Small Car Segment Dominates Europe's Biggest Markets 16.11.2007

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cross-Country Comparison of Substitution Patterns in the European Car Market

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Research Papers in Economics Cross-country comparison of substitution patterns in the European car market Paper submitted to obtain the degree of Master of Advanced Studies in Economics Faculty of Business and Economics K.U. Leuven, Belgium Supervisor: Frank Verboven. Discussant: Patrick Van Cayseele Candidate: Victoria Oliinik January 2007 Abstract AIMS. Using recent data on sales, prices and product characteris- tics of new passenger vehicles sold in Europe’s seven largest markets during years 2000 through 2005, I estimate a demand function us- ing two approaches to the differentiated product demand estimation: the Logit and the Nested Logit. For the Nested Logit model, I use nests that roughly correspond to segmentation used in the automo- bile industry. I then compare substitution patterns resulting from Logit and Nested Logit specifications across countries and segments. FINDINGS. Regression outcomes demonstrate strong evidence of seg- mentation. Consumer preferences are strongly correlated for the most basic as well as for the luxury and sports segments, whereas core seg- ments display more heterogeneity. While car size preference varies across countries, Europeans typically like high and wide cars and dis- like long cars. Engine performance appreciation appears to have a curved shape: consumers are willing to pay for a fast car but at a de- creasing rate. Compared to their neighbors, Germans shop the most for premium brands yet display strongest price sensitivity, whereas most concerned about fuel consumption are the Brits. Aside from a few exceptions, all elasticities are within expected range, substitu- tion patterns vary mainly across segments but follow a similar pattern across countries. -

2017 CADILLAC ATS-V: the Smallest and Lightest V-Series Sedan and Coupe Ever Receive Technology Enhancements and an Available Carbon Black Sport Package

2017 CADILLAC ATS-V: the smallest and lightest V-Series sedan and coupe ever receive technology enhancements and an available Carbon Black sport package New for 2017 • AVAILABLE CARBON BLACK SPORT PACKAGE • CADILLAC CUE ENHANCEMENTS INCLUDING TEEN DRIVER AND COLLECTION The first-generation Cadillac ATS-V introduced class-leading twin-turbocharged performance and a comprehensive suite of design and performance systems to the lightest and smallest V- Series Sedans and Coupe models ever. The 2017 Cadillac ATS-V adds a Carbon Black sport package and upgrades and enhancements for the Cadillac CUE infotainment system improving the ATS-V’s superior connectivity. The enhanced Cadillac CUE includes new standard technologies such as the myCadillac Mobile App, Teen Driver and Cadillac Collection. Since its inception in 2004, Cadillac’s V-Series performance family has driven remarkable power and performance capability into the brand’s growing luxury car range. Building on the strengths of the award-winning Cadillac ATS product line, V-Series adds impressive track capability to what was already the lightest and most agile-driving car in the luxury compact class. The result is a dual-purpose luxury performer – a car with true track capability right from the factory that is also a sophisticated luxury car on the road. Key features include: • The Cadillac Twin Turbo V-6 engine mated to a standard six-speed manual transmission or paddle-shift eight-speed automatic transmission • Standard carbon fiber hood and available carbon fiber package, including -

Kia Ceed Sw Owners Manual

Kia Ceed Sw Owners Manual KIA CEED SW 2010 OWNERS MANUAL - Manual Unlimited Kia Ceed Sw 2010 Owners Manual Manual Unlimited with 2010 kia ceed, 2010 kia ceed and 2010 kia ceed http://www.meetar.com/kia-ceed-sw-2010-owners-manual-manual-unlimited/ Kia Ceed Sw Service Manual KIA CEED SW MANUAL PDF Title: KIA CEED SW MANUAL PDF Author: Manuals Online Subject: KIA CEED SW MANUAL PDF Keywords: Get access to PDF Ebook Kia Ceed Sw Manual. http://pdf276.sivoh.com/kia-ceed-sw-service-manual-atkthvs.pdf kia ceed repair manual pdf download | PDF Owner Jun 07, 2012 Kia Ceed Repair Manual Pdf Download in pdf that we indexed in Manual Guide. This manual books file was hosted in www.kia.com that avaialble for FREE http://www.abcccodes.com/kia-ceed-repair-manual-pdf-download/ Kia Ceed SW (2013) - NetCarShow.com The Kia Ceed SW has been one of Kia's leading download from the owner's mobile telephone. The Kia cee'd manual versions of the cee'd Sportswagon http://www.netcarshow.com/kia/2013-ceed_sw/ KIA CEED SW MANUAL | Free PDF Owner Guide KIA CEED SW MANUAL PDF Ebook Library KIA CEED SW MANUAL Are you looking for Kia Ceed Sw Manual? Here is Kia Ceed Sw Manual you have to read before http://www.bookdocs.xyz/view-pdfguide/kia-ceed-sw-manual-3663/ Kia Cee'd hatchback owner reviews: MPG, problems, Kia Cee'd hatchback 14,805 Service costs through Kia dealers is expensive but they don't all (like new range rover sport) and i'm just as happy in my ceed http://www.carbuyer.co.uk/reviews/kia/ceed/hatchback/owner-reviews Kia cee'd - Live more life! | Kia Motors Smart Parking Assist System * Only in cee'd. -

