Transferring Your Company to Key Employees White Paper

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Preqin Special Report: Subscription Credit Facilities

PREQIN June 2019 SPECIAL REPORT: SUBSCRIPTION CREDIT FACILITIES PREQIN SPECIAL REPORT; SUBSCRIPTION CREDIT FACILITIES Contents 3 CEO’s Foreword 4 Subscription Credit Facility Usage in Private Capital 7 Subscription Lines of Credit and LP-GP Alignment: ILPA’s Recommendations - ILPA 8 Are Subscription Facilities Oversubscribed? - Fitch Ratings 10 Subscription Finance Market - McGuireWoods LLP Download the Data Pack All of the data presented in this report is available to download in Excel format: www.preqin.com/SCF19 As with all our reports, we welcome any feedback you may have. To get in touch, please email us at: [email protected] 2 CEO's Foreword Subscription credit facilities: angels or demons? A legitimate and valuable tool for managing liquidity and streamlining transactions in a competitive market, or a cynical ploy for massaging IRRs? The debate continues in private equity and wider private capital circles. As is often the case, historical perspective is helpful. Private capital operates in a dynamic and competitive environment, as GPs and LPs strive to achieve superior net returns, through good times and bad. Completing deals and generating the positive returns that LPs Mark O’Hare expect has never been more challenging than it is CEO, Preqin today, given the availability of capital and the appetite for attractive assets in the market. Innovation and answers: transparent data, combined with thoughtful dynamism have long been an integral aspect of the communication and debate. private capital industry’s arsenal of tools, comprised of alignment of interest; close attention to operational Preqin’s raison d’être is to support and serve the excellence and value add; over-allocation in order to alternative assets industry with the best available data. -

Valuing the Employee Purchase of Employer Company Stock—Part II

VOL. 13, ISSUE NO. 4 OCTOBER 2010 Valuing the Employee Purchase of Employer Company Stock—Part II by Robert F. Reilly 8. Protective provisions and veto rights; 9. Board participation rights; Editor’s Note : The previous installment of this series sum- 10. Drag-along rights; marized the generally accepted valuation approaches related 11. Right to participate in future equity offerings; to the employee purchase of employer company stock. This 12. Right of fi rst refusal in future equity offerings; installment summarizes the impact of security-specifi c con- 13. Management rights; tractual rights and privileges on the employer stock valuation . 14. Access to information rights; and 15. Tag-along rights. Contractual Rights and Privileges Some contractual rights and privileges can separately (and Each of the above-listed contractual rights may relate to a materially) impact the stock value in an employee stock pur- particular class of employer company equity. More com- chase, as well as have an effect on the stock marketability and monly, these particular rights and privileges may only relate, control attributes. The valuation analyst should ensure that by contract, to a particular block of the company stock. For the value increment associated with contractual rights is not example, that block of stock may be the stock sold to the double-counted (i.e., both considered as a marketability/con- general employee group, the stock granted to identifi ed senior trol attribute and then added again as a contractual attribute). executives, or the stock retained by certain members of the company founding family. Each of these contractual rights and The analyst should also ensure that the full value increment privileges has a value. -

2016-2017 MBA Courses for Finance Development Program Course Offerings and Descriptions

