Connecting Components, Dividing Communities. Tin Production For

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report 2007 Corporate Directory

ANNUAL REPORT 2007 CORPORATE DIRECTORY Directors Jianming Xiao – Chairman Anthony Wehby – Vice Chairman Stephen Woodham – Non-Executive Director Wenxiang Gao – Non-Executive Director Robin Chambers - Non-Executive Director Richard Hill – Non-Executive Director Company Secretary Mr Matthew Sikirich Registered Office and Principal place of business YTC Resources Limited 2 Corporation Place ORANGE NSW 2800 Telephone: (02) 6361 4700 Facsimile: (02) 6361 4711 Email: [email protected] Share Register Security Transfer Registrars Pty Ltd 770 Canning Highway Applecross WA 6153 Telephone: (08) 9315 2333 Facsimile: (08) 9315 2233 Stock Exchange Listing YTC Resources Limited shares are listed on the Australian Stock Exchange, the home branch being Perth ASX Code: YTC Auditors Ernst and Young 11 Mounts Bay Road Perth WA 6000 * Pictures in this report may not represent assets of the Company. CONTENTS REVIEW OF ACTIVITIES....................................................5 DIRECTORS’ REPORT.....................................................18 CORPORATE GOVERNANCE STATEMENT...............................29 INCOME STATEMENT......................................................32 BALANCE SHEET..........................................................33 STATEMENT OF CHANGES IN EQUITY..................................34 CASH FLOW STATEMENT.................................................34 NOTES TO THE FINANCIAL STATEMENTS..............................35 DIRECTORS’ DECLARATION..............................................57 AUDITOR’S INDEPENDENCE -

Weekly Briefing 22Nd - 28Th April 2014

WEEKLY BRIEFING 22ND - 28TH APRIL 2014 IPIS is an independent research institute which focuses on Sub-Saharan Africa. Our studies concern three core themes: arms trade, exploitation of natural resources and corporate social responsibility. This briefing provides a round-up of the week's news and analysis on security, natural resource and CSR issues arising in the Great Lakes region of Africa Content NEWS IN BRIEF News in brief The Ugandan People’s Defence Force, tracking Joseph Kony in the Central African Republic (CAR) reported the capture of Lord’s Resistance Army leader Charles Okello this week. In the IPIS’ Latest Publications CAR around 1,300 Muslims were escorted from Bangui by peacekeepers over the weekend. The event was marked by clashes between French Sangaris forces and armed actors, occasioning at least 7 deaths. This incident was shortly followed by an attack on an MSF Conflict and security hospital in Nanga Bougila, reportedly killing 15 tribal leaders and three MSF workers. The DRC attack is alleged to have been orchestrated by ex-Seleka combatants, an assertion denied by Rwanda the new president of the former coalition. The deputy heads for the pending UN peacekeeping Burundi force for the CAR (MINUSCa) have been named. CAR In Kinshasa, 500 Congolese nationals have arrived following expulsion from the Republic of Humanitarian news Congo. In the East, the Nduma Defense of Congo (NDC) militia has been called upon to DRC disarm after displacing thousands in Lubero, North Kivu. In Province Oriental, South Sudanese soldiers are accused of killing two students and 30 cattle in Dungu territory and naval forces Burundi are said to be committing abuses against the population of Basoko. -

Organized Crime and Instability in Central Africa

Organized Crime and Instability in Central Africa: A Threat Assessment Vienna International Centre, PO Box 500, 1400 Vienna, Austria Tel: +(43) (1) 26060-0, Fax: +(43) (1) 26060-5866, www.unodc.org OrgAnIzed CrIme And Instability In CenTrAl AFrica A Threat Assessment United Nations publication printed in Slovenia October 2011 – 750 October 2011 UNITED NATIONS OFFICE ON DRUGS AND CRIME Vienna Organized Crime and Instability in Central Africa A Threat Assessment Copyright © 2011, United Nations Office on Drugs and Crime (UNODC). Acknowledgements This study was undertaken by the UNODC Studies and Threat Analysis Section (STAS), Division for Policy Analysis and Public Affairs (DPA). Researchers Ted Leggett (lead researcher, STAS) Jenna Dawson (STAS) Alexander Yearsley (consultant) Graphic design, mapping support and desktop publishing Suzanne Kunnen (STAS) Kristina Kuttnig (STAS) Supervision Sandeep Chawla (Director, DPA) Thibault le Pichon (Chief, STAS) The preparation of this report would not have been possible without the data and information reported by governments to UNODC and other international organizations. UNODC is particularly thankful to govern- ment and law enforcement officials met in the Democratic Republic of the Congo, Rwanda and Uganda while undertaking research. Special thanks go to all the UNODC staff members - at headquarters and field offices - who reviewed various sections of this report. The research team also gratefully acknowledges the information, advice and comments provided by a range of officials and experts, including those from the United Nations Group of Experts on the Democratic Republic of the Congo, MONUSCO (including the UN Police and JMAC), IPIS, Small Arms Survey, Partnership Africa Canada, the Polé Institute, ITRI and many others. -

