For Immediate Release

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Organization Sector Report Title Publication Year Report Type

GRI Reports List 2012(Japan) last updated: April 2013 Organization Sector Report Title Publication Year Report type Application Level Status Adeka Chemicals CSR Report 2012 2012 GRI - Referenced Advantest Technology Hardware Corporate Report 2012 2012 GRI - Referenced AEON Retailers Environmental and Social Report 2012 2012 GRI - Referenced Aeon Retailers Environmental & Social Initiatives 2012 2012 Non - GRI Aishin Seiki Equipment Aisin Report 2012 2012 GRI - Referenced Ajinomoto Food and Beverage Products Sustainability Report 2012 2012 Non - GRI All Nippon Airways Coompany Limited Aviation Annual Report 2012 Non - GRI Asahi Glass Company Chemicals AGC Report 2012 2012 GRI - Referenced Asahi Group Holdings Food and Beverage Products CSR Communication Report 2012 2012 GRI - Referenced Asahi Kasei Chemicals CSR Report 2012 2012 GRI - Referenced Astellas Pharma Health Care Products Annual Report 2012 2012 GRI - G3.1 B Self-declared azbil Conglomerates azbil Report 2012 2012 Non - GRI Benesse Holdings, Inc. Other Benesse Report 2012 2012 GRI - Referenced Bridgestone Chemicals CSR Report 2012 2012 GRI - Referenced Brother Technology Hardware CSR Report 2012 2012 GRI - Referenced Canon Technology Hardware Sustainability Report 2012 2012 GRI - Referenced Casio Consumer Durables Sustainability Report 2012 2012 GRI - G3.1 B Self-declared Chiyoda Corporation Construction CSR Report 2012 2012 GRI - Referenced Chubu Electric Power Energy Annual Report 2012 2012 GRI - Referenced Citizen Holdings Conglomerates CSR Report 2012 2012 GRI - Referenced -

Published on July 21, 2021 1. Changes in Constituents 2

Results of the Periodic Review and Component Stocks of Tokyo Stock Exchange Dividend Focus 100 Index (Effective July 30, 2021) Published on July 21, 2021 1. Changes in Constituents Addition(18) Deletion(18) CodeName Code Name 1414SHO-BOND Holdings Co.,Ltd. 1801 TAISEI CORPORATION 2154BeNext-Yumeshin Group Co. 1802 OBAYASHI CORPORATION 3191JOYFUL HONDA CO.,LTD. 1812 KAJIMA CORPORATION 4452Kao Corporation 2502 Asahi Group Holdings,Ltd. 5401NIPPON STEEL CORPORATION 4004 Showa Denko K.K. 5713Sumitomo Metal Mining Co.,Ltd. 4183 Mitsui Chemicals,Inc. 5802Sumitomo Electric Industries,Ltd. 4204 Sekisui Chemical Co.,Ltd. 5851RYOBI LIMITED 4324 DENTSU GROUP INC. 6028TechnoPro Holdings,Inc. 4768 OTSUKA CORPORATION 6502TOSHIBA CORPORATION 4927 POLA ORBIS HOLDINGS INC. 6503Mitsubishi Electric Corporation 5105 Toyo Tire Corporation 6988NITTO DENKO CORPORATION 5301 TOKAI CARBON CO.,LTD. 7011Mitsubishi Heavy Industries,Ltd. 6269 MODEC,INC. 7202ISUZU MOTORS LIMITED 6448 BROTHER INDUSTRIES,LTD. 7267HONDA MOTOR CO.,LTD. 6501 Hitachi,Ltd. 7956PIGEON CORPORATION 7270 SUBARU CORPORATION 9062NIPPON EXPRESS CO.,LTD. 8015 TOYOTA TSUSHO CORPORATION 9101Nippon Yusen Kabushiki Kaisha 8473 SBI Holdings,Inc. 2.Dividend yield (estimated) 3.50% 3. Constituent Issues (sort by local code) No. local code name 1 1414 SHO-BOND Holdings Co.,Ltd. 2 1605 INPEX CORPORATION 3 1878 DAITO TRUST CONSTRUCTION CO.,LTD. 4 1911 Sumitomo Forestry Co.,Ltd. 5 1925 DAIWA HOUSE INDUSTRY CO.,LTD. 6 1954 Nippon Koei Co.,Ltd. 7 2154 BeNext-Yumeshin Group Co. 8 2503 Kirin Holdings Company,Limited 9 2579 Coca-Cola Bottlers Japan Holdings Inc. 10 2914 JAPAN TOBACCO INC. 11 3003 Hulic Co.,Ltd. 12 3105 Nisshinbo Holdings Inc. 13 3191 JOYFUL HONDA CO.,LTD. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

