And Long-Run Evidence from Bitcoin and Altcoin Markets

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Peer Co-Movement in Crypto Markets

Peer Co-Movement in Crypto Markets G. Schwenkler and H. Zheng∗ February 4, 2021y Abstract We show that peer linkages induce significant price co-movement in crypto markets in excess of common risk factors and correlated demand shocks. When large abnormal return shocks hit one crypto, its peers experience unusually large abnormal returns of the opposite sign. These effects are primarily concentrated among smaller peers and revert after several weeks, resulting in predictable returns. We develop trading strategies that exploit this rever- sal, and show that they are profitable even after accounting for trading fees and frictions. We establish our results by identifying crypto peers through co-mentions in online news using novel natural language processing technologies. Keywords: Cryptocurrencies, peers, co-movement, competition, natural language pro- cessing. JEL codes: G12, G14, C82. ∗Schwenkler is at the Department of Finance, Santa Clara University Leavey School of Business. Zheng is at the Department of Finance, Boston University Questrom School of Business. Schwenkler is corresponding author. Email: [email protected], web: http://www.gustavo-schwenkler.com. yThis is a revision of a previous paper by the two authors called \Competition or Contagion: Evidence from Cryptocurrency Markets." We are grateful to Jawad Addoum (discussant), Daniele Bianchi (discussant), Will Cong, Tony Cookson, Sanjiv Das, Seoyoung Kim, Andreas Neuhierl, Farzad Saidi, and Antoinette Schoar, seminar participants at Boston University and the Society for Financial Econometrics, and the participants at the 2020 Finance in the Cloud III Virtual Conference, the 2020 MFA Annual Meeting, the 3rd UWA Blockchain, Cryptocurrency and FinTech Conference, and the 2020 INFORMS Annual Meeting for useful comments and suggestions. -

YEUNG-DOCUMENT-2019.Pdf (478.1Kb)

Useful Computation on the Block Chain The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters Citation Yeung, Fuk. 2019. Useful Computation on the Block Chain. Master's thesis, Harvard Extension School. Citable link https://nrs.harvard.edu/URN-3:HUL.INSTREPOS:37364565 Terms of Use This article was downloaded from Harvard University’s DASH repository, and is made available under the terms and conditions applicable to Other Posted Material, as set forth at http:// nrs.harvard.edu/urn-3:HUL.InstRepos:dash.current.terms-of- use#LAA 111 Useful Computation on the Block Chain Fuk Yeung A Thesis in the Field of Information Technology for the Degree of Master of Liberal Arts in Extension Studies Harvard University November 2019 Copyright 2019 [Fuk Yeung] Abstract The recent growth of blockchain technology and its usage has increased the size of cryptocurrency networks. However, this increase has come at the cost of high energy consumption due to the processing power needed to maintain large cryptocurrency networks. In the largest networks, this processing power is attributed to wasted computations centered around solving a Proof of Work algorithm. There have been several attempts to address this problem and it is an area of continuing improvement. We will present a summary of proposed solutions as well as an in-depth look at a promising alternative algorithm known as Proof of Useful Work. This solution will redirect wasted computation towards useful work. We will show that this is a viable alternative to Proof of Work. Dedication Thank you to everyone who has supported me throughout the process of writing this piece. -

Blockchain – Operator Opportunities Version 1.0 July 2018

Blockchain – Operator Opportunities Version 1.0 July 2018 About the GSMA The GSMA represents the interests of mobile operators worldwide, uniting more than 750 operators with over 350 companies in the broader mobile ecosystem, including handset and device makers, software companies, equipment providers and internet companies, as well as organisations in adjacent industry sectors. The GSMA also produces the industry-leading MWC events held annually in Barcelona, Los Angeles and Shanghai, as well as the Mobile 360 Series of regional conferences. For more information, please visit the GSMA corporate website at www.gsma.com. Follow the GSMA on Twitter: @GSMA. About the GSMA Internet Group The GSMA Internet Group (IG) is the key working group which researches, analyses and measures the potential opportunities and impacts of new web and internet technologies on mobile operator networks and platforms. We maintain the most up-to-date knowledge base of new internet and web innovations through intelligence gathering of available global research and active participation in key Standards organisations. www.gsma.com/workinggroups Authors: Peter Ajn Vanleeuwen, KPN Douwe van de Ruit, KPN Contributors: Dan Druta, AT&T Axel Nennker, Deutsche Telecom Shamit Bhat, GSMA Rinze Cats, KPN Kaissar Jabr, Monty Holding Page 2 of 36 Table of Contents Blockchain – Operator Opportunities ............................................................................ 1 Version 1.0 ............................................................................................................................... -

