PREFACE This Report Has Been Prepared for Submission to Governor Under Article 151(2) of the Constitution. Eleventh Finance Comm

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Bond Forever…

READYMIX CONCRETE A BOND FOREVER… www.bestreadymix.com READYMIX CONCRETE Towards emerging future… Best Readymix, a division of the leading business house - the Best Group, Thrissur, Kerala is engaged in supplying high quality readymix cement solutions to the diverse needs of the building industry. We produce and supply ready mixed concrete to customers through a network of fixed commercial outlets and project specific onsite batching facilities. Promoted by leading suppliers of raw materials and equipments to the building and construction industry, our extensive experience in Cement C & F, Quarrying, Earth Moving etc. ensures better quality of raw materials to cater to projects ranging in size from the smallest home application to the largest construction projects. Professionalism Committed to to the core… quality construction… Our professional team has the resources and Rigorous quality control is carried out technical expertise to provide a wide range of throughout the manufacturing process and ready mix mixes and match right mix design to the right concrete meets a great variety of needs in terms of application and can be supplied to several technical sophistication, ease of use, assembly positions in one delivery. Readymix concrete is and design. Devotion to quality is apparent in the cost effective and its speed of discharge onsite is consistency and predictability of Best Readymix very useful to meet tight construction deadlines. products. Best Ready mix meets exacting standards Our own quarry ensures quality gravel and our through a series of internal and external checks. fully equipped laboratory delivers quality ready Practices and facilities are carefully tested and mix concrete. Computerized control of the plant monitored by professioal independent also allows different concrete recipes as per your laboratories. -

2015-16 Term Loan

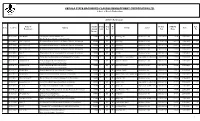

KERALA STATE BACKWARD CLASSES DEVELOPMENT CORPORATION LTD. A Govt. of Kerala Undertaking KSBCDC 2015-16 Term Loan Name of Family Comm Gen R/ Project NMDFC Inst . Sl No. LoanNo Address Activity Sector Date Beneficiary Annual unity der U Cost Share No Income 010113918 Anil Kumar Chathiyodu Thadatharikathu Jose 24000 C M R Tailoring Unit Business Sector $84,210.53 71579 22/05/2015 2 Bhavan,Kattacode,Kattacode,Trivandrum 010114620 Sinu Stephen S Kuruviodu Roadarikathu Veedu,Punalal,Punalal,Trivandrum 48000 C M R Marketing Business Sector $52,631.58 44737 18/06/2015 6 010114620 Sinu Stephen S Kuruviodu Roadarikathu Veedu,Punalal,Punalal,Trivandrum 48000 C M R Marketing Business Sector $157,894.74 134211 22/08/2015 7 010114620 Sinu Stephen S Kuruviodu Roadarikathu Veedu,Punalal,Punalal,Trivandrum 48000 C M R Marketing Business Sector $109,473.68 93053 22/08/2015 8 010114661 Biju P Thottumkara Veedu,Valamoozhi,Panayamuttom,Trivandrum 36000 C M R Welding Business Sector $105,263.16 89474 13/05/2015 2 010114682 Reji L Nithin Bhavan,Karimkunnam,Paruthupally,Trivandrum 24000 C F R Bee Culture (Api Culture) Agriculture & Allied Sector $52,631.58 44737 07/05/2015 2 010114735 Bijukumar D Sankaramugath Mekkumkara Puthen 36000 C M R Wooden Furniture Business Sector $105,263.16 89474 22/05/2015 2 Veedu,Valiyara,Vellanad,Trivandrum 010114735 Bijukumar D Sankaramugath Mekkumkara Puthen 36000 C M R Wooden Furniture Business Sector $105,263.16 89474 25/08/2015 3 Veedu,Valiyara,Vellanad,Trivandrum 010114747 Pushpa Bhai Ranjith Bhavan,Irinchal,Aryanad,Trivandrum -

