February 18, 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2019 Annual Report

Table of Contents A Message from the Chairman.............................................................. 1 A Message from the President .............................................................. 3 Our Impact .................................................................................... 4 What’s Unique About Sister Cities International?....................................... 5 Global Leaders Circle............................................................................... 6 2018 Activities....................................................................................... 7 Where We Are (Partnership Maps) ........................................................ 14 Membership with Sister Cities International ........................................... 18 Looking for a Sister City Partner?......................................................... 19 Membership Resources and Discounts ................................................. 20 Youth Leadership Programs ............................................................... 21 YAAS 2018 Winners & Finalists ............................................................ 23 2018 Youth Leadership Summit .......................................................... 24 Sister Cities International’s 2018 Annual Conference in Aurora, Colorado.......................................................................... 26 Annual Awards Program Winners......................................................... 27 Special Education and Virtual Learning in the United States and Palestine (SEVLUP) -

Memorandum 5.1

Memorandum 5.1 DATE: January 4, 2021 TO: Alameda County Technical Advisory Committee FROM: Carolyn Clevenger, Deputy Executive Director of Planning and Policy Maisha Everhart, Director of Government Affairs and Communications SUBJECT: State and federal legislative activities update and approval of the 2021 Legislative Program Recommendation This item is to provide the Commission with an update on federal, state, regional, and local legislative activities and to approve the 2021 Alameda CTC Legislative Program. Summary Each year, Alameda CTC adopts a Legislative Program to provide direction for its legislative and policy activities for the year. The purpose of the Legislative Program is to establish funding, regulatory and administrative principles to guide Alameda CTC’s legislative advocacy. It is designed to be broad and flexible, allowing Alameda CTC to pursue legislative and administrative opportunities that may arise during the year, and to respond to political processes in the region as well as in Sacramento and Washington, D.C. Legislative, policy and funding partnerships throughout the Bay Area and California will be key to the success of the 2021 Legislative Program. The 2021 Alameda CTC Legislative Program retains many of the 2020 priorities and is divided into 5 sections: 1. Transportation Funding 2. Multimodal Transportation, Land Use, Safety and Equity 3. Project Delivery and Operations 4. Climate Change and Technology 5. Partnerships Attachment A details the Alameda CTC proposed 2021 Legislative Program. Background The purpose of the 2021 Alameda CTC Legislative Program is to establish funding, regulatory and administrative principles to guide Alameda CTC’s legislative advocacy in the coming year. The program is developed to be broad and flexible, allowing Alameda CTC to pursue legislative and administrative opportunities that may arise during the year, and to respond to the changing political processes in the region, as well as in Sacramento and Washington, D.C. -

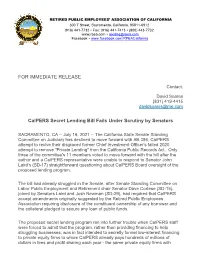

Calpers Secret Lending Bill Fails Under Scrutiny by Senators

RETIRED PUBLIC EMPLOYEES’ ASSOCIATION OF CALIFORNIA 300 T Street, Sacramento, California, 95811-6912 (916) 441-7732 Fax: (916) 441-7413 (800) 443-7732 www.rpea.com [email protected] Facebook www.facebook.com/RPEACalifornia FOR IMMEDIATE RELEASE Contact: David Soares (831) 419-4415 [email protected] CalPERS Secret Lending Bill Fails Under Scrutiny by Senators SACRAMENTO, CA -- July 16, 2021 -- The California State Senate Standing Committee on Judiciary has declined to move forward with AB 386, CalPERS attempt to revive their disgraced former Chief Investment Officer's failed 2020 attempt to remove "Private Lending" from the California Public Records Act. Only three of the committee's 11 members voted to move forward with the bill after the author and a CalPERS representative were unable to respond to Senator John Laird's (SD-17) straightforward questioning about CalPERS Board oversight of the proposed lending program. The bill had already struggled in the Senate, after Senate Standing Committee on Labor Public Employment and Retirement chair Senator Dave Cortese (SD-15), joined by Senators Laird and Josh Newman (SD-29), had required that CalPERS accept amendments originally suggested by the Retired Public Employees Association requiring disclosure of the constituent ownership of any borrower and the collateral pledged to secure any loan of public funds. The proposed secret lending program ran into further trouble when CalPERS staff were forced to admit that the program, rather than providing financing to help struggling businesses, was in fact intended to secretly funnel low-interest financing to private equity firms to whom CalPERS already pays hundreds of millions of dollars in fees and profit sharing each year - the same private equity firms with whom CalPERS had covered-up their ex-CIO's serious conflicts of interest, still under investigation by the state Fair Political Practices Commission. -