Crypto Daily Report – June 9

This document is being provided publicly in the following form. Please subscribe to FSInsight.com for more. Members Area Crypto Daily Crypto Daily Report – June 9 Crypto Daily Crypto Daily Report – June 9 June 9 FSInsight Team Crypto Daily Report The Most Important Daily Data for Digital Assets Daily Analysis from FSInsight June 9, 2021 Late Tuesday evening, lawmakers in El Salvador's Congress voted by a supermajority in favor of making bitcoin legal tender. The law allows for the prices of goods and services to be denominated and paid in BTC, and perhaps more notably, exempts any exchanges in bitcoin from capital gains tax. Coinbase (Nasdaq: COIN) revealed Tuesday that its institutional holdings grew 170% from $45 billion to $122 billion in Q1 2021 as demand skyrocketed alongside the latest crypto bull run. The Company has over 8,000 institutional clients, many of which use its Coinbase Custody product. Crypto exchange Gemini acquired custody specialist Shard X for an undisclosed amount on Wednesday morning. Gemini COO, Noah Perlman, stated that the acquisition will enable Gemini " to meet the current demand for fast withdrawals, interacting with DeFi staking, or the transferring of digital assets with greater efficiency." Daily Important Metrics CRYPTO SIZE SENTIMENT BULLISH SIGNAL Bullish signal is tied to the crypto market growing Market Cap $1.5T +$42B ( +2.79% ) BTC Dominance 41.64% ( +1.49% ) STABLE COINS FUTURES CME BULLISH SIGNAL A positive spread between Futures Prices and Spot BULLISH SIGNAL Prices is Bullish Increase in circulating -

Linking Wallets and Deanonymizing Transactions in the Ripple Network

Proceedings on Privacy Enhancing Technologies ; 2016 (4):436–453 Pedro Moreno-Sanchez*, Muhammad Bilal Zafar, and Aniket Kate* Listening to Whispers of Ripple: Linking Wallets and Deanonymizing Transactions in the Ripple Network Abstract: The decentralized I owe you (IOU) transac- 1 Introduction tion network Ripple is gaining prominence as a fast, low- cost and efficient method for performing same and cross- In recent years, we have observed a rather unexpected currency payments. Ripple keeps track of IOU credit its growth of IOU transaction networks such as Ripple [36, users have granted to their business partners or friends, 40]. Its pseudonymous nature, ability to perform multi- and settles transactions between two connected Ripple currency transactions across the globe in a matter of wallets by appropriately changing credit values on the seconds, and potential to monetize everything [15] re- connecting paths. Similar to cryptocurrencies such as gardless of jurisdiction have been pivotal to their suc- Bitcoin, while the ownership of the wallets is implicitly cess so far. In a transaction network [54, 55, 59] such as pseudonymous in Ripple, IOU credit links and transac- Ripple [10], users express trust in each other in terms tion flows between wallets are publicly available in an on- of I Owe You (IOU) credit they are willing to extend line ledger. In this paper, we present the first thorough each other. This online approach allows transactions in study that analyzes this globally visible log and charac- fiat money, cryptocurrencies (e.g., bitcoin1) and user- terizes the privacy issues with the current Ripple net- defined currencies, and improves on some of the cur- work. -

