to maximize the value of your seniors housing industry loans (CRE as well as construction loans). We o er solutions to buy your existing loans or to bring in operating partners to turn around existing situations. Please contact us today to explore ways we can partner WELL with you. CONTACT US TODAY Tim McHugh, EVP and CFO Nikhil Chaudhri, VP, Investments [email protected] [email protected] (646) 677-8743 (646) 677-8772 0C2_ABM0920 2 8/12/2020 2:30:18 PM Contents September 2020 | VOL. 130 | NO. 9 REPUTATION SURVEY 14 14 On the rebound Buoyed by its efforts to help consumers and businesses weather the pandemic, the banking industry saw its reputation improve for the first time in several years. Our annual survey offers some insight on how to keep the goodwill flowing. 20 Talking points The coronavirus crisis shows how much crisis communications matter. -

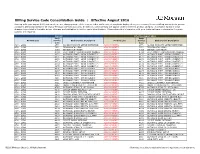

Billing Service Code Consolidation Guide | Effective August 2016

Billing Service Code Consolidation Guide | Effective August 2016 Starting with your August 2016 statement, we are changing some of the service codes and service descriptions displayed on your Treasury Services Billing statement to provide consistent billing standards for all of your Treasury Services accounts. In addition, some services will appear under a different product category. A complete listing of these changes is provided in the table below. Changes are highlighted in red for easier identification. Please share this information with your technical team to determine if system updates are required. Current Effective August 2016 Bank Bank Product Line Service Bank Service Description Product Line Service Bank Service Description Code Code ACH - GIRO 2770 ACHDD MANDATE SETUP(INITIATOR) ACH PAYMENTS 2770 ACHDD MANDATE SETUP(INITIATOR) ACH - GIRO 3971 ZENGIN ACH (LOW) ACH PAYMENTS 3971 ZENGIN ACH (LOW) ACH - GIRO 4093 ZENGIN ACH (HIGH) ACH PAYMENTS 4093 ZENGIN ACH (HIGH) ACH - GIRO 4094 ELECTRONIC TRANSMISSION CHARGE ACH PAYMENTS 4094 ELECTRONIC TRANSMISSION CHARGE ACH - GIRO 4170 OUTWARD PYMT - GIRO (URGENT) 1 ACH PAYMENTS 4170 OUTWARD PYMT - GIRO (URGENT) 1 ACH - GIRO 4171 OUTWARD PYMT - GIRO (URGENT) 2 ACH PAYMENTS 4171 OUTWARD PYMT - GIRO (URGENT) 2 ACH - GIRO 4172 OUTWARD PYMT - GIRO (URGENT) 3 ACH PAYMENTS 4172 OUTWARD PYMT - GIRO (URGENT) 3 ACH - GIRO 4173 OUTWARD PYMT - GIRO (URGENT) 4 ACH PAYMENTS 4173 OUTWARD PYMT - GIRO (URGENT) 4 ACH - GIRO 4174 OUTWARD PYMT - GIRO (URGENT) 5 ACH PAYMENTS 4174 OUTWARD PYMT - GIRO (URGENT) -

The Evolution of Electronic Bill Payment in Canada November 21, 2011 the Evolution of Electronic Bill Payment in Canada by W

The Evolution of Electronic Bill Payment in Canada November 21, 2011 The Evolution of Electronic Bill Payment in Canada By W. H. (Bill) Loewen, C.M., F.C.A., Chairman, Telpay Incorporated Since 1985 an estimated two billion bill payments have been generated electronically, first by telephone and then by personal computers. Nearly all of those payments were generated by individuals paying monthly bills such as utilities and credit cards. The resulting savings have been enormous. One consultant estimated that the bank cost of processing an electronic payment was one ninth the cost of a paper payment. That would put nearly $200,000,000 in the pockets of the banks and credit unions. The utilities and credit card companies probably saved in the order of $1.00 per payment over processing cheque payments via the mail. That could be $2 billion in savings to them. Then the bill payers saved over 50¢ per payment for postage alone for another billion dollars savings. At 2010 volumes of over 400,000,000 electronic payments, the annual savings to all parties, consumers, utilities and financial institutions, would likely come to somewhere near $600,000,000. And volumes continue to increase annually. How did this come about? The Canadian Payments Association (CPA) would have us believe they had a big hand in it. Their submission to the Task Force for Payment System Review says “The CPA was instrumental in driving the transition from cheques and paper in the 80s to electronic payments in the 90s”. That is simply not true. It was Telpay that started electronic bill payment 1985 and had to dodge sticks from the CPA and certain banks to stay in business. -

