Journal of Mathematical Economics Implementation of Pareto Efficient Allocations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

![Arxiv:0803.2996V1 [Q-Fin.GN] 20 Mar 2008 JEL Classification: A10, A12, B0, B40, B50, C69, C9, D5, D1, G1, G10-G14](https://docslib.b-cdn.net/cover/4730/arxiv-0803-2996v1-q-fin-gn-20-mar-2008-jel-classi-cation-a10-a12-b0-b40-b50-c69-c9-d5-d1-g1-g10-g14-354730.webp)

Arxiv:0803.2996V1 [Q-Fin.GN] 20 Mar 2008 JEL Classification: A10, A12, B0, B40, B50, C69, C9, D5, D1, G1, G10-G14

The virtues and vices of equilibrium and the future of financial economics J. Doyne Farmer∗ and John Geanakoplosy December 2, 2008 Abstract The use of equilibrium models in economics springs from the desire for parsimonious models of economic phenomena that take human rea- soning into account. This approach has been the cornerstone of modern economic theory. We explain why this is so, extolling the virtues of equilibrium theory; then we present a critique and describe why this approach is inherently limited, and why economics needs to move in new directions if it is to continue to make progress. We stress that this shouldn't be a question of dogma, but should be resolved empir- ically. There are situations where equilibrium models provide useful predictions and there are situations where they can never provide use- ful predictions. There are also many situations where the jury is still out, i.e., where so far they fail to provide a good description of the world, but where proper extensions might change this. Our goal is to convince the skeptics that equilibrium models can be useful, but also to make traditional economists more aware of the limitations of equilib- rium models. We sketch some alternative approaches and discuss why they should play an important role in future research in economics. Key words: equilibrium, rational expectations, efficiency, arbitrage, bounded rationality, power laws, disequilibrium, zero intelligence, mar- ket ecology, agent based modeling arXiv:0803.2996v1 [q-fin.GN] 20 Mar 2008 JEL Classification: A10, A12, B0, B40, B50, C69, C9, D5, D1, G1, G10-G14. ∗Santa Fe Institute, 1399 Hyde Park Rd., Santa Fe NM 87501 and LUISS Guido Carli, Viale Pola 12, 00198, Roma, Italy yJames Tobin Professor of Economics, Yale University, New Haven CT, and Santa Fe Institute 1 Contents 1 Introduction 4 2 What is an equilibrium theory? 5 2.1 Existence of equilibrium and fixed points . -

An Equilibrium-Conserving Taxation Scheme for Income from Capital

Eur. Phys. J. B (2018) 91: 38 https://doi.org/10.1140/epjb/e2018-80497-x THE EUROPEAN PHYSICAL JOURNAL B Regular Article An equilibrium-conserving taxation scheme for income from capital Jacques Temperea Theory of Quantum and Complex Systems, Universiteit Antwerpen, Universiteitsplein 1, 2610 Antwerpen, Belgium Received 28 August 2017 / Received in final form 23 November 2017 Published online 14 February 2018 c The Author(s) 2018. This article is published with open access at Springerlink.com Abstract. Under conditions of market equilibrium, the distribution of capital income follows a Pareto power law, with an exponent that characterizes the given equilibrium. Here, a simple taxation scheme is proposed such that the post-tax capital income distribution remains an equilibrium distribution, albeit with a different exponent. This taxation scheme is shown to be progressive, and its parameters can be simply derived from (i) the total amount of tax that will be levied, (ii) the threshold selected above which capital income will be taxed and (iii) the total amount of capital income. The latter can be obtained either by using Piketty's estimates of the capital/labor income ratio or by fitting the initial Pareto exponent. Both ways moreover provide a check on the amount of declared income from capital. 1 Introduction distribution of money over the agents involved in additive transactions follows a Boltzmann{Gibbs exponential dis- The distribution of income has been studied for a long tribution. Note that this is a strongly simplified model of time in the economic literature, and has more recently economic activity: it is clear that in reality global money become a topic of investigation for statistical physicists conservation is violated. -

