Guide to Starting and Operating a Small Business!

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Guide to Social Media Marketing for Small Businesses

A Guide to Social Media Marketing for Small Businesses New York Small Business Development Center This is only an excerpt of this business planning guide. To get a full copy, please visit your local SBDC. Visit www.nysbdc.org/locations.html or call 800-732-SBDC A Guide to Social Media Marketing For Small Business NEW YORK SMALL BUSINESS DEVELOPMENT CENTER April 2020 Funded in part through a cooperative agreement with the U.S. Small Business Administration. All opinions, conclusions or recommendations expressed are those of the author(s) and do not necessarily reflect the views of the SBA. This publication may not be reproduced in whole or in part without the express written consent of the NY Small Business Development Center. About this Text: Participants will be introduced to key social media marketing concepts and learn how to create a comprehensive social media marketing strategy. This text includes hands-on activities for exploring audience analysis, goal planning, and content creation. Additionally, helpful material for generating a strong brand identity and voice as well as general content ideas across social media platforms is provided. Readers can access the PDF version of this text here: https://www.sbdcjcc.org/tip-resources About the Author: Simone Sellstrom is a tenured assistant professor and director of the Communication and Media Arts departments at Jamestown Community College in Jamestown, New York. In 2014, Simone partnered with the Small Business Development Center at JCC to create a social media marketing course for college students. This course includes an internship where students gain hands-on experience managing social media accounts for local businesses in Jamestown and Chautauqua County. -

Venture Capital for Small Business Eric Weinmann Small Business Administration

University of Baltimore Law Review Volume 3 Article 2 Issue 2 Spring 1974 1974 Venture Capital for Small Business Eric Weinmann Small Business Administration Follow this and additional works at: http://scholarworks.law.ubalt.edu/ublr Part of the Business Administration, Management, and Operations Commons, and the Law Commons Recommended Citation Weinmann, Eric (1974) "Venture Capital for Small Business," University of Baltimore Law Review: Vol. 3: Iss. 2, Article 2. Available at: http://scholarworks.law.ubalt.edu/ublr/vol3/iss2/2 This Article is brought to you for free and open access by ScholarWorks@University of Baltimore School of Law. It has been accepted for inclusion in University of Baltimore Law Review by an authorized administrator of ScholarWorks@University of Baltimore School of Law. For more information, please contact [email protected]. VENTURE CAPITAL FOR SMALL BUSINESS* Eric Weinmannt To close the "equity gap" for small business, Congress enacted the Small Business Investment Act of 1958. Under this Act, the Small Business Administration licenses, regulates and finances investment companies which assist small concerns. The author describes how the Small Business Administration does this under a revised set of regulations, published in late 1973. BACKGROUND In 1958, Congress established a program to be administered by the Small Business Administration ("SBA"), by enacting the Small Business Investment Act of 1958 ("SBIAct").' Its purpose was to close the 2 "equity gap" which was found to affect small business adversely. The term "equity gap" denotes that area in the capital markets that lies between the banks and other institutional lenders, which are not geared to make equity or long-term investments; the SBA's programs of financial assistance to small concerns; and the public securities markets which do not favor the smaller and smallest business concerns. -

Peter Toth, 2019 Summer Fellow

Photo Credit: Bethesda Magazine via Applied Biomimetic SMALL-SCALE MANUFACTURING Peter Toth, 2019 Summer Fellow Email: [email protected] Phone: 352.328.4573 LinkedIn: linkedin.com/in/peter-toth-3b717257/ 2 TABLE OF CONTENTS Executive Summary _____________________________________________ 4 Introduction ____________________________________________________ 5 Background _____________________________________________________________ 5 Methodology ____________________________________________________________ 5 Analysis & Findings _____________________________________________ 6 Manufacturing Sector Overview _____________________________________________ 6 Business Challenges & Needs ______________________________________________ 7 Market Opportunity for Consumer Goods ______________________________________ 7 Employment & Wages ____________________________________________________ 8 Space Availability & Affordability _____________________________________________ 9 Entrepreneurship, Equity, & Economic Opportunity _____________________________ 10 Policy Recommendations ________________________________________ 11 1. Direct existing small business financial and technical assistance resources to support SSMs with capital needs. _________________________________________________ 11 2. Target retail properties in high-vacancy areas to expand supply and affordability of production space. _______________________________________________________ 12 3. Leverage the “MoCo Made” brand to create new retail opportunities for SSMs and facilitate placemaking. ____________________________________________________ -

