Electricity and Natural Gas Cost Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Below Is the List of Category 1, 2, and 3 Slot Machine Licensees Who Have Been Awarded an Interactive Gaming Certificate by the Pennsylvania Gaming Control Board

Below is the list of Category 1, 2, and 3 Slot Machine Licensees who have been awarded an Interactive Gaming Certificate by the Pennsylvania Gaming Control Board. Also listed are the Interactive Gaming Operators licensed by the Board to provide interactive gaming on behalf of the Interactive Gaming Certificateholder, and any authorized website for interactive gaming. If no Interactive Gaming Operator or Manufacturer, types of interactive gaming authorized, or interactive gaming website are listed, interactive gaming has not yet been authorized for that Certificateholder or Operator. The commencement date of interactive gaming operations is also listed for each website. Format • Interactive Gaming Certificateholder o Interactive Gaming Operator ▪ Types of interactive gaming authorized • Authorized websites or mobile apps o Commencement date of operations • Chester Downs and Marina, LLC d/b/a Harrah’s Philadelphia Casino and Racetrack o No interactive gaming operator ▪ Slots; Table Games • https://pa.caesarsonline.com/#HarrahsPhiladelphi a • Caesars PA mobile app o April 23, 2020 ▪ Poker • http://www.wsop.com/#HarrahsPhiladelphia • WSOP Mobile app o July 15, 2021 Updated: 8/11/2021 • Downs Racing, LP d/b/a Mohegan Sun Pocono o Unibet Interactive, Inc. ▪ Slots; Table Games • https://pa.unibet.com/mohegansun/casino • Unibet mobile app o November 15, 2019 • Greenwood Gaming and Entertainment, Inc. d/b/a Parx Casino o No interactive gaming operator ▪ Slots; Table Games • https://pa.parxcasino.com/ • Parx Casino mobile app o July 17, 2019 • Mount -

With the a Message from Our President & CEO the Greater Wyoming Valley Chamber of Commerce Dba the the Workplace, and the Economic Impact to Uplift the Area

Celebrate & Support Local with the A Message from Our President & CEO The Greater Wyoming Valley Chamber of Commerce dba the the workplace, and the economic impact to uplift the area. It’s not Greater Wilkes-Barre Chamber of Commerce (The Chamber) the heavy load that breaks you down; it’s how you carry it. We and Greater Wilkes-Barre Chamber of Business and Industry is know how to do the heavy lifting and we know how to carry it. dedicated to local businesses of all sizes, to the diversity of our workforce and industrial base, and to the vitality and quality of We are better than anything this pandemic brings. Helen Keller life in our community. once said, “The best and most beautiful things in the world can’t be seen or even heard, they must be felt from the heart.” • We connect, innovate and elevate our local businesses, com- munity and economy. We have a rich diversity of workforce and workplace, a strong • We build value to attract businesses to the area. culture of charity and support, all represented right here in or- • We build sustainability to create legacy businesses. ganizations throughout the Wyoming Valley that truly shine • We build upon our core business value propositions to make amongst us. And during a time of this pandemic, reflect that life it built to last. always waits for a crisis to reveal how brilliant we can be and • We advocate on business related policy and government af- how we can pivot during this time of crisis to be rebuilt, as we fairs for our members with our NEPA, State and Federal lead- regain our foothold to build it back reimagined and better. -

Kindred Goes Online in Pennsylvania

Kindred Group Press Release Malta, 15 November 2019 Kindred goes online in Pennsylvania Only a few weeks after launching the Unibet Sportsbook at Mohegan Sun Pocono, Kindred Group goes live with both online sports and casino in Pennsylvania. As of today, Unibet customers in Pennsylvania will be able to experience a full range of first-class sportsbook and casino products in a safe and secure environment. Kindred Group (previously Unibet Group) takes its next significant step in the US market with the launch of both online sports and casino in Pennsylvania. The announcement is in line with the Group’s strategy to establish a presence in what will most likely become the largest gambling market in the world. Kindred continues to adopt a local focus and global expertise wherever it operates, ensuring that customers can enjoy Unibet’s full range of first-class sportsbook and casino products in a familiar, safe and secure environment. “After a successful launch of our betting lounge, Unibet Sportsbook at Mohegan Sun Pocono, we are thrilled to take the partnership with Mohegan Sun online and bring the Pennsylvanian guests a state-of-the-art online gambling experience, including the best online casino games and an impressive online sportsbook”, says Manuel Stan, SVP Kindred US. “We’re thrilled to introduce to our customers an opportunity to place bets and game online within the state borders,” said Aviram Alroy, Vice President of Interactive Gaming at Mohegan Gaming & Entertainment. “Our sportsbook lounge is a highly engaging and joyful experience on-premises and Kindred Group are able to extend that experience online through our strategic partnership.” This is Kindred’s second state in the US, after launching online casino and sportsbook earlier this year in New Jersey in partnership with Hard Rock Hotel & Casino Atlantic City. -