Strong Nash Equilibria and Mixed Strategies

Strong Nash equilibria and mixed strategies Eleonora Braggiona, Nicola Gattib, Roberto Lucchettia, Tuomas Sandholmc aDipartimento di Matematica, Politecnico di Milano, piazza Leonardo da Vinci 32, 20133 Milano, Italy bDipartimento di Elettronica, Informazione e Bioningegneria, Politecnico di Milano, piazza Leonardo da Vinci 32, 20133 Milano, Italy cComputer Science Department, Carnegie Mellon University, 5000 Forbes Avenue, Pittsburgh, PA 15213, USA Abstract In this paper we consider strong Nash equilibria, in mixed strategies, for finite games. Any strong Nash equilibrium outcome is Pareto efficient for each coalition. First, we analyze the two–player setting. Our main result, in its simplest form, states that if a game has a strong Nash equilibrium with full support (that is, both players randomize among all pure strategies), then the game is strictly competitive. This means that all the outcomes of the game are Pareto efficient and lie on a straight line with negative slope. In order to get our result we use the indifference principle fulfilled by any Nash equilibrium, and the classical KKT conditions (in the vector setting), that are necessary conditions for Pareto efficiency. Our characterization enables us to design a strong–Nash– equilibrium–finding algorithm with complexity in Smoothed–P. So, this problem—that Conitzer and Sandholm [Conitzer, V., Sandholm, T., 2008. New complexity results about Nash equilibria. Games Econ. Behav. 63, 621–641] proved to be computationally hard in the worst case—is generically easy. Hence, although the worst case complexity of finding a strong Nash equilibrium is harder than that of finding a Nash equilibrium, once small perturbations are applied, finding a strong Nash is easier than finding a Nash equilibrium. -

Egalitarianism in Mechanism Design∗

Egalitarianism in Mechanism Design∗ Geoffroy de Clippely This Version: January 2012 Abstract This paper examines ways to extend egalitarian notions of fairness to mechanism design. It is shown that the classic properties of con- strained efficiency and monotonicity with respect to feasible options become incompatible, even in quasi-linear settings. An interim egali- tarian criterion is defined and axiomatically characterized. It is applied to find \fair outcomes" in classical examples of mechanism design, such as cost sharing and bilateral trade. Combined with ex-ante utilitari- anism, the criterion characterizes Harsanyi and Selten's (1972) interim Nash product. Two alternative egalitarian criteria are proposed to il- lustrate how incomplete information creates room for debate as to what is socially desirable. ∗The paper beneficiated from insightful comments from Kfir Eliaz, Klaus Nehring, David Perez-Castrillo, Kareen Rozen, and David Wettstein. Financial support from the National Science Foundation (grant SES-0851210) is gratefully acknowledged. yDepartment of Economics, Brown University. Email: [email protected] 1. INTRODUCTION Developments in the theory of mechanism design, since its origin in the sev- enties, have greatly improved our understanding of what is feasible in envi- ronments involving agents that hold private information. Yet little effort has been devoted to the discussion of socially desirable selection criteria, and the computation of incentive compatible mechanisms meeting those criteria in ap- plications. In other words, extending the theory of social choice so as to make it applicable in mechanism design remains a challenging topic to be studied. The present paper makes some progress in that direction, with a focus on the egalitarian principle. -

![Arxiv:1701.06410V1 [Q-Fin.EC] 27 Oct 2016 E Od N Phrases](https://docslib.b-cdn.net/cover/6156/arxiv-1701-06410v1-q-fin-ec-27-oct-2016-e-od-n-phrases-1566156.webp)