2016-2017 MBA Courses for Finance Development Program Course Offerings and Descriptions Preparing Financial Professionals for Success 1.0 About Training The Street: Training The Street (TTS) offers state-of-the-art, instructor-led courses in capital markets, financial modeling and corporate valuation. Founded in 1999, TTS is the world’s leading financial learning services company offering targeted and customized training courses to corporate and educational clients. TTS’s corporate clients include the world’s leading investment banks, consulting firms & Fortune 500 companies. We specialize in applied learning using practical examples and annotated guides. With more than 150 years of combined professional and teaching experience, TTS's instructors have worked across a broad spectrum of industries-from high-technology to retail-and across a wide range of financial disciplines-from investment banking, accounting, and financial research to global trade finance and credit risk management. Several of our instructors are Adjunct Professors at leading academic institutions. For more information on TTS, please visit www.trainingthestreet.com. Calendar of Courses Offered: 2016-2017 Finance Development Program 1) Excel Best Practices – Friday, August 19, 2016 (5:00 – 9:00pm), Koury 2) Introduction to Financial Modeling – Friday, September 16, 2016 (1:00pm – 5:00pm), Kenan 204 3) M&A Strategy and Corporate Valuation – Saturday, September 24, 2016 (9:00am – 5:00pm), McColl 2250 4) Anatomy of a Deal – Saturday, October 1, 2016 (10:00am – 4:00pm), McColl 2500 5) LBO Modeling – Tuesday, October 25, 2016 (4:30pm – 8:30pm), McColl 2500 6) Restructuring and Credit Analysis – Friday, November 11, 2016 (9:00am – 5:00pm), McColl 2600 7) Interview Preparation: Private Equity – Saturday, December 3, 2016 (9:00am – 11:30pm), McColl 2500 8) Interview Preparation: Finance – Saturday, December 3, 2016 (12:00pm – 3:30pm), McColl 2500 Detailed course descriptions are on the following pages. -

Unpacking Private Equity Characteristics and Implications by Asset Class

Unpacking Private Equity Characteristics and Implications by Asset Class www.mccombiegroup.com | +1 (786) 664-8340 Unpacking Private Equity: Characteristics & implications by asset class The term private equity is often treated as a catchall, used interchangeably to describe a broad variety of investments. Such loose use of the phrase fails to capture the range of nuanced business ownership strategies it refers to and risks branding an entire asset class with characteristics and implications that are typically relevant to only a particular sub-category. Recently, this has especially been the case given the outsized global attention placed on the leveraged buyout deals of Bain Capital, a private equity firm founded by Republican U.S. presidential candidate Mitt Romney. In this context, popular discourse has inappropriately attached the label of private equity to a general practice of debt-fueled corporate takeovers that disproportionately focus on cost cutting. In reality, however, private equity refers to an array of investment strategies each with a unique risk-return profile and differing core skillsets for success. This article is intended to help family office executives better understand the nuances of the various sub-categories of private equity. It seeks to draw high-level distinctions, serving as a practical guide for investors entering the private equity arena, be it directly or through a more curated fund structure. Ultimately by understanding the characteristics and implications of each asset class, the reader should be equipped to make an educated choice regarding the most relevant and appropriate strategy for their unique profile. From a technical perspective, private equity is nothing more than making investments into illiquid non-publicly traded companies— i.e. -

Bfm Sem – Vi Corporate Restructuring

BFM SEM – VI CORPORATE RESTRUCTURING Multiple Questions:- 1. _________ merger involves firm engaged in unrelated types of activities. a. Vertical b. Horizontal c. Conglomerate d. Demerger 2. When existing company is dissolved to form few new companies, it is called as ________ a. Sin off b. Split off c. Split up d. All of the above 3. __________means an acquirer takes over the control of the target company. a. Joint Venture b. Takeover c. Disinvestment d. Demerger 4. The ___________means changing the structure of an organization such as reducing the hierarchical levels. a. Financial Restructuring b. Organizational Restructuring c. Corporate Restructuring d. All of the above 5. ________parties work together or a single project for a finite period of time. a. Strategic Alliance b. Joint Venture c. Disinvestment d. Franchising 6. __________means the action of an organization or government selling or liquidating an asset or subsidiary. a. Merger b. Joint Venture c. Takeover d. Disinvestment 7. __________ is an arrangement whereby the assets of two or more companies come under the control of one company. a. Merger b. Buyout c. Joint Venture d. Demerger 8. ________may be defined as an arrangement where one party grants another party the right to use trade name. a. Alliance b. Franchising c. Slump sale d. Joint Venture 9. ________merger is a merger of two or more companies that compete in the same industry. a. Vertical b. Horizontal c. Co generic d. Conglomerate 10. ____________ helps a firm to grow and expand. a. Corporate Restructuring b. Merger c. Takeover d. Demerger 11. In _________, company distributes its shareholding in subsidiary to its shareholders thereby not changing the ownership pattern. -

