Scheme C - Tier I

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

India Capital Markets Experience

Dorsey’s Indian Capital Markets Capabilities March 2020 OVERVIEW Dorsey’s capital markets team has the practical wisdom and depth of experience necessary to help you succeed, even in the most challenging markets. Founded in 1912, Dorsey is an international firm with over 600 lawyers in 19 offices worldwide. Our involvement in Asia began in 1995. We now cover Asia from our offices in Hong Kong, Shanghai and Beijing. We collaborate across practice areas and across our international and U.S. offices to assemble the best team for our clients. Dorsey offers a full service capital markets practice in key domestic and international financial centers. Companies turn to Dorsey for all types of equity offerings, including IPOs, secondary offerings (including QIPs and OFSs) and debt offerings, including investment grade, high-yield and MTN programs. Our capital markets clients globally range from emerging companies, Fortune 500 seasoned issuers, and venture capital and private equity sponsors to the underwriting and advisory teams of investment banks. India has emerged as one of Dorsey’s most important international practice areas and we view India as a significant market for our clients, both in and outside of India. Dorsey has become a key player in the Indian market, working with major global and local investment banks and Indian companies on a range of international securities offerings. Dorsey is recognized for having a market-leading India capital markets practice, as well as ample international M&A and capital markets experience in the United States, Asia and Europe. Dorsey’s experience in Indian capital markets is deep and spans more than 15 years. -

NHPC Limited: Ratings Reaffirmed

July 09, 2021 NHPC Limited: Ratings reaffirmed Summary of rating action Previous Rated Amount Current Rated Amount Instrument* Rating Action (Rs. crore) (Rs. crore) Long term bonds programme 6,710.41 6,710.41 [ICRA]AAA(Stable) reaffirmed [ICRA]AAA(Stable) reaffirmed and Long term bonds programme 2,039.59 - withdrawn Total 8,750.0 6,710.41 *Instrument details are provided in Annexure-1 Rationale ICRA’s rating reflects NHPC Limited’s (NHPC) established position in India’s hydropower generation sector, its significant scale of operations and strategic importance to the Government of India (GoI) as reflected in GoI’s shareholding of 70.95% as on March 31, 2021. ICRA also favourably notes the competitive tariff level for the company’s power plants and strong operating efficiencies as reflected in its plant availability factor (PAF) over the years. The rating continues to reflect the low business risk for the company’s operational portfolio arising out of cost-plus tariff mechanism applicable for its hydel power generating stations and superior operational efficiency levels, ensuring regulated returns. Further, the rating continues to factor in the healthy track record of power generation from operational hydel power projects aided by a favourable hydrology. The company’s credit profile is also supported by a favourable capital structure as reflected in a debt-to-equity ratio of 0.71 times on a consolidated basis (0.80 times on standalone basis) and strong liquidity as reflected in cash and bank balances of Rs. 2,257 crore on a consolidated basis (Rs. 914 crore on a standalone basis), as on March 31, 2021. -

ICICI Bank Strong Performance, Attractive Franchise

ICICI Bank Strong performance, attractive franchise Powered by the Sharekhan 3R Research Philosophy Banks & Finance Sharekhan code: ICICIBANK Result Update Update Stock 3R MATRIX + = - Summary Right Sector (RS) ü ICICI Bank posted strong Q4FY2021 results with core operational performance coming higher than expectations, lower-than-expected slippages and sequentially improving Right Quality (RQ) ü asset quality are key positives. GNPA/NNPA ratio improved to 4.96%/1.14% (versus pro forma GNPA/NNPA of 5.42%/1.26% Right Valuation (RV) ü in Q3FY2021) and watchlist book declined; management commentary was positive and indicated strong growth in FY2022E. = - + Positive Neutral Negative The bank is available at 2.4x/2.1x its FY2022E/FY2023E BVPS. The stock has corrected by ~16% from its highs, and we believe valuations are attractive. What has changed in 3R MATRIX We maintain Buy rating on the stock with a revised SOTP-based PT of Rs. 800. Old New ICICI Bank posted strong Q4FY2021 results with core operational performance coming higher than expectations, lower-than-expected slippages, and sequentially improving asset quality RS being key positives. The quarter saw core operating performance above expectations with NII growth at 16.8% y-o-y, led by recovery in loan growth and NIMs improving by 17 bps q-o-q RQ to 3.84%. Strong traction in advances growth was seen with domestic loan growth posting 18% y-o-y growth. Going forward, as the bank looks to build on growth with a focus on a well- RV rated book, pickup in advances, and opex/credit cost will be key support and positives. -

