Deriving the Economic Impact of Derivatives

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Commodity Risk Management Techniques & Hedge

9/4/2018 COMMODITY RISK MANAGEMENT TECHNIQUES & HEDGE ACCOUNTING CHANGES September 5, 2018 To Receive CPE Credit • Individuals . Participate in entire webinar . Answer polls when they are provided • Groups . Group leader is the person who registered & logged on to the webinar . Answer polls when they are provided . Complete group attendance form . Group leader sign bottom of form . Submit group attendance form to [email protected] within 24 hours of webinar • If all eligibility requirements are met, each participant will be emailed their CPE certificate within 15 business days of webinar 1 9/4/2018 Bryan Wright Partner | BKD Indianapolis I 317.383.5471 Allen Douglass Regional Director | INTL FCStone Financial, Inc. FCM Division Indianapolis l 317.732.4660 Disclaimer The trading of derivatives such as futures, options, and over-the-counter (OTC) products or “swaps” may not be suitable for all investors. Derivatives trading involves substantial risk of loss, and you should fully understand those risks prior to trading. Past financial results are not necessarily indicative of future performance. All references to futures and options on futures trading are made solely on behalf of the FCM Division of INTL FCStone Financial Inc., a member of the National Futures Association (“NFA”) and registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a futures commission merchant. All references to and discussion of OTC products or swaps are made solely on behalf of INTL FCStone Markets, LLC (“IFM”), a member of the NFA and provisionally registered with the CFTC as a swap dealer. IFM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of IFM. -

Three Essays in Commodity Risk Management

THREE ESSAYS IN COMMODITY RISK MANAGEMENT by Phat Vinh Luong A Dissertation Submitted To The Graduate School Of Business Of Rutgers, The State University of New Jersey In Partial Fulfillment Of The Requirements For The Degree Of Doctor Of Philosophy Written under the direction of Ben Sopranzetti (Principal Adviser) And approved by Xiaowei Xu Bruce Mizrach Weiwei Chen Newark, NJ. May 2018 © Copyright by Phat Vinh Luong 2018 All Rights Reserved Abstract This thesis includes three essays. These essays focus on the commodity market and cover a wide range of topics. Their topics range from the roles of inventory, pricing strategies to impacts of government policies on the commodity market. The first essay provides an analytical framework to distinguish the roles of inventory by investigating their behaviors in a frequency domain. If inventory was used as a buffer for demand shocks, then the stock level should decrease at all frequencies under both the production smoothing and the stockout avoidance strategies. The inventory investment is negative at all frequencies under the stockout avoidance strategy while it is negative at high frequencies (short-term) and is positive at low frequencies (long-term). On the other hand, if inventory is used as a speculative tool, then its level and the inventory investment should increase with the increases in demand and prices at all frequencies. The volatilities of inventory investment also reveal the roles of inventory. Under production smoothing theory, inventory investment is as volatile as the demand at all frequencies while it is as volatile as the output if growth is persistent but less volatile than output if growth is not persistent. -

Factor-Based Commodity Investing

Factor-Based Commodity Investing January 2018 Athanasios Sakkas Assistant Professor in Finance, Southampton Business School, University of Southampton Nikolaos Tessaromatis Professor of Finance, EDHEC Business School, EDHEC-Risk Institute JEL Classification: G10, G11, G12, G23 Keywords: Commodities; Factor Premia; Momentum; Basis, Basis-Momentum, Variance Timing, Commodity Return Predictability EDHEC is one of the top five business schools in France. Its reputation is built on the high quality of its faculty and the privileged relationship with professionals that the school has cultivated since its establishment in 1906. EDHEC Business School has decided to draw on its extensive knowledge of the professional environment and has therefore focused its research on themes that satisfy the needs of professionals. EDHEC pursues an active research policy in the field of finance. EDHEC-Risk Institute carries out numerous research programmes in the areas of asset allocation and risk management in both the 2 traditional and alternative investment universes. Copyright © 2018 EDHEC Abstract A multi-factor commodity portfolio combining the high momentum, low basis and high basis- momentum commodity factor portfolios significantly, economically and statistically outperforms, widely used commodity benchmarks. We find evidence that a variance timing strategy applied to commodity factor portfolios improves the return to risk trade-off of unmanaged commodity portfolios. In contrast, dynamic commodities strategies based on commodity return prediction models provide little value added once variance timing has been applied to commodity portfolios. 1. Introduction There is growing evidence that commodity prices can be explained by a small number of priced commodity factors. Commodity portfolios exposed to commodity factors earn significant risk premiums, in addition to the premium offered by a broadly diversified commodity index. -