Green Audit Report 2018-19

Green Audit Report 2018-19 Nature's Green Guardians Foundation St. Mary's College, Thrissur - Green Audit Report 2018-19 St. MARY's COLLEGE THRISSUR Green Audit Report 2018-19 Nature's Green Guardians Foundation 1 St. Mary's College, Thrissur - Green Audit Report 2018-19 Preface The students who are at present in schools and colleges are to be the enlightened leaders of immediate tomorrow. India's educational authorities, as in most developed countries, therefore insist that every student in our country should learn why damages to the environment occur and also how such situations could be averted, emphasizing more on possible remedies. This green education, no doubt, should start from schools and colleges, and the insistence on annual Green Audit of higher education institutions is to make students and staff well informed of the magnitude of one's own ecological footprints, as well as on which areas one should concentrate to make his or her environs greener than before. The 2018-19 Green Audit Report of St. Mary's College, Thrissur, is prepared in such a manner that it can educate every stakeholder of the institution, on the major contributors tending to destroy, and on every step helpful to restore, leading to further flourishing of its green status. A brief presentation of the contents of this report at the beginning of the next academic year by the teachers to the other stakeholders would help in getting every one of them to start taking further steps to achieve a 'brighter shade of green' for their beloved campus and the region. -

Agenda & Notes for the Meeting of the R T a , Thrissur to Be Held on 02-02

1 Agenda & Notes for the Meeting of the R T A , Thrissur to be held on 02-02-2018 at 10.30 A.M (Venue : Conference Hall, District Collectorate, Thrissur) PRESENT : CHAIRMAN :SHRI.DR.A.KOWSIGAN I A S DISTRICT COLLECTOR & CHAIRMAN, R T A, THRISSUR. MEMBER : SHRI YATHISH CHANDRA I. P. S, DISTRICT POLICE CHIEF, THRISSUR RURAL, ( MEMBER, R T A, THRISSUR) MEMBER : SHRI. SHAJI JOSEPH DEPUTY TRANSPORT COMMISSIONER, CENTRAL ZONE-1, THRISSUR. ( MEMBER, R T A, THRISSUR) 2 Item No.1 G-128759/2017 Agenda :. To Consider the application for the grant of fresh regular permit in respect of suitable stage carriage ( 28 seats in all ) to operate on the route Karappadam-Chalakkudy-Thiruthyparambu-Chembankunnu,via Kundukuzhipadam- Koorkamattom-MarancodeStMary’sChurch, Kuttikkadu-Poovathinkal-Paroyaram- Anamala junction-Sadayam College-Vellanchira-Annur-Kottat-Kuttikkadu church- Mechira-Chowka-VGM-Thazhur church-Nayarangadi- as Ordinary service Applicant:Sri. Shaju,Pariyadan House,P O Pattikkad,Thrissur Proposal Timings Karappad Chalakk Thiruthipara Chalakk Karappad Chebanku am udy mbu udy am nnu 6.20 6.58 7.00 7.20 7.40 7.53 8.31 8.32 10.45 10.00/10. 9.40 9.20 07 10.47 11.25 11.30 11.50 12.10 12.48 1.26 2.35 1.57 3.18 4.03 4.53 4.10 5.03 5.46 6.48 6.05 7.46Halt 7.08 Total route length- 54.8KM. Overlapping on the notified route – Nil 3 1) Trip.at,6.20ViaKundukuzhi,Koorkamattom,Kuttikkad,Pariyaram,Anamal a road 2) Trip at,7.00 Via Sadayan College,Vellanchira 3) Trip.at,7.53ViaAnamalaRoad,Pariyaram,Poovathinkal,Kuttikkad, Karunalayam, Kuttichira 4) Trip.at,9.10ViaKundukuzhi,Koorkamattom,Kuttikkad,Pariyaram,Anamal -