Non-Performing Assets: a Comparison of ICICI Bank and HDFC Bank

Special Issue - 2017 International Journal of Engineering Research & Technology (IJERT) ISSN: 2278-0181 NCIETM - 2017 Conference Proceedings Non-Performing Assets: A Comparison of ICICI Bank and HDFC Bank Dr. Prerna Dawar*Ms. Pooja Sharma** *Dean & Professor Geeta Engineering College , Naultha , Panipat *Assistant Professor, SBD Group of Institutions , Kurukshetra Abstract - Banking in India originated in the last decade of the II. NON PERFORMING ASSETS (NPAs) 18th century. Private sector banks occupy a major part of NPA refers to loans that are in peril of default. The asset banking in India. Private sector banks have a very wide has been categorized as non-performing asset when the network of branches in rural and urban areas. But now a day borrower failed to make principle or interest payment they have diversified their activities to the emerged fields of within 90 days. It has always been a challenge for financial operations like merchant banking, leasing and venture capital etc. Due to increased level of competition private banks have institutions to manage their Non-performing assets because been lending aggressively to the customers which in turn of the dependency on interest payment. NPAs of financial increasing the proportion of Non-Performing Assets institutions increase due to pressure from economy as they (Henceforth, NPAs). Non-performing Asset has been an have to lent aggressively which in turn, reduces their important parameter to analyse of financial performance of capacity to capture all the assets completely. NPAs can be banks as it results in decreasing margin and higher divided into two main categories as follows: provisioning requirements for doubtful debts. -

NTPC Limited and BPDP on Build, Own and Operate Basis

Name of the Issue: NTPC 1Type of issue (IPO/ FPO) FPO 2 Issue size (Rs cr) 8,480.10 3 Grade of issue alongwith name of the rating agency Not applicable* * Grading applicable only for initial public offerings, as per ICDR and other applicable regulations 4 Subscription Level (Number of times) 1.24* Source: Final Post Issue Monitoring Report. * The above figure is net of cheque returns, but before technical rejections; Amount of subscription includes all bids received at Employee price of Rs 191 for eligible Employees, at floor price of Rs 201 for Retail Category and Non Institutional Category and above Floor Price of Rs 201 per equity share, at clearing price of Rs. 202 per equity share received from QIBs 5 QIB Holding (as a % of outstanding capital) Particulars % (i) allotment in the issue - Feb 18, 2010 (1) 4.53% (ii) at the end of the 1st Quarter immediately after the listing of the issue (March 31, 2010) (2) 11.59% (iii) at the end of 1st FY (March 31, 2010) (2) 11.59% (iv) at the end of 2nd FY (March 31, 2011) (2) 11.84% (v) at the end of 3rd FY (March 31, 2012) (2) 11.68% Source: (1) Basis of Allotment. Excludes pre-issue holding by QIBs. (2) Clause 35 Reporting with the Stock Exchanges. Represents holding of "Institutions" category. 6 Financials of the issuer (Rs. Crore) Parameters 1st FY (March 31, 2010) 2nd FY (March 31, 2011) 3rd FY (March 31, 2012) Income from operations* 50,163. 3 59,505.4 65,893.7 Net Profit for the period 8,837. -