Agricultural Commodity Risk Management

Agricultural Commodity Risk Management: Policy Options and Practical Instruments with Emphasis on the Tea Economy Alexander Sarris Director, Trade and Markets Division, FAO Presentation at the Intergovernmental Group of Tea, nineteenth session, Delhi India, May 12, 2010 Outline of presentation • Background and motivation • Risks faced by rural households • Risks in the tea economy • Agricultural productivity and credit • Constraints to expanding intermediate input use in agriculture • The demand for commodity price insurance • The demand for weather insurance • Operationalizing the use of price and weather insurance • Possibilities for the tea economy Background and motivation: Some major questions relevant to agricultural land productivity and risk • Is agricultural land productivity a factor in growth and poverty reduction? • What are the factors affecting land productivity? Is risk a factor? • Are there inefficiencies in factor use among smallholders? If yes in which markets? Why? • Determinants of intermediate input demand and access to seasonal credit • What are the impacts or risk at various segments of the value chain? Background and Motivation: Uncertainty and Risk • Small (and medium size) agricultural producers face many income and non-income risks • Individual risk management and risk coping strategies maybe detrimental to income growth as they lead to low returns low risk activities. Considerable residual income risk and vulnerability • Is there a demand for additional price and weather related income insurance in light of individual existing risk management strategies? • Can index insurance crowd in credit and how? • Is there a rationale for market based or publicly supported price and weather based safety nets • What are appropriate institutional structures conducive to combining index insurance with credit? Farmer Exposure to Risk. -

Banks As Regulated Traders

Finance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.C. Banks as Regulated Traders Antonio Falato, Diana Iercosan, and Filip Zikes 2019-005 Please cite this paper as: Falato, Antonio, Diana Iercosan, and Filip Zikes (2021). \Banks as Regulated Traders," Finance and Economics Discussion Series 2019-005r1. Washington: Board of Governors of the Federal Reserve System, https://doi.org/10.17016/FEDS.2019.005r1. NOTE: Staff working papers in the Finance and Economics Discussion Series (FEDS) are preliminary materials circulated to stimulate discussion and critical comment. The analysis and conclusions set forth are those of the authors and do not indicate concurrence by other members of the research staff or the Board of Governors. References in publications to the Finance and Economics Discussion Series (other than acknowledgement) should be cleared with the author(s) to protect the tentative character of these papers. Banks as Regulated Traders Antonio Falato Diana Iercosan Filip Zikes∗ July 29, 2021 Abstract Banks use trading as a vehicle to take risk. Using unique high-frequency regulatory data, we estimate the sensitivity of weekly bank trading profits to aggregate equity, fixed-income, credit, currency and commodity risk factors. Our estimates imply that U.S. banks had large trading exposures to equity market risk before the Volcker Rule, which they curtailed afterwards. They also have exposures to credit and currency risk. The results hold up in a quasi-natural experimental design that exploits the phased-in introduction of reporting requirements to address identification. Heterogeneity and placebo tests further corroborate the results. -

