Rob Stafsholt [email protected]

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Eau Claire County Democratic Party Coffee Klatch Notes Thursday

Eau Claire County Democratic Party Coffee Klatch Notes Thursday, August 27, 2020 Present: Carol Craig, Jan & Lou Frase, Ann Heywood, Linda Ladolce, Dennis Myhre, Mike O’Brien, Linda Norton, Connie Russell, Jeff Smith, Tate Williams UPCOMING EVENTS Coffee Klatch – Thursday, September 3, 10 a.m. – Noon via Zoom Let Carol Craig know if you have suggestions for guest speakers who would be knowledgeable resources for providing information about current issues. Video conferencing eliminates travel time, making it easier to have guests from beyond the local area. Campaign Nonviolence Action Week – September 19 – 27 to celebrate the International Day of Peace, Sept. 21. Look for updates in the E-News of events happening that week. Absentee Voting – September 1: The Wisconsin Elections Commission will be mailing information about voting in November to approximately 2.6 million registered Wisconsin voters who have not already requested an absentee ballot. The information packet will include an absentee request form and a postage-paid reply envelope September 17: Deadline for Clerks to mail absentee ballots for November 3 (47 days before) to registered voters with requests on file WPEN - The Wisconsin Public Education Network’s Online Workshop Series: See Link for details of the #VotePublicAction workshops on these dates, all on Thursdays from 3 – 5 p.m. Sept. 3 – Messaging & Media Nov. 19 – After the Election: Legislative Advocacy Sept. 17 – Back to School: Get the Facts Basics Oct. 15 – GOTV Strategies Dec. 17 – Local Level Action: Statewide Impact RECOMMENDED READING Book: It Was All a Lie: How the Republican Party Became Donald Trump (August, 2020) by Stuart Stevens. -

Quarterly News

AGGREGATE QUARTERLY PRODUCERS NEWS of WISCONSIN June 2020 Producers of Crushed Stone, Sand and Gravel Message from the President Message from the President 1 From the Executive Director 2 Legislative & Regulatory Report The New Normal for the Old School November 2020 Elections Will Bring Many Faces to By the time you read this, it will be well over three months since the coronavirus Wisconsin Legislature 3 pandemic took over our country. Literally…it took over our country! Every facet of National Industry News our daily lives was suddenly turned upside down. House Introduces Text of I hope you and your families have persevered during the pandemic and the INVEST in America Act 5 endless onslaught of media coverage, CDC guideline changes, testing protocols, NSSGA Commends House and PPE shortages. While our industry was considered essential, we should really Transportation & Infrastructure Committee Introduction of “tip our hard hats” to the front line medical professionals, doctors, nurses, EMTs, Infrastructure Bill That Includes police, and firefighters who have taken on this nasty virus and served our local ROCKS Act 7 communities with the same care and compassion as they always have. Thank you Member News 19–23 to all of these professionals. APW Regulatory News 20 So, over these last few months, what have we learned about our families, WI DNR Issues Changes to businesses, employees, and ourselves as we face these uncertain times? NR 812 21 Regarding family, the first few weeks of Safer at Home might have felt like a 5th Annual APW Shooting vacation. Time for family dinners, board games, and reruns on the television that Event 24 kind of took us back to family days of the past. -