Annualreport

ANNUALReport PENNSYLVANIA Gaming Control Board 2018-2019 Published - October 1, 2019 TABLE OF Contents Board Members ........................................................................................................... 2 Message from Chairman Barasch ...............................................................................3 Message from Executive Director O’Toole ................................................................3 Year in Review ...........................................................................................................4-7 Office of Compulsive & Problem Gambling ...............................................................8 Category 4 Satellite Casinos ........................................................................................9 1 Video Gaming Terminals at Truck Stops ................................................................... 10 Interactive Gaming ..................................................................................................... 11 Sports Wagering .........................................................................................................12 Fantasy Contests ........................................................................................................13 Revenue and Expenditures ....................................................................................... 14 Public Meetings and Executive Sessions ..................................................................15 Casino Revenue Data ........................................................................................... -

Below Is the List of Category 1, 2, 3, and 4 Slot Machine Licensees Who Have Been Awarded a Sports Wagering Certificate by the Pennsylvania Gaming Control Board

Below is the list of Category 1, 2, 3, and 4 Slot Machine Licensees who have been awarded a Sports Wagering Certificate by the Pennsylvania Gaming Control Board. Also listed are the Sports Wagering Operators who are licensed by the Board to provide sports wagering on behalf of the Sports Wagering Certificateholder, and any authorized website for interactive sports wagering. If no Sports Wagering Operator or types of sports wagering authorized are listed, a Sports Wagering Certificate has been issued, but no sports wagering has been authorized. If no website is listed, interactive or mobile sports wagering has not yet been authorized for that Operator. The commencement dates of online and retail sports wagering operations are also listed for each certificateholder. Format • Sports Wagering Certificateholder o Sports Wagering Operator ▪ Types of sports wagering authorized • Authorized websites and mobile apps o Commencement of online sports wagering o Commencement of retail sports wagering • Chester Downs and Marina, LLC d/b/a Harrah’s Philadelphia Casino and Racetrack o OpenBet Technologies Limited; NYX Digital Gaming (USA), LLC; American Wagering, Inc. ▪ Retail sportsbook ▪ Caesars online/mobile sportsbook • https://pa.caesarsonline.com/sports • Caesars PA mobile app o Online: March 13, 2020 o Retail: January 24, 2019 Updated: 6/28/2021 • Downs Racing, LP d/b/a Mohegan Sun Pocono o Unibet Interactive, Inc. ▪ Retail sportsbook ▪ Unibet online/mobile sportsbook • https://pa.unibet.com/sports#home • Unibet mobile app o Online: November 15, -

State of the States 2020 the AGA Survey of the Commercial Casino Industry a Message from the American Gaming Association

State of the States 2020 The AGA Survey of the Commercial Casino Industry A Message from the American Gaming Association June 2020 Dear Gaming Industry Colleague: gaming. Sports betting was being legalized at an unprecedented pace, with 20 states and the District of I am pleased to present State of the States 2020: Columbia having passed legislation allowing consumers The AGA Survey of the Commercial Casino Industry, to bet on sports with legal, regulated operators. the American Gaming Association’s (AGA) signature research report and the definitive economic analysis The AGA continues its important work as your of U.S. commercial gaming in 2019. advocate. Here in Washington, DC, we continue to cultivate Congressional champions from gaming 2019 marked another record-setting year for the communities and strengthen our voice on Capitol commercial gaming segment. Helped in part by the Hill. In states across the country, we are working with expansion of legal sports betting, the commercial industry leaders and regulators to give operators and casino sector logged its fifth consecutive year of suppliers more flexibility in running their businesses gaming revenue growth in 2019—surging 3.7 percent and evolve regulation to meet the demands of our to $43.6 billion, a new historic high. 21st century hospitality industry. At the end of 2019, Americans never had a higher On a personal note, it has been a privilege to get to opinion of our industry and nearly half said they know many of you during my first year as the AGA’s planned to visit a casino over the next year. -

