Debt Restructuring of Deccan Chronicle

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Newspaper Wise.Xlsx

PRINT MEDIA COMMITMENT REPORT FOR DISPLAY ADVT. DURING 2013-2014 CODE NEWSPAPER NAME LANGUAGE PERIODICITY COMMITMENT(%)COMMITMENTCITY STATE 310672 ARTHIK LIPI BENGALI DAILY(M) 209143 0.005310639 PORT BLAIR ANDAMAN AND NICOBAR 100771 THE ANDAMAN EXPRESS ENGLISH DAILY(M) 775695 0.019696744 PORT BLAIR ANDAMAN AND NICOBAR 101067 THE ECHO OF INDIA ENGLISH DAILY(M) 1618569 0.041099322 PORT BLAIR ANDAMAN AND NICOBAR 100820 DECCAN CHRONICLE ENGLISH DAILY(M) 482558 0.012253297 ANANTHAPUR ANDHRA PRADESH 410198 ANDHRA BHOOMI TELUGU DAILY(M) 534260 0.013566134 ANANTHAPUR ANDHRA PRADESH 410202 ANDHRA JYOTHI TELUGU DAILY(M) 776771 0.019724066 ANANTHAPUR ANDHRA PRADESH 410345 ANDHRA PRABHA TELUGU DAILY(M) 201424 0.005114635 ANANTHAPUR ANDHRA PRADESH 410522 RAYALASEEMA SAMAYAM TELUGU DAILY(M) 6550 0.00016632 ANANTHAPUR ANDHRA PRADESH 410370 SAKSHI TELUGU DAILY(M) 1417145 0.035984687 ANANTHAPUR ANDHRA PRADESH 410171 TEL.J.D.PATRIKA VAARTHA TELUGU DAILY(M) 546688 0.01388171 ANANTHAPUR ANDHRA PRADESH 410400 TELUGU WAARAM TELUGU DAILY(M) 154046 0.003911595 ANANTHAPUR ANDHRA PRADESH 410495 VINIYOGA DHARSINI TELUGU MONTHLY 18771 0.00047664 ANANTHAPUR ANDHRA PRADESH 410398 ANDHRA DAIRY TELUGU DAILY(E) 69244 0.00175827 ELURU ANDHRA PRADESH 410449 NETAJI TELUGU DAILY(E) 153965 0.003909538 ELURU ANDHRA PRADESH 410012 ELURU TIMES TELUGU DAILY(M) 65899 0.001673333 ELURU ANDHRA PRADESH 410117 GOPI KRISHNA TELUGU DAILY(M) 172484 0.00437978 ELURU ANDHRA PRADESH 410009 RATNA GARBHA TELUGU DAILY(M) 67128 0.00170454 ELURU ANDHRA PRADESH 410114 STATE TIMES TELUGU DAILY(M) -

Job and Salary Satisfaction of Journalists in Telugu Press: a Survey Analysis in Andhra Pradesh

International Journal of Research in Social Sciences Vol. 8 Issue 10, October 2018, ISSN: 2249-2496 Impact Factor: 7.081 Journal Homepage: http://www.ijmra.us, Email: [email protected] Double-Blind Peer Reviewed Refereed Open Access International Journal - Included in the International Serial Directories Indexed & Listed at: Ulrich's Periodicals Directory ©, U.S.A., Open J-Gage as well as in Cabell‟s Directories of Publishing Opportunities, U.S.A Job and Salary Satisfaction of Journalists in Telugu Press: A Survey Analysis in Andhra Pradesh Dr. J.Madhu Babu* J.Manjunath** ABSTRACT This study explores how to job and salary satisfaction of Journalists inTelugu Press inAndhra Pradesh.For this study, a survey was conducted on 100 journalists working at 9 general daily Newspapers in Krishna District (Rural) of Andhra Pradesh, India. The research results showed that, demographic profile of journalists,Qualification in Journalism, working position in the present organization, Job and salary satisfaction.Majority of journalists feel unsatisfied with their salaries, and they have no appointment orders. They were said their work was temporarily basis. Finally concluded that the attitude of managements did not interest to pay salaries to Journalists. Key words: Telugu Press, Journalists, Satisfaction, salary, Job. Introduction At the beginning of the journalistic career the rather tough and adverse conditions i.e. low payments, unpaid extra working hours, acting as assistant to the Chief Reporter or Staff reporter by serving personal works, and not working as a real reporter. It‟s may give rise to professional dissatisfaction and lead journalists to change their jobs and sometimes, even their careers‟. -