Legislative Senate Committees

2021-22 LEGISLATURE: COMMITTEES AND COMMITTEE CHAIRPERSONS Senate Committees Committee Name Chair Vice-Chair Senate Committee on Administrative Rules Sen. Stephen Nass Senate Committee on Agriculture and Tourism Sen. Joan Ballweg Sen. Howard Marklein Senate Committee on Economic and Workforce Sen. Dan Feyen Sen. Patrick Testin Development Senate Committee on Education Sen. Alberta Darling Sen. Kathleen Bernier Senate Committee on Elections, Election Process Sen. Kathleen Bernier Sen. Alberta Darling Reform and Ethics Senate Committee on Finance Sen. Marklein Senate Committee on Financial Institutions and Sen. Dale Kooyenga Sen. Dan Feyen Revenue Senate Committee on Government Operations, Legal Sen. Duey Stroebel Sen. Mary Felzkowski Review and Consumer Protection Senate Committee on Health Sen. Patrick Testin Sen. Dale Kooyenga Senate Committee on Housing, Commerce and Trade Sen. Dan Feyen Sen. Roger Roth Senate Committee on Human Services, Children and Sen. Andre Jacque Sen. Joan Ballweg Families Senate Committee on Insurance, Licensing and Sen. Mary Felzkowski Sen. Rob Stafsholt Forestry Senate Committee on Judiciary and Public Safety Sen. Van Wanggaard Sen. Eric Wimberger Senate Committee on Labor and Regulatory Reform Sen. Stephen Nass Sen. Van Wanggaard Senate Committee on Natural Resources and Energy Sen. Robert Cowles Sen. Mary Felzkowski Senate Committee on Senate Organization Sen. Devin LeMahieu Sen. Chris Kapenga Senate Committee on Sporting Heritage, Small Sen. Rob Stafsholt Sen. Jerry Petrowski Business and Rural Issues Senate Committee on Transportation and Local Sen. Jerry Petrowski Sen. Robert Cowles Government Senate Committee on Universities and Technical Sen. Roger Roth Sen. Stephen Nass Colleges Senate Committee on Utilities, Technology and Sen. Julian Bradley Sen. Roger Roth Telecommunications Senate Committee on Veterans and Military Affairs Sen. -

2017-2018 Legislative Directory

2017-2018 LEGISLATIVE DIRECTORY 2017-2018 LEGISLATIVE DIRECTORY PO Box 14440 • Madison WI 53708-0440 Ph: 608-256-3228 (Madison) • toll-free: 888-378-7395 Web: www.wifamilycouncil.org Email: [email protected] For Additional copies Email: [email protected] or Call toll free: (888) 378-7395 To access directory online, go to www.wifamilycouncil.org. Under "Take Action!" select "Contact Officials." The link to the Legislative Directory is under "Two Resources for Identifying Elected Officials." © Wisconsin Family Council 2017. All rights reserved. Table of Contents My Elected Officials/Quick Reference Form ........................3 Wisconsin Congressional Delegation ..................................4-5 US Senate ..................................................................................4 US House of Representatives ..................................................4-5 US Capitol Contact Information ...........................................5 White House Contact Information ........................................6 State of Wisconsin ...................................................................6 Office of the Governor ..............................................................6 Wisconsin State Legislature ..............................................6-26 Wisconsin State Senate .........................................................6-12 Senate and Assembly by District Number...............................7-9 Wisconsin State Assembly ..................................... ............12-19 Joint Standing Committees -