Sword Group 2014 Financial Report

Sword Group 2014 Financial Report 1,201 employees as at 31/12/2014 19 countries Revenue 2014: €117.1 million EBITDA: 16.1% CONTENTS 1 STATEMENT BY THE PERSONS IN CHARGE OF THE 2014 FINANCIAL REPORT P 3 2 INDEPENDENT AUDITOR P 3 3 DIRECTORS P 3 4 COMPANY INFORMATION P 3 5 KEY FINANCIAL INFORMATION P 4 6 GROUP ORGANISATION CHART P 5 7 OVERVIEW OF ACTIVITIES P 6 8 CORPORATE SOCIAL RESPONSIBILITY P 7 9 CORPORATE GOVERNANCE P 8 10 MANAGEMENT REPORT P 19 11 INDEPENDENT AUDITOR’S REPORT ON THE ANNUAL ACCOUNTS AS AT 31 DECEMBER 2014 P 43 12 ANNUAL ACCOUNTS AS AT 31 DECEMBER 2014 P 44 13 NOTES TO THE 2014 ANNUAL ACCOUNTS P 51 14 INDEPENDENT AUDITOR’S REPORT ON THE CONSOLIDATED FINANCIAL STATEMENTS AS AT 31 DECEMBER 2014 P 62 15 CONSOLIDATED FINANCIAL STATEMENTS AS AT 31 DECEMBER 2014 P 63 16 NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS AS AT 31 DECEMBER 2014 P 70 17 CONTACTS P 125 Sword Group – Financial Report 2014 V19-03-2015 Page 2 1 STATEMENT BY THE PERSONS IN CHARGE OF THE 2014 FINANCIAL REPORT 2014 Pursuant to Article 3 (2) c) of the Law of 11 January 2008 on transparency requirements for information about issuers whose securities are admitted to trading on a regulated market, I declare that these financial statements have been prepared in accordance with applicable accounting standards and that the financial statements present fairly, to my knowledge, a true and fair view of the financial position as at 31 December 2014, financial performance and cash flows of the Company and a description of the principal risks and uncertainties the Company faces. -

Employee Stock Ownership Plan Vs. Management Buyout

The following information and opinions are provided courtesy of Wells Fargo Bank, N.A. Wealth Planning Update Employee stock ownership plan vs. management buyout MAY 2021 Key takeaways: Jeremy Miller • When considering the transition of your business, a sale to an Senior Business Transition Strategist employee stock ownership plan (ESOP) and a management Wells Fargo Bank, N. A. buyout (MBO) are two alternatives that allow the business to continue to be run by your existing employees. Joseph Gilbert • An ESOP allows all of the employees to have ownership in the Financial Advisor business and can include tax advantages. Wells Fargo Advisors • An MBO allows you to choose which key employees the business is sold to. What this may mean for you: • It is important to review the strengths and weaknesses of an ESOP and an MBO and see how they align with the facts and circumstances of your situation in order to determine if either transition alternative is the right fit for your business. Transitioning a business is a monumental step for a business owner. Therefore, it is important to understand your options to have confidence that the transition option you ultimately choose is right for you. As you evaluate your alternatives, two options that are commonly compared side by side are an ESOP and an MBO. Approximately 25% of business owners transition via an MBO, while nearly 5% transition via an ESOP.1 Although the numbers show a preference for an MBO, a thorough review of these two options should be undertaken to know which path is right for you and your business or if an alternate path may be appropriate. -