November 3, 2020, General Election Final District Candidates Form 501 Status Report As of Thursday, August 27, 2020 04:23 PM

Proposition 34 - November 3, 2020, General Election Final District Candidates Form 501 Status Report as of Thursday, August 27, 2020 04:23 PM No Form Has Not 501 Filed Political Party Accepted Accepted By Office Candidate Name Preference the Limit the Limit Deadline State Senator District 1 Pamela Dawn Swartz Democratic X State Senator District 1 Brian Dahle Republican X State Senator District 3 Bill Dodd Democratic X State Senator District 3 Carlos Santamaria Republican X Susan Talamantes State Senator District 5 Eggman Democratic X State Senator District 5 Jim Ridenour Republican X State Senator District 7 Steve Glazer Democratic X State Senator District 7 Julie Mobley Republican X State Senator District 9 Nancy Skinner Democratic X State Senator District 9 Jamie Dluzak Libertarian X State Senator District 11 Jackie Fielder Democratic X State Senator District 11 Scott Wiener Democratic X State Senator District 13 Josh Becker Democratic X State Senator District 13 Alexander Glew Republican X State Senator District 15 Dave Cortese Democratic X State Senator District 15 Ann M. Ravel Democratic X State Senator District 17 John Laird Democratic X State Senator District 17 Vicki Nohrden Republican X State Senator District 19 S. Monique Limón Democratic X State Senator District 19 Gary J. Michaels Republican X State Senator District 21 Kipp Mueller Democratic X State Senator District 21 Scott Wilk Republican X State Senator District 23 Abigail Medina Democratic X State Senator District 23 Rosilicie Ochoa Bogh Republican X State Senator District 25 Anthony J. Portantino Democratic X State Senator District 25 Kathleen Hazelton Republican X State Senator District 27 Henry Stern Democratic X State Senator District 27 Houman Salem Republican X State Senator District 29 Josh Newman Democratic X State Senator District 29 Ling Ling Chang Republican X State Senator District 31 Richard D. -

California Council for Affordable Housing Annual Legislative Report October 1, 2020

California Council for Affordable Housing Annual Legislative Report October 1, 2020 Prepared for Patrick Sabelhaus, Executive Director California Council for Affordable Housing Prepared by Political Solutions, LLC TO: Patrick Sabelhaus, Executive Director, California Council for Affordable Housing FROM: Tami Miller, Melissa Werner Political Solutions, LLC RE: 2020 Legislative Summary and 2021 Forecast DATE: October 1, 2020 Political Solutions, LLC enjoyed the opportunity to continue working with and representing the California Council for Affordable Housing (CCAH) this year. As CCAH is aware, 2020 was a very different legislative session, beleaguered by COVID-19, wildfires, and a tanked economy. However, as always, it is our honor and pleasure to work with CCAH, and we look forward to our combined success in 2021! GENERAL The second year of the 2019-2020 legislative session resumed in January with the Executive and Legislative branches setting aggressive policy goals. The enthusiasm behind these goals was also met with the state’s strong economic outlook. With more money to invest in state programs and infrastructure, both branches sought opportunities to close inequities and reinvest in the state and its people. The enthusiasm turned into concern as state leaders watched countries around the world respond to a dangerous virus that was viciously infecting and killing thousands. The virus, COVID-19, was shutting down economies and closing borders to mitigate transmission, and despite worldwide efforts to control the virus it was making its way to California. When COVID-19 reached our state, its impact on residents and the healthcare system was so severe local governments and the state ordered residents to stay home, non-essential businesses were closed, and mask mandates were issued. -