2015 Annual Report

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 ____________________________________________________________ FORM 10-K ____________________________________________________________ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended September 30, 2015 or TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number 033-80655 ____________________________________________________________ MOHEGAN TRIBAL GAMING AUTHORITY (Exact name of registrant as specified in its charter) ____________________________________________________________ Not Applicable 06-1436334 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.) One Mohegan Sun Boulevard, Uncasville, CT 06382 (Address of principal executive offices) (Zip Code) (860) 862-8000 (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: None None (Title of each class) (Name of each exchange on which registered) Securities registered pursuant to Section 12(g) of the Act: None (Title of Class) ____________________________________________________________ Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act: Yes No Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act: Yes No Indicate by check mark whether -

Mohegan Tribal Gaming Authority Announces Closing of Financing for Construction of Exposition and Convention Center

MOHEGAN TRIBAL GAMING AUTHORITY ANNOUNCES CLOSING OF FINANCING FOR CONSTRUCTION OF EXPOSITION AND CONVENTION CENTER Uncasville, CT, April 19, 2017 – The Mohegan Tribal Gaming Authority, or the Authority, the owner of Mohegan Sun in Uncasville, Connecticut, and Mohegan Sun Pocono in Wilkes-Barre, Pennsylvania, announced today that it has closed on its financing for the construction of its planned $80 million, 240,000- square-foot exposition and convention center. The exposition and convention center will be located adjacent to and fully integrated into the Authority’s flagship property in Connecticut, Mohegan Sun, and is expected to open in the summer of 2018. “With this financing in place, we are excited to proceed with the construction phase of the project and look forward to its planned opening next summer,” said Mario C. Kontomerkos, Chief Financial Officer of the Authority. “Mohegan Sun currently turns away tens of thousands of meeting room requests every year. This new amenity will provide us with much needed exposition and meeting space to capture these requests and will continue to solidify Mohegan Sun as the Northeast’s preeminent gaming and non-gaming destination.” About the Authority The Authority is an instrumentality of the Mohegan Tribe of Indians of Connecticut, or the Tribe, a federally recognized Indian tribe with an approximately 595-acre reservation situated in southeastern Connecticut, adjacent to Uncasville, Connecticut. The Authority has been granted the exclusive authority to conduct and regulate gaming activities on the existing reservation of the Tribe, including the operation of Mohegan Sun, a gaming and entertainment complex located on an approximately 185-acre site on the Tribe’s reservation. -

State of the States 2021

State of the States 2021 The AGA Survey of the Commercial Casino Industry © Chon Kit Leong / Alamy Stock Photo A Message from the American Gaming Association May 2021 a strong industry advocate in Washington, and the AGA worked tirelessly to deliver access to federal Dear Gaming Industry Colleague: stimulus for gaming businesses. Unlike every previous I am pleased to present State of the States 2021: federal stimulus that explicitly carved gaming out, The AGA Survey of the Commercial Casino Industry, suffering gaming entities were able to access hundreds the American Gaming Association’s (AGA) signature of millions of dollars in relief offered as part of the research report and the definitive economic analysis of CARES Act. And we’ll never settle for anything less U.S. commercial gaming in 2020. than this equal footing again. The U.S. commercial gaming sector entered 2020 with In the months ahead, we will continue our efforts strong momentum. On the heels of five consecutive to recruit Congressional champions from gaming years of gaming revenue expansion, January and communities, strengthen our voice on Capitol Hill February 2020 showed strong growth to start the year, and highlight the vital role gaming’s recovery plays in and the continued advancement of legal casino gaming communities across the country. and sports betting was providing access to regulated Although 2020 presented a tremendous challenge gaming to an ever-growing number of Americans. and many headwinds remain, I’m optimistic about With such a positive start to the year, the immediate gaming’s future. States around the country expanded impacts of the COVID-19 pandemic were jarring. -

