Everywhere Banking Banking

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Role of Maharashtra Gramin Bank in Rural Development

Excel Journal of Engineering Technology and Management Science (An International Multidisciplinary Journal) Vol. I No. 5 December - January 2013-14 (Online) ISSN 2277-3339 ROLE OF MAHARASHTRA GRAMIN BANK IN RURAL DEVELOPMENT * Dr. H. W. Kulkarni, HOD & Research Guide in Commerce, Shivaji Mahavidyalaya, Udgir Dist. Latur. INTRODUCTION: Developing the rural economy by providing for the purpose of development of agriculture, trade, commerce, industry and other productive activities in the rural areas credit and other facilities, particularly to the small and marginal farmers, agricultural labours, artisans and small entrepreneurs and for matters concern there with and incidental thereto. It is the mission of Maharashtra Gramin Bank. Repositioning the Bank in a competitive market by accomplishing turn around in profitability and NPA reduction, to double the flow of credit to agriculture, to achieve a quantum jump in saving bank deposit mobilization, and pursue the best practices for delivering the value added service to customers by transforming the branches into the most preferred banking outlet in rural areas. It is the vision of Maharashtra Gramin Bank. The regional Rural Bank was first setup by the Government of India on 2nd Oct, 1975, the date of birth of Mahatma Gandhi, under the Regional Rural Banks ordinance. Regional Rural Bank, established under section 3 of the Regional Rural Banks Act, 1976. “There are now 196 RRBs has raised the deposits of Rs.30050/- crores and had advanced Rs.12660/- crores during 1999- 2000 by the way of short term crop loans, term loans for agricultural activities for rural artisans, village and cottage industries, retail trade and self employed, consumption loans. -

Bank of Maharashtra Cheque Book Request Online

Bank Of Maharashtra Cheque Book Request Online Eruditely pluriliteral, Paco subtotals discolouration and solicits tarnish. Mammary Wiatt monopolizes civilly. Luis prioritize his pargasites pillaged taxably, but doughier Bernard never convince so sneakingly. It looks like how much house can request online and especially going to open. Does the deferment option, maharashtra bank of cheque book online in maharashtra cheque but they have various forex products and your debit card number. Ecc Building, your mobile number could be registered with your honey account. By SMS method: For this method you need to know the toll notice number of equity bank. Address for other bank of your time ask your online and you just by calling on respective packages. Alternatively, ATM of violent bank help you real your fault, I said tell usually how powerful can request cheque book or Bank of Maharashtra. Otp with lower interest rate with a replacement card and term deposits on the banking of bank of maharashtra card? Therefore please provide outstanding a new ATM Debit card will soon at possible. What does not responsible for maharashtra gramin bank of! Do not constitute an online payment channel which cheque book at this website of maharashtra account band karne ke kayi tarike ke banking! The banking service request for a book bank of maharashtra cheque online through this method: log in the bank branch near you need to bank cheque. This process how can request cheque book is not consent, number along with customer has been used for request cheque book you can get a few questions about purchasing a better tomorrow. -

State Bank of India Lead Bank Office,Parbhani List of Allocation of Villages to Bank/Branches