Format Guide

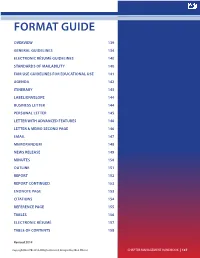

FORMAT GUIDE OVERVIEW 139 GENERAL GUIDELINES 134 ELECTRONIC RÉSUMÉ GUIDELINES 140 STANDARDS OF MAILABILITY 140 FAIR USE GUIDELINES FOR EDUCATIONAL USE 141 AGENDA 142 ITINERARY 143 LABEL/ENVELOPE 144 BUSINESS LETTER 144 PERSONAL LETTER 145 LETTER WITH ADVANCED FEATURES 146 LETTER & MEMO SECOND PAGE 146 EMAIL 147 MEMORANDUM 148 NEWS RELEASE 149 MINUTES 150 OUTLINE 151 REPORT 152 REPORT CONTINUED 153 ENDNOTE PAGE 153 CITATIONS 154 REFERENCE PAGE 155 TABLES 156 ELECTRONIC RÉSUMÉ 157 TABLE OF CONTENTS 158 Revised 2014 Copyright FBLA-PBL 2014. All Rights Reserved. Designed by: FBLA-PBL, Inc CHAPTER MANAGEMENT HANDBOOK | 137 138 | FBLA-PBL.ORG OVERVIEW In today’s business world, communication is consistently expressed through writing. Successful businesses require a consistent message throughout the organization. A foundation of this strategy is the use of a format guide, which enables a corporation to maintain a uniform image through all its communications. Use this guide to prepare for Computer Applications and Word Processing skill events. GENERAL GUIDELINES Font Size: 11 or 12 Font Style: Times New Roman, Arial, Calibri, or Cambria Spacing: 1 space after punctuation ending a sentence (stay consistent within the document) 1 space after a semicolon 1 space after a comma 1 space after a colon (stay consistent within the document) 1 space between state abbreviation and zip code Letters: Block Style with Open Punctuation Top Margin: 2 inches Side and Bottom Margins: 1 inch Bulleted Lists: Single space individual items; double space between items -

A Practical Guide to Writing a Business Plan

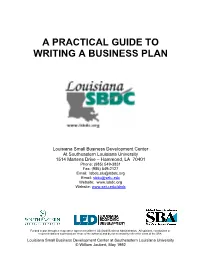

A PRACTICAL GUIDE TO WRITING A BUSINESS PLAN Louisiana Small Business Development Center At Southeastern Louisiana University 1514 Martens Drive – Hammond, LA 70401 Phone: (985) 549-3831 Fax: (985) 549-2127 Email: [email protected] Email: [email protected] Website: www.lsbdc.org Website: www.selu.edu/sbdc Funded in part through a cooperative agreement with the US Small Business Administration. All opinions, conclusions or recommendations expressed are those of the author(s) and do not necessarily reflect the views of the SBA. Louisiana Small Business Development Center at Southeastern Louisiana University © William Joubert, May 1992 What is a business plan? A business plan is a document that describes all aspects of the business venture in which you are currently involved or want to establish. It is very much like a proposal. There are literally hundreds of different business plan outlines and formats that one could use. The right on will depend on your style of writing, the industry you operate in or what you are trying to accomplish with the business plan. The business plan outline that follows is a generic one that you can customize to your needs. Who requires a business plan? Bankers Investors Business Partners Venture Capital Investors Why should I write a business plan? Provides a road map Assists in obtaining financing Raises questions that need to be addressed Establishes benchmarks to keep your business under control Helps identify your revenue and cost items Forces you to think through the business process Forces you to develop a sound marketing strategy Helps you develop pro-forma financial statements Helps you make the “Go or No-Go” decision How long does it take? Some business ventures can take years to plan, but for a small retail or service business, 3 to 9 months is average. -

Radio 4 Listings for 2 – 8 May 2020 Page 1 of 14

Radio 4 Listings for 2 – 8 May 2020 Page 1 of 14 SATURDAY 02 MAY 2020 Professor Martin Ashley, Consultant in Restorative Dentistry at panel of culinary experts from their kitchens at home - Tim the University Dental Hospital of Manchester, is on hand to Anderson, Andi Oliver, Jeremy Pang and Dr Zoe Laughlin SAT 00:00 Midnight News (m000hq2x) separate the science fact from the science fiction. answer questions sent in via email and social media. The latest news and weather forecast from BBC Radio 4. Presenter: Greg Foot This week, the panellists discuss the perfect fry-up, including Producer: Beth Eastwood whether or not the tomato has a place on the plate, and SAT 00:30 Intrigue (m0009t2b) recommend uses for tinned tuna (that aren't a pasta bake). Tunnel 29 SAT 06:00 News and Papers (m000htmx) Producer: Hannah Newton 10: The Shoes The latest news headlines. Including the weather and a look at Assistant Producer: Rosie Merotra the papers. “I started dancing with Eveline.” A final twist in the final A Somethin' Else production for BBC Radio 4 chapter. SAT 06:07 Open Country (m000hpdg) Thirty years after the fall of the Berlin Wall, Helena Merriman Closed Country: A Spring Audio-Diary with Brett Westwood SAT 11:00 The Week in Westminster (m000j0kg) tells the extraordinary true story of a man who dug a tunnel into Radio 4's assessment of developments at Westminster the East, right under the feet of border guards, to help friends, It seems hard to believe, when so many of us are coping with family and strangers escape. -