Deccan Chronicle Holdings Limited Andhra Bhoomi Daily (Telugu) All A

Deccan Chronicle Holdings Limited Andhra Bhoomi Daily (Telugu) All A. P. Editions 1,945.00 2,365.00 3,480.00 2,290.00 4,220.00 36, S.D. Road, Secunderabad - 500 003. Ph: 27803930 Fax: 27805207 Individual editions 700.00 1,400.00 1,890.00 1,720.00 2,290.00 Deccan Chronicle Financial Chronicle Printed from Hyderabad, Chennai, Bangalore, Coimbatore, Kochi, Printed from Mumbai, Delhi, Chennai GUARANTEED PAGE & POSITION PREMIUM Trivandrum, Kozikhode, Vijayawada, Visakhapatnam, Rajahmundry, Bangalore & Hyderabad PAGE 3 30% EXTRA ON RESPECTIVE RATES Ananthapur, Karimnagar & Nellore PAGE 5 25% EXTRA ON RESPECTIVE RATES The Asian Age Andhra Bhoomi PAGE 3 TOP OF COLUMN 30% + 25% EXTRA ON RESPECTIVE RATES Printed from New Delhi, Mumbai, Kolkata & London Printed from Hyderabad,Vijayawada,Visakhapatnam, ANY SPECIFIED PAGE 25% EXTRA ON RESPECTIVE RATES Rajahmundry, Ananthapur, Karimnagar & Nellore ANY SPECIFIED PAGE & POSITION 40% EXTRA ON RESPECTIVE RATES (OTHERTHAN PAGE 3 & 5) Revised Advertisement Rates Effective from 4th August , 2014 (Rates per sq cms) GUARANTEED SOLUS ON FRONT PAGE 25% EXTRA ON 16CM X 25 CM Inside Inside Front Back Navigator (MIN. 16CM X 25 CM) B&W Colour Page (Clr) Page (Clr) CANCELLATION / POSTPONEMENT CHARGES Display / Tender / Political / Financial / Notice Rs. Rs. Rs. Rs. Rs. DECCAN CHRONICLE Time of cancellation / Postponement Premium Non Premium DC Group- DC+FC+AB+TAA- All Editions 9,940.00 12,420.00 24,840.00 16,490.00 29,800.00 position position DC + TAA All editions 7,450.00 9,360.00 18,720.00 13,670.00 25,670.00 72 hours in advance of printing time 20% - DC+AB All Editions 7,700.00 9,275.00 18,550.00 12,250.00 22,600.00 48 hours in advance of printing time 35% 10% DC + FC- Bangalore+Chennai+ Hyderabad 5,300.00 6,625.00 13,250.00 9,360.00 10,760.00 24 hours in advance of printing time 50% 20% DC All Editions 5,880.00 7,285.00 14,570.00 10,240.00 18,870.00 DC Blr + Chn+ Hyd. -

Dossier Final

IMA Dilli Chalo Dossier (June 06, 2017) PRINT CLIPS Delhi PRINT CLIP Publication: Hindustan Page No.: 05 Date: June 07, 2017 PRINT CLIP Publication: Dainik Jagran Page No.: 04 Date: June 07, 2017 PRINT CLIP Publication: Dainik Bhaskar Page No.: 02 Date: June 07, 2017 PRINT CLIP Publication: Rastriya Sahara Page No.: 02 Date: June 07, 2017 PRINT CLIP Publication: Amar Ujala Page No.: 04 Date: June 07, 2017 PRINT CLIP Publication: Punjab Kesari Page No.: 08 Date: June 07, 2017 PRINT CLIP Publication: Navodaya Times Page No.: 09 Date: June 07, 2017 PRINT CLIP Publication: Nai Duniya Page No.: 02 Date: June 07, 2017 PRINT CLIP Publication: Hari Bhoomi Page No.: 03 Date: June 07, 2017 PRINT CLIP Publication: Deshbandhu Page No.: 03 Date: June 07, 2017 PRINT CLIP Publication: Virat Vaibhav Page No.: 03 Date: June 07, 2017 PRINT CLIP Publication: Akbhar e Mashriq Page No.: 02 Date: June 07, 2017 PRINT CLIP Publication: Hindustan Express Page No.: 08 Date: June 07, 2017 PRINT CLIP Publication: Shah Times Page No.: 05 Date: June 07, 2017 Agra PRINT CLIP Publication: Dainik Jagran Page No.: 03 Date: June 07, 2017 PRINT CLIP Publication: Hindustan Page No.: 01 Date: June 07, 2017 PRINT CLIP Publication: Amar Ujala Page No.: 04 Date: June 07, 2017 PRINT CLIP Publication: I-Next Page No.: 02 Date: June 07, 2017 PRINT CLIP Publication: Data Sandesh Page No.: 08 Date: June 07, 2017 PRINT CLIP Publication: Pushp Savera Page No.: 08 Date: June 07, 2017 PRINT CLIP Publication: Swaraj Times Page No.: 08 Date: June 07, 2017 PRINT CLIP Publication: The Sea -

