United States Securities and Exchange Commission Washington, D.C

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PUBLIC NOTICE Federal Communications Commission 445 12Th St., S.W

PUBLIC NOTICE Federal Communications Commission 445 12th St., S.W. News Media Information 202 / 418-0500 Internet: https://www.fcc.gov Washington, D.C. 20554 TTY: 1-888-835-5322 DA 18-782 Released: July 27, 2018 MEDIA BUREAU ESTABLISHES PLEADING CYCLE FOR APPLICATIONS FILED FOR THE TRANSFER OF CONTROL AND ASSIGNMENT OF BROADCAST TELEVISION LICENSES FROM RAYCOM MEDIA, INC. TO GRAY TELEVISION, INC., INCLUDING TOP-FOUR SHOWINGS IN TWO MARKETS, AND DESIGNATES PROCEEDING AS PERMIT-BUT-DISCLOSE FOR EX PARTE PURPOSES MB Docket No. 18-230 Petition to Deny Date: August 27, 2018 Opposition Date: September 11, 2018 Reply Date: September 21, 2018 On July 27, 2018, the Federal Communications Commission (Commission) accepted for filing applications seeking consent to the assignment of certain broadcast licenses held by subsidiaries of Raycom Media, Inc. (Raycom) to a subsidiary of Gray Television, Inc. (Gray) (jointly, the Applicants), and to the transfer of control of subsidiaries of Raycom holding broadcast licenses to Gray.1 In the proposed transaction, pursuant to an Agreement and Plan of Merger dated June 23, 2018, Gray would acquire Raycom through a merger of East Future Group, Inc., a wholly-owned subsidiary of Gray, into Raycom, with Raycom surviving as a wholly-owned subsidiary of Gray. Immediately following consummation of the merger, some of the Raycom licensee subsidiaries would be merged into Gray Television Licensee, LLC (GTL), with GTL as the surviving entity. The jointly filed applications are listed in the Attachment to this Public -

Appendix a Stations Transitioning on June 12

APPENDIX A STATIONS TRANSITIONING ON JUNE 12 DMA CITY ST NETWORK CALLSIGN LICENSEE 1 ABILENE-SWEETWATER SWEETWATER TX ABC/CW (D KTXS-TV BLUESTONE LICENSE HOLDINGS INC. 2 ALBANY GA ALBANY GA NBC WALB WALB LICENSE SUBSIDIARY, LLC 3 ALBANY GA ALBANY GA FOX WFXL BARRINGTON ALBANY LICENSE LLC 4 ALBANY-SCHENECTADY-TROY ADAMS MA ABC WCDC-TV YOUNG BROADCASTING OF ALBANY, INC. 5 ALBANY-SCHENECTADY-TROY ALBANY NY NBC WNYT WNYT-TV, LLC 6 ALBANY-SCHENECTADY-TROY ALBANY NY ABC WTEN YOUNG BROADCASTING OF ALBANY, INC. 7 ALBANY-SCHENECTADY-TROY ALBANY NY FOX WXXA-TV NEWPORT TELEVISION LICENSE LLC 8 ALBANY-SCHENECTADY-TROY PITTSFIELD MA MYTV WNYA VENTURE TECHNOLOGIES GROUP, LLC 9 ALBANY-SCHENECTADY-TROY SCHENECTADY NY CW WCWN FREEDOM BROADCASTING OF NEW YORK LICENSEE, L.L.C. 10 ALBANY-SCHENECTADY-TROY SCHENECTADY NY CBS WRGB FREEDOM BROADCASTING OF NEW YORK LICENSEE, L.L.C. 11 ALBUQUERQUE-SANTA FE ALBUQUERQUE NM CW KASY-TV ACME TELEVISION LICENSES OF NEW MEXICO, LLC 12 ALBUQUERQUE-SANTA FE ALBUQUERQUE NM UNIVISION KLUZ-TV ENTRAVISION HOLDINGS, LLC 13 ALBUQUERQUE-SANTA FE ALBUQUERQUE NM PBS KNME-TV REGENTS OF THE UNIV. OF NM & BD.OF EDUC.OF CITY OF ALBUQ.,NM 14 ALBUQUERQUE-SANTA FE ALBUQUERQUE NM ABC KOAT-TV KOAT HEARST-ARGYLE TELEVISION, INC. 15 ALBUQUERQUE-SANTA FE ALBUQUERQUE NM NBC KOB-TV KOB-TV, LLC 16 ALBUQUERQUE-SANTA FE ALBUQUERQUE NM CBS KRQE LIN OF NEW MEXICO, LLC 17 ALBUQUERQUE-SANTA FE ALBUQUERQUE NM TELEFUTURKTFQ-TV TELEFUTURA ALBUQUERQUE LLC 18 ALBUQUERQUE-SANTA FE CARLSBAD NM ABC KOCT KOAT HEARST-ARGYLE TELEVISION, INC. -