STOXX Japan 50 Last Updated: 03.08.2015

STOXX Japan 50 Last Updated: 03.08.2015 Rank Rank (PREVIOUS ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) ) JP3633400001 6900643 7203.T 690064 Toyota Motor Corp. JP JPY Y 176.4 1 1 JP3902900004 6335171 8306.T 659668 Mitsubishi UFJ Financial Group JP JPY Y 93.2 2 2 JP3890350006 6563024 8316.T 656302 Sumitomo Mitsui Financial Grou JP JPY Y 57.3 3 3 JP3854600008 6435145 7267.T 643514 Honda Motor Co. Ltd. JP JPY Y 52.7 4 4 JP3436100006 6770620 9984.T 677062 Softbank Group Corp. JP JPY Y 48.7 5 5 JP3885780001 6591014 8411.T 625024 Mizuho Financial Group Inc. JP JPY Y 47.9 6 6 JP3735400008 6641373 9432.T 664137 Nippon Telegraph & Telephone C JP JPY Y 45.5 7 7 JP3496400007 6248990 9433.T 624899 KDDI Corp. JP JPY Y 42.9 8 8 JP3726800000 6474535 2914.T 647453 Japan Tobacco Inc. JP JPY Y 39.5 9 10 JP3783600004 6298542 9020.T 629854 East Japan Railway Co. JP JPY Y 35.2 10 16 JP3802300008 6332439 9983.T 633243 Fast Retailing Co. Ltd. JP JPY Y 34.9 11 17 JP3422950000 B0FS5D6 3382.T 679717 Seven & I Holdings Co. Ltd. JP JPY Y 34.2 12 18 JP3463000004 6870445 4502.T 687044 Takeda Pharmaceutical Co. Ltd. JP JPY Y 33.5 13 14 JP3566800003 6183552 9022.T 618355 Central Japan Railway Co. JP JPY Y 32.7 14 11 JP3898400001 6596785 8058.T 659678 Mitsubishi Corp. JP JPY Y 31.8 15 13 JP3242800005 6172323 7751.T 617232 Canon Inc. -

Notice Regarding Execution of Share Exchange Agreement Concerning Nisshinbo Holdings Inc

[Translation] The share exchange described in this press release involves securities of a Japanese company. The offer is subject to disclosure requirements of Japan that are different from those of the United States. Financial information included in this document, if any, was excerpted from financial statements prepared in accordance with non-U.S. accounting standards that may not be comparable to the financial statements of United States companies. It may be difficult for you to enforce your rights and any claim you may have arising under the U.S. federal securities laws, since the issuer is located in Japan and all of its officers and directors reside outside of the United States. You may not be able to sue a Japanese company or its officers or directors in a Japanese court for violations of the U.S. securities laws. It may be difficult to compel a Japanese company and its affiliates to subject themselves to a U.S. court’s judgment. You should be aware that the issuer may purchase securities otherwise than under the share exchange, such as in open market or privately negotiated purchases. This document has been translated from the Japanese-language original for reference purposes only. While this English translation is believed to be generally accurate, it is subject to, and qualified by, in its entirety, the Japanese-language original. Such Japanese-language original shall be the controlling document for all purposes. May 10, 2018 For immediate release Company: Nisshinbo Holdings Inc. Representative: Masaya Kawata, President Securities Code: 3105 TFS (First Section); NSE (First Section); SSE; FSE Contact: Investor Relations & Public Relations Group (Tel: 03-5695-8854) Company: New Japan Radio Co., Ltd. -