MOHEGAN SUN P O C O N O O

MOHEGAN SUN P O C O N O o MOHEGAN SUN POCONO Written Testimony of Anthony Carlucci President and General Manager Submitted to: PENNSYLANIA HOUSE OF REPRESENTATIVES GAMING OVERSIGHT COMMITTEE Public Hearing on the Impacts of the Covid-19 Pandemic on Pennsylvania’s Casinos February 24, 2021 Honorable Chairs and Members of the House Gaming Oversight Committee: On behalf of Mohegan Sun Pocono, thank you for holding this hearing and bringing attention to the substantial impacts and challenges the Covid-19 pandemic has thrust upon Pennsylvania’s Casino industry, including our operations in Wilkes-Barre, Pennsylvania, our employees and our business and community partners. Mohegan Sun Pocono whole-heartedly joins in the joint written testimony submitted by us and our fellow casinos, and we submit this additional statement addressing our specific experiences during the pandemic for the Committee’s consideration. Like so many businesses across the Commonwealth, especially those in the hospitality industry, the Covid-19 pandemic wrought devastating effects on our company, our family of employees and our business. From mid-March until mid to late June 2020, our operations were forced to close, severely restricting our revenue while the costs associated with our facilities went largely unabated. This same scenario was suffered again in mid-December 2020, when the state for a second time forced us to close our doors (despite the investment of considerable sums to ensure safe operations). When business has been permitted to resume, our operations have been dealt a serious blow from the severe restrictions and capacity limitations imposed under the state’s mitigation orders. -

(PSAP) Inventory Report

Commonwealth of Pennsylvania Public Safety Answering Point (PSAP) Inventory Report Submitted to the Pennsylvania Emergency Management Agency (PEMA) March 30, 2016 TABLE OF CONTENTS EXECUTIVE SUMMARY ........................................................................................................................................... 1 1. INTRODUCTION ................................................................................................................................................. 4 2. 9-1-1 IN THE COMMONWEALTH TODAY ........................................................................................................ 9 FACILITIES .......................................................................................................................................................... 12 CALL DELIVERY .................................................................................................................................................. 22 CALL PROCESSING ........................................................................................................................................... 27 CALL DISPATCH ................................................................................................................................................. 33 SUMMARY ........................................................................................................................................................... 49 3. PSAP INVENTORY SUMMARIES ................................................................................................................... -

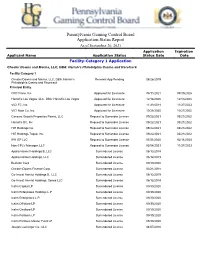

Pennsylvania Gaming Control Board Application Status Report

Pennsylvania Gaming Control Board Application Status Report As of September 26, 2021 Application Expiration Applicant Name Application Status Status Date Date Facility-Category 1 Application Chester Downs and Marina, LLC, DBA: Harrah’s Philadelphia Casino and Racetrack Facility-Category 1 Chester Downs and Marina, LLC, DBA: Harrah’s Renewal App Pending 08/26/2019 Philadelphia Casino and Racetrack Principal Entity CRC Finco, Inc Approved for Licensure 08/11/2021 08/10/2026 Harrah's Las Vegas, LLC, DBA: Harrah's Las Vegas Approved for Licensure 12/16/2020 12/15/2025 VICI FC, Inc. Approved for Licensure 11/28/2018 11/27/2023 VICI Note Co. Inc. Approved for Licensure 10/28/2020 10/27/2025 Caesars Growth Properties Parent, LLC Request to Surrender License 09/22/2021 03/21/2022 Harrah's BC, Inc Request to Surrender License 09/22/2021 03/21/2022 HIE Holdings Inc. Request to Surrender License 09/22/2021 03/21/2022 HIE Holdings Topco, Inc. Request to Surrender License 09/22/2021 03/21/2022 IPH GP LLC Request to Surrender License 07/31/2020 02/11/2025 Non-CPLV Manager, LLC Request to Surrender License 05/04/2021 11/27/2023 Apollo Hamlet Holdings B, LLC Surrendered License 06/12/2019 Apollo Hamlet Holdings, LLC Surrendered License 06/12/2019 Beckton Corp Surrendered License 09/30/2020 Chester Downs Finance Corp. Surrendered License 03/21/2018 Co-Invest Hamlet Holdings B, LLC Surrendered License 06/12/2019 Co-Invest Hamlet Holdings, Series LLC Surrendered License 06/12/2019 Icahn Capital LP Surrendered License 09/30/2020 Icahn Enterprises Holdings L.P.