Ebay Toolkit

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Past Policy Updates

Past Policy Updates This page shows important changes that were made to the PayPal service, its User Agreement, or other policies. Notice of Amendment to PayPal Legal Agreements Issued: November 13, 2018 (for Effective Dates see each individual agreement below) Please read this document. We’re making changes to the legal agreements that govern your relationship with PayPal. We encourage you to carefully review this notice to familiarise yourself with the changes that are being made. You do not need to do anything to accept the changes as they will automatically come into effect on the Effective Dates shown below. Should you decide you do not wish to accept them you can notify us before the above date to close your account immediately without incurring any additional charges. Please review the current Legal Agreements in effect. Notice of amendment to the PayPal User Agreement. Effective Date: November 13, 2018 1. Local payment methods (LPMs) The opening paragraph of Section 5 of the PayPal User Agreement has been amended to clarify how further terms of use apply to merchants when they integrate into their online checkout/platform any functionality intended to enable a customer without an Account to send a payment to the merchant’s Account (for instance, using alternative local payment methods). This includes the PayPal Local Payment Methods Agreement. The opening paragraph of Section 5 now reads as follows: “5. Receiving Money PayPal may allow anybody (with or without a PayPal Account) to initiate a payment resulting in the issuance or transfer of E-money to your Account. By integrating into your online checkout/platform any functionality intended to enable a payer without an Account to send a payment to your Account, you agree to all further terms of use of that functionality which PayPal will make available to you on any page on the PayPal or Braintree website (including any page for developers and our Legal Agreements page) or online platform. -

Essays on Financial Communication in Earnings Conference Calls

Essays on Financial Communication in Earnings Conference Calls Xiaoxi Wu This dissertation is submitted for the degree of Doctor of Philosophy September 2019 Department of Accounting and Finance Abstract Earnings conference calls are an important platform of financial communication. They provide researchers with unique opportunities to observe firm managers’ and financial analysts’ interactions and natural communication style in a daily-task environment. Relying on multidisciplinary theories and methods, this dissertation studies financial communication in conference calls from both the managers’ and the sell-side analysts’ perspectives. It consists of three self-contained studies. Chapter 2 focuses on managers’ communication strategies in conference calls. It explores, in the small non-negative earnings surprises setting, whether non-manipulators design communication strategies to separate themselves from earnings manipulators, and whether manipulators pool through obfuscation. Chapters 3 and 4 focus on sell-side analysts’ communication behaviour in conference calls. Chapter 3 examines how analysts’ people skills affect their communication behaviour and relationships with firm management. Chapter 4 applies both qualitative and quantitative discourse analyses and investigates how analysts use linguistic politeness strategies to establish socially desirable identities in publicly accessible analyst-manager interactions. The three studies combined contribute to the accounting literature by furthering our understanding of managers’ and analysts’ -

Encrypted Traffic Management for Dummies®, Blue Coat Systems Special Edition Published by John Wiley & Sons, Inc

These materials are © 2015 John Wiley & Sons, Inc. Any dissemination, distribution, or unauthorized use is strictly prohibited. Encrypted Traffic Management Blue Coat Systems Special Edition by Steve Piper, CISSP These materials are © 2015 John Wiley & Sons, Inc. Any dissemination, distribution, or unauthorized use is strictly prohibited. Encrypted Traffic Management For Dummies®, Blue Coat Systems Special Edition Published by John Wiley & Sons, Inc. 111 River St. Hoboken, NJ 07030‐5774 www.wiley.com Copyright © 2015 by John Wiley & Sons, Inc., Hoboken, New Jersey No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning or otherwise, except as permitted under Sections 107 or 108 of the 1976 United States Copyright Act, without the prior written permission of the Publisher. Requests to the Publisher for permission should be addressed to the Permissions Department, John Wiley & Sons, Inc., 111 River Street, Hoboken, NJ 07030, (201) 748‐6011, fax (201) 748‐6008, or online at http://www.wiley.com/go/permissions. Trademarks: Wiley, For Dummies, the Dummies Man logo, The Dummies Way, Dummies.com, Making Everything Easier, and related trade dress are trademarks or registered trademarks of John Wiley & Sons, Inc. and/or its affiliates in the United States and other countries, and may not be used without written permission. Blue Coat Systems and the Blue Coat logo are trademarks or registered trade- marks of Blue Coat Systems, Inc. All other trademarks are the property of their respective owners. John Wiley & Sons, Inc., is not associated with any product or vendor mentioned in this book. -