CSBL Unpaid Dividend, Refund Consolidated As on 22.09.2015.Xlsx

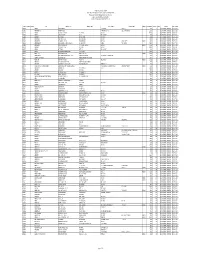

The Catholic Syrian Bank Limited Regd. Office, "CSB Bhavan", St. Mary's College Road, Thrissur 680020 Phone: 0487 -2333020, 6451640, eMail: [email protected] List of Unpaid Dividend as on 22.09.2015 (Dividend for the periods 2007-08 to 2013-14) FOLIO / DEMAT ID INITLS NAME ADDRESS LINE 1 ADDRESS LINE 2 ADDRESS LINE 3 ADDRESS LINE 4 PINCOD DIV.AMOUNT DWNO MICR PERIOD IEPF. TR. DATE A00350 ANTONY PALLANS HOUSE KURIACHARA TRICHUR, 30.00 0 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00385 ANNAMMA P X AKKARA HOUSE PANAMKUTTICHIRA OLLUR, TRICHUR DIST 150.00 5 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00398 ANTONY KUTTENCHERY HOUSE HIGH ROAD TRICHUR 1020.00 0 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00406 ANTONY KALLIATH HOUSE OLLUR TRICHUR DIST 27.00 9 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00409 ANTHONY PLOT NO 143 NEHRU NAGAR TRICHUR-6 120.00 0 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00643 ANTHAPPAN PADIKKALA HOUSE EAST FORT GATE TRICHUR 540.00 12 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00647 ANTHONY O K OLAKKENGAL HOUSE LOURDEPURAM TRICHUR - KERALA STATE. 680005 180.00 13 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00668 ANTHONISWAMI C/O INASIMUTHU MUDALIAR SONS 55 NEW STREET KARUR TAMILNADU 2100.00 14 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00822 ANNA JACOB C/O J S MANAVALAN 5 V R NAGAR ADAYAR MADRAS - 600020 210.00 18 2007-08 UNPAID DIVIDEND 25-OCT-2015 A01072 ANTHONY VI/62 PALACE VIEW EAST FORT TRICHUR 4200.00 0 2007-08 UNPAID DIVIDEND 25-OCT-2015 A01077 ANTONY KOTTEKAD KUTTUR TRICHUR DIST 30.00 0 2007-08 UNPAID DIVIDEND 25-OCT-2015 A01103 ANTONY ELUVATHINGAL CHERUVATHERI -

LB Block Name District

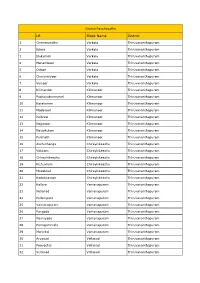

Grama Panchayaths LB Block Name District 1 Chemmaruthy Varkala Thiruvananthapuram 2 Edava Varkala Thiruvananthapuram 3 Elakamon Varkala Thiruvananthapuram 4 Manamboor Varkala Thiruvananthapuram 5 Ottoor Varkala Thiruvananthapuram 6 Cherunniyoor Varkala Thiruvananthapuram 7 Vettoor Varkala Thiruvananthapuram 8 Kilimanoor Kilimanoor Thiruvananthapuram 9 Pazhayakunnumel Kilimanoor Thiruvananthapuram 10 Karavaram Kilimanoor Thiruvananthapuram 11 Madavoor Kilimanoor Thiruvananthapuram 12 Pallickal Kilimanoor Thiruvananthapuram 13 Nagaroor Kilimanoor Thiruvananthapuram 14 Navaikulam Kilimanoor Thiruvananthapuram 15 Pulimath Kilimanoor Thiruvananthapuram 16 Anchuthengu Chirayinkeezhu Thiruvananthapuram 17 Vakkom Chirayinkeezhu Thiruvananthapuram 18 Chirayinkeezhu Chirayinkeezhu Thiruvananthapuram 19 Kizhuvilam Chirayinkeezhu Thiruvananthapuram 20 Mudakkal Chirayinkeezhu Thiruvananthapuram 21 Kadakkavoor Chirayinkeezhu Thiruvananthapuram 22 Kallara Vamanapuram Thiruvananthapuram 23 Nellanad Vamanapuram Thiruvananthapuram 24 Pullampara Vamanapuram Thiruvananthapuram 25 Vamanapuram Vamanapuram Thiruvananthapuram 26 Pangode Vamanapuram Thiruvananthapuram 27 Nanniyode Vamanapuram Thiruvananthapuram 28 Peringammala Vamanapuram Thiruvananthapuram 29 Manickal Vamanapuram Thiruvananthapuram 30 Aryanad Vellanad Thiruvananthapuram 31 Poovachal Vellanad Thiruvananthapuram 32 Vellanad Vellanad Thiruvananthapuram 33 Vithura Vellanad Thiruvananthapuram 34 Uzhamalakkal Vellanad Thiruvananthapuram 35 Kuttichal Vellanad Thiruvananthapuram 36 Tholicode Vellanad -