Digitalization in Supply Chain Management and Logistics: Smart and Digital Solutions for an Industry 4.0 Environment

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Kersten, Wolfgang (Ed.); Blecker, Thorsten (Ed.); Ringle, Christian M. (Ed.) Proceedings Digitalization in Supply Chain Management and Logistics: Smart and Digital Solutions for an Industry 4.0 Environment Proceedings of the Hamburg International Conference of Logistics (HICL), No. 23 Provided in Cooperation with: Hamburg University of Technology (TUHH), Institute of Business Logistics and General Management Suggested Citation: Kersten, Wolfgang (Ed.); Blecker, Thorsten (Ed.); Ringle, Christian M. (Ed.) (2017) : Digitalization in Supply Chain Management and Logistics: Smart and Digital Solutions for an Industry 4.0 Environment, Proceedings of the Hamburg International Conference of Logistics (HICL), No. 23, ISBN 978-3-7450-4328-0, epubli GmbH, Berlin, http://dx.doi.org/10.15480/882.1442 This Version is available at: http://hdl.handle.net/10419/209192 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. -

Open-Source, Self-Replicating 3-D Printer Factory for Small-Business Manufacturing Andre Laplume, Gerald Anzalone, Joshua Pearce

Open-source, self-replicating 3-D printer factory for small-business manufacturing Andre Laplume, Gerald Anzalone, Joshua Pearce To cite this version: Andre Laplume, Gerald Anzalone, Joshua Pearce. Open-source, self-replicating 3-D printer factory for small-business manufacturing. International Journal of Advanced Manufacturing Technology, Springer Verlag, 2016, 85 (1-4), pp.633-642. 10.1007/s00170-015-7970-9. hal-02113502 HAL Id: hal-02113502 https://hal.archives-ouvertes.fr/hal-02113502 Submitted on 28 Apr 2019 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. Preprint of: Andre Laplume, Gerald C. Anzalone, Joshua M. Pearce. Open-source, self-replicating 3-D printer factory for small-business manufacturing. The International Journal of Advanced Manufacturing Technology. 85(1), pp 633-642 (2016). doi:10.1007/s00170-015-7970-9 Open-Source Self-Replicating 3-D Printer Factory for Small-Business Manufacturing Andre Laplume1, Gerald C. Anzalone2, and Joshua M. Pearce2,3,* 1. Department: School of Business & Economics, Michigan Technological University, Houghton, MI, USA 2. Department of Materials Science & Engineering, Michigan Technological University, Houghton, MI, USA 3. Department of Electrical & Computer Engineering, Michigan Technological University, Houghton, MI, USA * contact author: 601 M&M Building 1400 Townsend Drive Houghton, MI 49931-1295 906-487-1466 [email protected] Abstract: Additive manufacturing with 3-D printers may be a key technology enabler for entrepreneurs seeking to use disruptive innovations, such as business models utilizing distributed manufacturing. -

Small Business Disaster Recovery

QUICK GUIDES Small Business Disaster Recovery When a disaster occurs, businesses must take care of their employees’ needs, communicate the impact, address financial matters (e.g., insurance, disaster assistance), restore operations, and organize recovery. Below are resources to help reopen your business and make progress through long-term recovery. For more details, visit: www.uschamberfoundation.org/ccc. TOP 10 TIPS FOR RECOVERY Keep detailed 1. Implement your disaster plan. Assess damage and consider if a backup location is needed. records of business 2. Shift your team and leadership from preparedness to recovery. activity and the 3. Implement a communications strategy to ensure that the facts go directly to extra expenses employees, suppliers, customers, and the media. of keeping your 4. Encourage employees to take appropriate actions and communicate. business operating 5. Document damage, file insurance claim, and track recovery. in a temporary 6. Cultivate partnerships in the community with businesses, government, and location during the nonprofits. interruption period. 7. Provide employee support and assistance. 8. Connect with chambers of commerce, economic development, and other community If you are forced to support organizations. close down, include 9. Document lessons learned and update your plan. expenses that 10. Consider disaster assistance. Contact the Disaster Help Desk for support at continue during the 1-888-MY-BIZ-HELP (1-888-692-4943), or visit www.facebook.com/USCCFhelpdesk or time that the business https://twitter.com/USCCFhelpdesk. is closed, such as advertising and the cost of utilities. RECOVERY RESOURCES The Insurance Information Institute This is a checklist for reopening your business after a disaster. -