Mobile Banking! Mobile Banking Allows You to Easily Access Your Centinel Bank Accounts Via an App Designed for Your Iphone®, Ipad®, Or Android® Device

Welcome to Mobile Banking! Mobile Banking allows you to easily access your Centinel Bank accounts via an app designed for your iPhone®, iPad®, or Android® device. With Mobile Banking you can… View Account Balances and Recent Transaction History Transfer Funds between Accounts Pay Bills to Existing Payees View Alerts Deposit a Check (You must apply and be approved for this service) Find a Branch Location Manage your debit/ATM card Download For an all-inclusive Mobile Banking experience, download the Centinel Bank of Taos Mobile Banking Application through iTunes® or Google play®. Login Login using your existing Online Banking ID and Password. (You must be enrolled in Online Banking to utilize Mobile Banking. To enroll in Online Banking, Contact a Centinel Bank Representative) Terms and Conditions Accept the Terms and conditions to utilize the Mobile Banking Application. You may also obtain a copy of the Terms and Conditions through your Online Banking Account or by contacting a Centinel Bank Representative at (575)758-6700. Enroll Complete your enrollment with a few steps…….. Turn ON or OFF Text Message Alerts Input your Mobile Number Select your Wireless Provider Select Enroll to complete your enrollment! (000)000-0000 Home Home is the initial screen for Mobile Banking and allows quick access to all application options. Options Include: Accounts Transfers Bill Payments Remote Deposit Manage Cards Alerts Locations My Accounts Accounts lists all of the accounts your have selected to view through Mobile Banking. Select an account to view specific transactions for that account. Select a transaction to see details about that specific transaction. -

Banner Bank Small Business Bill Pay Agreement

SMALL BUSINESS BILL PAYMENT AGREEMENT – TERMS AND CONDITIONS OF THE BILL PAYMENT SERVICE This Small Business Bill Payment Agreement (“Agreement”) sets forth the terms and conditions of the bill payment service offered by Banner Bank (the “Service”). This Agreement supplements the terms and conditions of the Account Agreement as defined below. SERVICE DEFINITIONS “Account Agreement” means the signature cards and accompanying documents that comprise the depository account agreement and related depository services, including, the Terms and Conditions of Your Account, Online and Mobile Banking User Agreement, and as applicable, treasury management or other agreements. "Agreement" means these terms and conditions of the bill payment service. “Bank,” “we” or “us” means Banner Bank. "Business Day" is every Monday through Friday, excluding Federal Reserve holidays. "Customer Service" means the Customer Service department of Banner Bank. Please see the CONTACT AND SUPPORT section below for Customer Service contact information. "Due Date" is the date reflected on your Payee statement for which the payment is due; it is not the late date or grace period. "Pay From Account" is the checking account from which bill payments will be debited. "Payee" is the person or entity to which you wish a bill payment to be directed or is the person or entity from which you receive electronic bills, as the case may be. "Payment Date" is the day you want your Payee to receive your bill payment. This day can only be a Business Day and is only an estimate. Delivery may take more or less time when we are required to mail a check to your Payee. -

Payment Services Guide

CitiDirect® Online Banking Payments Services Guide March 2004 Proprietary and Confidential These materials are proprietary and confidential to Citibank, N.A., and are intended for the exclusive use of CitiDirect ® Online Banking customers. The foregoing statement shall appear on all copies of these materials made by you in whatever form and by whatever means, electronic or mechanical, including photocopying or in any information storage system. In addition, no copy of these materials shall be disclosed to third parties without express written authorization of Citibank, N.A. Table of Contents Overview .......................................................................................................................................1 Payments Services....................................................................................................................1 Creating Service Requests From Transaction Lookup..............................................................2 Creating Service Requests From Transaction Details ..............................................................9 Modifying Service Requests....................................................................................................14 Authorizing or Deleting Service Requests...............................................................................16 Viewing Service Request Transactions...................................................................................18 Disclaimer ...................................................................................................................................20 -