(KSDMA) Observatory Hills, Vikas Bhavan PO, Thiruvananthapuram

Kerala State Disaster Management Authority (KSDMA) Observatory Hills, Vikas Bhavan P.O, Thiruvananthapuram, Kerala - 695033 Day time phone - 0471 2331345, 0471-2331645, Night time phone - 0471 2364424 Toll Free 1079, Fax - 0471 2364424. www.sdma.kerala.gov.in List of Local Self Governments needing special attention and Containment Zones - 02-09- 2020 GO (Ms) No. 18/2020/DMD dated 17-06-2020 LSGs needing Sl. No District Containment Zones special attention 1 Kannur Aalakkod 10, 12 2 Kannur Anthoor 5,20,21,24,28 3 Kannur Aralam 2, 3, 11, 15 4 Kannur Ayyankunnu 2, 4, 6, 8, 10, 11 5 Kannur Azeekkode 1, 3, 4, 7, 8, 9, 12, 13, 14, 15 6 Kannur Chembilode 3, 5, 10, 14, 19 7 Kannur Chengalayi 2, 4, 6, 18 8 Kannur Cherukunnu 1,2,3,5,7,8,9 9 Kannur Cheruthazham 2,5,7,10,13,15 1,2,4,5,7,8,10,11,12,13,14,15,16,20,22 10 Kannur Chirakkal (entire ward) 11 Kannur Chittaripparamba 5, 6, 7, 8 (Entire Ward) 12 Kannur Chokli 5, 9, 10 13 Kannur Contonment Board DSC Center 14 Kannur Darmadam 1,3,4,12,13,14,16,17,18 15 Kannur Eramam Kuttur 4, 5 16 Kannur Eranjoli 1, 3, 8, 9 17 Kannur Eruvessi 1 18 Kannur Ezhom 2, 3, 4, 5, 6, 12 19 Kannur Irikkoor 4 20 Kannur Iritty (M) 2,3,7,8,13,18,19,32 Kadannappally 21 Kannur 1 Panappuzha 22 Kannur Kallyasseri 3, 15, 16 23 Kannur Kanichar 12, 13 Kankol 24 Kannur 8, 9, 10, 11, 12 Alapadamba 25 Kannur Kannapuram 12 1,2,4,5,8,10,11,12,13,15,18, 20,21,22,23,25,26,27,29,30,31,32,33,37 26 Kannur Kannur (C) ,38, 39,40,41,42,43,45,48,49,50,51,52,54,55 27 Kannur Karivellur-Peralam 1, 4, 6 28 Kannur Kathiroor 2,5,8,12,14, 18 29 Kannur -

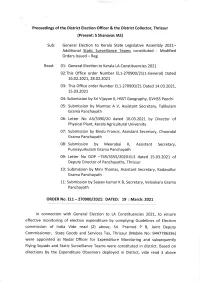

Submission by Meerabai K, Assistant Secretary, Commission of Lndia Vide

Proceedings of the District Election Officer & the District Collector, Thrissur (Present: S Shanavas IAS) Sub General Election to Kerala State Legislative Assembly 2O2L- Additional Static Surveillance Teams constituted - Modified Orders lssued - Reg Read: 01: General Election to Kerala LA Constituencies 2021, 02:This Office order Number ELL-27090O/21,(1,-General) Dated 76.02.2021,, 28.02.2021, 03: This Office order Number EL1,-27O9O0/21, Dated L4.O3.2021, L5.03.202L 04: Submission by Sri Vijayan K, HSST Geography, GVHSS Peechi 05: Submission by Mumtaz AY, Assistant Secretary, Talikulam Grama Panchayath 06: Letter No A3/3390/20 dated t6.O3.2O21 by Director of Physical Plant, Kerala Agricultural University 07: Submission by Bindu Francis, Assistant Secretary, Choondal Grama Panchayath 08: Submission by Meerabai K, Assistant Secretary, Punnayurkulam Grama Panchayath 09: Letter No DDP -TSR/3555 /202O-EL3 dated 15.03.2021 of Deputy Director of Panchayaths, Thrissur 10: Submission by Mini Thomas, Assistant Secretary, Kadavallur Grama Panchayath 1L: Submission by Sajeev kumar K B, Secretary, Velookara Grama Panchayath ORDER No. EL1 -27O9OOl2O2t: DATED: 19 : March:2O21 ln connection with General Election to LA Constituencies 202L, to ensure effective monitoring of election expenditure by complying Guidelines of Election commission of lndia Vide read (2) above, Sri. Pramod P B, Joint Deputy Commissioner, State Goods and Services Tax, Thrissur (Mobile No 9447786336) were appointed as Nodal Officer for Expenditure Monitoring and subsequently Flying Squads and Static Surveillance Teams were constituted in district. Based on directions by the Expenditure Observers deployed in District, vide read 3 above additional 6 Flying Squads and Static Surveillance Teams were duly constituted ih District. -