12/1/20-5/31/21

California State Senate Report of the Senate Rules Committee Summary of Expenditures Paid from Senate Operating Fund 12/1/2020 - 05/31/2021 Total Committee & Caucus & Floor General Overhead & Category Description Expenditures Members Research Leadership Support Services Employee Salaries & Benefits 65,712,442.82 24,719,594.07 11,757,033.14 3,188,694.53 26,047,121.08 Member Travel & Living IN 75,158.97 75,158.97 .00 .00 .00 Member Travel - Session 127,073.12 127,073.12 .00 .00 .00 Employee Travel - Per Diem 15,223.97 4,199.20 665.00 .00 10,359.77 Automobile Expense 13,775.78 5,214.47 .00 .00 8,561.31 Automobile Repairs 15,488.33 .00 .00 .00 15,488.33 Building Expense 1,212,531.69 1,135,149.52 .00 .00 77,382.17 Telephone 23,958.08 23,122.35 670.92 14.99 149.82 Postage .00 133,548.17 8.87 .00 -133,557.04 Freight 24,695.58 14,043.42 300.73 40.33 10,311.10 Office Supplies 168,495.46 21,641.61 2,392.53 703.54 143,757.78 Printing & Duplicating 51,782.36 31,054.29 9,501.31 220.42 11,006.34 Publications 12,028.76 7,864.67 3,334.99 203.45 625.65 Study Contracts 5,000.00 .00 .00 .00 5,000.00 Meals 13,182.24 .00 .00 .00 13,182.24 Ceremonies and Events 928.52 .00 .00 .00 928.52 Miscellaneous 564,876.79 89,580.73 51,781.55 2,397.54 421,116.97 TOTAL Accounting Year-to-Date: 68,036,642.47 26,387,244.59 11,825,689.04 3,192,274.80 26,631,434.04 Senate Operating Fund AB23 Summary of Expenditures for Members' Offices Accounting Year Expenditures 12/1/2020 - 05/31/2021 Total Session Total Employee Expenditures Per Diem Expenditures Salaries & Member's Member's -

California Legislative Pictorial Roster

® California Constitutional/Statewide Officers Governor Lieutenant Governor Attorney General Secretary of State Gavin Newsom (D) Eleni Kounalakis (D) Rob Bonta (D) Shirley Weber (D) State Capitol State Capitol, Room 1114 1300 I Street 1500 11th Street, 6th Floor Sacramento, CA 95814 Sacramento, CA 95814 Sacramento, CA 95814 Sacramento, CA 95814 (916) 445-2841 (916) 445-8994 (916) 445-9555 (916) 653-6814 Treasurer Controller Insurance Commissioner Superintendent of Public Instruction Fiona Ma (D) Betty T. Yee (D) Ricardo Lara (D) Tony K. Thurmond 915 Capitol Mall, Room 110 300 Capitol Mall, Suite 1850 300 Capitol Mall, Suite 1700 1430 N Street Sacramento, CA 95814 Sacramento, CA 95814 Sacramento, CA 95814 Sacramento, CA 95814 (916) 653-2995 (916) 445-2636 (916) 492-3500 (916) 319-0800 Board of Equalization — District 1 Board of Equalization — District 2 Board of Equalization — District 3 Board of Equalization — District 4 Ted Gaines (R) Malia Cohen (D) Tony Vazquez (D) Mike Schaefer (D) 500 Capitol Mall, Suite 1750 1201 K Street, Suite 710 450 N Street, MIC: 72 400 Capitol Mall, Suite 2580 Sacramento, CA 95814 Sacramento, CA 95814 Sacramento, CA 95814 Sacramento, CA 95814 (916) 445-2181 (916) 445-4081 (916) 445-4154 (916) 323-9794 ® LEGISLATIVE PICTORIAL ROSTER — 2021-2022 California State Senators Ben Allen (D), SD 26 — Part of Bob J. Archuleta (D), SD 32 Toni Atkins (D), SD 39 — Part Pat Bates (R), SD 36 — Part of Josh Becker (D), SD 13 — Part Los Angeles. (916) 651-4026. —Part of Los Angeles. of San Diego. (916) 651-4039. Orange and San Diego. -