Arxiv:1701.06410V1 [Q-Fin.EC] 27 Oct 2016 E Od N Phrases

ECONOMICS CANNOT ISOLATE ITSELF FROM POLITICAL THEORY: A MATHEMATICAL DEMONSTRATION BRENDAN MARKEY-TOWLER ABSTRACT. The purpose of this paper is to provide a confession of sorts from an economist to political science and philosophy. A confession of the weaknesses of the political position of the economist. It is intended as a guide for political scientists and philosophers to the ostensible policy criteria of economics, and an illustration of an argument that demonstrates logico-mathematically, therefore incontrovertibly, that any policy statement by an economist contains, or is, a political statement. It develops an inescapable compulsion that the absolute primacy and priority of political theory and philosophy in the development of policy criteria must be recognised. Economic policy cannot be divorced from politics as a matter of mathematical fact, and rather, as Amartya Sen has done, it ought embrace political theory and philosophy. 1. THE PLACE AND IMPORTANCE OF PARETO OPTIMALITY IN ECONOMICS Economics, having pretensions to being a “science”, makes distinctions between “positive” statements about how the economy functions and “normative” statements about how it should function. It is a core attribute, inherited largely from its intellectual heritage in British empiricism and Viennese logical positivism (McCloskey, 1983) that normative statements are to be avoided where possible, and ought contain little by way of political presupposition as possible where they cannot. Political ideology is the realm of the politician and the demagogue. To that end, the most basic policy decision criterion of Pareto optimality is offered. This cri- terion is weaker than the extremely strong Hicks-Kaldor criterion. The Hicks-Kaldor criterion presupposes a consequentialist, specifically utilitarian philosophy and states any policy should be adopted which yields net positive utility for society, any compensation for lost utility on the part arXiv:1701.06410v1 [q-fin.EC] 27 Oct 2016 of one to be arranged by the polity, not the economist, out of the gains to the other. -

Pareto Efficiency by MEGAN MARTORANA

RF Fall Winter 07v42-sig3-INT 2/27/07 8:45 AM Page 8 JARGONALERT Pareto Efficiency BY MEGAN MARTORANA magine you and a friend are walking down the street competitive equilibrium is typically included among them. and a $100 bill magically appears. You would likely A major drawback of Pareto efficiency, some ethicists claim, I share the money evenly, each taking $50, deeming this is that it does not suggest which of the Pareto efficient the fairest division. According to Pareto efficiency, however, outcomes is best. any allocation of the $100 would be optimal — including the Furthermore, the concept does not require an equitable distribution you would likely prefer: keeping all $100 for distribution of wealth, nor does it necessarily suggest taking yourself. remedial steps to correct for existing inequality. If the Pareto efficiency says that an allocation is efficient if an incomes of the wealthy increase while the incomes of every- action makes some individual better off and no individual one else remain stable, such a change is Pareto efficient. worse off. The concept was developed by Vilfredo Pareto, an Martin Feldstein, an economist at Harvard University and Italian economist and sociologist known for his application president of the National Bureau of Economic Research, of mathematics to economic analysis, and particularly for his explains that some see this as unfair. Such critics, while con- Manual of Political Economy (1906). ceding that the outcome is Pareto Pareto used this work to develop efficient, might complain: “I don’t his theory of pure economics, have fewer material goods, but I analyze “ophelimity,” his own have the extra pain of living in a term indicating the power of more unequal world.” In short, giving satisfaction, and intro- they are concerned about not only duce indifference curves. -

Agent Based Models

1 1 BUT INDIVIDUALS ARE NOT GAS MOLECULES A. Chakraborti TOPICS TO BE COVERED IN THIS CHAPTER: • Agent based models: going beyond the simple statistical mechanics of colliding particles • Explaining the hidden hand of economy: self-organization in a collection of interacting "selfish" agents • Bio-box on A Smith • Minority game and its variants (evolutionary, adaptive etc) • Box on contributions of: WB Arthur, YC Zhang, D Challet, M Marsili et al • Agent-based models for explaining the power law for price fluctuations 1.1 Agent based models: going beyond the simple statistical mechanics of colliding particles One might actually wonder how the mathematical theories and laws which try to explain the physical world of electrons, protons, atoms and molecules could be applied to understand the complex social structure and economic behavior of human beings. Specially so, since human beings are complex and widely varing in nature, properties or characteristics, whereas e.g., the electrons are identical (we do not have to electrons of different types) and indistinguishable. Each electron has a charge of 1.60218 × 10−19C, mass of 9.10938 × 10−31kg, and is a spin-1/2 particle. Moreover, such properties of Econophysics. Sinha, Chatterjee, Chakraborti and Chakrabarti Copyright c 2008 WILEY-VCH Verlag GmbH & Co. KGaA, Weinheim ISBN: 3-527-XXXXX-X 2 1 BUT INDIVIDUALS ARE NOT GAS MOLECULES electrons are universal (identical for all electrons), and this amount of informa- tion is sufficient to explain many physical phenomena concerning electrons, once you know the inter actions. But is such little information sufficient to in- fer the complex behavior of human beings? Is it possible to quantify the nature of the interactions between human beings? The answers to these questions are on the negative. -

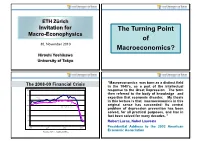

The Turning Point of Macroeconomics?