Casebook Issue 30: Insolvency Tale of Deccan Chronicle Holdings Limited

Casebook Issue 30: Insolvency Tale of Deccan Chronicle Holdings Limited Index 1. About Deccan Chronicle Holdings Limited……………………………2 2. Major Financial Creditors/Bankers………………………………………2 3. CIRP of Deccan Chronicle Holdings Limited………………………… 3-8 . Financial Creditors files an application in National Company Law Tribunal (“NCLT”) . Appointment of IRP . Canara Bank files an appeal in National Company Law Tribunal (“NCLAT”) . IRP files application in NCLT for extension of the CIRP period . Appointment of Resolution Professional (“RP”) . Mr. Vinayak Ravi Reddy files application in NCLT for directions . IHFL files application in NCLT for directions . IDBI Bank files application challenging the approval of Resolution Plan by COC . RP files application in NCLT for approval of Resolution Plan 4. Concluding Notes…………………………………………………………..……8 5. Timeline of CIRP…………………………………………………………………9 6. Bibliography………………………………………………………………………10 Page 1 of 10 About Deccan Chronicle Holdings Limited (“DCHL”)1 Deccan Chronicle Holdings Limited (DCHL) publishes the largest circulated English newspaper in South India -- Deccan Chronicle, bringing every day the most comprehensive bouquet of news and analysis. Its remarkable skill of journalism over 75 years has won the Deccan Chronicle a mature and dedicated readership from all over the world and it is growing. The Deccan Chronicle has a circulation of over 1.45 million copies each day across Andhra Pradesh, Telangana, Tamil Nadu, Karnataka and Kerala. There are eight editions in Andhra Pradesh and Telangana - Hyderabad, Vijayawada, Rajahmundry, Vishakapatnam, Anantapur, Karimnagar, Nellore and Coimbatore. The paper also has a robust presence in Chennai, Bengaluru, and Kochi. DCHL also publishes The Asian Age, an English daily with editions in Mumbai, Delhi, Kolkata, and London. -

Irs 2019 Q3 Analysis

2019 Q3 (Compilation of 3 Quarters of previous rounds and 1 new quarter study) 2019 Q3 MRUC has released the readership data 2019 Q3. MRUC has decided to release the readership data every Quarter from 2019 onwards. This is called the rolling sample method. Rolling sample is a compilation of the findings of the 4 Quarters study, which includes the fresh Quarter and the preceding 3 Quarters of the earlier study. The findings are averaged and released. Sample size: 3,29,900 households all India The rolling sample details for this quarter are: Quarter Startdate of End date of study study 2017 Q4 August 2017 December 2017 2019 Q1 November 2018 April 2019 2019 Q2 April 2019 July 2019 2019 Q3 August 2019 November 2019 2 2019 Q3 All India trends Media consumption in the last 1 month in India in % Internet access on the rise across India Newspaper readership fell marginally TV viewership fell in Urban India Radio listenership and cinema going remained unchanged ALL INDIA URBAN INDIA RURAL INDIA 2019 Q3 2019 Q2 2019 Q1 2019 Q3 2019 Q2 2019 Q1 2019 Q3 2019 Q2 2019 Q1 1095874 1087143 1078543 384436 380677 376976 711438 706466 701567 Totals READ 38 39 39 51 53 53 30 31 32 NEWSPAPERS READ 5 5 6 9 9 9 3 4 4 MAGAZINES 76 76 77 88 89 90 70 70 70 WATCHED TV LISTENED TO 20 20 20 29 29 29 16 16 16 RADIO ACCCESSED 35 29 24 49 44 39 27 22 16 INTERNET WATCHED 3 3 3 6 6 6 1 1 2 CINEMA OWNED MOBILE 57 56 55 67 67 66 51 50 49 PHONE Q3 2019 consists of Q4 2017 and Q1, Q2,Q3 2019 4 Read and Understand English in % increased across India but remained unchanged -