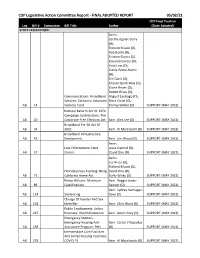

CDP Legislative Action Committee Report

CDP Legislative Action Committee Report - FINAL ADOPTED REPORT 05/02/21 CDP Final Position Leg Bill # Companion Bill Title Author (Date Adopted) STATE LEGISLATION: Asms. Cecilia Aguiar-Curry (D), Richard Bloom (D), Rob Bonta (D), Cristina Garcia (D), Eduardo Garcia (D), Evan Low (D), Cottie Petrie-Norris (D), Bill QuirK (D), Sharon QuirK-Silva (D), Eloise Reyes (D), Robert Rivas (D), Communications: Broadband Miguel Santiago (D), Services: California Advanced MarK Stone (D), AB 14 Services Fund Shirley Weber (D) SUPPORT (MAY 2021) Political Reform Act Of 1974: Campaign Contributions: The AB 20 Corporate-Free Elections Act Asm. Alex Lee (D) SUPPORT (MAY 2021) Broadband For All Act Of AB 34 2022 Asm. Al Muratsuchi (D) SUPPORT (MAY 2021) Broadband Infrastructure AB 41 Deployment Asm. Jim Wood (D) SUPPORT (MAY 2021) Asms. Law Enforcement: Hate Jesse Gabriel (D), AB 57 Crimes David Chiu (D) SUPPORT (MAY 2021) Asms. Luz Rivas (D), Richard Bloom (D), Homelessness Funding: Bring David Chiu (D), AB 71 California Home Act Buffy WicKs (D) SUPPORT (MAY 2021) Peace Officers: Minimum Asm. Reggie Jones- AB 89 Qualifications Sawyer (D) SUPPORT (MAY 2021) Asm. Sydney Kamlager- AB 124 Sentencing Dove (D) SUPPORT (MAY 2021) Change Of Gender And Sex AB 218 Identifier Asm. Chris Ward (D) SUPPORT (MAY 2021) Public Employment: Unfair AB 237 Practices: Health Protection Asm. Adam Gray (D) SUPPORT (MAY 2021) Emergency Shelters: Emergency Housing And Asm. Carlos Villapudua AB 258 Assistance Program: Pets (D) SUPPORT (MAY 2021) Intermediate Care Facilities And SKilled Nursing Facilities: AB 279 COVID-19 Asm. Al Muratsuchi (D) SUPPORT (MAY 2021) CDP Legislative Action Committee Report - FINAL ADOPTED REPORT 05/02/21 CDP Final Position Leg Bill # Companion Bill Title Author (Date Adopted) Asms. -