The Mineral Industry of China in 2016

2016 Minerals Yearbook CHINA [ADVANCE RELEASE] U.S. Department of the Interior December 2018 U.S. Geological Survey The Mineral Industry of China By Sean Xun In China, unprecedented economic growth since the late of the country’s total nonagricultural employment. In 2016, 20th century had resulted in large increases in the country’s the total investment in fixed assets (excluding that by rural production of and demand for mineral commodities. These households; see reference at the end of the paragraph for a changes were dominating factors in the development of the detailed definition) was $8.78 trillion, of which $2.72 trillion global mineral industry during the past two decades. In more was invested in the manufacturing sector and $149 billion was recent years, owing to the country’s economic slowdown invested in the mining sector (National Bureau of Statistics of and to stricter environmental regulations in place by the China, 2017b, sec. 3–1, 3–3, 3–6, 4–5, 10–6). Government since late 2012, the mineral industry in China had In 2016, the foreign direct investment (FDI) actually used faced some challenges, such as underutilization of production in China was $126 billion, which was the same as in 2015. capacity, slow demand growth, and low profitability. To In 2016, about 0.08% of the FDI was directed to the mining address these challenges, the Government had implemented sector compared with 0.2% in 2015, and 27% was directed to policies of capacity control (to restrict the addition of new the manufacturing sector compared with 31% in 2015. -

2020 Conflict Minerals Report

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM SD Specialized Disclosure Report O-I GLASS, INC. (Exact name of registrant as specified in its charter) Delaware 1-9576 22-2781933 (State or other jurisdiction of (Commission (IRS Employer incorporation or organization) file number) Identification No.) One Michael Owens Way, Perrysburg, Ohio 43551 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code: (567) 336-5000 Mary Beth Wilkinson (567) 336-5000 (Name and telephone number, including area code, of the person to contact in connection with this report.) Check the appropriate box to indicate the rule pursuant to which this form is being filed, and provide the period to which the information in this form applies: ☒ Rule 13p-1 under the Securities Exchange Act (17 CFR 240.13p-1) for the reporting period from January 1 to December 31, 2019. Section 1 - Conflict Minerals Disclosure Item 1.01 Conflict Minerals Disclosure and Report A copy of the Conflict Minerals Report for O-I Glass, Inc. (the “Company”) is provided as Exhibit 1.01 hereto and is publicly available at www.o-i.com. The term “Company,” as used herein and unless otherwise stated or indicated by context, refers to Owens-Illinois, Inc. and its affiliates (“O-I”) prior to the Corporate Modernization (as defined below) and to O-I Glass, Inc. and its affiliates (“O-I Glass”) after the Corporate Modernization. On December 26 and 27, 2019, the Company implemented the Corporate Modernization (“Corporate Modernization”), whereby O-I Glass became the new parent entity with Owens-Illinois Group, Inc. -

The Collapse of the International Tin Agreement

CORE Metadata, citation and similar papers at core.ac.uk Provided by IDS OpenDocs The Collapse of the International Tin Agreement Michael Prest Introduction unimportant part of an international dispute which it Early on the morning of 24 October 1985 Michael only dimly understood. The field was quickly Brown,chiefexecutiveof the London Metal dominated by national governments, big banks, and in Exchange, was sitting in his office chatting to the the background the United Nations Conference on chairman of the exchange's committee, Ted Jordan. Trade and Development. The telephone range. It was Pieter de Koning, the International Tin Council's buffer stock manager and For the LME the issues were the sanctity of contract the most powerful person in the world tin market. and the preservation of the exchange. But for the other There was a brief conversation. Brown recalls:'I participants it was a matter of realpolitik, in which the turned to Ted and said "de Koning has suspended stakes were the future of international commodity trading".' agreements, the debt crisis, and relations between developing commodity producing countries and In that instant both realised that chaos threatened. industrial consumers of commodities. What originated Their immediate concern was the LME and its as a commercial dispute - the announcement by the members. They knew that around half of the LME's 27 ITC that it could not pay its debts - rapidly ring dealing members' were heavily involved with the intensified and expanded into a test case of the ability buffer stock. They also suspected that de Koning's of commodity agreements to survive in adverse careful word 'suspend' was code for defaulting on his market conditions. -