Statement Showing the Quantum of Advertisements

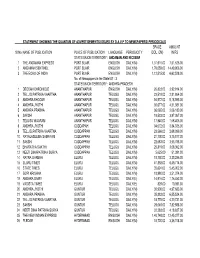

STATEMENT SHOWING THE QUANTUM OF ADVERTISEMENTS ISSUED BY D.A.V.P TO NEWSPAPERS/ PERIODICALS SPACE AMOUNT Sl No NAME OF PUBLICATION PLACE OF PUBLICATION LANGUAGE PERIODICITY (COL .CM) IN RS STATE/UNION TERRITORY : ANDAMAN AND NICOBAR 1 THE ANDAMAN EXPRESS PORT BLAIR ENGLISH DAILY(M) 1,31,916.00 7,51,625.00 2 ANDAMAN SENTINEL PORT BLAIR ENGLISH DAILY(M) 1,76,059.00 14,49,906.00 3 THE ECHO OF INDIA PORT BLAIR ENGLISH DAILY(M) 1,12,515.90 6,62,528.00 No. of Newspapers in the State/UT : 3 STATE/UNION TERRITORY : ANDHRA PRADESH 1 DECCAN CHRONICLE ANANTHAPUR ENGLISH DAILY(M) 26,823.00 3,92,914.00 2 TEL.J.D.PATRIKA VAARTHA ANANTHAPUR TELUGU DAILY(M) 23,519.00 2,81,864.00 3 ANDHRA BHOOMI ANANTHAPUR TELUGU DAILY(M) 54,572.00 5,18,595.00 4 ANDHRA JYOTHI ANANTHAPUR TELUGU DAILY(M) 30,677.00 4,31,381.00 5 ANDHRA PRABHA ANANTHAPUR TELUGU DAILY(M) 36,065.00 2,06,189.00 6 SAKSHI ANANTHAPUR TELUGU DAILY(M) 18,533.00 3,87,367.00 7 TELUGU WAARAM ANANTHAPUR TELUGU DAILY(M) 17,940.00 1,68,405.00 8 ANDHRA JYOTHI CUDDAPAH TELUGU DAILY(M) 34,072.00 3,84,335.00 9 TEL.J.D.PATRIKA VAARTHA CUDDAPPAH TELUGU DAILY(M) 23,566.00 2,68,399.00 10 RAYALASEEMA SAMAYAM CUDDAPPAH TELUGU DAILY(M) 21,700.00 3,75,877.00 11 SAKSHI CUDDAPPAH TELUGU DAILY(M) 22,683.00 3,95,788.00 12 BHARATHA SAKTHI CUDDAPPAH TELUGU DAILY(M) 25,819.00 3,08,362.00 13 NEETI DINAPATRIKA SURYA CUDDAPPAH TELUGU DAILY(M) 5,625.00 51,391.00 14 RATNA GARBHA ELURU TELUGU DAILY(M) 18,750.00 3,33,285.00 15 ELURU TIMES ELURU TELUGU DAILY(M) 41,858.00 6,49,774.00 16 STATE TIMES ELURU TELUGU DAILY(M) 35,624.00 -