The Origins of the SUV

The origins of the SUV IFTY YEARS AGO, farmers, soldiers, hunt- Fers and the odd explorer drove four-wheel drives. Four-wheel drives were listed in most car guides as commercial vehicles, along with pickup trucks and goods vans. The sight of a four-wheel drive on main street simply meant that a farmer had come to town for the day. Three events changed all that. 1 Uncredited images are believed to be in the public domain. Credited images are copyright their respective owners. All other contentAll © content The Dog © &dogandlemon.com Lemon Guide 2016 2016 • All rights reserved In 1963, Jeep produced a vehicle called the Wagoneer. It looked like a family station wagon with fake wooden panelling. However, the Wag- oneer shared most of its DNA with the Jeep Gladiator pickup truck. As such, four-wheel drive versions of the Wagoneer were both tough and capable offroad. A few people have claimed that the Wagoneer was the first modern SUV, although none of these people appear to have actually driven one: the ride is rattly, boneshakingly hard and the handling crudely boat-like. The Wagoneer was also rather poorly built. However, the Wagoneer was gradually im- proved and lasted, amazingly, until 1991. 2 All content © dogandlemon.com 2016 The 1970 Range Rover is a more likely candi- date for the first modern SUV. It was designed from scratch, as a vehicle for Britain’s upper classes. Range Rover owners could effortlessly tow their horse floats up muddy roads while they rode up front in semi-luxury. When Range Rover owners returned to their mansions, their servants could clean out the interior with a hose (carpets weren’t fitted to early models). -

8EMEKRD*Ajicfc+ Akebono

LISTA DE APLICACIONES - BUYERS GUIDE 181906 181906 90R-01111/2567 8EMEKRD*ajicfc+ Akebono Qty: 300 Weight: 1.555 136.4x56.4x15.9 O.E.M. MAKE 45022-SZT-G00 HONDA 45022-SZY-T00 HONDA WVA FMSI 45022-T5R-A01 HONDA 24979 D1394-8502 45022-T5R-A50 HONDA 24980 D1783-8502 45022-T9A-T00 HONDA 24981 45022-TAR-G00 HONDA 25672 45022-TF0-G00 HONDA 25673 45022-TF0-G01 HONDA MAKE 45022-TF0-G02 HONDA HONDA 45022-TG0-T00 HONDA HONDA (DONGFENG) 45022-TK6-A00 HONDA HONDA (GAC) 45022-TM8-G00 HONDA 45022-TZB-G00 HONDA Trac. CC Kw CV Front / Rear HONDA CITY V / BALADE (GM2, GM3) 09.08- Saloon (Supermini car-B Segment) 1.4 i-V TEC (L13Z1) Gasolina FWD 1339 73 99 09.08- ■ 1.5 i-VTEC (GM2) (L15A7) Gasolina FWD 1497 88 120 02.09- ■ CITY VI / BALLADE / GREIZ / GIENIA (GM4, GM5, GM6, GM9, GM7) 07.13- Saloon (Supermini car-B Segment) 1.5 CNG Gasolina FWD 1497 75 102 01.14- ■ 1.5 i-VTEC (L15A7) Gasolina FWD 1497 88 119 01.14- ■ 1.5 i-VTEC (L15Z1) Gasolina FWD 1497 88 119 01.14- ■ 1.5 i-DTEC (N15A1) Diesel FWD 1498 74 100 01.14- ■ CR-Z (ZF) 06.10- Coupe (Compact car-C Segment) 1.5 IMA (ZF1) (LEA1) Gasol./el FWD 1497 84 114 06.10- ■ éc. 1.5 IMA (LEA1) Gasol./el FWD 1497 89 121 11.12- ■ éc. 1.5 IMA (LEA3) Gasol./el FWD 1497 89 121 11.12- ■ éc. 1.5 IMA (LEA1) Gasol./el FWD 1497 91 124 09.10-12.13 ■ éc. -