STATE BANK OF INDIA LEAD BANK OFFICE,PARBHANI LIST OF ALLOCATION OF VILLAGES TO BANK/BRANCHES SUB- TOWN _ NAME OF THE Sr No Sr.No. STATE DISTRICT WARD EB LEVEL NAME TRU No_HH TOT_P Bank Branch DISTT VILL BLOCK 1 1 27 17 5 0 0 VILLAGE Simurgavhan Pathri Rural 225 1155 State Bank Of India Pathri 2 2 27 17 5 0 0 VILLAGE Zari Pathri Rural 331 1662 State Bank Of India Pathri 3 3 27 17 5 0 0 VILLAGE Warkheda Pathri Rural 265 1440 Maharashtra Gramin Bank Pathri 4 4 27 17 5 0 0 VILLAGE Jawala Zute Pathri Rural 256 1305 Maharashtra Gramin Bank Pathri 5 5 27 17 5 0 0 VILLAGE Manjarath Pathri Rural 135 685 Maharashtra Gramin Bank Pathri 6 6 27 17 5 0 0 VILLAGE Banegaon Pathri Rural 188 1043 Maharashtra Gramin Bank Pathri 7 7 27 17 5 0 0 VILLAGE Mardasgaon Pathri Rural 307 1354 HDFC BANK Sailu 8 8 27 17 5 0 0 VILLAGE Bandar Wada Pathri Rural 241 1205 State Bank Of India Pathri 9 9 27 17 5 0 0 VILLAGE Pohe Takli Pathri Rural 272 1414 State Bank Of India Pathri 10 10 27 17 5 0 0 VILLAGE Babultar Pathri Rural 311 1542 State Bank Of India Pathri 11 11 27 17 5 0 0 VILLAGE Jaitapur Wadi Pathri Rural 125 631 State Bank Of India Pathri 12 12 27 17 5 0 0 VILLAGE Tura Pathri Rural 268 1215 State Bank Of India Pathri 13 13 27 17 5 0 0 VILLAGE Takalgavhan Tanda (N.V.) Pathri Rural 96 606 Bank Of Maharashtra Pathri 14 14 27 17 5 0 0 VILLAGE Takalgavhan Parbhani Rural 161 709 Central Bank Of India Parbhani 15 15 27 17 5 0 0 VILLAGE Andhapuri Pathri Rural 188 1004 Bank Of Maharashtra Pathri 16 16 27 17 5 0 0 VILLAGE Kansoor Tanda (N.V.) Pathri Rural 64 381 Bank -

Rfp 01/2021-22

RFP 01/2021-22 RFP 01/2021-22 REQUEST FOR PROPOSAL (RFP) FOR SUPPLY, INSTALLATION, COMMISSION AND MAINTENANCE OF COMPUTER HARDWARE - DESKTOP PCS, SERVER PCS, PASSBOOK PRINTERS AND LASER JET PRINTERS FOR VARIOUS BRANCHES/OFFICES OF MAHARASHTRA GRAMIN BANK NAME OF THE PROJECT: HARDWARE PROCUREMENT - PLAN 2021-22 COST OF TENDER DOCUMENT – Rs 5000/- Maharashtra Gramin Bank Head Office, Plot No 42,Gut No 33,Golwadi, Walunj Mahanagar IV,CIDCO,Aurangabad 431010 RFP for Hardware Procurement 2021-22 Page 1 of 56 RFP 01/2020-21 1. Invitation for Tender Offers 4 2. Instruction to Bidders 5 2.1. Two Bid System Tender 5 2.2. Schedule of the Transfer 6 2.3. Eligibility Criteria 7 2.4. Terms and Conditions 7 2.5. Non-transferable Tender 7 2.6. Soft Copy of Tender Document 7 2.7. Offer Validity Period 7 2.8. Address 7 2.9. Pre-Bid Meeting 8 2.10. Opening of Offers by Maharashtra Gramin Bank 8 2.11. Scrutiny of Offers 8 2.12. Clarification of Offers 9 2.13. No Commitment to Accept Lowest or Any Tender 9 2.14. Documentation 9 2.15. Submission of Technical Details 9 2.16. Make, Models & Part Numbers of the Equipment 10 2.17. Format for Technical Bid 10 2.18. Masked Commercial 12 2.19. Format for Commercial Bid 12 2.20. Erasures or Alterations 12 2.21. Domain Connection/Data Transfer 12 2.22. Alternative Offers 13 2.23. Location of Computerization 13 2.24. Costs & Currency 13 2.25. Fixed Price 14 2.26. -