5 Easy Steps to Find Your State Legislator 1

WBA ADVOCACY TOOLKIT 5 Easy Steps to Find Your State Legislator 1 . Go to https://legis .wisconsin .gov . 2 . Enter your address in the highlighted field . 3 . Click “Find Your Legislator .” Find contact information for 4 . your State Senator and State Representative . Send them an email or 5 . call their office line! 413 WBA ADVOCACY TOOLKIT Wisconsin Delegation - District Offices HOW TO ADDRESS A U.S. SENATOR The Honorable XXXXX United States Senate 709 Hart Senate Building Washington, DC 20510 Dear Senator XXXX: Senator Ron Johnson Senator Tammy Baldwin 328 Hart Senate Office Building 709 Hart Senate Office Building Washington, DC 20510 Washington, DC 20510 Phone: (202) 224-5323 Phone: (202) 224-5653 219 Washington Avenue Ste 100 30 West Mifflin Street Suite 700 Oshkosh, WI 54901 Madison, WI 53703 Phone: 920-230-7250 Phone: 608-264-5338 HOW TO ADDRESS A MEMBER OF THE U.S. HOUSE OF REPRESENTATIVES The Honorable XXXXX U .S . House of Representatives 2252 Rayburn House Office Building Washington, DC 20515 Dear Congressman(woman) XXXX Rep. Bryan Steil Rep. Mark Pocan Rep. Ron Kind Rep. Gwen Moore (R-District 1) (D-District 2) (D-District 3) (D-District 4) 20 South Main Street Suite 10 10 East Doty Street Suite 405 205 Fifth Avenue S., Suite 400 316 N Milwaukee St., Suite 406 Janesville, WI 53545 Madison, WI 53703 La Crosse, WI 54601 Milwaukee, WI 53202 Phone: 608-752-4050 Phone: 608-258-9800 Phone: 608-782-2558 Phone: 414-297-1140 Rep. Scott Fitzgerald Rep. Glenn Grothman Rep. Tom Tiffany Rep. Mike Gallagher (R-District 5) (R-District 6) (R-District 7) (R-District 8) 120 Bishops Way, Room 154 24 West Pioneer Road 2620 Stewart Avenue, Suite 312 1915 S. -

Type a Notice for This Election Shall Be Published by All County Clerks on April 10, 2018

NOTICE OF ELECTION PARTISAN PRIMARY - AUGUST 14, 2018 AND GENERAL ELECTION - NOVEMBER 6, 2018 STATE OF WISCONSIN ss. WISCONSIN ELECTIONS COMMISSION } NOTICE IS HEREBY GIVEN that in the several towns, villages, cities, wards, and election districts of the State of Wisconsin, at a primary to be held on Tuesday, August 14, 2018, and at an election to be held on Tuesday, November 6, 2018, the following officers are to be nominated and elected: CONSTITUTIONAL OFFICERS FIVE CONSTITUTIONAL OFFICERS, each for the term of four years, to succeed the present incumbents listed, whose terms of office will expire on January 7, 2019: Governor - Scott Walker Lieutenant Governor - Rebecca Kleefisch Attorney General - Brad Schimel Secretary of State - Doug La Follette State Treasurer - Matt Adamczyk CONGRESSIONAL OFFICERS ONE UNITED STATES SENATOR, for the term of 6 years, to succeed the present incumbent listed, whose terms of office will expire on January 3, 2019: Tammy Baldwin EIGHT REPRESENTATIVES IN CONGRESS, each for the term of two years, to succeed the present incumbents listed, whose terms of office will expire on January 3, 2019: 1st Congressional District - Paul Ryan 2nd Congressional District - Mark Pocan 3rd Congressional District - Ron Kind 4th Congressional District - Gwen S. Moore 5th Congressional District - F. James Sensenbrenner, Jr. 6th Congressional District - Glenn Grothman 7th Congressional District - Sean Duffy 8th Congressional District - Mike Gallagher 1 LEGISLATIVE OFFICERS SEVENTEEN STATE SENATORS, from the odd-numbered Senatorial Districts of the State, each for the term of four years, to succeed the present incumbents listed, whose terms of office will expire on January 7, 2019: Senate District 1 - Vacant Senate District 3 - Tim Carpenter Senate District 5 - Leah Vukmir Senate District 7 - Chris J. -