Federal Communications Commission Record 10 FCC Red No

DA 95-1755 Federal Communications Commission Record 10 FCC Red No. 17 clusive of others, based on measured viewing patterns. Before the Essentially, each county in the United States is allocated to Federal Communications Commission a market based on which home-market stations receive a Washington, D.C. 20554 preponderance of total viewing hours in the county. For purposes of this calculation, both over-the-air and cable television viewing are included.3 In re: 3. Under the Act, however, the Commission is also di rected to consider changes in ADI areas. Section 4 provides Multimedia WMAZ, Inc. CSR-4182-A that the Commission may: Macon, Georgia with respect to a particular television broadcast sta For Modification of Station tion, include additional communities within its tele WMAZ-TV©s ADI vision market or exclude communities from such station©s television market to better effectuate the purposes of this section. MEMORANDUM OPINION AND ORDER In considering such requests, the Act provides that: Adopted: August 3,1995; Released: August 17,1995 the Commission shall afford particular attention to By the Deputy Chief, Cable Services Bureau: the value of localism by taking into account such factors as - (I) whether the station, or other stations located in INTRODUCTION the same area, have been historically carried on the 1. In the captioned proceeding, Multimedia WMAZ, Inc., cable system or systems within such community; licensee of station WMAZ-TV (CBS, Channel 13), Macon, Georgia (hereinafter "WMAZ-TV") has requested the Com (II) whether the -

View Annual Report

The origin of Gray Communications Systems, Inc. dates back more than 100 years to a single, local newspaper in Albany, Georgia. In 1967, Gray underwent its first initial public offering. In 1992, Gray operated three television stations and one daily newspaper, which generated $24.6 million in revenue and Gray’s total market capitalization was $49.6 million. After the infusion of a significant equity investment in 1993, Gray’s strategic direction changed. This change fueled both internal and external growth by improving existing operations and by leading to 10 strategic acquisitions. Today, Gray operates 10 major network-affiliated television stations, four daily newspapers, including the original Albany, Georgia newspaper, a weekly advertising shopper in southwest Georgia, a communications and paging business and one of the largest fleets of satellite uplink trucks in the Southeast. Revenues for 1998 totaled $128.9 million and Gray’s market capitalization grew to $479.6 million. Gray has continued its tradition of 31 consecutive years of paying dividends. How will Gray Communications Systems, Inc. continue to build stockholder value? The same way we have since 1993, by focusing on local interests to enhance the value of Gray’s existing operations and, when appropriate, selectively acquiring properties that provide opportunities Communications Systems, Inc. Communications Systems, to strengthen stockholder value. annual report Communications Systems, Inc. At a Glance Gray Communications Systems, Inc. is a communications company whose primary mission is to provide quality news and entertainment services to the local markets in which the Company operates. Our commitment to local interests and a selective acquisition strategy provides growth opportunities, which builds long-term value for our stockholders. -