S.No Name of the Media Person Designation Place of Working Organization Acc

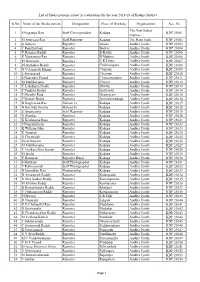

List of Media persons issued Accreditations for the year 2018-19 of Kadapa District S.No Name of the Media person Designation Place of Working Organization Acc. No The New Indian 1 S Nagaraja Rao Staff Correspondent Kadapa KDP 23001 Express 2 M Srinivasa Rao Staff Reporter Kadapa The Hans India KDP 23002 3 A Sanjeev Reporter Atloor Andhra Jyothi KDP 23003 4 T Ramthirtham Reporter Badvel Andhra Jyothi KDP 23004 5 V Ramana Reddy Reporter B Kodur Andhra Jyothi KDP 23005 6 K Nageswara Rao Reporter B Mattam Andhra Jyothi KDP 23006 7 M Narayana Reporter C.K.Dinne Andhra Jyothi KDP 23007 8 M Sudhakar Reddy Reporter Chakrayapeta Andhra Jyothi KDP 23008 9 N V Sampath Kumar Reporter Chapadu Andhra Jyothi KDP 23009 10 L Sivaprasad Reporter Chennur Andhra Jyothi KDP 23010 11 S Nagendra Prasad Reporter Chinnamandem Andhra Jyothi KDP 23011 12 M Mallikarjuna Reporter Chitvel Andhra Jyothi KDP 23012 13 Y Lakshman Naidu Reporter Duvvur Andhra Jyothi KDP 23013 14 P Venkata Reddy Reporter Galiveedu Andhra Jyothi KDP 23014 15 P Maruthi Raju Reporter Gopavaram Andhra Jyothi KDP 23015 16 P Mastan Basha Reporter Jammalamadugu Andhra Jyothi KDP 23016 17 B Nageswara Rao Edition I/c Kadapa Andhra Jyothi KDP 23017 18 B Govinda Swamy Bureau I/c Kadapa Andhra Jyothi KDP 23018 19 E Anjaneyulu Staff Reporter Kadapa Andhra Jyothi KDP 23019 20 N Shankar Reporter Kadapa Andhra Jyothi KDP 23020 21 K Krishnama Raju Reporter Kadapa Andhra Jyothi KDP 23021 22 P Nagamallaiah Reporter Kadapa Andhra Jyothi KDP 23022 23 K William John Reporter Kadapa Andhra Jyothi KDP 23023 24 -

1 Office of the Assistant Director, Information and Public Relations

1 Office of the Assistant Director, Information and Public Relations Department, West Godavari District, Eluru. Details of Accreditation Sanctioned :- Format – 1 S.No. No. of Applications No. of Cards Sanctioned No. of Cards distributed Received 1 1557 1080 620 Submitted for favour of kind information. Assistant Director, Information and Public Relations Department, West Godavari District, Eluru. Copy Submitted to the Commissioner, Information and Public Relations Department, Hyderabad for favour of kind information. Copy Submitted to the Regional Joint Director, Zone-II, Information and Public Relations Department, Vijayawada, Krishna District for favour of kind information. 2 Office of the Assistant Director, Information and Public Relations Department, West Godavari District, Eluru. Details of Accreditation Sanctioned :- Format – 2 S.No. Organization No. of State Cards No. of District Cards 1. The Hindu 1 2. Indian Express 1 3. Eenadu 2 52 4. Sakshi Daily 8 55 5. ACT TV 4 3 6. Andhra Jyothi 10 54 7. Andhra Bhoomi 3 44 8. Andhra Prabha 5 45 9. Vartha 9 55 10. Visalaandhra 5 22 11. Prajasakthi 5 49 12. Surya 5 15 13. Hansindia 1 14. ETV 2 9 15. PTI 1 16. All India Radio 1 17. Doordarshan 1 6 18. Sakshi TV 4 13 19. TV-9 4 7 20. NTV 2 14 21. 10 TV 4 12 22. Gemini News 4 13 23. ABN Andhra Jyothi 4 10 24. I News 4 13 25. TV 5 4 10 26. Maha TV 4 27. CVR News 4 13 28. Express TV 4 13 29. Studio N 4 11 30. 6 TV 4 13 31. -

Kevalkumar M. Patel1 and Avinashi Mahant2

e-Library Science Research Journal ISSN : 2319-8435 Impact Factor : 2.2030(UIF) Vol.3 | Issue.4 | Feb. 2015 Available online at www.lsrj.in A BIBLIOMETRIC STUDY OF INDIA PRESS: FREE ONLINE E- NEWSPAPERS Kevalkumar M. Patel1 and Avinashi Mahant2 1Librarian of C. K. Shah Vijapurwala Institute of Management, Pratapnagar, Vadodara, Gujarat. 2Librarian of Anand People’s Medicare Society, Anand, Gujarat. Abstract:-The “India Press” (http://www.indiapress.org) provides read free online newspapers links to all Indian different language daily newspapers without downloading their fonts including all regional newspapers of India. In this research paper author made an effect to study the total number of 101 full texts read free online newspapers were accesses through “India Press” and analyzed based on title/alphabetical word wise, state wise, languages wise published in India their accessibility of archives of read free online newspapers. Keywords:Online Newspapers, Read Free Online Open Access, Online E-Newspapers, India Press 1.INTRODUCTION A newspaper plays an important role in disseminating current information and events and keeps its readers up-to-date. The electronic newspaper or e-newspaper is a self-contained, reusable and refreshable version of a traditional newspaper that acquires and holds information electronically. Moreover, electronic newspapers retrieve information electronically from online databases, process it electronically with word processors, desktop publishing packages and a variety of more technical hardware and software, and transmit it electronically to the end- users. Broadly speaking, e-news items which evolve from ‘online newspaper’, ‘PDF newspaper’, and ‘e-news via e- devices’ may not be taken synonymously since they are different from each other in terms of developments and use. -