![SUZUKI GOES Off [ROAD]!](https://docslib.b-cdn.net/cover/8806/suzuki-goes-off-road-488806.webp)

SUZUKI GOES Off [ROAD]!

SUZUKI AUTUMN 2007 AUTUMN NOW SX4 GOES OFF [ROAD]! CONGRATULATIONS CAMERON GIRLS’ DAY OUT EVENT SWIFT toPS AWards again FUNKY NEW JIMNY ltd 2 NEW dealersHIPS OPEN vitara DRIVE day NEAR YOU cover STORY More than just ‘a pretty face’ Motoring journalists around the country are raving about Suzuki’s newest kid on the block – the SX4. 2 “ThIS IS ONE HELL OF A GOOD LOOKING experience to the next level. This feature CAR. It has enough real 4WD cues in the particularly impressed motoring journalist styling to satisfy the macho image, but Rob Maetzig ‘…when road conditions get … combines a sedan look so it is also tight or unsealed, it is a breeze to flick into stylish. On looks alone, this is going to the automatic or locked AWD modes which be another winner for Suzuki. But there make the driving sensation even more is more to the SX4 than a pretty face.” secure. That’s what makes the new SX4 NZ Driver Magazine. something rather special’ Indeed, there is plenty of substance behind Forty-five leading motoring journalists from this very good-looking exterior. around the world also agree that the SX4 is rather special – as they have selected it The SX4 is offered standard with 4WD and as one of the top ten finalists in the 2007 a 2-litre petrol engine – similar to the World Car of the Year award. It is one of one in the Grand Vitara. There is a choice only two Japanese cars in the top ten – the of 5-speed manual transmission and an other is the Lexus LS 460. -

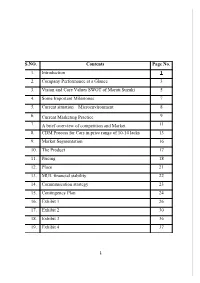

S.NO. Contents Page No. 1. Introduction 1 2. Company Performance at a Glance 3 3. Vision and Core Values SWOT of Maruti Suzuki 5 4

S.NO. Contents Page No. 1. Introduction 1 2. Company Performance at a Glance 3 3. Vision and Core Values SWOT of Maruti Suzuki 5 4. Some Important Milestones 7 5. Current situation – Microenvironment 8 6. Current Marketing Practice 9 7. A brief overview of competition and Market 11 8. CDM Process for Cars in price range of 10-14 lacks 13 9. Market Segmentation 16 10. The Product 17 11. Pricing 18 12. Place 21 13. MUL financial stability 22 14. Communication strategy 23 15. Contingency Plan 24 16. Exhibit 1 26 17. Exhibit 2 30 18. Exhibit 3 36 19. Exhibit 4 37 1 1. I NTRODUCTION Maruti Suzuki India Ltd. – Company Profile Maruti Suzuki India Ltd. (current logo) Maruti Udyog Ltd. (old logo) Maruti Suzuki is one of the leading automobile manufacturers of India, and is the leader in the car segment both in terms of volume of vehicle sold and revenue earned. It was established in February, 1981 as Maruti Udyog Ltd. (MUL), but actual production started in 1983 with the Maruti 800 (based on the Suzuki Alto kei car of Japan), which was the only modern car available in India at that time. Previously, the Government of India held a 18.28% stake in the company, and 54.2% was held by Suzuki of Japan. However, in June 2003, the Government of India held an initial public offering of 25%. By May 10, 2007 sold off its complete share to Indian financial institutions. Through 2004, Maruti Suzuki has produced over 5 million cars. Now, the company annually exports more than 50,000 cars and has an extremely large domestic market in India selling over 730,000 cars annually. -