April 3, 2020 Governor Tony Evers PO Box 7863 Madison, WI 53707 Dear

April 3, 2020 Governor Tony Evers P.O. Box 7863 Madison, WI 53707 Dear Governor Evers: The CARES Act is a one-time federal windfall that must be spent wisely to help Wisconsin deal with the human and economic catastrophes caused by the coronavirus outbreak. As we learned late last week, Wisconsin will be awarded $2.2 billion, with $1.9 billion of that headed directly to the state. Because of the seriousness of this pandemic, we believe in the importance of setting aside partisan differences and working together. We hope you believe the same. Over the past two weeks, we have spoken to thousands of Wisconsinites. We have reached out to our local health care providers, business owners, farmers, and local governments to understand their most pressing concerns during this very trying time. As you know, you and your administration have the sole ability to allocate the federal stimulus money, so we would like to outline what we believe are the main priorities of Wisconsinites statewide. When it comes to healthcare, you have likely heard as we have, that nursing homes are struggling terribly to pay for the necessary personal protection equipment (PPE) that is needed to follow CDC guidelines. Our nursing home workers are on the frontlines of this pandemic. If they are not able to adequately keep residents safe, it will directly impact our hospitals. In addition, PPE is still a need for healthcare and other essential workers across the state. The state also must have more readily available and rapid testing supplies. We hope you will prioritize the needs of hospitals and healthcare facilities as you spend these federal resources. -

Elections and Political Parties

ELECTION RESULTS AND WISCONSIN PARTIES Political parties qualifying for ballot status as of April 2019 in the order they will be listed on the ballot Democratic Party of Wisconsin 15 N Pinckney Street, Suite 200, Madison, WI 53703; 608-255-5172; www .wisdems .org Executive political director . .Devin Remiker Executive party operations director . Breianna Hasenzahl-Reeder Communications director . .Courtney Beyer Party affairs director . .Will Hoffman Digital communications director . .Chuck Engel Data director . Ali Nikseresht Finance director . Tom McCann Membership manager . Gabriela Luna Candidate services director . .Hannah Mullen Compliance and operations managers . Dee Hanson, Joshua Rubin State Administrative Committee Party officers . .Martha Laning, Sheboygan, chair; David Bowen, Milwaukee, first vice chair; Mandela Barnes, Milwaukee, second vice chair; Meg Andrietsch, Racine, secretary; Randy Udell, Madison, treasurer National committee members . .Martha Love, Milwaukee; Andrew Werthmann, Eau Claire; Khary Penebaker, Hartland; Janet Bewley, Mason; Jason Rae, College Democrats representative . .Shea Senger, Milwaukee Young Democrats representative . .Sarah . Smith, Milwaukee Milwaukee County chair . Christopher Walton, Milwaukee At-large members . Dian Palmer, Brookfield; Gretchen Lowe, Madison; Michael Childers, La Pointe; Paul DeMain, Hayward; David Duran, Lodi; Yee L . Xiong, Weston; Mary Lang Sollinger, Madison; Penny Bernard Schaber, Appleton; Melissa Lemke, Racine; Luke Fuszard, Middleton; Sarah Lloyd, Wisconsin Dells; Ryan Greendeer, Black River Falls; Gail Hohenstein, Green Bay County Chairs Association chair . Peter Hellios, Granton Assembly representative . .JoCasta Zamarripa, Milwaukee Senate representative . Janis Ringhand, Evansville CD 1 representative . Mary Jonker, Kenosha, chair; Matt Lowe, Muskego CD 2 representative . Christine Welcher, Stoughton, chair; Mike Martez Johnson, Madison CD 3 representative . .Lisa Herrmann, Eau Claire, chair; George Wilbur, La Farge CD 4 representative . -