Diversification on the Cards for Indian State-Owned Enterprises

1 Vibhuti Garg, Energy Economist December 2019 Diversification on the Cards for State-Owned Enterprises State-Owned Enterprises Going Green for Growth and to Stay Relevant The Indian Central Government is leading the country in the adoption of clean renewable energy, driving the uptake and the building of new capacity by state- owned enterprise (SOEs), through learning by doing. The ambition is clear. The country had already installed 83 gigawatts (GW) of renewable energy capacity as of October 2019,1 an 80% increase in less than three years. India has also put forward a target of 175GW of variable renewable energy by 2022 to 450GW by 2030, in a bid to clean up the air in its cities and lessen the economy’s rapidly growing dependence on imported fossil fuels. Currently, thermal power plant developers in India are under huge pressure. Existing plants are being underutilised, with the plant load factor (PLF) sitting below 60% over the past two years. Further stress is being caused by Thermal power plant excessive financial leverage, fuel supply developers in India are disruptions, issues in securing competitively under huge pressure. priced power purchase agreements (PPAs), and payment delays, which all together ensures debt servicing is extremely difficult. In contrast, falling renewable energy prices have led to a recent increase in privately funded renewable projects. The favourable addition of priority grid access, exemption from transmission charges, and increased renewable targets, have further boosted this optimistic sector. Transitioning of Energy Investment in India Energy investment by SOEs in India – also called public sector undertaking (PSU) or public sector enterprise (PSE) – has so far largely focused on fossil fuel production. -

LIC Housing Finance (LICHF)

LIC Housing Finance (LICHF) CMP: | 408 Target: | 400 (-2%) Target Period: 12 months HOLD months August 6, 2021 Uncertainty on stress accretion, low NPA buffer… About the stock: LIC Housing Finance (LICHF) is among the largest HFCs in India with an extensive distribution network of 282 marketing office and 2421 employees. Particulars Ess Total 91% of LICHF’s customers are salaried and 9% are self employed Particulars Amount Retail home loans form 78.3% of the overall book Market Capitalisation | 20605 crore Networth (FY21) | 20521 crore 52 week H/L 542 / 255 Face value | 2 Q1FY22 Results: Subdued overall performance; asset quality concern looming. Update Company Shareholding pattern NII up 4.5% YoY, down 15.3% QoQ, NIMs down 46 bps QoQ to 2.2% (in %) Jun-20 Sep-20 Dec-20 Mar-21 Jun-21 Promoter 40.3 40.3 40.3 40.3 40.3 Higher provisions at | 830 crore, C/I ratio rise impacted PAT at | 153 crore FII 34.3 34.4 29.3 28.2 28.8 Stage 3 assets rose 181 bps from 4.12% to 5.93% & 2.3% was restructured DII 10.6 10.4 15.4 16.8 15.6 Others 14.8 21.9 21.9 14.7 15.3 Price Chart What should investors do? LICHF has given ~57% return over the past year. 600 20000 500 However, we believe a healthy recovery on stressed asset is necessary for better 15000 valuations. 400 300 10000 200 We retain our HOLD rating on the stock 5000 100 Target Price and Valuation: We value LIC Housing at ~0.9 FY23E BV and revise 0 0 our target price for the stock at | 400 per share from | 475 earlier. -

NHPC LTD. (A Govt. of India Enterprise) TENDER DOCUMENT for Purchase of Spares of Two No of 3000 LPH, CEE DEE Make Transformer O