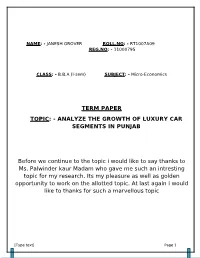

Analyze the Growth of Luxury Car Segments in Punjab

NAME: - JANESH GROVER ROLL.NO: - RT1007A09 REG.NO: - 11000795 CLASS: - B.B.A (I-sem) SUBJECT: - Micro-Economics TERM PAPER TOPIC: - ANALYZE THE GROWTH OF LUXURY CAR SEGMENTS IN PUNJAB Before we continue to the topic i would like to say thanks to Ms. Palwinder kaur Madam who gave me such an intresting topic for my research. Its my pleasure as well as golden opportunity to work on the allotted topic. At last again i would like to thanks for such a marvellous topic [Type text] Page 1 Contents Acknowledgment................................................................................................................ .................................1 Introduction........................................................................................................................ ..............................1-2 How segmentation is done?..............................................................................................................................2- 6 PUNJAB THE SUCCESSFULL PURVEYOR FOR LUXURY CARS IN INDIA...................................................................6 PUNJAB MATERIALIZE AS A NEW BAZAAR FOR CARS.......................................................................................6-8 List of luxury Cars in Punjab............................................................................................................................8- 11 Rush for Luxury cars..................................................................................................................................... .11-12 Luxury -

The Road to World Car

THE ROAD TO WORLD CAR OCTOBER 2018 INTRODUCTION PETER LYON - CO-CHAIRMAN, WORLD CAR AWARDS PROGRAM World Car Awards jurors at the Paris Auto Show Bonjour from the French capital. On October 2nd at in this year’s World Luxury Car award category. And thirdly, the Paris Auto Show inside the Audi stand, World Car WCA took advantage of the opportunity to officially launch commemorated several major milestones. its 2018-2019 evaluation season. Firstly, we celebrated the 15th anniversary of the Attended by over 150 media and industry types, WCA establishment of the World Car Awards, a non-profit program co-chairs Peter Lyon and Mike Rutherford shared organisation that has grown to become the world’s No 1 duties welcoming special guests, celebrating Audi’s program of its type in terms of media reach. record-breaking achievement and launching the Road To World Car journey which culminates in the Big Apple in April Secondly, WCA applauded the record-breaking nine trophy 2019 on the first press day of the New York International wins by Audi over those 15 years, including the A8’s victory Auto Show. THE ROAD TO WORLD CAR TAKES MANY PATHS In Geneva this year, WCA presented its first-ever World Car Person of the Year award to Volvo CEO Hakan Samuelsson for his outstanding leadership of the Swedish carmaker’s transformation. As of October, the WCA steering committee has already started the process of selecting finalists for the 2019 World Car Person of the Year when the winner will be announced next spring. World Car has a dual mission of celebrating the best of Audi France CEO, Lahouari Bennaoum, speaking in Paris today and inspiring the best ideas for tomorrow. -

Peugeot 207 the 207 Setting a New Standard

PEUGEOT 207 THE 207 SETTING A NEW STANDARD TODAy’s TECHNOLOGIES ARE TRANS FORMING OUR WORLD. AND WITH ITS SIMPLE LINES, AVANT-GARDE LOOKS AND DYNAMIC DESIGN, THE 207 IS THE PERFECT EXPRESSION OF THIS TRANSFORMATION. The 207’s lively character is clearly visible in the taut lines of its plun ging bonnet, its new, even more elegant front end and LED rear lights.* Its feline appearance gives it a balance and poise that suggests power, strength and robustness – even when the car is at a standstill. And from the moment you take to the wheel, your first impressions of the 207 will be confirmed. You’ll immediately notice the benefit of its advanced economic petrol or HDi diesel engines, the high level of comfort throughout the interior, and the sophistication of the equipment designed for your enjoyment and your safety. In the 207, you will see the world differently. *Available on the 207 hatch. 3 207 TOURING DESIGNED FOR ADVENTURE THE 207 TOURING IS THE IDEAL CAR FOR THOSE IN SEARCH OF NEW EXPERIENCES. IT IS PARTICULARLY WELL SUITED TO ADVENTURERS OR SPORTS ENTHUSIASTS IN NEED OF A VERSATILE CAR. Its robust appearance is enhanced by a raised ride height along with SUV-style wheel arch extensions and sill panels – underlining its spirit of adventure. 207 TOURING designed FOR adVentUre With its increased effective space, exceptional ambience and superior The 207 Touring’s rear more than hints at its impressive volume and practicality, the 207 Touring stands out from its rivals. robust design. The attention given to the lights and tailgate confirm its sporty and spirited nature. -