Wisconsin Municipal Guide 2018-19

WISCONSIN MUNICIPAL GUIDE 2018-19 Municipalities by County Selected State and Regional Contacts State Assembly State Senate U.S. Congress 2018-19 Wisconsin Municipal Guide MUNICIPALITIES BY COUNTY Table of Contents Wisconsin State Holidays 2018 2019 Municipalities by County .................................2 New Year’s Day New Year’s Day Selected State and Regional Contacts ..........37 Monday 1/1/2018 Tuesday 1/1/2019 State Assembly ..............................................40 Martin Luther King, Martin Luther King, Jr. Day Jr. Day Monday 1/15/2018 Monday 1/21/2019 State Senate ..................................................47 Memorial Day Memorial Day U.S. Congress ................................................49 Monday 5/28/2018 Monday 5/27/2019 Independence Day Independence Day Wednesday 7/4/2018 Thursday 7/4/2019 The information in this Labor Day Labor Day publication is supplied by: Monday 9/3/2018 Monday 9/2/2019 Content Providers, LLC P.O. Box 5425 Thanksgiving Day Thanksgiving Day Austin, TX 78763-5425 Thursday 11/22/2018 Thursday 11/28/2019 Please email changes, corrections or requests for additional copies to: Christmas Eve Day Christmas Eve Day [email protected] Monday 12/24/2018 Tuesday 11/24/2019 Please email all other inquiries to: [email protected] Christmas Day Christmas Day Tuesday 12/25/2018 Wednesday 12/25/2019 ©2018 Municipal Publishing, LLC. All rights reserved. Reproduction in whole or in part without written permission from the publisher is strictly prohibited. Municipal Publishing, LLC is a privately-owned business entity, that is not affiliated with any city, village, town, county or other governmental entity. The sponsors and information set forth in this publication do not necessarily reflect the views and opinions of any city, village, town, county or other governmental entity, its elected officials, administrators or staff. -

State Offices to Be Elected at 2018 Fall Election August 14, 2018 Partisan Primary November 6, 2018 General Election

STATE OFFICES TO BE ELECTED AT 2018 FALL ELECTION AUGUST 14, 2018 PARTISAN PRIMARY NOVEMBER 6, 2018 GENERAL ELECTION OFFICE INCUMBENT ID -No. Statewide Constitutional Officers Governor Scott Walker 102575 Lieutenant Governor Rebecca Kleefisch 104890 Attorney General Brad Schimel 104385 Secretary of State Doug La Follette 100216 State Treasurer Matt Adamczyk 104336 United States Senator Tammy Baldwin 200491 Representatives in Congress District 1 Paul Ryan 200500 District 2 Mark Pocan 200696 District 3 Ron Kind 200435 District 4 Gwen S. Moore 200564 District 5 F. James Sensenbrenner, Jr. 200049 District 6 Glenn Grothman 200731 District 7 Sean Duffy 200681 District 8 Mike Gallagher 200745 State Senators District 1 Vacant -- District 3 Tim Carpenter 100881 District 5 Leah Vukmir 104015 District 7 Chris J. Larson 104991 District 9 Devin LeMahieu 105206 District 11 Steve Nass 102660 District 13 Scott L. Fitzgerald 103112 District 15 Janis Ringhand 104291 District 17 Howard Marklein 104815 District 19 Roger Roth 104439 District 21 Van Wanggaard 104422 District 23 Terry Moulton 104124 District 25 Janet Bewley 104882 District 27 Jon B. Erpenbach 103549 District 29 Jerry Petrowski 103686 District 31 Kathleen Vinehout 104443 District 33 Chris Kapenga 104883 Representatives to the Assembly District 1 Joel Kitchens 105512 District 2 Andre Jacque 104808 District 3 Ron Tusler 105788 Offices to be Elected at the 2018 Fall Election Page 2 District 4 David Steffen 105539 District 5 Jim Steineke 104713 District 6 Gary Tauchen 104463 District 7 Daniel G. Riemer 105193 District 8 JoCasta Zamarripa 104989 District 9 Josh Zepnick 104034 District 10 David Bowen 105535 District 11 Jason M. -