307439 Ferdig Master Thesis

Master's Thesis Using Derivatives And Structured Products To Enhance Investment Performance In A Low-Yielding Environment - COPENHAGEN BUSINESS SCHOOL - MSc Finance And Investments Maria Gjelsvik Berg P˚al-AndreasIversen Supervisor: Søren Plesner Date Of Submission: 28.04.2017 Characters (Ink. Space): 189.349 Pages: 114 ABSTRACT This paper provides an investigation of retail investors' possibility to enhance their investment performance in a low-yielding environment by using derivatives. The current low-yielding financial market makes safe investments in traditional vehicles, such as money market funds and safe bonds, close to zero- or even negative-yielding. Some retail investors are therefore in need of alternative investment vehicles that can enhance their performance. By conducting Monte Carlo simulations and difference in mean testing, we test for enhancement in performance for investors using option strategies, relative to investors investing in the S&P 500 index. This paper contributes to previous papers by emphasizing the downside risk and asymmetry in return distributions to a larger extent. We find several option strategies to outperform the benchmark, implying that performance enhancement is achievable by trading derivatives. The result is however strongly dependent on the investors' ability to choose the right option strategy, both in terms of correctly anticipated market movements and the net premium received or paid to enter the strategy. 1 Contents Chapter 1 - Introduction4 Problem Statement................................6 Methodology...................................7 Limitations....................................7 Literature Review.................................8 Structure..................................... 12 Chapter 2 - Theory 14 Low-Yielding Environment............................ 14 How Are People Affected By A Low-Yield Environment?........ 16 Low-Yield Environment's Impact On The Stock Market........ -

National Spot Exchange: Services

National Spot Exchange Operations - its features & benefits’ www.nationalspotexchange.com 1 OVERVIEW OF NATIONAL SPOT EXCHANGE www.nationalspotexchange.com 2 NATIONAL SPOT EXCHANGE – INTRODUCTION Mission Statement: “To develop a pan India, institutionalized, electronic, transparent Common Indian Market offering compulsory delivery based spot contracts in various agricultural and non agricultural commodities, with a view to reduce the cost of intermediation by improving marketing efficiency and thereby improving producers’ realization coupled with reduction in consumer paid price.” PROMOTERS . A National level Electronic Transparent institutionalized spot market. A market place where farmers, traders, corporates, processors and importers can sell and buy at the best possible and competitive rates. Provides counter party guarantee in respect of all trades. Provides services like quality certification, storage of goods and other customized value added services. With the launch of NSEL, the canvass of commodity trading is complete – India has both spot and futures market available on electronic platform with national reach. www.nationalspotexchange.com 3 NSEL’S KEY STAKEHOLDERS . Farmers/Producers: Small and marginal farmers, get a better price for their produce. Commodity Traders/APMC Traders: elimination of credit risk, access to bank finance through NSEL against pledge of warehouse receipts . Corporates/Food processors: Hassle free procurement of farm produce, quality guaranteed by the Exchange, reduces cost of procurement, freedom from counter party defaults; ITC, United Breweries, Jayant Agro, N K Proteins etc. Government Companies: MMTC, PEC, NAFED, HAFED, FCI, Cotton Corporation of India; . Exporters & Importers: Exporters use NSEL platform for procurement; importers to sell. Efficient price discovery and elimination of credit risk. Government: NSEL conducts Minimum Support Price Operation (MSP) OPERATION ON BEHALF OF Government agencies. -