1832280004.Pdf

Federal· Communications Commission FCC 97-116 REPLY COMMENTS OF FOURTH NOTICE OF PROPOSED RULEMAKING and THIRD NOTICE OF INQUIRY ATVIHDTV (DOCKET NO. 87-268) Filed by: Date Filed: Abacus Television Jan. 16, 1996 Alliance for Community Media Jan. 22, 1996 Ameritech New Media Enterprises, Inc. Jan. 16, 1996 Ann Arbor Community Television Network Jan. 12, 1996 Apple Computer, Inc. Jan. 22, 1996 Association of America's Public TV Stations & the Public B'casting Service Jan. 22, 1996 Bell Atlantic Jan. 22, 1996 Benton Foundation Feb. 1, 1996 Blue Mountain Translator Jan. 22, 1996 Broadcasters' Jan. 22, 1996 Business Software Alliance Jan. 23, 1996 Capital Community Television Jan. 16, 1996 Children Now Jan. 16, 1996 Cincinnati Community Video Jan. 16, 1996 Comcast Cable Communications, Inc. Jan. 22, 1996 Community Assess Television Jan. 18, 1996 Community Access Televisoin of Salina, Inc. Jan. 17, 1996 Community Broadcasters Association Jan. 16, 1996 Computer & Communications Industry Association Jan. 22, 1996 Digital HDTV Grand Alliance Jan. 22, 1996 Donnell, Stephen Jan. 22, 1996 East Side Community Access Jan. 22, 1996 Electronic Industries Association and the Advanced TV Committee Jan. 22, 1996 Fireweed Communications Corporation Jan. 16, 1996 General Instrument Corporation Jan. 22, 1996 Hartford Public Access Television, Inc. Jan. 22, 1996 Home Box Office (HBO) Jan. 16, 1996 Internatinal Broadcasting Network's Jan. 16, 1996 Larcan-TTC, Inc. Jan. 17, 1996 Malrite Communications Group, Inc. Jan. 24, 1996 Mattis, William E., Jr. Jan. 17, 1996 Media Access Project, et. al. Jan. 22, 1996 ;'\iational Cable Television Association, Inc. Jan. 22, 1996 ~ational Translator Association Jan. 16, 1996 Nielsen, A.c. -

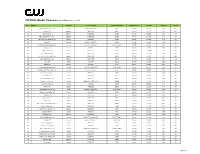

Cwplus Station List 090119.Xlsx

CW PLUS Market Clearance (as of September 1, 2019) Rank Market Time Zone On Air Call Letters Nielsen Call Letters CWPlus TV HH's TV HH's CWPlus % HD/SD 78 Harlingen-Wslco-Brnsvl, TX Central KCWT / KNVO-DT4 KCWT 249,656 351,810 71% HD 93 Savannah, GA Eastern WSAV-DT2 ESAV 328,860 328,860 100% HD 94 Charleston, SC Eastern WCBD-DT2 ECBD 257,322 320,980 80% HD 95 Myrtle Beach-Florence, SC Eastern WWMB-DT2 EWMB 184,596 281,550 66% HD 96 Burlington, VT-Plattsburgh, NY Eastern WPTZ-DT2 EPTZ 198,676 294,020 68% HD 100 Boise, ID Mountain KYUU-LP / KBOI-DT2 KYUU 264,300 264,300 100% HD 101 Fort Smith-Fay-Springdale, AR Central KHBS-DT2 / KHOG-DT2 NHBS / NHOG 281,757 292,160 96% HD 104 Fort Wayne, IN Eastern WISE-DT WISE 249,130 249,130 100% HD 105 Augusta-Aiken, GA Eastern WAGT-DT2 EAGT 192,379 249,090 77% HD 106 Johnstown-Altoona, PA Eastern WJAC-DT4 HJAC 262,840 262,840 100% HD 107 Greenville-New Bern-Wash, NC Eastern WNCT-DT2 ENCT 311,465 285,650 109% HD 108 Springfield-Holyoke, MA Eastern WWLP-DT2 EWLP 237,580 237,580 100% HD 109 Reno, NV Pacific KOLO-DT3 OOLO 263,990 263,990 100% HD 110 Lansing, MI Eastern WLAJ-DT2 ELAJ 230,333 238,990 96% HD 111 Lincoln-Hastings-Kearney, NE Central KCWH-LD / KNHL-DT3 KCWH / ONHL 210,488 263,110 80% SD 112 Tallahassee, FL-Thomasville, GA Eastern WTLF/ WTLH-DT2 WTLF 257,570 257,570 100% HD 113 Peoria-Bloomington, IL Central WEEK-DT3 GHOI 222,210 222,210 100% HD 114 Tyler-Longview, TX Central KYTX-DT2 MYTX 151,749 253,230 60% HD 115 Sioux Falls(Mitchell), SD Central KSFY-DT2 NSFY 252,660 252,660 100% HD 116 Montgomery-Selma, -

EEO Public Inspection File Report South Carolina Educational Television Commission 1101 George Rogers Blvd., Columbia, SC 29201