On the Relationship of Cryptocurrency Price with US Stock and Gold Price Using Copula Models

mathematics Article On the Relationship of Cryptocurrency Price with US Stock and Gold Price Using Copula Models Jong-Min Kim 1 , Seong-Tae Kim 2 and Sangjin Kim 3,* 1 Statistics Discipline, University of Minnesota at Morris, Morris, MN 56267, USA; [email protected] 2 Department of Mathematics, North Carolina A&T State University, Greensboro, NC 27411, USA; [email protected] 3 Department of Management and Information Systems, Dong-A University, Busan 49236, Korea * Correspondence: [email protected] Received: 15 September 2020; Accepted: 20 October 2020; Published: 23 October 2020 Abstract: This paper examines the relationship of the leading financial assets, Bitcoin, Gold, and S&P 500 with GARCH-Dynamic Conditional Correlation (DCC), Nonlinear Asymmetric GARCH DCC (NA-DCC), Gaussian copula-based GARCH-DCC (GC-DCC), and Gaussian copula-based Nonlinear Asymmetric-DCC (GCNA-DCC). Under the high volatility financial situation such as the COVID-19 pandemic occurrence, there exist a computation difficulty to use the traditional DCC method to the selected cryptocurrencies. To solve this limitation, GC-DCC and GCNA-DCC are applied to investigate the time-varying relationship among Bitcoin, Gold, and S&P 500. In terms of log-likelihood, we show that GC-DCC and GCNA-DCC are better models than DCC and NA-DCC to show relationship of Bitcoin with Gold and S&P 500. We also consider the relationships among time-varying conditional correlation with Bitcoin volatility, and S&P 500 volatility by a Gaussian Copula Marginal Regression (GCMR) model. The empirical findings show that S&P 500 and Gold price are statistically significant to Bitcoin in terms of log-return and volatility. -

Vulnerability of Blockchain Technologies to Quantum Attacks

Vulnerability of Blockchain Technologies to Quantum Attacks Joseph J. Kearneya, Carlos A. Perez-Delgado a,∗ aSchool of Computing, University of Kent, Canterbury, Kent CT2 7NF United Kingdom Abstract Quantum computation represents a threat to many cryptographic protocols in operation today. It has been estimated that by 2035, there will exist a quantum computer capable of breaking the vital cryptographic scheme RSA2048. Blockchain technologies rely on cryptographic protocols for many of their essential sub- routines. Some of these protocols, but not all, are open to quantum attacks. Here we analyze the major blockchain-based cryptocurrencies deployed today—including Bitcoin, Ethereum, Litecoin and ZCash, and determine their risk exposure to quantum attacks. We finish with a comparative analysis of the studied cryptocurrencies and their underlying blockchain technologies and their relative levels of vulnerability to quantum attacks. Introduction exist to allow the legitimate owner to recover this account. Blockchain systems are unlike other cryptosys- tems in that they are not just meant to protect an By contrast, in a blockchain system, there is no information asset. A blockchain is a ledger, and as central authority to manage users’ access keys. The such it is the asset. owner of a resource is by definition the one hold- A blockchain is secured through the use of cryp- ing the private encryption keys. There are no of- tographic techniques. Notably, asymmetric encryp- fline backups. The blockchain, an always online tion schemes such as RSA or Elliptic Curve (EC) cryptographic system, is considered the resource— cryptography are used to generate private/public or at least the authoritative description of it. -