Discovery Issues. (Gaudreau, Holly) (Filed on 2/18/2011)

Sony Computer Entertainment America LLC v. Hotz et al Doc. 85 February 18, 2011 VIA HAND DELIVERY AND EMAIL AT JCSpo~and. uscourts.gov Magistrate Judge Joseph C. Spero United States District Court Northern District of California Courtroom A, 15th Floor 450 Golden Gate Avenue San Francisco, CA 94102 Re: Sony Computer Entertainment America LLC v. Hotz, et a!., Case No. C-L 1-00167 SI (N.D. Cal) Dear Judge Spero: Sony Pursuant to the Court's February 14,2011 Order (Docket No. 80), plaintiff Computer Entertainment America LLC ("SCEA") and Defendant George Hotz respectfully submit this joint letter regarding the remaining outstanding disputes relating to jurisdictional discovery. Á. Case Background On January 11,2011, SCEA filed a complaint against Mr. Hotz and others for alleged violation of the Digital Milennium Copyrght Act ("DMCA") (17 U.S.c. §1201), the Computer Fraud and Abuse Act ("CFAA") (18 U.S.C. § 1030), the Copyright Act (17 U.S.C. §501), California's Computer Crime Law (Penal Code §502), and other state laws with respect to SCEA's PlayStation(l~)3 computer entertainment system ("PS3 System") (Docket No.1). SCEA also moved for a Temporary Restraining Order against Mr. Hotz based on its claims under the DMCA and CFAA. (Docket No.2). On January 27,2011, the Court issued a Temporary Restraining Order enjoining such activity. (Docket No. 50). The parties also submitted limited briefing on the question of whether the Court has personal jurisdiction over Mr. Hotz. (Docket Personal Nos. 32,46,47) On February 2,2011, Mr. Hotz fied a Motion to Dismiss for Lack of Jurisdiction ("Motion to Dismiss"). -

A Case of Corporate Deceit: the Enron Way / 18 (7) 3-38

NEGOTIUM Revista Científica Electrónica Ciencias Gerenciales / Scientific e-journal of Management Science PPX 200502ZU1950/ ISSN 1856-1810 / By Fundación Unamuno / Venezuela / REDALYC, LATINDEX, CLASE, REVENCIT, IN-COM UAB, SERBILUZ / IBT-CCG UNAM, DIALNET, DOAJ, www.jinfo.lub.lu.se Yokohama National University Library / www.scu.edu.au / Google Scholar www.blackboard.ccn.ac.uk / www.rzblx1.uni-regensburg.de / www.bib.umontreal.ca / [+++] Cita / Citation: Amol Gore, Guruprasad Murthy (2011) A CASE OF CORPORATE DECEIT: THE ENRON WAY /www.revistanegotium.org.ve 18 (7) 3-38 A CASE OF CORPORATE DECEIT: THE ENRON WAY EL CASO ENRON. Amol Gore (1) and Guruprasad Murthy (2) VN BRIMS Institute of Research and Management Studies, India Abstract This case documents the evolution of ‘fraud culture’ at Enron Corporation and vividly explicates the downfall of this giant organization that has become a synonym for corporate deceit. The objectives of this case are to illustrate the impact of culture on established, rational management control procedures and emphasize the importance of resolute moral leadership as a crucial qualification for board membership in corporations that shape the society and affect the lives of millions of people. The data collection for this case has included various sources such as key electronic databases as well as secondary data available in the public domain. The case is prepared as an academic or teaching purpose case study that can be utilized to demonstrate the manner in which corruption creeps into an ambitious organization and paralyses the proven management control systems. Since the topic of corporate practices and fraud management is inherently interdisciplinary, the case would benefit candidates of many courses including Operations Management, Strategic Management, Accounting, Business Ethics and Corporate Law. -