EEO Public Inspection File Report South Carolina Educational Television Commission 1101 George Rogers Blvd., Columbia, SC 29201 Stations WRLK and WLTR (FM) RECRUITMENT SUMMARY FOR THOSE INTERVIEWED FOR POSITIONS FILLED August 01, 2012 Through July 31, 2013 Agency Title: ETV Agency CodeH67 Columbia Television and Radio (WRLK and WLTR) Position Number Date Posted Date Hired Recruitment Sources Total Title Source for Hire Interviewed Upstate Underwriting Sales 5/4/2012 8/2/2012 SCSWS (3) Other (3) Hire 6 Representative (Other) Education Multimedia Producer 10/25/2012 11/19/2012 SCSWS (36) Internal (4) Other 6 (9) ETVWS (2) DEW (5) Coll (1) Media (1) Hire (Internal) National Radio Production 10/23/2012 12/3/2012 SCSWS (7) Internal (2) Other 15 Assistant (6) Hire (Other) Web/Member Services 11/12/2012 1/02/2013 SCSWS (2) Other (1) ETVWS 5 Coordinator (1) DEW (1) Hire (ETVWS) FTS Technician III 2/26/2013 4/17/2013 SCSWS (1) Internal (1) Other 5 (2) DEW (1) Hire (Other) Broadcast/Engineering 2/12/2013 5/2/2013 SCSWS (2) Internal (3) Other 12 Maintenance Technician III (6) ETVWS (1) Hire (Other) Note: Counts of persons interviewed includes the person hired. ^ See attached list of Recruitment Source abbreviations and additional information * The attached Referral Source mailing list is also notified of all job openings. Long Term Recruitment Initiatives for the Period August 1, 2012 to July 31, 2013 Please note that this report includes descriptions of the long-term initiatives completed for the period ending July 31, 2013, in order to demonstrate compliance with the initiative requirements of the FCC’s rules. -

All Full-Power Television Stations by Dma, Indicating Those Terminating Analog Service Before Or on February 17, 2009

ALL FULL-POWER TELEVISION STATIONS BY DMA, INDICATING THOSE TERMINATING ANALOG SERVICE BEFORE OR ON FEBRUARY 17, 2009. (As of 2/20/09) NITE HARD NITE LITE SHIP PRE ON DMA CITY ST NETWORK CALLSIGN LITE PLUS WVR 2/17 2/17 LICENSEE ABILENE-SWEETWATER ABILENE TX NBC KRBC-TV MISSION BROADCASTING, INC. ABILENE-SWEETWATER ABILENE TX CBS KTAB-TV NEXSTAR BROADCASTING, INC. ABILENE-SWEETWATER ABILENE TX FOX KXVA X SAGE BROADCASTING CORPORATION ABILENE-SWEETWATER SNYDER TX N/A KPCB X PRIME TIME CHRISTIAN BROADCASTING, INC ABILENE-SWEETWATER SWEETWATER TX ABC/CW (DIGITALKTXS-TV ONLY) BLUESTONE LICENSE HOLDINGS INC. ALBANY ALBANY GA NBC WALB WALB LICENSE SUBSIDIARY, LLC ALBANY ALBANY GA FOX WFXL BARRINGTON ALBANY LICENSE LLC ALBANY CORDELE GA IND WSST-TV SUNBELT-SOUTH TELECOMMUNICATIONS LTD ALBANY DAWSON GA PBS WACS-TV X GEORGIA PUBLIC TELECOMMUNICATIONS COMMISSION ALBANY PELHAM GA PBS WABW-TV X GEORGIA PUBLIC TELECOMMUNICATIONS COMMISSION ALBANY VALDOSTA GA CBS WSWG X GRAY TELEVISION LICENSEE, LLC ALBANY-SCHENECTADY-TROY ADAMS MA ABC WCDC-TV YOUNG BROADCASTING OF ALBANY, INC. ALBANY-SCHENECTADY-TROY ALBANY NY NBC WNYT WNYT-TV, LLC ALBANY-SCHENECTADY-TROY ALBANY NY ABC WTEN YOUNG BROADCASTING OF ALBANY, INC. ALBANY-SCHENECTADY-TROY ALBANY NY FOX WXXA-TV NEWPORT TELEVISION LICENSE LLC ALBANY-SCHENECTADY-TROY AMSTERDAM NY N/A WYPX PAXSON ALBANY LICENSE, INC. ALBANY-SCHENECTADY-TROY PITTSFIELD MA MYTV WNYA VENTURE TECHNOLOGIES GROUP, LLC ALBANY-SCHENECTADY-TROY SCHENECTADY NY CW WCWN FREEDOM BROADCASTING OF NEW YORK LICENSEE, L.L.C. ALBANY-SCHENECTADY-TROY SCHENECTADY NY PBS WMHT WMHT EDUCATIONAL TELECOMMUNICATIONS ALBANY-SCHENECTADY-TROY SCHENECTADY NY CBS WRGB FREEDOM BROADCASTING OF NEW YORK LICENSEE, L.L.C. -