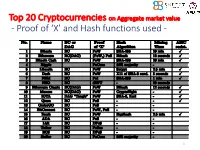

Proof of 'X' and Hash Functions Used

Top 20 Cryptocurrencies on Aggregate market value - Proof of ‘X’ and Hash functions used - 1 ISI Kolkata BlockChain Workshop, Nov 30th, 2017 CRYPTOGRAPHY with BlockChain - Hash Functions, Signatures and Anonymization - Hiroaki ANADA*1, Kouichi SAKURAI*2 *1: University of Nagasaki, *2: Kyushu University Acknowledgements: This work is supported by: Grants-in-Aid for Scientific Research of Japan Society for the Promotion of Science; Research Project Number: JP15H02711 Top 20 Cryptocurrencies on Aggregate market value - Proof of ‘X’ and Hash functions used - 3 Table of Contents 1. Cryptographic Primitives in Blockchains 2. Hash Functions a. Roles b. Various Hash functions used for Proof of ‘X’ 3. Signatures a. Standard Signatures (ECDSA) b. Ring Signatures c. One-Time Signatures (Winternitz) 4. Anonymization Techniques a. Mixing (CoinJoin) b. Zero-Knowledge proofs (zk-SNARK) 5. Conclusion 4 Brief History of Proof of ‘X’ 1992: “Pricing via Processing or Combatting Junk Mail” Dwork, C. and Naor, M., CRYPTO ’92 Pricing Functions 2003: “Moderately Hard Functions: From Complexity to Spam Fighting” Naor, M., Foundations of Soft. Tech. and Theoretical Comp. Sci. 2008: “Bitcoin: A peer-to-peer electronic cash system” Nakamoto, S. Proof of Work 5 Brief History of Proof of ‘X’ 2008: “Bitcoin: A peer-to-peer electronic cash system” Nakamoto, S. Proof of Work 2012: “Peercoin” Proof of Stake (& Proof of Work) ~ : Delegated Proof of Stake, Proof of Storage, Proof of Importance, Proof of Reserves, Proof of Consensus, ... 6 Proofs of ‘X’ 1. Proof of Work 2. Proof of Stake Hash-based Proof of ‘X’ 3. Delegated Proof of Stake 4. Proof of Importance 5. -

PWC and Elwood

2020 Crypto Hedge Fund Report Contents Introduction to Crypto Hedge Fund Report 3 Key Takeaways 4 Survey Data 5 Investment Data 6 Strategy Insights 6 Market Analysis 7 Assets Under Management (AuM) 8 Fund performance 9 Fees 10 Cryptocurrencies 11 Derivatives and Leverage 12 Non-Investment Data 13 Team Expertise 13 Custody and Counterparty Risk 15 Governance 16 Valuation and Fund Administration 16 Liquidity and Lock-ups 17 Legal and Regulatory 18 Tax 19 Survey Respondents 20 About PwC & Elwood 21 Introduction to Crypto Hedge Fund report In this report we provide an overview of the global crypto hedge fund landscape and offer insights into both quantitative elements (such as liquidity terms, trading of cryptocurrencies and performance) and qualitative aspects, such as best practice with respect to custody and governance. By sharing these insights with the broader crypto industry, our goal is to encourage the adoption of sound practices by market participants as the ecosystem matures. The data contained in this report comes from research that was conducted in Q1 2020 across the largest global crypto hedge funds by assets under management (AuM). This report specifically focuses on crypto hedge funds and excludes data from crypto index/tracking/passive funds and crypto venture capital funds. 3 | 2020 Crypto Hedge Fund Report Key Takeaways: Size of the Market and AuM: Performance and Fees: • We estimate that the total AuM of crypto hedge funds • The median crypto hedge fund returned +30% in 2019 (vs - globally increased to over US$2 billion in 2019 from US$1 46% in 2018). billion the previous year. -

Blocksci: Design and Applications of a Blockchain Analysis Platform

BlockSci: Design and applications of a blockchain analysis platform Harry Kalodner Steven Goldfeder Alishah Chator [email protected] [email protected] [email protected] Princeton University Princeton University Johns Hopkins University Malte Möser Arvind Narayanan [email protected] [email protected] Princeton University Princeton University ABSTRACT to partition eectively. In fact, we conjecture that the use of a tra- Analysis of blockchain data is useful for both scientic research ditional, distributed transactional database for blockchain analysis and commercial applications. We present BlockSci, an open-source has innite COST [5], in the sense that no level of parallelism can software platform for blockchain analysis. BlockSci is versatile in outperform an optimized single-threaded implementation. its support for dierent blockchains and analysis tasks. It incorpo- BlockSci comes with batteries included. First, it is not limited rates an in-memory, analytical (rather than transactional) database, to Bitcoin: a parsing step converts a variety of blockchains into making it several hundred times faster than existing tools. We a common, compact format. Currently supported blockchains in- describe BlockSci’s design and present four analyses that illustrate clude Bitcoin, Litecoin, Namecoin, and Zcash (Section 2.1). Smart its capabilities. contract platforms such as Ethereum are outside our scope. Second, This is a working paper that accompanies the rst public release BlockSci includes a library of useful analytic and visualization tools, of BlockSci, available at github.com/citp/BlockSci. We seek input such as identifying special transactions (e.g., CoinJoin) and linking from the community to further develop the software and explore addresses to each other based on well-known heuristics (Section other potential applications. -