NHPC LTD. (A Govt. of India Enterprise) TENDER DOCUMENT FOR Purchase of Spares of Two no of 3000 LPH, CEE DEE make Transformer oil Filtration plant Tender Specification No._NH/DG/PCS/1507/120 dated 22/06/18 SECTION – 0 NOTICE INVITING TENDER (NIT) एन एच पी सी लिलिटेड NHPC LIMITED (A Govt. of India Enterprise) Procurement Contract Services Dhauliganga Power Station, Tapovan, Dharchula-PIN 262545 CIN: L40101HR1975GOI032564 SECTION–0: NOTICE INVITING E-TENDER (NIT) (Domestic Open Competitive Bidding) Online electronic bids (e-tenders) under two cover system are invited on behalf of NHPC Limited (A Public Sector Enterprise of the Government of India) from domestic bidders registered in India. Purchase of Spares of Two no of 3000 LPH, CEE DEE make Transformer oil Filtration plant Tender Specification No.:( NH/DG/PCS/1507/2018/120 ) Tender document can be viewed and downloaded from NHPC Limited website www.nhpcindia.com and Central Public Procurement Portal (CPPP) at https://eprocure.gov.in/eprocure/app. The bid is to be submitted online only on https://eprocure.gov.in/eprocure/app up to last date and time of submission of bids. Sale of hard copy of tender document is not applicable. 1.0 Brief Details & Critical Dates of Tender: 1.1 Brief Details of Tender: S. Item Description No. Purchase of Spares of Two no of 3000 LPH, CEE (i) Name of work DEE make Transformer oil Filtration plant (ii) Tender Specification No. NH/DG/PCS/1507/2018/120 (iii) Mode of tendering e-procurement system (Open Tender) (iv) Tender ID 2018_NHPC_351819 (v) Cost of bidding document Rs 590/- in the form of Crossed Demand Draft in favour of “NHPC Limited” payable at SBI DHARCHULA. -

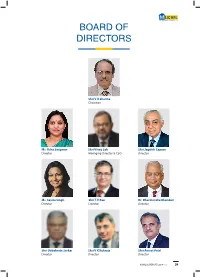

Board of Directors

BOARD OF DIRECTORS Shri V K Sharma Chairman Ms. Usha Sangwan Shri Vinay Sah Shri Jagdish Capoor Director Managing Director & CEO Director Ms. Savita Singh Shri T.V Rao Dr. Dharmendra Bhandari Director Director Director Shri Debabrata Sarkar Shri V K Kukreja Shri Ameet Patel Director Director Director 23 LIC HOUSING FINANCE LIMITED ANNUAL REPORT 2016-17 24 BOARD OF DIRECTORS SHRI V K SHARMA MS. USHA SANGWAN Chairman Director Shri Vijay Kumar Sharma took charge as Chairman, Life Mrs. Usha Sangwan, is the first ever woman Managing Insurance Corporation of India on 16th December, 2016. Prior Director of Life Insurance Corporation of India. She is Post to his taking over as Managing Director, LIC of India, on 1st Graduate in Economics and Post Graduate Diploma holder in November, 2013, he was Managing Director & Chief Executive Human Resource Management and Licentiate from Insurance Officer, LIC Housing Finance Limited (LICHFL), a premiere Institute of India. She joined LIC as Direct Recruit Officer in 1981. housing finance provider in the country with loan portfolio exceeding `83,000 crore. Mrs. Sangwan is the whole time Director of LIC of India, Board Member of General Insurance Corporation of India, Shri Vijay Kumar Sharma, born on 19th December, 1958 is LIC Housing Finance Ltd., Axis Bank, Ambuja Cements Ltd. a post-graduate (M.Sc.) in Botany from Patna University. and Bombay Stock Exchange Ltd., Board Member of LIC Shri Sharma joined LIC as Direct Recruit Officer in 1981 (International) BSC © Bahrain, Kenindia Assurance Co. Ltd., LIC and has grown with the Company since then. During his Card Services Ltd., Member of Governing Council of National stint as Senior Divisional Manager, Karnal, a rural division, Insurance Academy, Member on the Board of Education of had catapulated to Number One position in the country Insurance Institute of India, a Trustee of LIC Golden Jubilee in premium income ahead of all other metro centres. -