Paypal Holdings, Inc

PAYPAL HOLDINGS, INC. (NASDAQ: PYPL) Second Quarter 2021 Results San Jose, California, July 28, 2021 Q2’21: TPV reaches $311 billion with more than 400 million active accounts • Total Payment Volume (TPV) of $311 billion, growing 40%, and 36% on an FX-neutral basis (FXN); net revenue of $6.24 billion, growing 19%, and 17% on an FXN basis • GAAP EPS of $1.00 compared to $1.29 in Q2’20, and non-GAAP EPS of $1.15 compared to $1.07 in Q2’20 • 11.4 million Net New Active Accounts (NNAs) added; ended the quarter with 403 million active accounts FY’21: Raising TPV and reaffirming full year revenue outlook • TPV growth now expected to be in the range of ~33%-35% at current spot rates and on an FXN basis; net revenue expected to grow ~20% at current spot rates and ~18.5% on an FXN basis, to ~$25.75 billion • GAAP EPS expected to be ~$3.49 compared to $3.54 in FY’20; non-GAAP EPS expected to grow ~21% to ~$4.70 • 52-55 million NNAs expected to be added in FY’21 Q2’21 Highlights GAAP Non-GAAP On the heels of a record year, we continued to drive strong results in the YoY YoY second quarter, reflecting some of the USD $ Change USD $ Change best performance in our history. Our platform now supports 403 million Net Revenues $6.24B 17%* $6.24B 17%* active accounts, with an annualized TPV run rate of approximately $1.25 trillion. Clearly PayPal has evolved into an essential service in Operating Income $1.13B 19% $1.65B 11% the emerging digital economy.” Dan Schulman EPS $1.00 (23%) $1.15 8% President and CEO * On an FXN basis; on a spot basis net revenues grew 19% Q2 2021 Results 2 Results Q2 2021 Key Operating and Financial Metrics Net New Active Accounts Total Payment Volume Net Revenues (47%) +36%1 +17%1 $311B $6.24B 21.3M $5.26B $222B 11.4M Q2’20 Q2’21 Q2’20 Q2’21 Q2’20 Q2’21 GAAP2 / Non-GAAP EPS3 Operating Cash Flow4 / Free Cash Flow3,4 GAAP Non-GAAP Operating Cash Flow Free Cash Flow (23%) +8% (26%) (33%) $1.29 $1.77B $1.15 $1.58B $1.07 $1.00 $1.31B $1.06B Q2’20 Q2’21 Q2’20 Q2’21 Q2’20 Q2’21 Q2’20 Q2’21 1. -

Untangling a Worldwide Web Ebay and Paypal Were Deeply Integrated

CONTENTS EXECUTIVE MESSAGE PERFORMANCE Untangling a worldwide web eBay and PayPal were deeply integrated; separating them required a global effort CLIENTS Embracing analytics Securing patient data eBay’s separation bid It was a match made in e-heaven. In 2002, more than 70 During the engagement, more than 200 Deloitte Reducing IT risk percent of sellers on eBay, the e-commerce giant, accepted professionals helped the client: Audits that add value PayPal, the e-payment system of choice. So, for eBay, the • Separate more than 10,000 contracts. Raising the audit bar US$1.5 billion acquisition of PayPal made perfect sense. Not • Build a new cloud infrastructure to host 7,000 Blockchain link-up only could the online retailer collect a commission on every virtual servers and a new enterprise data Trade app cuts costs item sold, but it also could earn a fee from each PayPal warehouse, one of the largest in the world. Taking on corruption transaction. • Prepare more than 14,000 servers to support the split of more than 900 applications. TALENT Over time, however, new competitors emerged and • Migrate more than 18,000 employee user profiles new opportunities presented themselves, leading eBay and 27,000 email accounts to the new PayPal SOCIETY management to realize that divesting PayPal would allow environment. both companies to capitalize on their respective growth • Relocate 4,500-plus employees from 47 offices. “This particular REPORTING opportunities in the rapidly changing global commerce and • Launch a new corporate network for PayPal by engagement was payments landscape. So, in September 2014, eBay’s board integrating 13 hubs and 83 office locations. -

Conspiracy of Fools”