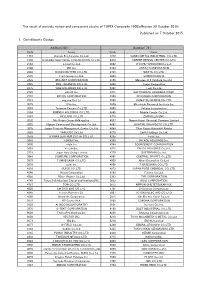

Published on 7 October 2016 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 31 October 2016) Published on 7 October 2016 1. Constituents Change Addition( 70 ) Deletion( 60 ) Code Issue Code Issue 1810 MATSUI CONSTRUCTION CO.,LTD. 1868 Mitsui Home Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 2196 ESCRIT INC. 2117 Nissin Sugar Co.,Ltd. 2198 IKK Inc. 2124 JAC Recruitment Co.,Ltd. 2418 TSUKADA GLOBAL HOLDINGS Inc. 2170 Link and Motivation Inc. 3079 DVx Inc. 2337 Ichigo Inc. 3093 Treasure Factory Co.,LTD. 2359 CORE CORPORATION 3194 KIRINDO HOLDINGS CO.,LTD. 2429 WORLD HOLDINGS CO.,LTD. 3205 DAIDOH LIMITED 2462 J-COM Holdings Co.,Ltd. 3667 enish,inc. 2485 TEAR Corporation 3834 ASAHI Net,Inc. 2492 Infomart Corporation 3946 TOMOKU CO.,LTD. 2915 KENKO Mayonnaise Co.,Ltd. 4221 Okura Industrial Co.,Ltd. 3179 Syuppin Co.,Ltd. 4238 Miraial Co.,Ltd. 3193 Torikizoku co.,ltd. 4331 TAKE AND GIVE. NEEDS Co.,Ltd. 3196 HOTLAND Co.,Ltd. 4406 New Japan Chemical Co.,Ltd. 3199 Watahan & Co.,Ltd. 4538 Fuso Pharmaceutical Industries,Ltd. 3244 Samty Co.,Ltd. 4550 Nissui Pharmaceutical Co.,Ltd. 3250 A.D.Works Co.,Ltd. 4636 T&K TOKA CO.,LTD. 3543 KOMEDA Holdings Co.,Ltd. 4651 SANIX INCORPORATED 3636 Mitsubishi Research Institute,Inc. 4809 Paraca Inc. 3654 HITO-Communications,Inc. 5204 ISHIZUKA GLASS CO.,LTD. 3666 TECNOS JAPAN INCORPORATED 5998 Advanex Inc. 3678 MEDIA DO Co.,Ltd. 6203 Howa Machinery,Ltd. 3688 VOYAGE GROUP,INC. 6319 SNT CORPORATION 3694 OPTiM CORPORATION 6362 Ishii Iron Works Co.,Ltd. 3724 VeriServe Corporation 6373 DAIDO KOGYO CO.,LTD. 3765 GungHo Online Entertainment,Inc. -

Important Notice the Depository Trust Company

Important Notice The Depository Trust Company B #: 14454-20 Date: December 24, 2020 To: All Participants Category: TaxRelief, Distributions From: International Services Attention: Operations, Reorg & Dividend Managers, Partners & Cashiers Tax Relief – Country: JAPAN Depositary for Unsponsored DR Program: BNYM Securities: See Below Subject: CUSIP(s): Please refer to Dividend Event Matrix for list of CUSIPs Record Date: 12/30/2020 Payable Date: TBD CA Web Instruction Deadline: 01/20/2021 8:00 PM ET Participants can use DTC’s Corporate Actions Web (CA Web) service to certify all or a portion of their position entitled to the applicable withholding tax rate. Participants are urged to consult TaxInfo respectively before certifying their instructions over the CA Web. Important: Prior to certify listing tax withholding instructions, participants are urged to read, understand and comply with the information in the Legal Conditions category found on TaxInfo on the CA Web. Questions regarding this Important Notice may be directed to GlobeTax 212-747-9100. Important Legal Information: The Depository Trust Company (“DTC”) does not represent or warrant the accuracy, adequacy, timeliness, completeness or fitness for any particular purpose of the information contained in this communication, which is based in part on information obtained from third parties and not independently verified by DTC and which is provided as is. The information contained in this communication is not intended to be a substitute for obtaining tax advice from an appropriate professional advisor. In providing this communication, DTC shall not be liable for (1) any loss resulting directly or indirectly from mistakes, errors, omissions, interruptions, delays or defects in such communication, unless caused directly by gross negligence or willful misconduct on the part of DTC, and (2) any special, consequential, exemplary, incidental or punitive damages. -