DR Congo 2015 Update

Analysis of the interactive map of artisanal mining areas in eastern DR Congo 2015 update International Peace Information Service (IPIS) 1 Editorial Analysis of the interactive map of artisanal mining areas in eastern DR Congo: 2015 update Antwerp, October 2016 Front Cover image: Cassiterite mine Malemba-Nkulu, Katanga (IPIS 2015) Authors: Yannick Weyns, Lotte Hoex & Ken Matthysen International Peace Information Service (IPIS) is an independent research institute, providing governmental and non-governmental actors with information and analysis to build sustainable peace and development in Sub-Saharan Africa. The research is centred around four programmes: Natural Resources, Business & Human Rights, Arms Trade & Security, and Conflict Mapping. Map and database: Filip Hilgert, Alexandre Jaillon, Manuel Claeys Bouuaert & Stef Verheijen The 2015 mapping of artisanal mining sites in eastern DRC was funded by the International Organization of Migration (IOM) and PROMINES. The execution of the mapping project was a collaboration between IPIS and the Congolese Mining Register (Cadastre Minier, CAMI). The analysis of the map was funded by the Belgian Development Cooperation (DGD). The content of this publication is the sole responsibility of IPIS and can in no way be taken to reflect the views of IOM, PROMINES, CAMI or the Belgian government. 2 Table of contents Editorial ............................................................................................................................................... 2 Executive summary ............................................................................................................................. -

Download Article

Advances in Economics, Business and Management Research, volume 42 Second International Symposium on Business Corporation and Development in South-East and South Asia under B&R Initiative (ISBCD 2017) Entrepreneurship in the Transformation of Yunnan 's Modern Industrialization Yang Haibin* Guo Yuanqin Department of Economics of International Business School Yunnan University of Finance and Economics Department of Economics of International Business School Kunming, China Yunnan University of Finance and Economics [email protected] Kunming, China [email protected] Abstract—Modern industrial development in Yunnan is very and steel. At this time the form of industry is also mainly in rapid period, although it is affected by geographical factors and the form of government and government officials to do political factors, but its industry in the southwest region and even business, mainly concentrated in the mining industry. China's in the whole of China is still made a larger development, is an modern industrial system and the start of modern private important emerging modern industrial power. Through the study enterprises is the formation of the basic form of this period. of modern industrial transformation in Yunnan, this paper found The second stage is in the Sino-Japanese war, The signing of that entrepreneur and entrepreneurial spirit has a very crucial the Treaty of Shimonoseki makes China's economic resources role. Through the entrepreneurial innovation behavior and further looted and controlled by foreign countries. Despite the industrial development of mutual benefit and mutual catalysis, frequent warfare at this time, the economy is struggling, but entrepreneurial spirit of Yunnan's modern industrial the capital investment of modern Chinese industry still transformation has played an important role in promoting. -

Walikale Nicholas Garrett Artisanal Cassiterite Mining and Trade in North Kivu June 1, 2008 Implications for Poverty Reduction and Security

Walikale Nicholas Garrett Artisanal Cassiterite Mining and Trade in North Kivu June 1, 2008 Implications for Poverty Reduction and Security 1 ACKNOWLEDGEMENTS This report was prepared by Nicholas Garrett for the Communities and Artisanal & Small-scale Mining initiative (CASM). Nicholas Garrett is a Mining Consultant from the UK Resource Consulting Services Ltd (RSS), and specialising in conflict and post-conflict minerals management and corporate social responsibility in high-risk environments. The contribution of Estelle A. Levin and Harrison Mitchell (RSS) and of those who have reviewed the final report is acknowledged, as well as to everyone who provided support to the author to conduct extensive research on the ground in the DR Congo. Front cover photo: Artisanal cassiterite mining in Bisie, North Kivu/DRC © Nicholas Garrett Disclaimer: The views expressed in this report are those of the author and do not necessarily reflect those of CASM or other organizations. 2 CONTENTS List of Acronyms 5 Sections Preface and Methodology 6 Synopsis 7 Background and Context 12 Legal Framework 18 Governance 23 Geography, Physical Access, Infrastructure and Transport 32 Structure of Production 37 Economics of Production 41 Economics of Trade 43 Payments to Authorities 56 Demography and Poverty 63 External Stakeholders and Development Assistance 62 Conclusion and Recommendations 76 Bibliography 87 Fact Boxes Box 1: What is Cassiterite? 13 Box 2: Key Features of Artisanal Mining (AM) in North Kivu 16 Box 3: SAESSCAM 22 Box 4: Workers’ Income in Bisie -