Merged Mining: Curse Or Cure?

Merged Mining: Curse or Cure? Aljosha Judmayer, Alexei Zamyatin, Nicholas Stifter, Artemios Voyiatzis, Edgar Weippl SBA Research, Vienna, Austria (firstletterfirstname)(lastname)@sba-research.org Abstract: Merged mining refers to the concept of mining more than one cryp- tocurrency without necessitating additional proof-of-work effort. Although merged mining has been adopted by a number of cryptocurrencies already, to this date lit- tle is known about the effects and implications. We shed light on this topic area by performing a comprehensive analysis of merged mining in practice. As part of this analysis, we present a block attribution scheme for mining pools to assist in the evaluation of mining centralization. Our findings disclose that mining pools in merge-mined cryptocurrencies have operated at the edge of, and even beyond, the security guarantees offered by the underlying Nakamoto consensus for ex- tended periods. We discuss the implications and security considerations for these cryptocurrencies and the mining ecosystem as a whole, and link our findings to the intended effects of merged mining. 1 Introduction The topic of merged mining has received little attention from the scientific community, despite having been actively employed by a number of cryptocurrencies for several years. New and emerging cryptocurrencies such as Rootstock continue to consider and expand on the concept of merged mining in their designs to this day [19]. Merged min- ing refers to the process of searching for proof-of-work (PoW) solutions for multiple cryptocurrencies concurrently without requiring additional computational resources. The rationale behind merged mining lies in leveraging on the computational power of different cryptocurrencies by bundling their resources instead of having them stand in direct competition, and also to serve as a bootstrapping mechanism for small and fledgling networks [27, 33]. -

Blockchain & Cryptocurrency Regulation

Blockchain & Cryptocurrency Regulation Third Edition Contributing Editor: Josias N. Dewey Global Legal Insights Blockchain & Cryptocurrency Regulation 2021, Third Edition Contributing Editor: Josias N. Dewey Published by Global Legal Group GLOBAL LEGAL INSIGHTS – BLOCKCHAIN & CRYPTOCURRENCY REGULATION 2021, THIRD EDITION Contributing Editor Josias N. Dewey, Holland & Knight LLP Head of Production Suzie Levy Senior Editor Sam Friend Sub Editor Megan Hylton Consulting Group Publisher Rory Smith Chief Media Officer Fraser Allan We are extremely grateful for all contributions to this edition. Special thanks are reserved for Josias N. Dewey of Holland & Knight LLP for all of his assistance. Published by Global Legal Group Ltd. 59 Tanner Street, London SE1 3PL, United Kingdom Tel: +44 207 367 0720 / URL: www.glgroup.co.uk Copyright © 2020 Global Legal Group Ltd. All rights reserved No photocopying ISBN 978-1-83918-077-4 ISSN 2631-2999 This publication is for general information purposes only. It does not purport to provide comprehensive full legal or other advice. Global Legal Group Ltd. and the contributors accept no responsibility for losses that may arise from reliance upon information contained in this publication. This publication is intended to give an indication of legal issues upon which you may need advice. Full legal advice should be taken from a qualified professional when dealing with specific situations. The information contained herein is accurate as of the date of publication. Printed and bound by TJ International, Trecerus Industrial Estate, Padstow, Cornwall, PL28 8RW October 2020 PREFACE nother year has passed and virtual currency and other blockchain-based digital assets continue to attract the attention of policymakers across the globe.