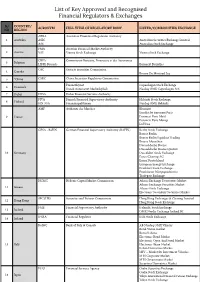

List of Key Approved and Recognised Financial Regulators & Exchanges

List of Key Approved and Recognised Financial Regulators & Exchanges S/ COUNTRY/ ACRONYM FULL TITLE OF REGULATORY BODY LISTED/COMMODITIES EXCHANGE NO REGION APRA Australian Prudential Regulation Authority 1 Australia ASIC Australian Securities Exchange Limited ASE Australian Stock Exchange FMA Austrian Financial Market Authority 2 Austria VSE Vienna Stock Exchange Vienna Stock Exchange CBFA Commission Bancaire, Financiere et des Assurances 3 Belgium LIFFE Brussels Euronext Bruxelles OSC Ontario Securities Commission 4 Canada Bourse De Montreal Inc 5 *China CSRC China Securities Regulatory Commission Finanstilsynet Copenhagen Stock Exchange 6 Denmark Dansk Autoriseret Markedsplads Nasdaq OMX Copenhagen A/S 7 Dubai DFSA Dubai Financial Services Authority FIVA Finnish Financial Supervisory Authority Helsinki Stock Exchange 8 Finland FIN-FSA Finansinspektionen Nasdaq OMX Helsinki AMF Authorite des Marches Bluenext Eurolist by Euronext Paris 9 France Euronext Paris Matif Euronext Paris Monep LCH SA GFSA - BaFIN German Financial Supervisory Authority (BAFIN) Berlin Stock Exchange Boerse Berlin Boerse Berlin Equiduct Trading Boerse Muenchen Duesseldorfer Boerse Duesseldorfer Boerse Quotrix 10 Germany Dusseldorf Stock Exchange Eurex Clearing AG Eurex Deutschland European Energy Exchange Frankfurt Stock Exchange Frankfurter Wertpapierboerse Tradegate Exchange HCMC Hellenic Capital Market Commission Athens Exchange Derivatives Market Athens Exchange Securities Market 11 Greece Athens Stock Exchange Electronic Secondary Securities Market SFC (HK) -

The Behaviour of Small Investors in the Hong Kong Derivatives Markets

Tai-Yuen Hon / Journal of Risk and Financial Management 5(2012) 59-77 The Behaviour of Small Investors in the Hong Kong Derivatives Markets: A factor analysis Tai-Yuen Hona a Department of Economics and Finance, Hong Kong Shue Yan University ABSTRACT This paper investigates the behaviour of small investors in Hong Kong’s derivatives markets. The study period covers the global economic crisis of 2011- 2012, and we focus on small investors’ behaviour during and after the crisis. We attempt to identify and analyse the key factors that capture their behaviour in derivatives markets in Hong Kong. The data were collected from 524 respondents via a questionnaire survey. Exploratory factor analysis was employed to analyse the data, and some interesting findings were obtained. Our study enhances our understanding of behavioural finance in the setting of an Asian financial centre, namely Hong Kong. KEYWORDS: Behavioural finance, factor analysis, small investors, derivatives markets. 1. INTRODUCTION The global economic crisis has generated tremendous impacts on financial markets and affected many small investors throughout the world. In particular, these investors feared that some European countries, including the PIIGS countries (i.e., Portugal, Ireland, Italy, Greece, and Spain), would encounter great difficulty in meeting their financial obligations and repaying their sovereign debts, and some even believed that these countries would default on their debts either partially or completely. In response to the crisis, they are likely to change their investment behaviour. Corresponding author: Tai-Yuen Hon, Department of Economics and Finance, Hong Kong Shue Yan University, Braemar Hill, North Point, Hong Kong. Tel: (852) 25707110; Fax: (852) 2806 8044 59 Tai-Yuen Hon / Journal of Risk and Financial Management 5(2012) 59-77 Hong Kong is a small open economy. -

Annotated Presentation of Regulated Markets and National Provisions

15.7.2011 EN Official Journal of the European Union C 209/21 Annotated presentation of regulated markets and national provisions implementing relevant requirements of MiFID (Directive 2004/39/EC of the European Parliament and of the Council) (2011/C 209/13) Article 47 of the Markets in Financial Instruments Directive (Directive 2004/39/EC, OJ L 145, 30.4.2004) authorises each Member State to confer the status of ‘regulated market’ on those markets constituted on its territory and which comply with its regulations. Article 4, paragraph 1, point 14 of Directive 2004/39/EC defines a ‘regulated market’ as a multilateral system operated and/or managed by a market operator, which brings together or facilitates the bringing together of multiple third-party buying and selling interests in financial instruments — in the system and in accordance with its non-discretionary rules — in a way that results in a contract, in respect of the financial instruments admitted to trading under its rules and/or systems, and which is authorised and functions regularly and in accordance with the provisions of Title III of Directive 2004/39/EC. Article 47 of Directive 2004/39/EC requires that each Member State maintains an updated list of regulated markets authorised by it. This information should be communicated to other Member States and the European Commission. Under the same article (Article 47 of Directive 2004/39/EC), the Commission is required to publish a list of regulated markets, notified to it, on a yearly basis in the Official Journal of the European Union. The present list has been compiled pursuant to this requirement. -