Federal Register/Vol. 86, No. 91/Thursday, May 13, 2021/Proposed Rules

26262 Federal Register / Vol. 86, No. 91 / Thursday, May 13, 2021 / Proposed Rules FEDERAL COMMUNICATIONS BCPI, Inc., 45 L Street NE, Washington, shown or given to Commission staff COMMISSION DC 20554. Customers may contact BCPI, during ex parte meetings are deemed to Inc. via their website, http:// be written ex parte presentations and 47 CFR Part 1 www.bcpi.com, or call 1–800–378–3160. must be filed consistent with section [MD Docket Nos. 20–105; MD Docket Nos. This document is available in 1.1206(b) of the Commission’s rules. In 21–190; FCC 21–49; FRS 26021] alternative formats (computer diskette, proceedings governed by section 1.49(f) large print, audio record, and braille). of the Commission’s rules or for which Assessment and Collection of Persons with disabilities who need the Commission has made available a Regulatory Fees for Fiscal Year 2021 documents in these formats may contact method of electronic filing, written ex the FCC by email: [email protected] or parte presentations and memoranda AGENCY: Federal Communications phone: 202–418–0530 or TTY: 202–418– summarizing oral ex parte Commission. 0432. Effective March 19, 2020, and presentations, and all attachments ACTION: Notice of proposed rulemaking. until further notice, the Commission no thereto, must be filed through the longer accepts any hand or messenger electronic comment filing system SUMMARY: In this document, the Federal delivered filings. This is a temporary available for that proceeding, and must Communications Commission measure taken to help protect the health be filed in their native format (e.g., .doc, (Commission) seeks comment on and safety of individuals, and to .xml, .ppt, searchable .pdf). -

List of Directv Channels (United States)

List of DirecTV channels (United States) Below is a numerical representation of the current DirecTV national channel lineup in the United States. Some channels have both east and west feeds, airing the same programming with a three-hour delay on the latter feed, creating a backup for those who missed their shows. The three-hour delay also represents the time zone difference between Eastern (UTC -5/-4) and Pacific (UTC -8/-7). All channels are the East Coast feed if not specified. High definition Most high-definition (HDTV) and foreign-language channels may require a certain satellite dish or set-top box. Additionally, the same channel number is listed for both the standard-definition (SD) channel and the high-definition (HD) channel, such as 202 for both CNN and CNN HD. DirecTV HD receivers can tune to each channel separately. This is required since programming may be different on the SD and HD versions of the channels; while at times the programming may be simulcast with the same programming on both SD and HD channels. Part time regional sports networks and out of market sports packages will be listed as ###-1. Older MPEG-2 HD receivers will no longer receive the HD programming. Special channels In addition to the channels listed below, DirecTV occasionally uses temporary channels for various purposes, such as emergency updates (e.g. Hurricane Gustav and Hurricane Ike information in September 2008, and Hurricane Irene in August 2011), and news of legislation that could affect subscribers. The News Mix channels (102 and 352) have special versions during special events such as the 2008 United States Presidential Election night coverage and during the Inauguration of Barack Obama. -