ETH Zürich Invitation for The Turning Point Macro-Econophysics of 30, November 2010 Macroeconomics? Hiroshi Yoshikawa University of Tokyo “Macroeconomics was born as a distinct field The 2008-09 Financial Crisis in the 1940‟s, as a part of the intellectual (2005=100) 130 response to the Great Depression. The term 120 then referred to the body of knowledge and Exports expertise that economic disaster. My thesis 110 in this lecture is that macroeconomics in this 100 original sense has succeeded: Its central Industrial Production problem of depression prevention has been 90 solved, for all practical purposes, and has in 80 fact been solved for many decades. ” 70 Robert Lucas, Nobel Laureate 60 2006 2007 2008 2009 Presidential Address to the 2003 American Economic Association Source: METI, Cabinet Office Neoclassical Economics “ Most macroeconomics of the past 30 years was spectacularly Price Mechanism useless at best, and positively or Markets harmful at worst.” Paul Krugman、June 2009 Pareto Efficiency at Lionel Robbins Lectures in London School of Economics Adam Smith (1776) Invisible Hand “The most interesting recent developments The Adjustment of Price in macroeconomic theory seem to me describable as the reincorporation of Equates aggregative problems such as inflation and the business cycle within the general Demand for and Supply of Apples framework of „microeconomic‟ theory. If Price of Apple these developments succeed, the term „macroeconomic‟ will simply disappear from S use and the modifier „micro‟ will become superfluous.” P* Robert Lucas (1987) D Quantity of Apples Q* Behind Demand and Supply Curves …. Equilibrium As a Point The Marginal Utilities of All the Consumers (j=1,…,J) out of Consuming Apples are Equal to the Price. -

The Fair and Laissez-Faire Markets: from a Neoliberal Laissez- Faire Baseline to a Fair Market

Pursuit - The Journal of Undergraduate Research at The University of Tennessee Volume 5 Issue 1 Article 8 June 2014 The Fair and Laissez-Faire Markets: From a Neoliberal Laissez- Faire Baseline to a Fair Market Eric L. Dixon University of Tennessee, Knoxville, [email protected] Follow this and additional works at: https://trace.tennessee.edu/pursuit Part of the Economic Policy Commons, Economic Theory Commons, Ethics and Political Philosophy Commons, Inequality and Stratification Commons, Political Economy Commons, and the Public Policy Commons Recommended Citation Dixon, Eric L. (2014) "The Fair and Laissez-Faire Markets: From a Neoliberal Laissez-Faire Baseline to a Fair Market," Pursuit - The Journal of Undergraduate Research at The University of Tennessee: Vol. 5 : Iss. 1 , Article 8. Available at: https://trace.tennessee.edu/pursuit/vol5/iss1/8 This Article is brought to you for free and open access by Volunteer, Open Access, Library Journals (VOL Journals), published in partnership with The University of Tennessee (UT) University Libraries. This article has been accepted for inclusion in Pursuit - The Journal of Undergraduate Research at The University of Tennessee by an authorized editor. For more information, please visit https://trace.tennessee.edu/pursuit. The Fair and Laissez-Faire Markets: From a Neoliberal Laissez-Faire Baseline to a Fair Market Cover Page Footnote I would like to thank David Reidy, Jon Garthoff, and especially Jon Shefner for their continued assistance of my studies in political economy and political philosophy. I would also like to thank my friends and family for their unconditional support. This article is available in Pursuit - The Journal of Undergraduate Research at The University of Tennessee: https://trace.tennessee.edu/pursuit/vol5/iss1/8 Pursuit: The Journal of Undergraduate Research at the University of Tennessee Copyright © The University of Tennessee PURSUIT trace.tennessee.edu/pursuit Fair & Laissez-Faire Markets: From a laissez-faire baseline to a fair market conception ERIC L. -