PARALYZED ECONOMY? Restructure Your Investments Amid Gloomy Economy with Reduced Interest Rates

Outlook Money - Conclave pg 54 Interview: Prashant Kumar, Yes Bank pg 44 APRIL 2020, ` 50 OUTLOOKMONEY.COM C VID-19 PARALYZED ECONOMY? Restructure your investments amid gloomy economy with reduced interest rates 8 904150 800027 0 4 Contents April 2020 ■ Volume 19 ■ issue 4 pg 10 pg 10 pgpg 54 43 Cultivating OutlookOLM Conclave Money ConclaveReports and insights from the third Stalwartsedition of share the Outlook insights Moneyon India’s valour goalConclave to achieve a $5-trillion economy Investors can look out for stock Pick a definite recovery point 36 Management34 stock strategies Pick of Jubilant in the market scenario, FoodWorksHighlighting and the Crompton management Greaves strategies of considering India’s already ConsumerJUBL and ElectricalsCGCE slow economic growth 4038 Morningstar Morningstar InIn focus: focus: HDFC HDFC short short term term debt, debt, HDFC HDFC smallsmall cap cap fund fund and and Axis Axis long long term term equity equity Gold Markets 4658 Yes Yes Bank Bank c irisisnterview Real EstateInsuracne AT1Unfair bonds treatment write-off meted leaves out investors to the AT1 in a Mutual FundsCommodities shock,bondholders exposes in gaps the inresolution our rating scheme system 5266 My My Plan Plan COVID-19: DedicatedHow dedicated SIPs can SIPs help can bring bring financial financial Volatile Markets disciplinediscipline in in your your life lives Investors need to diversify and 6 Talk Back Regulars : 6 Talk Back restructure portfolios to stay invested Regulars : and sail through these choppy waters AjayColumnsAjayColumns Bagga, Bagga, SS Naren,Naren, :: Farzana Farzana SuriSuri CoverCover Design: Vinay VINAY D DOMINICOMinic HeadHead Office Office AB-10, AB-10, S.J. -

Global Derivatives Market

GLOBAL DERIVATIVES MARKET Aleksandra Stankovska European University – Republic of Macedonia, Skopje, email: aleksandra. [email protected] DOI: 10.1515/seeur-2017-0006 Abstract Globalization of financial markets led to the enormous growth of volume and diversification of financial transactions. Financial derivatives were the basic elements of this growth. Derivatives play a useful and important role in hedging and risk management, but they also pose several dangers to the stability of financial markets and thereby the overall economy. Derivatives are used to hedge and speculate the risk associated with commerce and finance. When used to hedge risks, derivative instruments transfer the risks from the hedgers, who are unwilling to bear the risks, to parties better able or more willing to bear them. In this regard, derivatives help allocate risks efficiently between different individuals and groups in the economy. Investors can also use derivatives to speculate and to engage in arbitrage activity. Speculators are traders who want to take a position in the market; they are betting that the price of the underlying asset or commodity will move in a particular direction over the life of the contract. In addition to risk management, derivatives play a very useful economic role in price discovery and arbitrage. Financial derivatives trading are based on leverage techniques, earning enormous profits with small amount of money. Key words: financial derivatives, leverage, risk management, hedge, speculation, organized exchange, over- the counter market. 81 Introduction Derivatives are financial contracts that are designed to create market price exposure to changes in an underlying commodity, asset or event. In general they do not involve the exchange or transfer of principal or title (Randall, 2001).