2021 Senate & Assembly Committee Chairs

2021 Senate & Assembly Committee Chairs Senate Committees Agriculture & Tourism, Sen. Joan Ballweg Economic & Workforce Development, Sen. Dan Feyen Education, Sen. Alberta Darling Elections, Elections Process Reform & Ethics, Sen. Kathy Bernier Financial Institutions & Revenue, Sen. Dale Kooyenga Government Operations, Legal Review & Consumer Protection, Sen. Duey Stroebel Health, Sen. Pat Testin Human Services, Children & Families, Sen. André Jacque Insurance, Licensing & Forestry, Sen. Mary Felzkowski Judiciary & Public Safety, Sen. Van Wanggaard Labor & Regulatory Reform, Sen. Steve Nass Natural Resources & Energy, Sen. Rob Cowles Sporting Heritage, Small Business & Rural Issues, Sen. Rob Stafsholt Transportation & Local Government, Sen. Jerry Petrowski Universities & Technical Colleges, Sen. Roger Roth Utilities, Technology & Telecommunications, Sen. Julian Bradley Veteran and Military Affairs & Constitution and Federalism, Sen. Eric Wimberger Assembly Committees Aging and Long Term Care, Rep. Rick Gundrum Agriculture, Rep. Gary Tauchen Campaigns and Elections, Rep. Janel Brandtjen Children and Families, Rep. Pat Snyder Colleges and Universities, Rep. Dave Murphy Constitution and Ethics, Rep. Chuck Wichgers Consumer Protection, Rep. Barb Dittrich Corrections, Rep. Michael Schraa Criminal Justice and Public Safety, Rep. John Spiros Education, Rep. Jeremy Thiesfeldt Energy and Utilities, Rep. Mike Kuglitsch Environment, Rep. Joel Kitchens Family Law, Rep. Gae Magnafici Forestry, Parks and Outdoor Recreation, Rep. Jeff Mursau Financial Institutions, Rep. Cindi Duchow Government Accountability and Oversight, Rep. Dan Knodl Health, Rep. Joe Sanfelippo Housing and Real Estate, Rep. John Jagler Insurance, Rep. David Steffen Jobs and the Economy, Rep. Robert Wittke Judiciary, Rep. Ron Tusler Labor and Integrated Employment, Rep. James Edming Local Government, Rep. Todd Novak Mental Health, Rep. Paul Tittl Public Benefit Reform, Rep. Scott Krug Regulatory Licensing Reform, Rep. -

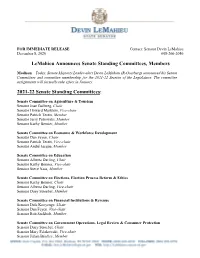

Released Committee Assignments

FOR IMMEDIATE RELEASE Contact: Senator Devin LeMahieu December 8, 2020 608-266-2056 LeMahieu Announces Senate Standing Committees, Members Madison – Today, Senate Majority Leader-elect Devin LeMahieu (R-Oostburg) announced his Senate Committees and committee membership for the 2021-22 Session of the Legislature. The committee assignments will formally take effect in January. 2021-22 Senate Standing Committees: Senate Committee on Agriculture & Tourism Senator Joan Ballweg, Chair Senator Howard Marklein, Vice-chair Senator Patrick Testin, Member Senator Jerry Petrowski, Member Senator Kathy Bernier, Member Senate Committee on Economic & Workforce Development Senator Dan Feyen, Chair Senator Patrick Testin, Vice-chair Senator André Jacque, Member Senate Committee on Education Senator Alberta Darling, Chair Senator Kathy Bernier, Vice-chair Senator Steve Nass, Member Senate Committee on Elections, Election Process Reform & Ethics Senator Kathy Bernier, Chair Senator Alberta Darling, Vice-chair Senator Duey Stroebel, Member Senate Committee on Financial Institutions & Revenue Senator Dale Kooyenga, Chair Senator Dan Feyen, Vice-chair Senator Rob Stafsholt, Member Senate Committee on Government Operations, Legal Review & Consumer Protection Senator Duey Stroebel, Chair Senator Mary Felzkowski, Vice-chair Senator Julian Bradley, Member Senate Committee on Health Senator Patrick Testin, Chair Senator Dale Kooyenga, Vice-chair Senator Julian Bradley, Member Senate Committee on Housing, Commerce & Trade Senator Dan Feyen, Chair Senator Roger Roth,