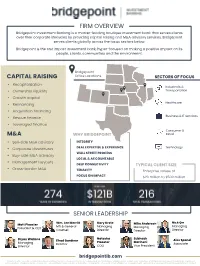

Firm Overview Capital Raising M&A Senior Leadership

FIRM OVERVIEW Bridgepoint Investment Banking is a market-leading boutique investment bank that serves clients over their corporate lifecycles by providing capital raising and M&A advisory services. Bridgepoint serves clients globally across the focus sectors below. Bridgepoint is the first impact investment bank, hyper-focused on making a positive impact on its people, clients, communities and the environment. Bridgepoint CAPITAL RAISING Office Locations SECTORS OF FOCUS • Recapitalization Industrials & • Ownership liquidity Transportation • Growth capital Healthcare • Refinancing • Acquisition financing Business & IT Services • Rescue finance • Leveraged finance Consumer & M&A WHY BRIDGEPOINT Retail • Sell-side M&A advisory INTEGRITY • Corporate divestitures DEAL EXPERTISE & EXPERIENCE Technology WALL STREET PROCESS • Buy-side M&A advisory LOCAL & ACCOUNTABLE • Management buyouts DEEP CONNECTIVITY TYPICAL CLIENT SIZE • Cross-border M&A TENACITY Enterprise values of FOCUS ON IMPACT $20 million to $500 million SENIOR LEADERSHIP Wm. Lee Merritt Gary Grote Nick Orr Matt Plooster Mike Anderson MD & General Managing Managing President & CEO Managing Counsel Director Director Director Natasha Subhash Bryan Wallace Chad Gardiner Alex Spanel Plooster Marineni Managing Director Associate Director COO Vice President bridgepointib.com In order to offer securities-related Investment Banking Services discussed herein, to include M&A and institutional capital raising, certain representatives of Bridgepoint Investment Banking are registered representatives -

Simply BUYOUT a Guide to Employee Buyouts and Becoming an Employee Owned Business Simply Buyout: a Guide to Employee Buyouts and Becoming an Employee Owned Business

Simply BUYOUT A guide to employee buyouts and becoming an employee owned business Simply Buyout: A guide to employee buyouts and becoming an employee owned business Foreword Employee ownership is high on the business and economic agenda and for good reason. Where a business is owned by its workforce, everyone has a stake in success. e longevity of companies with employee ownership is impressive. eir productivity is undoubted. A good number see employee ownership as complex. It need not be. e company can be much like any other company. What is different is how it is owned. Co-operative models are a welcome part of the employee ownership landscape here and abroad. ere are many leading employee owned businesses that can be classified as co-operatives under accepted international definitions. I have helped to advise and form many myself. Co-operative forms of employee ownership help to underpin an active role for employees in terms of governance and accountability. e review I conducted for the Government on employee ownership, which reported in 2012, concluded that clear advice and information is now a Graeme Nuttall key requirement, particularly at the point of business Partner, Field Fisher Waterhouse LLP succession and transfer. I warmly welcome this guide and author of Sharing Success: e Nuttall as key to this and wish you the best for using it. Review of Employee Ownership . Simply Buyout: A guide to employee buyouts and becoming an employee owned business Contents Introduction .................................................................................................................................................................................... 2 Who this guide is for and what it hopes to achieve ............................................................................................................... 2 How to use this guide ...................................................................................................................................................................... -

Reexamining the Effect of Sarbanes-Oxley on Firms' Going-Private Decisions Robert P. Bartle

Going Private But Staying Public: Reexamining the Effect of Sarbanes-Oxley on Firms’ Going-Private Decisions Robert P. Bartlett, III* April 2008 * Assistant Professor of Law, University of Georgia School of Law. I thank Dan Bodansky, Tom Eaton, Kent Greenfield, Paul Heald, Todd Henderson, Christine Hurt, Bob Lawless, Jim Linck, Harold Mulherin, Jeff Netter, Victoria Plaut, Annette Poulsen, Chuck O’Kelley, Peter Oh, Usha Rodrigues, Jim Rogers, Maggie Sachs, Jason Solomon, Jide Wintoki, and workshop participants at the University of Georgia Department of Finance, the Boston College School of Law and the University of Pittsburgh School of Law as well as participants at the 2008 Law and Entrepreneurship Retreat and participants at a 2008 symposium at Brooklyn Law School on the going-private of U.S. capital markets. Additionally, special thanks go to Marc Auerbach of Standard & Poors, and Eric Tutterow of Fitch Ratings for providing helpful data and discussion. All errors are my own. 1 Abstract: This article examines whether the cost of complying with the Sarbanes-Oxley Act of 2002 (SOX) contributed to the rise in going-private transactions after its enactment. Prior studies of this issue generally suffer from a mistaken assumption that by going- private, a publicly-traded firm necessarily immunizes itself from SOX. In actuality, the need to finance a going-private transaction often requires firms to issue high-yield debt securities that subject the surviving firm to SEC-reporting obligations and, as a consequence, most of the substantive provisions of SOX. This paper thus explores a previously unexamined natural experiment: To the extent SOX contributed to the rise in going-private transactions, one should observe after 2002 a transition away from high-yield debt in the financing of going-private transactions towards other forms of “SOX-free” finance. -