Notice Regarding Absorption-Type Demerger and Sale of Subsidiary Shares by Nisshinbo Brake Inc

[Translation] [NOTICE: Please note that the following is a translation of the Japanese language original for convenience purposes only, and in the event of any discrepancy, the Japanese language original shall prevail.] August 30, 2017 For immediate release Company: Nisshinbo Holdings Inc. Representative: President Masaya Kawata Securities Code: 3105 TSE (First Section); NSE (First Section); SSE; FSE Notice Regarding Absorption-Type Demerger and Sale of Subsidiary Shares by Nisshinbo Brake Inc. for the Purpose of Transferring the Foundation Brake Business At the Board of Directors meeting held today (August 30, 2017), Nisshinbo Holdings Inc. resolved to transfer (the “Transaction”) the Foundation Brake Business (the “Transferred Business”), part of the Automobile Brake Business of its consolidated subsidiaries including Nisshinbo Brake Inc. (“Nisshinbo Brake” or the “Demerging Company”), to Hosei Brake Industry Co., Ltd. (“Hosei Brake Industry”), a major subsidiary of the Aisin Seiki Group (the “Aisin Group”). The Transaction is intended to consist of the transfer of the assets, liabilities, rights, and obligations held by Nisshinbo Brake with respect to the Transferred Business to a wholly-owned subsidiary that Nisshinbo Brake will newly establish (the “New Company” or the “Successor Company”) through a demerger (the “Demerger”), followed by the sale of all of the outstanding shares of the New Company to Hosei Brake Industry (the “Share Sale”). I. Purpose of the Transaction The Nisshinbo Group operates its various businesses with the aim of being a group of “Environment and Energy Companies” that contributes to a secure society by proposing solutions to the problems that humanity faces, such as environmental degradation and global warming. -

Stoxx® Japan 600 Esg-X Index

STOXX® JAPAN 600 ESG-X INDEX Components1 Company Supersector Country Weight (%) Toyota Motor Corp. Automobiles & Parts Japan 3.87 Sony Corp. Consumer Products & Services Japan 2.55 Softbank Group Corp. Telecommunications Japan 2.44 Keyence Corp. Industrial Goods & Services Japan 1.77 RECRUIT HOLDINGS Industrial Goods & Services Japan 1.54 Mitsubishi UFJ Financial Group Banks Japan 1.48 Shin-Etsu Chemical Co. Ltd. Chemicals Japan 1.36 Nippon Telegraph & Telephone C Telecommunications Japan 1.36 Nintendo Co. Ltd. Consumer Products & Services Japan 1.30 Nidec Corp. Technology Japan 1.30 Fast Retailing Co. Ltd. Retail Japan 1.25 Daikin Industries Ltd. Construction & Materials Japan 1.19 Takeda Pharmaceutical Co. Ltd. Health Care Japan 1.18 Tokyo Electron Ltd. Technology Japan 1.16 Honda Motor Co. Ltd. Automobiles & Parts Japan 1.10 Daiichi Sankyo Co. Ltd. Health Care Japan 1.08 Sumitomo Mitsui Financial Grou Banks Japan 1.04 Murata Manufacturing Co. Ltd. Technology Japan 1.03 KDDI Corp. Telecommunications Japan 1.02 Hitachi Ltd. Industrial Goods & Services Japan 0.92 Itochu Corp. Industrial Goods & Services Japan 0.92 Fanuc Ltd. Industrial Goods & Services Japan 0.90 Hoya Corp. Health Care Japan 0.84 Mitsubishi Corp. Industrial Goods & Services Japan 0.83 Mizuho Financial Group Inc. Banks Japan 0.76 SOFTBANK Telecommunications Japan 0.75 Denso Corp. Automobiles & Parts Japan 0.72 Mitsui & Co. Ltd. Industrial Goods & Services Japan 0.71 Tokio Marine Holdings Inc. Insurance Japan 0.70 Oriental Land Co. Ltd. Travel & Leisure Japan 0.68 SMC Corp. Industrial Goods & Services Japan 0.68 Mitsubishi Electric Corp. Industrial Goods & Services Japan 0.67 Seven & I Holdings Co. -