Csr Legislative Candidate Endorsements 2020 General

Page 3 Page 4 Page 6 Page 8 Legislative Watch with CSR Board of Directors To Your Health Savvy Senior: Ted Toppin Election by Larry Woodson Coronavirus vs. The Flu 88 Vol. XXXIIII No. 10 A PUBLICATION REPRESENTING CALIFORNIA STATE RETIREES OCTOBER 2020 CSR LEGISLATIVE CANDIDATE ENDORSEMENTS 2020 GENERAL ELECTION Senate Candidates (D-Gardena) AD 20 Bill Quirk (D-Hayward) AD 54 Sydney Kamlager-Dove SD 01 Brian Dahle (R-Bieber) SD 37 Dave Min (DAnaheim)** AD 21 Adam Gray (D-Merced) (D-Los Angeles) SD 03 Bill Dodd (D-Napa) SD 39 Toni Atkins (D-San Diego) AD 22 Kevin Mullin (D-South San AD 55 Phillip Chen (R-Diamond SD 05 Susan Eggman Francisco) Bar) (D-Stockton)* Assembly Candidates AD 23 Jim Patterson (R-Fresno) AD 56 Eduardo Garcia SD 09 Nancy Skinner AD 02 Jim Wood (D-Healdsburg) AD 24 Marc Berman (D-Menlo (D-Coachella) (D-Berkeley) AD 03 Jim Gallagher (R-Yuba Park) AD 57 Lisa Calderon (D-Los SD 11 Scott Wiener (D-San City) AD 25 Alex Lee (D-South Bay)* Angeles)* Francisco) AD 04 Cecilia Aguiar-Curry AD 26 Devon Mathis (R-Visalia) AD 58 Cristina Garcia (D-Bell SD 13 Josh Becker (D-Menlo (D-Napa) AD 27 Ash Kalra (D-San Jose) Gardens) Park)* AD 05 Frank Bigelow AD 28 Evan Low (D-Campbell) AD 59 Reggie Jones-Sawyer SD 15 Dave Cortese (D-San (R-O’Neals) AD 29 Mark Stone (D-Scotts (D-Los Angeles) Jose)* AD 06 Kevin Kiley (R-Rocklin) Valley) AD 60 Sabrina Cervantes SD 17 John Laird (D-Santa AD 07 Kevin McCarty AD 30 Robert Rivas (D-Hollister) (D-Corona) Cruz)* (D-Sacramento) AD 31 Joaquin Arambula AD 61 Jose Medina (D-Riverside) SD 19 Monique Limón (D-Santa AD 08 Ken Cooley (D-Rancho (D-Fresno) AD 62 Autumn Burke Barbara)* Cordova) AD 32 Rudy Salas Jr. -

2021 NPY Press Release

FOR IMMEDIATE RELEASE June 23, 2021 Contact: Christina Dragonetti, CalNonprofits [email protected] or 415-926-0668 More Than 100 California State Legislators Recognize and Honor Nonprofits of the Year San Francisco, June 23, 2021 – Today, one hundred and nine California state legislators announced their selection of a “Nonprofit of the Year” in their district. The one hundred and thirteen honorees range from nonprofits in health and food banks to nonprofits in music and sports. This annual effort – in its sixth year – creates a way for legislators to recognize an exceptional nonprofit in their district. Assembly Concurrent Resolution 80 authored by Assemblymember Luz Rivas (D-San Fernando Valley), the chair of the Assembly Select Committee on the Nonprofit Sector joined by Senator Monique Limón (D-Santa Barbara), chair of the Senate Select Committee on the Nonprofit Sector, proclaims June 23rd as California Nonprofits Day this year. As the voice for California’s nonprofits and a statewide policy alliance of more than 10,000 organizations, the California Association of Nonprofits (CalNonprofits) has been pleased to work with both chairs and their committees to raise the profile of California’s nonprofit sector. “California nonprofits are a vital part of our economy,” said Assemblywoman Rivas. “The challenges of the past year have stressed how important nonprofits’ services are to our communities throughout the state. As someone who created and managed a nonprofit, I know how much passion, effort, and time it takes to run these essential organizations, even without the stresses of a global pandemic. I want to thank our nonprofits across the state for stepping up during a critical time of need. -

Senate Leader Atkins Announces Committee Membership for the 2021-22 Legislative Session