Accused Persons Arrested in Thrissur City District from 15.11.2015 to 21.11.2015

Accused Persons arrested in Thrissur City district from 15.11.2015 to 21.11.2015 Name of the Name of Name of the Place at Date & Court at Sl. Name of the Age & Cr. No & Sec Police Arresting father of Address of Accused which Time of which No. Accused Sex of Law Station Officer, Rank Accused Arrested Arrest accused & Designation produced 1 2 3 4 5 6 7 8 9 10 11 KUTTIKATTIL 3365/15 U/S TOWN HOUSE, THILAKAN. SUDHAKA 58 JAIHIND 15.11.2015 15(C) R/W 63 EAST PS BAILED BY 1 GOPALAN PUTHUKAD, A.S, SI OF RAN MALE BUILDING at 10.30 ABKARAI (THRISSUR POLICE NEAR OLD POLICE ACT CITY) POLICE STATION KORANGANMARI L HOUSE, P.O. KALADIPATTA, 3366/15 U/S TOWN THILAKAN. MANIKAN 38 MANJILATHIL 15.11.2015 15(C) R/W 63 EAST PS BAILED BY 2 CHANGAN M.O. ROAD A.S, SI OF DAN MALE DESAM, at 11.10 ABKARAI (THRISSUR POLICE POLICE ONGALLUR, ACT CITY) PATTAMBI, PALAKAD MAMBARAMBAT H HOUSE, TOWN SKT STAND 3367/15 U/S THILAKAN. 47 CHENDRAPPINNI 15.11.2015 EAST PS BAILED BY 3 VISWAN KUNJANDI SOUTH 279 IPC AND A.S, SI OF MALE DESAM, at 11.50 (THRISSUR POLICE RING 185 MV ACT POLICE KANNAMPULLIP CITY) ARAM THOMBIKATTIL TOWN HOUSE, THILAKAN. 19 PENSIONMO 15.11.2015 3368/15 U/S EAST PS BAILED BY 4 ELDHOSE THOMAS KUNDUKAD, A.S, SI OF MALE OLA at 13.05 279 IPC (THRISSUR POLICE THEKKUMKARA POLICE CITY) VILLAGE KOTTIYATH 3369/15 U/S TOWN HOUSE, V.K. -

THINKERS WORKSHOP DECENTRALISATION and DEVELOPMENT 20-21 January 2016

KILA’s International Conference Series THINKERS WORKSHOP DECENTRALISATION AND DEVELOPMENT 20-21 January 2016 Field Visit Guide Kerala Institute of Local Administration (KILA) Mulamkunnathukavu, Thrissur - Kerala - 680 581 Phone: 0487-2201768, 2200244, Director:2201312; Fax:0487-2201062 e-mail: [email protected]; website: www.kilaonline.org Field Visit Guide 1 20-2 KILA’s International Conference Series January 2016 THINKERS WORKSHOP - Decentralisation and Development KILA’s International Conference Series THINKERS WORKSHOP DECENTRALISATION AND DEVELOPMENT Field visit Guide Chief Editor Dr. P.P. Balan Editor Dr. Sunny George Associate Professor & Conference Coordinator Prepared by Prof. T. Raghavan Shri. P. V. Ramakrishnan Shri. Joshy P. B. Smt. Moly Thomas Compiled and Edited by Shri. K . Gopalalakrishnan Extension Faculty Member, KILA Printed and Published by Dr. P.P. Balan Director Kerala Institute of Local Administraion January 2016 Cover, DTP& Layout Designing : Rajesh Thanikudam Printed at : Co- operative Press, Mulamkunnathukavu. Phone: 0487 2200391, 9895566621 2 Field Visit Guide KILA’s International Conference Series THINKERS WORKSHOP DECENTRALISATION AND DEVELOPMENT 20-21 January 2016 Date and time of Field Visit 21.01.2016 02.00 p.m. - 07.00 p.m. All the members of field visit are requested to adhere to the programme schedule and time frame Please follow the directions of the team leader. Field Visit Guide 3 20-2 KILA’s International Conference Series January 2016 THINKERS WORKSHOP - Decentralisation and Development 4 Field Visit Guide Contents About Thrissur 1. India – from a two tier to three tier federation 1.1. The 73rd and 74th Amendments 1.2 Salient Features of the Constitutional Amendments 1.3. -