Sl No Code NEWSPAPER PUBLICATION Lan/Per

Home Back Print Statement showing the quantum of advertisements issued by DAVP to various newspapers/periodicals during the year 2012- 13 ------------------------------------------------------------------------------------------------------------- Sl No Code NEWSPAPER PUBLICATION Lan/Per INSERTIONS SPACE(sq.CM) Amount(Rs) ------------------------------------------------------------------------------------------------------------- State : ANDAMAN AND NICOBAR------------------------------------------------------ 1 310672 ARTHIK LIPI PORTBLAIR BEN/D 11 9,722.82 67,059.00 2 100771 THE ANDAMAN EXPRESS PORTBLAIR ENG/D 259 1,32,899.00 8,18,036.00 3 101067 THE ECHO OF INDIA PORTBLAIR ENG/D 343 1,70,361.00 16,21,012.00 State : ANDHRA PRADESH------------------------------------------------------ 1 410441 PRAJA JYOTHI ADILABAD TEL/D 38 24,505.00 3,21,598.00 2 410469 PRAJA JYOTHI ADILABAD TEL/W 2 816.00 6,228.00 3 410198 ANDHRA BHOOMI ANANTHAPUR TEL/D 73 42,095.40 4,07,428.00 4 410202 ANDHRA JYOTHI ANANTHAPUR TEL/D 23 13,325.00 1,98,441.00 5 410345 ANDHRA PRABHA ANANTHAPUR TEL/D 54 39,296.00 3,74,874.00 6 100820 DECCAN CHRONICLE ANANTHAPUR ENG/D 47 25,965.60 4,07,040.00 7 410370 SAKSHI ANANTHAPUR TEL/D 35 20,973.75 5,41,577.00 8 410171 TEL.J.D.PATRIKA VAARTHA ANANTHAPUR TEL/D 23 14,419.00 1,83,424.00 9 410400 TELUGU WAARAM ANANTHAPUR TEL/D 33 23,804.00 2,65,972.00 10 410495 VINIYOGA DHARSINI ANANTHAPUR TEL/M 1 408.00 4,172.00 11 410219 ANDHRA JYOTHI CUDDAPPAH TEL/D 25 14,346.00 1,81,268.00 12 410391 BHARATHA SAKTHI CUDDAPPAH TEL/D 11 6,321.00 85,465.00 -

Andhra Jyothi 30/6/2011 Eenadu 30/6/2011

Andhra Jyothi 30/6/2011 Eenadu 30/6/2011 Governance Now, 1/7/2011 Workshop to counter Telanga movement Visalandhra Mahasabha, a pro-united Andhra Pradesh organisation, is conducting a workshop on July 5 in New Delhi. The workshop will have eminent speakers from the academia and polity and some with public service background. The workshop will expose "truths" of the separatist movement for Telangana in the social, economic, political and cultural domains. The invitation to the workshop is reproduced below. Dear Supporters, Visalandhra Mahasabha is an organization committed towards a united Andhra Pradesh. It is a group of intellectuals, professionals, educationists and other socially conscious patriots from all the regions of AP – Telangana, Coastal Andhra and Rayalaseema.The separatist agitation in the state of Andhra Pradesh and the demand for separate Telangana is fraught with not only violence and vandalism based on claims of vicitimisation of Telangana people, but also fundamentally based on falsehood and distortion of facts and figures. The demand for Telangana is completely unjust.In this context, Visalandhara Mahasabha is attempting to showcase the hitherto unknown truths in social, economic, political, cultural and hitorical domains through a media Workshop and exhibition On The Unjust Demand for Telangana.We hope that this endeavor of ours helps you in arriving at a balanced view of the scenario based on facts rather than conjectures and wrong propaganda. The venue and other details are as follows. Workshop-1: July 5th 11.00 AM – 1.00 PM • Kuldip Nayar- Sr. Journalist • Sitaram Yechury- MP & CPM Politburo Member Workshop-2: July 6th 3.00 PM – 5.00 PM • K.P.S.