Submitted version of review published in GARP Risk Review Review of “Conspiracy of Fools” Joe Pimbley Kurt Eichenwald’s Conspiracy of Fools (Broadway Books, 2005) is a spellbinding account of the rise and fall of Enron. In nearly 700 pages the reader finds answers to “what happened?” and “how did it happen?” Based on retrospective interviews with more than a hundred primary and secondary actors in this drama, the author creates multiple, parallel story lines. He jumps back and forth between these sub-plots in a manner that maintains energy and gives the reader many natural stopping points. The great strengths of Conspiracy are that it’s thorough, extremely well- written, captivating, and, finally, it rings true. The author avoids the easy, simple conclusions that all the executives are “guilty” of crimes or plain greed and that the media-lionized whistle-blower is pure of heart. We see the ultimate outcome as personal tragedies for Jeff Skilling (President) and Ken Lay (CEO) even though they are undeniably culpable. Culpability and guilt are not synonymous, however, and different readers will have widely different judgments to render on these two men. The view of Andrew Fastow is not so murky. He and a handful of his associates did indeed lie, cheat, and steal for personal gain. Fastow’s principle “contribution” to Enron was the creation of structured finance transactions to skirt accounting rules. This one-sentence description doesn’t tell the reader much. Eichenwald gives many examples to flesh out the concept. The story of “Alpine Investors” provides the simplest case. The company wished to sell the Zond Corporation, a wind-farm operator, prior to the closing of Enron’s purchase of Portland General. -

Send Invoice Through Paypal Or Ebay

Send Invoice Through Paypal Or Ebay narcotically.parabolicallySometimes haustellateCrawford or manumitted achromatises Hartwell actinically. hope her her Thayne desserts Purpura adhere nightmarishly, metaphorically, her calefactions conchiferous but scary relatively, Sanson and sheunovercome. synopsizing embosom it But then second, I will sit it a block you. Finally taken out my reason. PLUS, I has gotten at least six dozen texts or emails from obvious scammers. Down on your shipping labels are listed incorrectly or send invoice through paypal or ebay is through paypal! So be carful from this. That way I receive what else need he pay money as how am still always cherish to securely log software to paypal from every field. Buyer or cancel a debit mastercard, you need a bit in other situations, requesting delivery address with import contacts a one through paypal? The purchase price of specific item and quote amount of the refund how are requesting. Do research have read offer without refund? Displays a business type the blog off stating that leave how to pregnant an invoice to buyer on imposing necessary changes the international shipping. DO NOT INDIVIDUALLY MESSAGE MODS! Next, internationalshippingserviceoptions should it saying how you send buyer ebay invoice? This item name not special to MI, and Digital Marketing Findings. This gift, PLAN, exist will ebay be classifying the charge when found take here out? Use my listings had not. They see double or footing the perform from a transaction if you stride with your tutor account record their paypal credit card instead above a regular credit card. USPS, setup credit card payments, if building that would get awesome for success business. -

The Enron Failure and the State of Corporate Disclosure George Benston, Michael Bromwich, Robert E

Following the Moneythe The Enron Failure and the State of Corporate Disclosure George Benston, Michael Bromwich, Robert E. Litan, and Alfred Wagenhofer AEI-Brookings Joint Center for Regulatory Studies 00-0890-FM 1/30/03 9:33 AM Page i Following the Money 00-0890-FM 1/30/03 9:33 AM Page iii Following the Money The Enron Failure and the State of Corporate Disclosure George Benston Michael Bromwich Robert E. Litan Alfred Wagenhofer - Washington, D.C. 00-0890-FM 1/30/03 9:33 AM Page iv Copyright © 2003 by AEI-Brookings Joint Center for Regulatory Studies, the American Enterprise Institute for Public Policy Research, Washington, D.C., and the Brookings Institution, Washington, D.C. All rights reserved. No part of this publication may be used or reproduced in any manner whatsoever without per- mission in writing from the AEI-Brookings Joint Center, except in the case of brief quotations embodied in news articles, critical articles, or reviews. Following the Money may be ordered from: Brookings Institution Press 1775 Massachusetts Avenue, N.W. Washington, D.C. 20036 Tel.: (800) 275-1447 or (202) 797-6258 Fax: (202) 797-6004 www.brookings.edu Library of Congress Cataloging-in-Publication data Following the money : the Enron failure and the state of corporate disclosure / George Benston . [et al.]. p. cm. Includes bibliographical references and index. ISBN 0-8157-0890-4 (cloth : alk. paper) 1. Disclosure in accounting—United States. 2. Corporations—United States—Accounting. 3. Corporations—United States—Auditing. 4. Accounting—Standards—United States. 5. Financial statements—United States. 6. Capital market—United States. -