Name Middle Name Last Name Address Country State City PIN Details Amount Transfer to IEPF DILIP P SHAH IDBI BANK, C.O

Biocon Limited Amount for unclaimed and unpaid Final dividend for the FY 2006-07 Folio NO/Demat Due date for Name Middle Name Last Name Address Country State City PIN details Amount transfer to IEPF DILIP P SHAH IDBI BANK, C.O. G.SUBRAHMANYAM HEAD INDIA MAHARASHTRA MUMBAI 400093 BIO022473 150.00 23-AUG-2014 CAP MARK SERV PLOT 82/83 ROAD 7 STREET NO 15 MIDC, ANDHERI.EAST, MUMBAI SURAKA IDBI BANK LTD C/O G SUBRAMANYAM HEAD INDIA MAHARASHTRA MUMBAI 400093 BIO043568 150.00 23-AUG-2014 CAPITAL MKT SER C P U PLOT NO 82/83 ROAD NO 7 ST NO 15 OPP RAMBAXY LAB ANDHERI MUMBAI (E) RAMANUJ MISHRA IDBI BANK LTD C/O G SUBRAHMANYAM INDIA MAHARASHTRA MUMBAI 400093 BIO047663 150.00 23-AUG-2014 HEAD CAP MARK SERV CPU PL 82/83 RD 7 ST 15 OPP SPECAILITY RANBAXY LAB MIDC ANDHERI EAST MUMBAI URMILA LAXMAN SAWANT C/O KOTAK MAHINDRA BANK LTD VINAYA INDIA MAHARASHTRA MUMBAI 400098 BIO043838 150.00 23-AUG-2014 BHAVYA COMPLEX 5TH FLR 159-A CST ROAD KALINA SANTACRUZ E MUMBAI PHONE- 56768300 NEHA KAMLESH SHAH G SUBRAHMANYAM HEAD CAPITAL MARKET INDIA MAHARASHTRA MUMBAI 400093 BIO043408 150.00 23-AUG-2014 SERVISES CENTRAL PROCESSING UNIT PLOT NO 82/83 ROAD NO 7 STREET NO 5 MIDC ANDHERI (E) MUMBAI NO NA INDIA DELHI NEW DELHI BIO054733 150.00 23-AUG-2014 NO NA INDIA DELHI NEW DELHI BIO054734 150.00 23-AUG-2014 NO NA INDIA DELHI NEW DELHI BIO054748 150.00 23-AUG-2014 NO 305 GOLF MANOR WIND TUNNEL ROAD 23-AUG-2014 MANISH SALNI MURUGESHPALYA BANGALORE INDIA KARNATAKA BANGALORE 560017 BIO038066 150.00 33 GOVINDAPPA ROAD BASAVANGUDI L VENKATA NARAYANAN BANGALORE INDIA KARNATAKA -

Village Directory, Cochin

2 I f ' CENSUS OF 1941 VILLAGE DIRECTORY COCHIN STATE Price Re. 1/.. PREFACE The Imperial and State Census Tables to be published along with the Census Report will not give specific information relating to the villages and hence it is usual here to publish the village statistics in a separate volume. This practice was commended at the Census Conference held in New Delhi early in 1940 and it was , . also suggested then that fuller details in addition' to population figures should be incorporated in this volume. Agreeably to this suggestion the scope of this publication has been considerably enhanced this time. Thus the area, number of shops, medical (Government-owned or aided) and educational institutions and places of worship, population by main religions and communities and sects therein such as Ezhuvas, Nairs, Viswakarmalas, Depressed Classes, etc., among Hindus,, and" Ramo. Syrians, Latin Catholics, etc., among Christians, the nearest Railway station and distance thereto, important festivals, industries or other local details are all shown this time. In fact the ideal has been not to leave out any' important or interesting detail pertaining to any village. To limit space a number of symbols and abbreviations have been used. A list of these is ,;iven at the next page. It IS hoped that this volume will be found useful and interesting. " B. V. K. MENON Census Commissioner List of Abbreviations used in this volume Column No. Column No. (C) Coastal tract which is usually a centre of coir and 23 S Synagogue. coir yam manufacture. T Temple. (F) Festival. Number of people attendink is shown AD Aided Dispensary.