Press Release Distribution Report

Press Release Distribution Report This distribution report contains links to where we can track your release. It shows the media target lists through our World Media Directory, quick links to show you your release on search engines and social media, full-page reprints from locations we can track, and the specific Wir es you r rele ases are feed ing out to. I f yo u hav e mo re que stions, plea se do n ot hes itate to c all us. We wis h you a very p rodu ctive and h appy day. Download PDF Report View tracking links in RSS View tracking links in CSV 5 SATURDAYS EDUCATION NON-PROFIT APPOINTS LEADERSHIP COUNCIL MEMBER Approved on February 26, 2018 03:43 GMT. The press release has been online for 1051 days and 14 hours now. View Release (Print Friendly, PDF) Title: 8 words, 67 characters Other Links: 1 link 5 SATURDAYS EDUCATION NON-PROFIT APPOINTS https://5saturdays.org LEADERSHIP COUNCIL MEMBER https://5saturdays.org https://5saturdays.org/leadership-council-new/ Text: 292 words, 2033 characters Group Provides Leaning Experiences in Agile & Scrum Embedded Images: 1 image Principles to High School Students COSTA MESA, CALIFORNIA, UNITED STATES, February 25, 2018 / EINPresswire.com / -- FOR Name: 5 Saturdays Logo IMMEDIATE RELEASE…Feb. 27, 2018…COSTA MESA, CALIF….5 Caption: 5 Saturdays Agile Life Skills Saturdays, an innovative … Alt Text: Empowering students with agility and innovation - Find your awesomeness Keyword Anchor Text Links: 3 links Full-size Image project-based education - https://5saturdays.org agile life skills - https://5saturdays.org Embedded Videos: 0 videos leadership - https://5saturdays.org/leadership-council- new/ California United States Google News Newswire Newswire Facebook Twitter Google Yahoo Bing Ask Education News Today Nanotechnology News Today Social Media News Today Technology Today KQCW Tulsa WAVE 3 Tulsa (OK) WTOL 11 WSFA 12 News Toledo (OH) Montgomery (AL) Kuam.com KNBN Guam (GU) Rapid City (SD) Fox 21 Delmarva 93.7 The Eagle Salisbury (MD) Lubbock (TX) WNKY 40 KFVS Bowling Green (KY) Paducah (MO) KMOV 4 KTVK 3 AZFamily St. -

Raycom Media Inc

RAYCOM MEDIA INC 175 198 194 195 170 197 128 201 180 DR. OZ 3RD QUEEN QUEEN SEINFELD 4TH SEINFELD 5TH TIL DEATH 1ST DR. OZ CYCLE LATIFAH LATIFAH CYCLE CYCLE KING 2nd Cycle KING 3rd Cycle CYCLE RANK MARKET %US STATION 2011-2014 2014-2015 2013-2014 2014-2015 4th Cycle 5th Cycle 2nd Cycle 3rd Cycle 2013-2014 19 CLEVELAND OH 1.28% WOIO/WUAB WEWS WJW WOIO/WUAB WKYC WJW WJW WOIO/WUAB WBNX WBNX 25 CHARLOTTE NC 1.00% WBTV WAXN/WSOC WJZY/WMYT WBTV WAXN/WSOC WJZY/WMYT WJZY/WMYT WJZY/WMYT 35 CINCINNATI OH 0.78% WXIX WLWT WLWT WLWT WKRC/WSTR EKRC/WKRC EKRC/WKRC/WSTR WXIX WXIX WXIX 38 WEST PALM BEACH-FT PIERCE FL 0.70% WFLX WPBF WPBF WPTV WPTV WFLX WFLX WTCN/WTVX WFLX 44 BIRMINGHAM (ANNISTON-TUSCALOOSA) AL 0.62% WBRC WBMA WBMA WBRC WBRC WABM/WTTO WABM/WTTO WABM/WTTO WVUA 49 LOUISVILLE KY 0.58% WAVE/WAVE-DT2 WAVE/WAVE-DT2 WBKI/WDRB/WMYO WAVE WAVE WBKI/WDRB/WMYO WBKI/WDRB/WMYO WBKI WBKI/WDRB/WMYO WBKI 50 MEMPHIS TN 0.58% WMC WMC WMC WMC WATN/WLMT WBII 51 NEW ORLEANS LA 0.56% WVUE WWL WUPL/WWL WDSU WUPL/WWL WVUE WGNO/WNOL WUPL/WWL WUPL/WWL 57 RICHMOND-PETERSBURG VA 0.48% WUPV/WWBT WTVR WRIC WUPV/WWBT WUPV/WWBT WRIC WRIC WUPV 61 KNOXVILLE TN 0.45% WTNZ EVLT/WVLT EVLT/WVLT WATE EVLT EVLT/WVLT WBXX/WKNX WBXX WBXX/WKNX WBXX 69 HONOLULU HI 0.39% KFVE/KGMB/KHNL KITV KITV KFVE KFVE KHON/KHON-DT2 KFVE KFVE/KHNL KFVE KHON/KHON-DT2 71 TUCSON (SIERRA VISTA) AZ 0.38% KOLD/KOLD-DT2 KOLD/KOLD-DT2 KVOA/KVOA-DT2 KMSB/KTTU KMSB/KTTU KMSB/KTTU KMSB/KTTU KMSB/KTTU KMSB/KTTU KMSB/KTTU 76 TOLEDO OH 0.36% WTOL/WUPW WNWO WTVG-DT2 WTVG/WTVG-DT2 WMNT WMNT WMNT WMNT WMNT 77 COLUMBIA