Annual Report 2018-19

43rd ANNUAL REPORT 2018-19 CORPORATE VISION To be a global leading organization CORPORATE MISSION for sustainable development of clean power through competent, To achieve excellence in development of responsible and clean power at international standards. innovative values. To execute & operate projects through efficient and competent contract management and innovative R&D in environment friendly and socio-economically responsive manner. To develop, nurture and empower the human capital to leverage its full potential. To practice the best corporate governance and competent value based management for a strong corporate identity and showing concern for employees, customer, environment and society. To adopt & innovate state-of-the-art technologies and optimize use of natural resources through effective management. Shri Balraj Joshi, CMD (centre), Shri Ratish Kumar, Director (Projects) (2nd from left), Shri N. K. Jain, Director (Personnel) (2nd from right), Shri M. K. Mittal, Director (Finance) (extreme left) and Shri Janardan Choudhary, Director (Technical) (extreme right) during the Analyst Meet at Mumbai on 30th May, 2019 Annual Report 2018-19 NHPC Digest of Important Financial Data (Five Years) ..................................................................... 2 Reference Information ......................................................................................................... 3 Letter to Shareholders ......................................................................................................... 5 NHPC’s Performance -

For Immediate Publication / Broadcast / Telecast PR / 1253

. For Immediate Publication / Broadcast / Telecast PR / 1253 IDBI Additional Tier - I (AT - I) Bonds oversubscribed Mumbai, October 17, 2014: IDBI Bank’s first Basel III compliant Additional Tier – I (AT - I) bonds amounting to `2,500 crore (`1,500 crore with an option to retain over-subscription upto `1,000 crore) received an overwhelming response and has been fully subscribed prior to the closure date. The issue opened on September 29, 2014. This is the first AT - I bond issuance by a bank in India after RBI modified its Basel III guidelines vide its circular dated September 1, 2014. The issue was competitively priced at a coupon of 10.75% p.a. payable annually. The issue is perpetual in nature with call option after the instrument has run for 10 years. The amount mobilised would be counted as a part of Tier I capital and enhance the capital adequacy of the Bank. The bonds are rated AA- by CRISIL and India Rating. Shri M. S. Raghavan, Chairman & Managing Director, IDBI Bank while commenting on the bond issuance, stated, "IDBI Bank is one of the best known names and has been a pioneer in various initiatives in the banking industry. The resounding success of this bond issue is testimony to this fact. This issuance will pave way for other banks to issue Tier I Bonds in the domestic market and will increase the acceptance of this instrument among the investors.” Axis Bank Ltd., Darashaw & Co. Pvt. Ltd., ICICI Bank Ltd., Trust Investment Advisors Pvt. Ltd. and IDBI Capital Market Services Ltd. -

A Flight to Safety As Indian Banks Navigate Tumultuous Times 2020 Greenwich Leaders: Indian Corporate Banking

A Flight to Safety as Indian Banks Navigate Tumultuous Times 2020 Greenwich Leaders: Indian Corporate Banking The global pandemic is putting economies and financial systems around the world under unprecedented stress. In India, this represents an even sterner test for a banking system that is still reeling from the impact of bank failures prior to the outbreak of COVID-19. Amid a national lockdown and fears of a liquidity crisis, companies in India are joining consumers in shifting business to the largest and presumably safest banks. In this report, we will analyze how the still-unfolding crisis and the many other challenges facing India’s banking sector are affecting the competitive positioning of individual public- and private-sector banks. INDIA’S BANKING WOES PILE UP These key factors converged to create a perfect storm in India’s banking system: J Stress of Public Sector (PSU) Banks’ Balance Sheet With direct intervention from the Indian government, non-performing asset (NPA) ratios had started to decline by 2019, but this is still a work-in-progress for the PSU banking sector. The series of public bank mergers orchestrated by RBI represent a critical step that will make the banking system stronger and more stable. However, navigating sweeping organizational integrations is going to be tough with the epic challenge of the COVID-19 crisis. J NBFC Liquidity Issues The nonbank financial companies (NBFC) crisis, which started in 2018 with the collapse of IL&FS, continues to plague the Indian banking sector. These 10,000+ lightly regulated NBFCs are not only a critical source of credit for small and medium businesses, they have also become intricately linked with the overall banking sector.