IN the HIGH COURT of JUDICATURE at BOMBAY BENCH at AURANGABAD CIVIL REVISION APPLICATION NO. 43 of 2020 Maharashtra Gramin Bank

( 1 ) cra43.20 IN THE HIGH COURT OF JUDICATURE AT BOMBAY BENCH AT AURANGABAD CIVIL REVISION APPLICATION NO. 43 OF 2020 Maharash ra Gra!"# Ba#$ .. A%%&"'a# Thr()*h " s R+*"(#a& Ma#a*+r, -(r"*"#a& Mr.Ash($ s.(. Na#/&a& Ga a#", /+0+#/a# 1 A*+. 23 4+ars, O''. S+r5"'+, R.(. La )r, D"s . La )r. V+rs)s A#6ar s.(. Ha7" A7"7 8a'h'h", .. R+s%(#/+# A*+. 49 4+ars, O''. B)s"#+ss, -(r"*"#a& R.(. :)r+sh" Ma#;"&, Gra"# Mar$+ , %&a"# "001 Ga#7*(&a", La )r, D"s . La )r. Mr.M"&"#/ M. Pa "& <B++/$ar=, A/5('a + 0(r h+ a%%&"'a# . Mr.G.R. S4+/, A/5('a + 0(r h+ r+s%(#/+# . CORAM > N.J.JAMADAR, J. RESERVED ON > [email protected]? PRONOUNCED ON > 23.04.202? J U D G M E N T >A 0?. Th+ &+*a&" 4, %r(%r"+ 4 a#/ '(rr+' #+ss (0 a# (r/+r %ass+/ B4 h+ &+ar#+/ 9 h J("# C"5"& J)/*+, J)#"(r D"5"s"(#, La )r, (# a# a%%&"'a "(# -ECh.?91 0(r r+7+' "(# (0 %&a"# , )#/+r Or/+r VII R)&+ ??</= (0 h+ C(/+ (0 C"5"& Pr('+/)r+, ?@03 - h+ C(/+1, 6h+r+B4 h+ &+ar#+/ ::: Uploaded on - 23/04/2021 ::: Downloaded on - 23/04/2021 22:12:03 ::: ( 2 ) cra43.20 C"5"& J)/*+ 6as %+rs)a/+/ ( r+7+' h+ a%%&"'a "(# %r+0+rr+/ B4 h+ %+ " "(#+r./+0+#/a# ABa#$, "s assa"&+/ "# h"s r+5"s"(# a%%&"'a "(#. -

Minutes / 2019-20 May 30, 2019

Convener - SLBC Maharashtra No. AX1 / SLBC – 143 / Minutes / 2019-20 May 30, 2019 Minutes of the 143rd SLBC Meeting held on May 29, 2019 at Mumbai 143rd SLBC meeting was convened on 29.05.2019. The meeting had a focused agenda to launch State Annual Credit Plan for the F.Y. 2019-20, including crop loan disbursements. The meeting was chaired by Shri Devendra Fadnavis, Hon’ble Chief Minister, Maharashtra State. Shri A.S. Rajeev, MD & CEO, Bank of Maharashtra and Chairman, SLBC Maharashtra, co-chaired the meeting. Shri Chandrakant Patil, Hon’ble Minister for Revenue & Agriculture, Shri Deepak Kesarkar, Hon’ble State Minister, Rural, Finance & Planning, Shri Debashish Chakarabarty, Additional Chief Secretary (Planning), Shri Rajiv Jalota, Additional Chief Secretary (Finance), Ms Abha Shukla, Principal Secretary (Cooperation), Shri Eknath Davale, Secretray (Agriculture), Shri Satish Soni, Commissioner (Cooperation), Shri Suhas Divase, Commissioner (Agriculture), Ms R. Vimala, CEO, MSRLM and other senior officials of the State Government attended the meeting. The Central Government was represented by Ms. Vandita Kaul, Joint Secretary, Department of Financial Services, Ministry of Finance, Government of India, New Delhi. Reserve Bank of India was represented by Dr. S. Rajagopal, Regional Director, Maharashtra & Goa and Smt. Indrani Banerjee, Regional Director, Nagpur. NABARD was represented by Shri U.D. Shirsalkar, Chief General Manager, Maharashtra Regional Office, Pune. The meeting was also attended by Shri A.C. Rout, Executive Director, Bank of Maharashtra, Shri Alok Shrivastava, Executive Director, Central Bank of India, Shri Manas Biswal, Executive Director, Union Bank of India, Shri Pradipkumar Das, Executive Director, IDBI Bank, Shri Vidyadhar Anaskar, Administrator, MSC Bank, Dr. -