Nisshinbo Group CSR Report 2009 Nisshinbo Group 2009 CSR Report

Nisshinbo Group CSR Report 2009 Nisshinbo Group 2009 CSR Report Foreword Nisshinbo Industries, Inc. adopted a holding company structure in April 2009. In accordance with this change, Nisshinbo Holdings Inc. will issue the Group’s CSR reports starting this year. Business Segment Core Company Holding Company Textiles Nisshinbo Textile Inc. Automobile Brakes Nisshinbo Brake Inc. Nisshinbo Holdings Inc. Papers Nisshinbo Paper Products Inc. Mechatronics Nisshinbo Mechatronics Inc. Chemicals Nisshinbo Chemical Inc. Electronics New Japan Radio Co., Ltd. Period Covered Sources for Additional Information The period covered is the fiscal year ended March Nisshinbo Annual Report (Japanese and 2009 (April 1, 2008 to March 31, 2009), but some English) information from other periods is also included. Financial Results (Japanese) Business Report and Shareholders Report for Scope of Report the 166th Fiscal Term (Japanese) The scope of this report includes all Nisshinbo Securities Report (Japanese) Group companies subject to consolidated reporting, but the Overview of the Nisshinbo Group on page These documents can be downloaded from the Nisshinbo Holdings website. 4 covers only Nisshinbo Holdings and its consolidated subsidiaries. URL (Investor Relations page): http://www.nisshinbo.co.jp/english/ir/library/index.html Guidelines Used for Reference ・ Environmental Reporting Guidelines 2007, Ministry of the Environment ・ Environmental Accounting Guidelines 2005, Ministry of the Environment ・ Sustainability Reporting Guidelines, Third Edition, Global Reporting Initiative Note In this report, “the Company” refers to Nisshinbo Holdings Inc., and “the Company and its five core subsidiaries” refers to the scope of Nisshinbo Industries, Inc. prior to the corporate split. Executive Message 2 Overview of the Nisshinbo Group 1. -