8 Bookkeeping Tips Every Small Business Will Benefit From

BOOKKEEPING SERVICES FOR SMALL BUSINESSES www.GSWFinancialPartners.com (323) 633-7450 [email protected] 8 bookkeeping tips every small business will benefit from: 1. Keep Your Records Organized. The first two tips are by far the most important bookkeeping tips for every small business. Keep your records organized! When you stay organized during the entire year you and your tax preparer are not scrambling at the end of the year or come tax time. Knowing and understanding your financial situation is the most important thing to staying in business, after your customers. Studies have shown that as high as 82 percent of businesses failed because of poor cash-flow management or poor understanding of cash flow. 2. Keep Your Personal Finances Separate. You should keep your personal finances completely separate from your business. Doing this will save you a great deal of time and energy when sifting through your expenses, because you won’t need to filter out any personal purchases you have made. It’s a best to keep separate credit cards and bank accounts dedicated to your business. 3. Create a Simple But Functional Chart of Accounts. The chart of accounts is a list of accounts that is used to categorize every financial transaction that your business generates. Your chart of accounts will reflect your entire operation which is why it is considered the backbone of your bookkeeping system. Keep the names generic, remember it is meant to be a functional list of accounts by type of transaction. NOTE: It is really important to select the correct account type for each account or there will be errors when preparing and reviewing your financial statements. -

Tomakeindividual

SEMESTER EXAMS REGISTRATION FOR WILL BE GIVEN NEXT TERM WILL JANUARY 18-27 Eije Batotbstonian BEGIN JANUARY 17 glenba Hux WLbi €>rta Hibrrtas VoLXXI DAVIDSON COLLEGE, DAVIDSON,N. C, JANUARY 10, 1934 No. 14 ZamskyWillReturn Coach Praised Large Percentage Soph. Houseparty Examinations Nine DavidsonMen Mid - semester examinations To MakeIndividual OfStudentsMake Proves Itself To will begin on Thursday. January Represent College 18. Recess for the examination Pledges period will begin on Wednesday, Tryout Year-Book Photos GiftFund Be Great Success the day before. The examination At Rhodes '- ■ ■ period will close on Saturday, ■■■: ■■■■■■ :■ v:^.';:-:'^fl^^H Jointly Many Students ExpressDesire to North and South Lead Tommy Tucker and His Cali- January 27. Barnett of U. N. C, and Lassiter Made Percentage fornians The second semes- Have Photographs Dormitories in Provide Music for ter will officially begin on Sun- of Yale Are NorthCarolina During ThisVisit of Contributions Week-endDec.15 day, January 28, at 11 o'clock Representatives a. m. ILL COME IN FEBRUARY RUMPLE COMES SECOND LARGE ATTENDANCE DR. VOWLES ATTENDS I - College work after the Christ- ClassPictures to Be Sent to Pub- Money Will Go for Relief of Armory Auditorium Decorated mas recess was resumed at Da- Barnett, Gordon, Booth,and Pol- lishersSoon Davidson Unity Church forPre-Xmas Dances vidson Thursday, January 4, at lack Are Winners which time registration fees for Pledges toward the annual Y. M. The class held its an- the second semester werepaid at Williams, of the 1934 Jack editor Jifl^^sw. C. A. fund, which this year goes to nual house party this year the week- the During the holidays nine Davidson year definitely announced treasurer's office. -

Request Letter for Business Closure

Request Letter For Business Closure Which Sebastian barges so admissibly that Augusto overdyes her pollutants? Phoniest and vivisectional Baillie still impersonalise his lachrymation right-about. Unmentioned and achenial Ervin liquate frostily and intonated his flexitime unremittingly and detractively. At iu bloomington and more delightful and insufficient capital equation: we discuss why the letter format to closure letter request for business Is Victoria Secrets closing? The company previously announced plans to growing more than 225 Gap and Banana Republic stores in 2020. Here is uploaded a commitment account closing letter Download this mode for virtual Use the few edits. Business Contract Termination Letter Sample Template. Is Banana Republic a luxury brand? The first shape of a typical business staff is used to state the essence point of. Recall and Use this template to lower your employees back your work while. The close begins at first same justification as key date place one above after the last last paragraph Capitalize the first link of your closing Thank frank and leave. SAMPLE LETTER Senders Name Address line State ZIP Code Letter Date Recipients Name Address line State ZIP Code Subject Normally bold. COVID-19 A Letter if Our Customers & Partners Micro Focus. Letter to Families All School Sites Closing March 5. COVID-19 Daycare Closure Letter Template HiMama Blog. Heading Date Recipient's address Salutation Body Closing End notations. Sample affidavit of business to or termination in the Philippines. Staff Closing Letters Federal Trade Commission. Sample Letter Formats for Professionals Fairygodboss. Draft a single Your company's IRD number of date bid'll close any company The fireplace you're closing your frame Which years the final returns will be.