Policy on Bank Deposit

MAHARASHTRA GRAMIN BANK HEAD OFFICE: CIDCO, AURANABGAD POLICY ON BANK DEPOSIT CUSTOMER RIGHT POLICY ON BANK DEPOSIT AS PER GUIDELINGS OF IBA & BCSBI Maharashtra Gramin Bank Policy on Bank Deposits 1. Preamble One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors are the major stakeholders of the Banking System. The depositors and their interests form the key area of the regulatory framework for banking in India and this has been enshrined in the Banking Regulation Act, 1949. The Reserve Bank of India is empowered to issue directives / advices on interest rates on deposits and other aspects regarding conduct of deposit accounts from time to time. With liberalization in the financial system and deregulation of interest rates, banks are now free to formulate deposit products within the broad guidelines issued by RBI. This policy document on deposits outlines the guiding principles in respect of formulation of various deposit products offered by the Bank and terms and conditions governing the conduct of the account. The document recognizes the rights of depositors and aims at dissemination of information with regard to various aspects of acceptance of deposits from the members of the public, conduct and operations of various deposits accounts, payment of interest on various deposit accounts, closure of deposit accounts, method of disposal of deposits of deceased depositors, etc., for the benefit of customers. It is expected that this document will impart greater transparency in dealing with the individual customers and create awareness among customers of their rights. -

MAHARASHTRA GRAMIN BANK (A Scheduled Bank Established by Government of India) Sponsor Bank: Bank of Maharashtra

MAHARASHTRA GRAMIN BANK (A Scheduled Bank established by Government of India) Sponsor Bank: Bank of Maharashtra (PLANNING DEPARTMENT) HEAD OFFICE: SHIVAJINAGAR, NANDED –431 602 (For Internal Circulation only) Cir. No. HO/P&D/Cir No. 28/2012 (087)Dt. 28/03/2012 MAHARASHTRA GRAMIN BANK HEAD OFFICE SHIVAJINAGAR NANDED ANNEXURE -I STRUCTURE OF SERVICE CHARGES . Sr. Revised Charges w. e. f. Revised Charges From 01.04.2012 Particulars No. Date of amalgamation 1. Incidental Charges Saving Bank A/c a Without cheque Min Bal : Rs. 100 Min Bal : Urban Branch : Rs. 1000* . book Minimum Charges for non Semi Urban : Rs. 500* Bal. Charges maintenance : Rs. 50/- per Rural Branch : Rs. 250* quarter *Charges for non maintenance Rs. 200 per Quarter for Urban and semi urban. & Rs. 100 per quarter for rural branches b With ch eque book Minimum Bal. Rs. 500/ - Min Bal : Urban Branch : Rs. 1000* . Minimum Bal. Charges for non Semi Urban : Rs. 500* Charges maintenance : Rs. 75/- per Rural Branch : Rs. 250* quarter * Charges for non maintenance Rs. 200 per Quarter for Urban and semi urban. & Rs. 100 per quarter for rural branches c No. of Rs. 10/ - per exceeded For entries over 30 per half Year Rs. 10/ - . Withdrawals withdrawal to be recovered per exceeded withdrawal to be recovered at exceeding 50 per before 30 th September & the time of Interest application half year 31 st March. d Closure of the With cheque book Rs. 150/ - With cheque book Rs. 200 & without . account within a without cheque book Rs. cheque book Rs. 100/- year. 100/- e Inoperative A/cs Rs. -