Published on 7 October 2015 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 30 October 2015) Published on 7 October 2015 1. Constituents Change Addition( 80 ) Deletion( 72 ) Code Issue Code Issue 1712 Daiseki Eco.Solution Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 1930 HOKURIKU ELECTRICAL CONSTRUCTION CO.,LTD. 2410 CAREER DESIGN CENTER CO.,LTD. 2183 Linical Co.,Ltd. 2692 ITOCHU-SHOKUHIN Co.,Ltd. 2198 IKK Inc. 2733 ARATA CORPORATION 2266 ROKKO BUTTER CO.,LTD. 2735 WATTS CO.,LTD. 2372 I'rom Group Co.,Ltd. 3004 SHINYEI KAISHA 2428 WELLNET CORPORATION 3159 Maruzen CHI Holdings Co.,Ltd. 2445 SRG TAKAMIYA CO.,LTD. 3204 Toabo Corporation 2475 WDB HOLDINGS CO.,LTD. 3361 Toell Co.,Ltd. 2729 JALUX Inc. 3371 SOFTCREATE HOLDINGS CORP. 2767 FIELDS CORPORATION 3396 FELISSIMO CORPORATION 2931 euglena Co.,Ltd. 3580 KOMATSU SEIREN CO.,LTD. 3079 DVx Inc. 3636 Mitsubishi Research Institute,Inc. 3093 Treasure Factory Co.,LTD. 3639 Voltage Incorporation 3194 KIRINDO HOLDINGS CO.,LTD. 3669 Mobile Create Co.,Ltd. 3197 SKYLARK CO.,LTD 3770 ZAPPALLAS,INC. 3232 Mie Kotsu Group Holdings,Inc. 4007 Nippon Kasei Chemical Company Limited 3252 Nippon Commercial Development Co.,Ltd. 4097 KOATSU GAS KOGYO CO.,LTD. 3276 Japan Property Management Center Co.,Ltd. 4098 Titan Kogyo Kabushiki Kaisha 3385 YAKUODO.Co.,Ltd. 4275 Carlit Holdings Co.,Ltd. 3553 KYOWA LEATHER CLOTH CO.,LTD. 4295 Faith, Inc. 3649 FINDEX Inc. 4326 INTAGE HOLDINGS Inc. 3660 istyle Inc. 4344 SOURCENEXT CORPORATION 3681 V-cube,Inc. 4671 FALCO HOLDINGS Co.,Ltd. 3751 Japan Asia Group Limited 4779 SOFTBRAIN Co.,Ltd. 3844 COMTURE CORPORATION 4801 CENTRAL SPORTS Co.,LTD. -

Ief-I Q3 2020

Units Cost Market Value INTERNATIONAL EQUITY FUND-I International Equities 96.98% International Common Stocks AUSTRALIA ABACUS PROPERTY GROUP 1,012 2,330 2,115 ACCENT GROUP LTD 3,078 2,769 3,636 ADBRI LTD 222,373 489,412 455,535 AFTERPAY LTD 18,738 959,482 1,095,892 AGL ENERGY LTD 3,706 49,589 36,243 ALTIUM LTD 8,294 143,981 216,118 ALUMINA LTD 4,292 6,887 4,283 AMP LTD 15,427 26,616 14,529 ANSELL LTD 484 8,876 12,950 APA GROUP 14,634 114,162 108,585 APPEN LTD 11,282 194,407 276,316 AUB GROUP LTD 224 2,028 2,677 AUSNET SERVICES 9,482 10,386 12,844 AUSTRALIA & NEW ZEALAND BANKIN 19,794 340,672 245,226 AUSTRALIAN PHARMACEUTICAL INDU 4,466 3,770 3,377 BANK OF QUEENSLAND LTD 1,943 13,268 8,008 BEACH ENERGY LTD 3,992 4,280 3,824 BEGA CHEESE LTD 740 2,588 2,684 BENDIGO & ADELAIDE BANK LTD 2,573 19,560 11,180 BHP GROUP LTD 16,897 429,820 435,111 BHP GROUP PLC 83,670 1,755,966 1,787,133 BLUESCOPE STEEL LTD 9,170 73,684 83,770 BORAL LTD 6,095 21,195 19,989 BRAMBLES LTD 135,706 987,557 1,022,317 BRICKWORKS LTD 256 2,997 3,571 BWP TRUST 2,510 6,241 7,282 CENTURIA INDUSTRIAL REIT 1,754 3,538 3,919 CENTURIA OFFICE REIT 154,762 199,550 226,593 CHALLENGER LTD 2,442 13,473 6,728 CHAMPION IRON LTD 1,118 2,075 2,350 CHARTER HALL LONG WALE REIT 2,392 8,444 8,621 CHARTER HALL RETAIL REIT 174,503 464,770 421,358 CHARTER HALL SOCIAL INFRASTRUC 1,209 2,007 2,458 CIMIC GROUP LTD 4,894 73,980 65,249 COCA-COLA AMATIL LTD 2,108 12,258 14,383 COCHLEAR LTD 1,177 155,370 167,412 COMMONWEALTH BANK OF AUSTRALIA 12,637 659,871 577,971 CORONADO GLOBAL RESOURCES INC 1,327