Private Equity Buyers As Divestiture Buyers: US and EU Perspectives

THE THRESHOLD Volume XIX, Number 2, Spring 2019 Private Equity Buyers As Divestiture Buyers: U.S. and EU Perspectives The Threshold Volume XIX Number 2 Newsletter of the Mergers & Spring 2019 Acquisitions Committee Marc Williamson, Lindsey Champlin, and Tomas Nilsson* Private equity sponsors globally have more than $3 trillion of assets under management. They are among the most acquisitive firms and account for a large number of merger control filings. A total of 5,106 private equity-backed buyout deals were announced in 2018 with an aggregate deal value of $465 billion.1 Private equity deals in recent years have included a significant number of “carve-outs” – where a unit, division or particular assets were acquired by a private equity fund from a larger company and “stood up” as a standalone business. Bloomberg reports that in the last 10 years, private equity firms have completed more than 460 carve-out deals worth $68.5 billion,2including major deals such as Bain Capital’s $17.9 billion carve-out of Toshiba Memory Corp., Blackstone’s $17 billion carve-out of Thomson Reuters’ Financial & Risk business and Carlyle’s €10.1 billion carve-out of AkzoNobel’s Specialty Chemicals business. * Marc Williamson is a partner and Lindsey Champlin and Tomas Nilsson are associates at Latham & Watkins LLP. 1 William Clarke, Alternatives in 2019: A Bumper Year for Private Equity Buyout Deals in 2018 – Will it Continue?, PREQIN (Jan. 24, 2019), available at https://www.preqin.com/insights/blogs/alternatives-in-2019-a-bumper-year-for-private- equitybuyout-deals-in-2018-will-it-continue/25270 2 Four steps to create value in private equity carve -outs, E&Y (Aug. -

Anatomy of a Leveraged Buyout: Leverage + Control + Going Private

Anatomy of a Leveraged Buyout: Leverage + Control + Going Private Aswath Damodaran Home Page: www.damodaran.com E-Mail: [email protected] Stern School of Business Aswath Damodaran 1 Leveraged Buyouts: The Three Possible Components Increase financial leverage/ debt Leverage Control Leveraged Buyout Take the company Change the way private or quasi- the company is private run (often with existing managers) Public/ Private Aswath Damodaran 2 One Example: The Harman Deal Pre-deal Post-deal Harman Harman Debt $ 4 billion Debt (mostly leases) $274 KKR & Goldman would buy out existing equity investors Publlicly traded KKR, equity Firm will become a Goldman & quasi-private Managers $ 5.5 billion company with 75% $3 billion of the equity held by KKR, Goldman and managers. Public $ 1 billion Aswath Damodaran 3 Issues in valuing leveraged buyouts Given that there are three significant changes - an increase in financial leverage, a change in control/management at the firm and a transition from public to private status - what are the valuation consequences of each one? Are there correlations across the three? In other words, is the value of financial leverage increased or decreased by the fact that control is changing at the same time? How does going private alter the way we view the first two? Given that you are not required to incorporate all three in a transaction, when does it make sense to do a leveraged buyout? How about just a buyout? How about just going for a change in control? Just a change in leverage? Aswath Damodaran 4 I. Value and Leverage Aswath Damodaran 5 What is debt..