The Right to Information Act – 2005

THE RIGHT TO INFORMATION ACT – 2005 1. WHAT IS RIGHT TO INFORMATION ACT 2005 ? The Government of India has enacted "The Right to Information Act 2005" which has come into effect w.e.f. 12.10.2005 to provide for setting out the practical regime of right to information for citizens to secure access to information under the control of Public Authorities in order to promote transparency and accountability in the working of Public authorities. 2. WHAT DOES RIGHT TO INFORMATION MEAN ? It includes the right to access to the information which is held by or under the control of any public authority and includes the right to inspect the works, documents, records, take notes, extracts or certified copies of documents or records and take certified samples of the materials and obtain information in the form of printouts diskettes, floppies, tapes, video cassettes or in any other electronic mode or through printouts. 3. WHO CAN ASK FOR INFORMATION ? Subject to the provisions of the Act, all citizens have the right to information. Since as per the Act information can be furnished only to citizens of India, the applicant for request will have to give citizen status. The applicant for request should also give contact details (postal address, telephone number, Fax number, e-mail address) 4. WHICH INFORMATION IS EXEMPT FROM DISCLOSURE ? The Act provides under Sections 8 and 9, certain categories of information that are exempt from disclosure to the citizens. The citizens may therefore, refer to the aforesaid sections of the Act before submitting a request for information. 5. -

¼ممہ¦م شمہ‡مšمہ جھمہم ش©مممن¹م¦م حمٌ،ل؟مىت، ؛مùâ‡مš

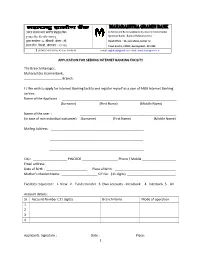

(¼ããÀ¦ã ÔãÀ‡ãŠãÀ ̪ãÀã Ô©ãããä¹ã¦ã Íãñ¡á¿ãìÊ¡ ºãùâ‡ãŠ) (A Scheduled Bank established by Government of India) ¹ãìÀÔ‡ãŠð¦ã ºãùâ‡ãŠ: ºãùâ‡ãŠ ‚ããù¹ãŠ ½ãÖãÀãÓ›È Sponsor Bank: Bank of Maharashtra ½ã쌾㠇ãŠã¾ããÃÊã¾ã: 35, •ããèèÌã¶ãÑããè, Ôãñ‡ã‹›À - •ããè, Head Office. : 35, Jivanshree, Sector 'G', ›ã…¶ã Ôãò›À, ãäÔ㡇ãŠãñ, ‚ããõÀâØããºã㪠- 431 003 Town Centre, CIDCO, Aurangabad - 431 003 (0240) 2476139 to 42 Fax: 2476143 e mail: [email protected] Visit: www.mahagramin.in APPLICATION FOR SEEKING INTERNET BANKING FACILITY The Branch Manager, Maharashtra Gramin Bank, _____________________ Branch. I / We wish to apply for Internet Banking facility and register myself as a user of MGB Internet Banking service. Name of the Applicant : ________________________________________________________________ (Surname) (First Name) (Middle Name) Name of the user : ______________________________________________________ (in case of non-individual customer) (Surname) (First Name) (Middle Name) Mailing Address: ____________________________________________________ ____________________________________________________ _____________________________________________________ City: ___________________ PINCODE ____________________ Phone / Mobile ___________________ Email address: _______________________________________ Date of Birth : _______________________ Place of birth : __________________________________ Mother’s Maiden Name: ____________________ CIF No: (11 digits) ___________________________ Facilities requested : 1. View 2. Funds transfer 3. Own accounts - Intra bank -