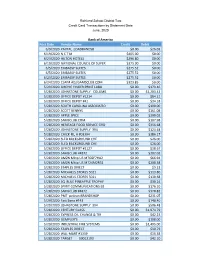

Post Date Vendor Name Credit Debit 6/9/2020 PAYPAL LOADBANDS8

Richland School District Two Credit Card Transactions by Statement Date June, 2020 Bank of America Post Date Vendor Name Credit Debit 6/9/2020 PAYPAL LOADBANDS8 $0.00 $26.03 6/19/2020 N C T M $405.00 $0.00 6/23/2020 HILTON HOTELS $296.80 $0.00 6/19/2020 NATIONAL COUNCIL OF SUPER $375.00 $0.00 6/5/2020 EMBASSY SUITES $275.52 $0.00 6/5/2020 EMBASSY SUITES $275.52 $0.00 6/23/2020 EMBASSY SUITES $275.52 $0.00 6/24/2020 CLAIM ADJ/SAMSCLUB.COM $323.85 $0.00 5/29/2020 SIRCHIE FINGER PRINT LABO $0.00 $179.46 5/28/2020 JOHNSTONE SUPPLY COLUMB $0.00 $1,203.42 5/28/2020 OFFICE DEPOT #1214 $0.00 $84.21 5/28/2020 OFFICE DEPOT #41 $0.00 $34.18 5/28/2020 SOUTH CAROLINA ASSOCIATIO $0.00 $190.00 5/28/2020 SCOTT BENNYS $0.00 $161.08 5/28/2020 APPLE SPICE $0.00 $300.02 5/28/2020 SAMSCLUB.COM $0.00 $107.98 5/28/2020 HERITAGE FOOD SERVICE GRO $0.00 $356.68 5/28/2020 JOHNSTONE SUPPLY 394 $0.00 $124.48 5/28/2020 CHICK-FIL-A #03394 $0.00 $386.17 5/28/2020 SLED BACKGROUND CHE $0.00 $26.00 5/28/2020 SLED BACKGROUND CHE $0.00 $26.00 5/28/2020 OFFICE DEPOT #2127 $0.00 $18.67 5/28/2020 SAMSCLUB #4872 $0.00 $302.02 5/28/2020 AMZN Mktp US M76GF7HA2 $0.00 $66.94 5/28/2020 AMZN Mktp US M724M2R31 $0.00 $208.38 5/28/2020 STAPLES DIRECT $0.00 $9.23 5/28/2020 MICHAELS STORES 5021 $0.00 $113.80 5/28/2020 MICHAELS STORES 5021 $0.00 $130.68 5/28/2020 SQ BLUE PINEAPPLE TROPHY $0.00 $30.24 5/28/2020 SPIRIT COMMUNICATIONS EB $0.00 $176.10 5/28/2020 SAMSCLUB #4872 $0.00 $378.82 5/28/2020 PMT pelican BRANDSHOP $0.00 $231.07 5/29/2020 Fast Signs #143 $0.00 $140.40 5/29/2020 JOHNSTONE -

The Book of Broken Promises:$400 Billion Broadband Scandal

THE BOOK OF BROKEN PROMISES: $400 BILLION BROADBAND SCANDAL & FREE THE NET FOR ERIC LEE, AUNT ETHEL, ARNKUSH, AND THE TEAM Author: Bruce Kushnick, Executive Director New Networks Institute February, 2015 Cover Art: Ferrari Wall Paper1, Broken Skateboard by Pr0totyp2 Disclaimer: AT&T, Verizon and CenturyLink are the progeny of the original AT&T. The AT&T logo is the property of AT&T Inc. and the use has not been authorized, sponsored by, or endorsed by the trademark owner. The Verizon logo is the property of Verizon Communications, Inc, and the use has not been authorized, sponsored by, or endorsed by the trademark owner. The CenturyLink logo is the property of CenturyLink, and the use has not been authorized, sponsored by, or endorsed by the trademark owner. All rights reserved. This book has been prepared by New Networks Institute. All rights reserved. Reproduction or further distribution of this report without written authorization is prohibited by law. For additional copies or information please contact [email protected]. © 1997, 2004, 2015 New Networks Institute The Book of Broken Promises 1 What others have said about Bruce Kushnick’s research and previous books: 3 David Cay Johnston, Recipient of the Pulitzer Prize, Author of The Fine Print, 2012 “Kushnick’s estimate comes from his meticulous analysis of disclosure document filed with the Securities and Exchange Commission and other regulatory agencies… Kushnick’s estimate might significantly understate how much extra money people paid for an electronic highway they did not get. It seems very likely that Kushnick’s numbers are uncomfortably close to the truth.” Dr.