Automated Teller Machine Usage and Customers' Satisfactionin Nigeria

Global Journal of Management and Business Research: C Finance Volume 14 Issue 4 Version 1.0 Year 2014 Type: Double Blind Peer Reviewed International Research Journal Publisher: Global Journals Inc. (USA) Online ISSN: 2249-4588 & Print ISSN: 0975-5853 Automated Teller Machine usage and Customers’ Satisfaction in Nigeria By Odusina, Ayokunle Olumide Abraham Adesanya Polytechnic, Nigeria. Abstract- This paper endeavors to investigate ATM Usage and Customers’ Satisfaction in Nigeria. It was discovered that despite the increasing number of ATM installations in Nigeria. Customers’ needs are not satisfactorily met as customers are always seen on queue in large numbers at various ATM designated centers as well as poor service delivery of some of these machine. The research engages comparative analysis of three banks in Ogun State, Metropolis of Nigeria viz-a- viz First Bank, Guaranty Trust Bank and Skye Bank. However, questionnaires were distributed to the respondents. A total of 200 respondents answered the questionnaire cutting across the three banks, the chi-square statistical tool was used to analyze the data and the results showed a positive and significant relationship between ATM Usage and Customers’ Satisfaction. Keywords: ATM, bank, customers’ satisfaction, nigeria. GJMBR-C Classification : JEL Code: G19 AutomatedTellerMachineusageandCustomersSatisfactioninNigeria Strictly as per the compliance and regulations of: © 2014. Odusina, Ayokunle Olumide. This is a research/review paper, distributed under the terms of the Creative Commons Attribution-Noncommercial 3.0 Unported License http://creativecommons.org/licenses/by-nc/3.0/), permitting all non-commercial use, distribution, and reproduction in any medium, provided the original work is properly cited. Automated Teller Machine usage and Customers’ Satisfaction in Nigeria Odusina, Ayokunle Olumide Abstract - This paper endeavors to investigate ATM Usage and the available staff on the other hand. -

The Ever Changing Landscape of Electronic Bill Payment WPTA Annual Conference April 12 – 14, 2017 Disclaimer

The Ever Changing Landscape of Electronic Bill Payment WPTA Annual Conference April 12 – 14, 2017 Disclaimer This document is designed to provide general information only and is not comprehensive nor is it legal advice. In providing this information, neither KeyBank nor its affiliates are acting as your agent, broker, advisor, or fiduciary, or is offering any tax, accounting, or legal advice regarding these instruments or transactions. If legal advice or other expert assistance is required, the services of a competent professional should be sought. KeyBank does not make any warranties regarding the results obtained from the use of this information. ©2017 KeyCorp. KeyBank is Member FDIC. 170330-215135 1 1 Presenter Information David Ptasznik Sr. Product Manager Enterprise Commercial Payments group • Based in Cleveland, Ohio. • Over 20 years of payments experience with the past 14 years at KeyBank in various roles. • Certified Treasury Professional (CTP) and was the past president of the Northern Ohio AFP chapter. • Undergraduate degree from John Carroll University and MBA from Baldwin Wallace University. 2 2 Agenda and Objectives Agenda Objectives • Overview Discuss the trends, needs and • C2B Trends challenges of billers and payers in • Industry Update the bill payment space, and • Benefits to Payers and Billers current and future solutions in the • Current and Future Trends future • Discussion • Takeaways 3 3 4 4 Overview Technological advances over the past five to ten years have increased the number of electronic bill payment options for billers and consumer/business payers. We will examine the trends of the bill payment landscape, needs of billers and payers, ways to increase paper to electronic adoption, current solutions available and emerging functionality/technologies in 2017 and beyond. -

Online Banking

Getting Started ONLINE BANKING TRANSACTION CUTOFF TIMES Service BNH Cutoff Times Bill Pay 4:00 p.m. EST External Transfers 6:00 p.m. EST Mobile Deposit 6:00 p.m. EST Internal Transfers 6:00 p.m. EST BROWSER SETTINGS In order to utilize Bank of New Hampshire’s online banking, we require you to use a current version of the web browser (i.e. Internet Explorer, Firefox, Chrome, Safari) or the latest version of our BeMobile Banking app. BankNH.com Member FDIC ENROLLING IN BNH ONLINE BANKING 1. Visit BankNH.com and select the Online Banking tab. 2. Choose Enroll Today. 3. Select either Personal Enrollment or Business Enrollment based on your needs. Please note: The Business enrollment process will differ from the Personal process listed below. 4. Complete the enrollment form and then click Continue. 5. We need to send you a one-time use Secure Access Code. Click either the truncated email address or phone number displayed on the screen. *The Secure Access Code delivery options displayed are based on information we have on file. If your contact information is not correct, you will need to contact us to complete the enrollment process. Once you gain access, you can add additional delivery options under Preferences. 6. Enter the Secure Access Code that was sent to you and then click Submit. 7. Now select a password for online banking and confirm. ClickSubmit . 8. The Online Banking Terms and Conditions will display. ClickAccept . 9. The Statement Delivery Preferences prompt will display. Click Enroll Now to enroll in electronic statements.