The Popularity of the Light Car in 21St-Century Europe

The popularity of the light car in 21st-century Europe By light cars I mean supermini cars, mini or small multipurpose vehicles, mini or small sport utility vehicles and City or minicar’s. In the United Kingdom today we seem to be overwhelmed with even larger Sport utility vehicles ,fancy trucks, and large German saloon cars, This led me to think about at what proportion are the various classes of vehicles on the road in the UK today. I was unable to obtain the data I was looking for the UK but was able to find a couple of sites that were able to furnish me with Data for Europe. One of them was carsalesbase.com which gave me the individual registration totals of cars in Europe for the last 20 years. Another site that gave me total for all passenger cars each year was the European automobile manufacturers association site the ACCO, and between those I was able to compose a simple list of all the classes of cars registered in Europe for the years 2015. Also I was able to produce detailed lists of the various light cars types for the last twenty years. Passenger car registrations in Europe for the period 1997 to 2016 amounted to two hundred and eighty-two million. The total number passenger cars registered in Europe in 2015 was almost thirteen point two million. The various size cars registered is as follows. Large cars 6%, Midsize cars 26%, Compact cars 25% and light or small cars 43% . The light car total is composed of the following. -

No. Parte Descripción Cantidad 043916 GRANDE PUNTO ABARTH

No. Parte Descripción Cantidad 043916 GRANDE PUNTO ABARTH PROYECTO 1 115804 EVAPORADOR AIRE ACONDICIONAD 3 178400 PLUMA LIMPIAPARABRISAS TRAD 29 178401 PLUMA LIMPIAPARABRISAS TRADI 20 178402 PLUMA LIMPIAPARABRISAS TRADI 44 178403 PLUMA LIMPIAPARABRISAS TRAD 40 178404 PLUMA LIMPIAPARABRISAS TRADI 32 178405 PLUMA LIMPIAPARABRISAS TRADI 38 178406 PLUMA LIMPIAPARABRISAS TRADI 11 178407 PLUMA LIMPIAPARABRISAS TRADI 16 178408 PLUMA LIMPIAPARABRISAS TRAD 25 178409 PLUMA LIMPIAPARABRISAS TRADI 19 178410 PLUMA LIMPIAPARABRISAS TRADI 37 178411 PLUMA LIMPIAPARABRISAS TRADI 19 178412 PLUMA LIMPIAPARABRISAS TRAD 18 178413 PLUMA LIMPIAPARABRISAS TRADI 21 178414 PLUMA LIMPIAPARABRISAS TRADI 7 178415 PLUMA LIMPIAPARABRISAS TRADI 54 178420 PLUMA LIMPIAPARABRISAS BEAM 28 178421 PLUMA LIMPIAPARABRISAS BEAM 8 178422 PLUMA LIMPIAPARABRISAS BEAM 7 178423 PLUMA LIMPIAPARABRISAS BEAM 16 178424 PLUMA VALEO LIMPIAPABRISAS 2 30 178425 PLUMA LIMPIAPARABRISAS BEAM 27 178426 PLUMA LIMPIAPARABRISAS BEAM 30 178427 PLUMA LIMPIAPARABRISAS BEAM 9 178428 PLUMA LIMPIAPARABRISAS BEAM 18 178429 PLUMA VALEO LIMPIAPARABRISAS 35 178438 PLUMA LIMP 14OE ULTIMATE BEA 22 178440 Pluma Limpiaparabrisas Beam 15 178441 PLUMA LIMPIAPARABRISAS BEAM 92 178442 PLUMA LIMPIAPARABRISAS BEAM 41 178443 PLUMA LIMPIAPARABRISAS BEAM 30 178444 Pluma Limpiaparabrisas Beam 89 178445 Pluma Limpiaparabrisas Beam 29 178446 PLUMA LIMPIAPARABRISAS BEAM 15 178447 Pluma Limpiaparabrisas Beam 16 178448 PLUMA LIMPIAPARABRISAS BEAM 44 178450 PLUMA LIMPIAPARABRISAS REAR 24 178451 PLUMA LIMPIAPARABRISAS REAR 32