SPANISH CEPAL Economic Commission

Distr. RESTRICTED E/CEPAL/R.249 1H January 1932 ENGLISH ORIGINAL: SPANISH C E P A L Economic Commission for Latin America LINKS OF THE TRANSNATIONAL CORPORATIONS WITH THE TIN INDUSTRY IN BOLIVIA Jan Kfiakal */ jV The author is a regional expert of the CEPAL/CTC Joint Unit on Transnational Corporations. The views expressed in this working paper are those of the author and do not necessarily reflect the views of the Organization. 81-9-2017 - 1X• • 1» - CONTENTS Page Introduction . i Part One THE INTERNATIONAL TIN INDUSTRY 5 1. Characteristics of the product 5 2. Tin mining and reserves 7 3. Sovereignty of the developing countries over their tin resources 10 4. Tin smelting and position of the main transnational corporations 15 5. Control over the world tin market 20 Part Two THE BOLIVIAN TIN INDUSTRY AND ITS LINKS WITH TRANSNATIONAL CORPORATIONS 29 1. The importance of mining and tin in the Bolivian economy 29 2. Early stage of the industry and its nationalization in 1952 . 31 3. Establishment of the Corporación Minera de Bolivia and the* postnationalization period 34 4. Continued dependence on foreign smelters 36 5. Importance of the public enterprise in tin smelting 42 6. Domestic integration of the mining and metallurgical sector (COMIBOL and ENAF) and reaction of the foreign smelters 44 7. Marketing of metal tin by ENAF 57 8. Industrialization based on tin: its limits and possibilities for increased regional co-operation 64 9. Conclusions to be drawn from the Bolivian experience 71 Annex 1 Selected Bibliography 77 Annex 2 Main clauses and technical specifications included in ENAF's tin marketing contracts 79 Annex 3 Contract between ENAF and an international sales agent . -

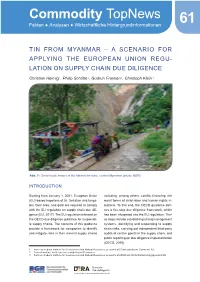

Tin from Myanmar – a Scenario for Applying the European Union Regu- Lation on Supply Chain Due Diligence

Commodity TopNews Fakten ● Analysen ● Wirtschaftliche Hintergrundinformationen 61 TIN FROM MYANMAR – A SCENARIO FOR APPLYING THE EUROPEAN UNION REGU- LATION ON SUPPLY CHAIN DUE DILIGENCE Christian Heimig 1, Philip Schütte 2, Gudrun Franken 2, Christoph Klein 3 Abb. 1:: Small-scale miners at the Mawchi tin mine, central Myanmar (photo: BGR). INTRODUCTION Starting from January 1, 2021, European Union including, among others, conflict financing, the (EU)-based importers of tin, tantalum and tungs- worst forms of child labor and human rights vi- ten, their ores, and gold are required to comply olations. To this end, the OECD guidance defi- with the EU regulation on supply chain due dili- nes a five-step due diligence framework, which gence (EU, 2017). The EU regulation is based on has been integrated into the EU regulation. The- the OECD due diligence guidance for responsib- se steps include establishing strong management le supply chains. The contents of this guidance systems, identifying and responding to supply provide a framework for companies to identify chain risks, carrying out independent third-party and mitigate risks in their mineral supply chains audits at certain points in the supply chain, and public reporting on due diligence implementation (OECD, 2016). 1 Formerly Federal Institute for Geosciences and Natural Resources, presently at Südwestdeutsche Salzwerke AG 2 Federal Institute for Geosciences and Natural Resources 3 Formerly Federal Institute for Geosciences and Natural Resources, presently at KPMG AG Wirtschaftsprüfungsgesellschaft 2 Commodity TopNews The US Dodd-Frank Act, enacted in 2010, al- oned experts to develop an indicative global list ready defines certain sourcing requirements for of such areas, companies remain responsible for so-called conflict minerals. -

2020 Report on Global Tin Resources & Reserves

Global Resources & Reserves Security of long-term Ɵ n supply 2020 Update Contents Global Resources and Reserves .......................................................................................................... 3 Summary ............................................................................................................................................. 3 The Risk: Critical Materials .................................................................................................................. 3 Resources and Reserves ...................................................................................................................... 4 Tin resources and reserves calculation ........................................................................................... 5 ITA’s estimate of global tin resources and reserves ....................................................................... 6 Resources and Reserves by Region ..................................................................................................... 8 North America ................................................................................................................................. 8 South America ................................................................................................................................. 9 Africa ............................................................................................................................................. 10 Europe ..........................................................................................................................................