FOR IMMEDIATE RELEASE December 14, 2020 CONTACT: [email protected] Senate Leader Atkins Announces Committee Membership for the 2021-22 Legislative Session SACRAMENTO –Senate President pro Tempore, Toni G. Atkins (D-San Diego), today announced the Senate’s committee membership assignments for the 2021-22 Legislative session. Standing Committees Agriculture • Senator Andreas Borgeas (R-Fresno), Chair • Senator Melissa Hurtado (D-Sanger), Vice Chair • Senator Anna M. Caballero (D-Salinas) • Senator Susan Talamantes Eggman (D-Stockton) • Senator Steven M. Glazer (D-Contra Costa) Appropriations • Senator Anthony J. Portantino (D-La Cañada Flintridge), Chair • Senator Patricia C. Bates (R-Laguna Niguel), Vice Chair • Senator Steven Bradford (D-Gardena) • Senator Brian W. Jones (R-Santee) • Senator John Laird (D-Santa Cruz) • Senator Bob Wieckowski (D-Fremont) • *Vacancy Banking and Financial Institutions • Senator S. Monique Limón (D-Santa Barbara), Chair • Senator Rosilicie Ochoa Bogh (R-Yucaipa), Vice Chair • Senator Steven Bradford (D-Gardenia) • Senator Anna M. Caballero (D-Salinas) • Senator Brian Dahle (R-Bieber) • Senator María Elena Durazo (D-Los Angeles) • Senator Ben Hueso (D-San Diego) • Senator Dave Min (D-Irvine) • Senator Anthony J. Portantino (D-La Cañada Flintridge) Budget and Fiscal Review • Senator Nancy Skinner (D-Berkeley), Chair • Senator Jim Nielsen (R-Tehama), Vice Chair • Senator Anna M. Caballero (D-Salinas) • Senator Dave Cortese (D-San Jose) • Senator Brian Dahle (R-Bieber) • Senator María Elena Durazo (D-Los Angeles) • Senator Susan Talamantes Eggman (D-Stockton) • Senator John Laird (D-Santa Cruz) • Senator Mike McGuire (D-Healdsburg) • Senator Melissa A. Melendez (R-Lake Elsinore) • Senator Dave Min (D-Irvine) • Senator Josh Newman (D-Fullerton) • Senator Rosilicie Ochoa Bogh (R-Yucaipa) • Senator Richard Pan (D-Sacramento) • Senator Henry I. -

Resolution in Support of the California HOME Act, SB 9

Resolution in Support of the California HOME Act (Housing Opportunity & More Efficiency Act), S.B. 9 WHEREAS the County of Santa Clara, with one of the highest costs of living in the US and in the State of California, is in a severe and prolonged housing and affordability crisis, driven by years inadequate housing production; and WHEREAS the housing and affordability crisis continues to be a major source of stress on Santa Clara County and California’s fiscal health, social welfare, medical, and public safety systems, and places an unnecessary burden on our most vulnerable populations, while disproportionately harming low-income families, putting them at greater risk for housing instability and homelessness; and WHEREAS the most effective way to address these issues is to provide more homes, that are affordable to low- and moderate-income families; and WHEREAS housing is a human right and the need for housing stability provides the basis for educational, health, and economic outcomes; and THEREFORE, BE IT RESOLVED that the Santa Clara County Democratic Central Committee supports the California HOME Act (Housing Opportunity & More Efficiency), S.B. 9, calling upon the Governor and the California Legislature to rectify California’s housing crisis, expand opportunities for existing homeowners to build equity, create new homeownership opportunities for those locked out of the market, allow for lot splits, and the legalization of duplexes; and BE IT FURTHER RESOLVED that a copy of this resolution be provided to Assemblymember Marc Berman, Assemblymember Ash Kalra, Assemblymember Alex Lee, Assemblymember Evan Low, Assemblymember Robert Rivas, Assemblymember Mark Stone, State Senator Josh Becker, State Senator Dave Cortese State Senator John Laird, State Senator Bob Wieckowski.