Survey of Self-Play in Reinforcement Learning

SURVEY OF SELF-PLAY IN REINFORCEMENT LEARNING APREPRINT Anthony DiGiovanni1 and Ethan Zell2 Departments of Statistics1 & Mathematics2 University of Michigan {adigi,ezell}@umich.edu July 8, 2021 ABSTRACT In reinforcement learning (RL), the term self-play describes a kind of multi-agent learning (MAL) that deploys an algorithm against copies of itself to test compatibility in various stochastic environments. As is typical in MAL, the literature draws heavily from well-established concepts in classical game theory and so this survey quickly reviews some fundamental concepts. In what follows, we present a brief survey of self-play literature, its major themes, criteria, and techniques, and then conclude with an assessment of current shortfalls of the literature as well as suggestions for future directions. 1 Introduction and Background Multi-agent learning (MAL) research aims to study interacting systems of agents in a shared environment, the incentives that govern the agents’ behavior, and the optimal way to behave in such environments. As we will see, the definitions of “optimality,” “environment,” and even “incentive” are crucial to developing useful problem statements and powerful solutions. Several agendas with distinct objectives and evaluation criteria have been developed for MAL [19]. From the perspective of online and reinforcement learning (RL), it is natural to formulate MAL as design of algorithms that can achieve a user’s goals optimally (or minimize regret), conditional on an environment induced by the actions taken by other algorithms. Model classes are constructed for this induced environment, on a spectrum from fully stochastic and equivalent to a Markov decision process (MDP) [4], to fully adversarial and unpredictable [3]. -

The Two Faces of Emergence in Economics

Swarthmore College Works Economics Faculty Works Economics 2007 The Two Faces Of Emergence In Economics Mark Kuperberg Swarthmore College, [email protected] Follow this and additional works at: https://works.swarthmore.edu/fac-economics Part of the Economics Commons Let us know how access to these works benefits ouy Recommended Citation Mark Kuperberg. (2007). "The Two Faces Of Emergence In Economics". Soundings. Volume 90, Issue 1/2. 49-63. https://works.swarthmore.edu/fac-economics/20 This work is brought to you for free by Swarthmore College Libraries' Works. It has been accepted for inclusion in Economics Faculty Works by an authorized administrator of Works. For more information, please contact [email protected]. THE TWO FACES OF EMERGENCE IN ECONOMICS Author(s): Mark Kuperberg Source: Soundings: An Interdisciplinary Journal, Vol. 90, No. 1/2, Emergence Theory (Spring/Summer 2007), pp. 49-63 Published by: Penn State University Press Stable URL: http://www.jstor.org/stable/41179190 Accessed: 04-10-2017 18:47 UTC REFERENCES Linked references are available on JSTOR for this article: http://www.jstor.org/stable/41179190?seq=1&cid=pdf-reference#references_tab_contents You may need to log in to JSTOR to access the linked references. JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about -

The Concept of "Efficiency" in Economics

WWS-597 REINHARDT THE CONCEPT OF "EFFICIENCY" IN ECONOMICS The concept of “efficiency” as used in economics is multi-faceted, as is shown in the chart below. First, a distinction is made between (a) efficiency in the production of goods and services and (b) (b) efficiency in the distribution of services from producers to end users. FIGURE 1 -- FACETS OF “ECONOMIC EFFICIENCY” IN AN ECONOMY OVERALL PARETO EFICIENCY IN THE ECONOMY EFFICIENCY IN Distribution of PRODUCTION available output among members of society in a Pareto efficient manner, given an initial Full use of Efficient (cost Production of Efficient (cost income distribution available minimizing) the right minimizing) distribution (whatever it may resources input combination channels from have been). in the combinations for of outputs producers to end users economy a given output desired by (transportation, society wholesale, retail, or advertising, etc). Maximum output for a given set of inputs Efficiency in production requires a) That available resources are fully used (which means among other things that en economic with involuntary unemployment is ipso facto inefficient) b) Real resources are used so as to maximize the total social value of the output to be had from any bundle of real resources or, which is the flip side, that any level of output with a given value to society be produced by the combination of real-resource inputs which minimizes the opportunity costs of those real resources. c) Producers collectively produce the right quantity and combination of out puts. d) that goods and services are carried from their producers to end users through cost-minimizing distribution channels.