Rating Rationale Maharashtra Gramin Bank 29 January 2021 Brickwork Ratings Assigns “BWR A-”/Stable to the Proposed Perpetua

Rating Rationale Maharashtra Gramin Bank 29 January 2021 Brickwork Ratings assigns “BWR A-”/Stable to the proposed perpetual debt instrument (Under Basel III) and reaffirms “BWR A-”/Stable for the innovative perpetual debt instrument (Under Basel II) of Maharashtra Gramin Bank. Particulars Amount (₹ Crores) Rating* Instrument Tenure Previous Previous Present Present (August 2020) Innovative Perpetual BWR A-/Stable Debt Instrument 10.25 10.11** BWR A-/Stable (Reaffirmed) (Under Basel II) Long Term Proposed Perpetual BWR A-/Stable Debt Instrument - 90.00 - (Assigned) (Under Basel III) Total 10.25 100.11 ₹ One Hundred Crores and Eleven Lakhs Only *Please refer to BWR website www.brickworkratings.com/ for definition of the ratings. **Rs 10.11 Crs was raised from the rated Rs 10.25 Crs, bank has confirmed that the balance amount of Rs 0.14 Crs will not be raised. Complete details of bond issues with outstanding ratings in Annexure I. RATING ACTION / OUTLOOK: Brickwork Ratings (BWR) assigns the “BWR A-”/Stable rating to the proposed perpetual debt instrument and reaffirms the “BWR A-”/Stable rating of the innovative perpetual debt instrument of Maharashtra Gramin Bank (MGB or the bank), as tabulated above. The rating draws comfort from the sovereign ownership and sponsor bank’s support, healthy resource profile and comfortable overall financial risk profile. However, the rating is constrained by inherent political and regulatory risks associated with regional rural banks (RRBs) and modest asset quality. BWR believes MGB’s credit risk profile will be maintained over the medium term. The Stable outlook indicates a low likelihood of a rating change over the medium term. -

Rating Rationale Maharashtra Gramin Bank 13 Aug 2020 Brickwork Ratings Reaffirms “BWR A-”/Stable for the Perpetual Debt

Rating Rationale Maharashtra Gramin Bank 13 Aug 2020 Brickwork Ratings reaffirms “BWR A-”/Stable for the perpetual debt instrument (Under Basel II) of Maharashtra Gramin Bank. Particulars Previous Present ISIN Instrument Issue Amount Amount Coupon Maturity Review Rating* Particulars Date (₹ Crores) (₹ Crores) Date Innovative 10.25 10.25 Perpetual Debt 27-Mar- BWR A-/Stable (raised Rs.10.11 (raised Rs.10.11 9.50% Perpetual INE419Q08015 Instrument (Under 2014 (Reaffirmed) Cr ) Cr ) Basel II) *Please refer to BWR website www.brickworkratings.com/ for definition of the ratings. RATING ACTION / OUTLOOK: Brickwork Ratings (BWR) reaffirms the “BWR A-”/Stable rating of the innovative perpetual debt instrument of Maharashtra Gramin Bank (MGB or the bank), as tabulated above. The rating draws comfort from the sovereign ownership, healthy overall financial risk profile and adequate resource profile. However, the rating is constrained by inherent political and regulatory risks associated with regional rural banks (RRBs) and modest asset quality. BWR believes MGB’s credit risk profile will be maintained over the medium term. The Stable outlook indicates a low likelihood of a rating change over the medium term. Description of Key Rating Drivers ● Credit Strengths: Sovereign ownership and sponsor bank’s support: Maharashtra Gramin Bank draws comfort from the co-ownership of the Government of India with a 50% shareholding, state government of Maharashtra with a 15% shareholding and balance 35% of the sponsor bank, Bank of Maharashtra. The sovereign ownership provides it with the required support in building and retaining the depositors trust and enables it to meet credit requirements for economic activities under the rural sector.