Falling Trees, Flying Limbs & Loud Neighbors

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Auto –Accidents - What Is “No-Fault” Insurance?

AUTO –ACCIDENTS - WHAT IS “NO-FAULT” INSURANCE? If you are injured in a car accident who pays your medical bills? Believe it or not, your medical insurance carrier does not have the primary responsibility to pay your medical bills for injuries sustained in an automobile accident - The applicable automobile insurance carrier does. But remember, if your injuries or above a certain threshold you can still sue the person who cause your injuries for money damages above what the applicable automobile insurance carrier provides. In New York State each automobile insurance policy must provide coverage known as Personal Injury Protection (“PIP”) and typically referred to a “No-Fault” insurance. Medical bills, some or all of the injured party’s lost wages and other expenses are paid from this portion of the policy, whether or not the injured party caused the accident. So if were in a car accident driving your own vehicle and you are injured as a result of another person's negligence, the no-fault portion of your automobile insurance policy will cover your medical bills to the extent that you have coverage. If your coverage runs out other insurance will kick in. The New York State Insurance Law, requires that all automobile insurance policies issued in this state contain a Personal Injury Protection (“PIP”) or “No-Fault” endorsement with a minimum of $50,000.00 in coverage. Generally speaking, this coverage extends to the driver and passengers in a covered vehicle, as well as to a pedestrian struck by the covered vehicle. The coverage “kicks in” regardless of fault in connection with an accident; under most circumstances, a covered individual will be afforded certain enumerated benefits regardless of that individual’s fault in connection with the happening of the accident. -

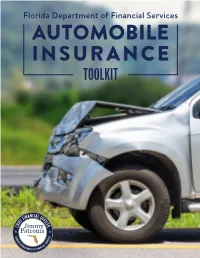

AUTOMOBILE INSURANCE TOOLKIT Automobile Insurance Toolkit

Florida Department of Financial Services AUTOMOBILE INSURANCE TOOLKIT Automobile Insurance Toolkit Insurance coverage is an integral part of a solid financial foundation. Insurance can help us recover financially after illness, accidents, natural disasters or even the death of a loved one. There are a wide variety of insurance products available and choosing the correct type and amount of coverage can be a challenge. This toolkit provides information to assist you with insuring your automobile and tips for settling an automobile insurance claim. TABLE OF CONTENTS Click a title or page number to navigate to a section. 01 Coverages & Minimum Requirements - 4 Coverage Descriptions - 5 Insurance Requirements for Special Cases - 8 02 Underwriting Guidelines - 11 Underwriting Factors That Cannot Affect Your Ability to Purchase Insurance - 11 Underwriting Factors That Affect Your Insurance Policy Premium - 12 Other Factors Affecting Your Premiums - 13 Shopping for Auto Insurance - 13 03 Automobile Claims - 14 Actions to Take Before and After an Auto Accident - 14 Disputing Claim Settlements - 16 04 Shopping for Coverage Checklist - 17 01 Coverages & Minimum Requirements In Florida, vehicle owners may be required to The second type of auto insurance is outlined in the purchase two types of auto insurance. Florida Financial Responsibility Law. It requires drivers The first type of auto insurance is outlined in the who have caused accidents involving bodily injury/death Florida Motor Vehicle No-Fault Law (s. 627.736, Florida or received certain citations, to purchase bodily injury Statutes). It requires every person who registers a liability (BI) coverage with minimum limits of $10,000 vehicle in Florida to provide proof they have personal per person and $20,000 per accident, referred to as injury protection (PIP) and property damage liability split limits. -

Frequently Asked Questions About Emergency Order 2020-1 and 2020-2

OFFICE of the INSURANCE COMMISSIONER WASHINGTON STATE Frequently Asked Questions: OIC Emergency Orders 20-01 and 20-02 and other COVID-19 related issues April 7, 2020 (NOTE: Additional FAQ’s may be issued as more information is available) Questions related to Emergency Order 20-02 Directive A: Telemedicine 1. Question: Will OIC be exercising its enforcement discretion to withhold enforcement of violations of the 30 day prompt pay rule for carrier adjudication of telehealth claims to ensure that they are paid at parity with in-person visits? Response: Yes, until April 25, 2020, the OIC will presume that good cause exists for carriers that fail to process telemedicine claims within the timeframes outlined in WAC 284-170-431(2) as long as 95% of all clean telemedicine claims are paid within 45 days of receipt by the responsible carrier or agent of the carrier. WAC 284-43-431(7) provides that providers, facilities, and carriers are not required to comply with the requirement to pay 95% of all clean claims within 30 days of receipt and 95% of all claims, clean or not, within 60 days of receipt, if the failure to comply is occasioned by any act of God, bankruptcy, act of a governmental authority responding to an act of God or other emergency, or the result of a strike, lockout, or other labor dispute. Governor Inslee’s Proclamation 20-29 regarding telemedicine payment parity was issued on March 25 and was effective immediately. For the initial thirty day period that Proclamation 20-29 is in effect, until April 25, 2020, exclusively for purposes of payment of telemedicine claims in compliance with Proclamation 20-29, OIC will presume that a failure to comply with the timeframes in WAC 284-170-431(2)(a)(i-ii) is caused by an act of a governmental authority responding to an emergency under WAC 284-170-431(7). -

Is COVID-19 an Act of God And/Or Will COVID-19 Be a Defense Against Failure to Perform? Swata Gandhi

ALERT Corporate Practice MAY 2020 Is COVID-19 an Act of God and/or Will COVID-19 Be a Defense Against Failure to Perform? Swata Gandhi This is the second in a series of alerts on Force Majeure and Common Law Defenses against failure to perform contracts. In our first alert, we discussed the elements of a force majeure clause and looked at how various states have interpreted force majeure clauses. We focused on how most states take a narrow view of these provisions and they adhere to the plain meaning of the force majeure provisions. This alert takes a look at one event often listed in force majeure clauses – Acts of God. As discussed in our previous alert, some courts will excuse performance of a contract only if the event causing the breach is actually listed in the force majeure clause. Among the list of events that would most likely excuse a failure to perform under a contract due to COVID-19 would be if the force majeure provision listed pandemics, epidemic, health emergencies or government orders or regulations. While your contract may not list these events, most force majeure provisions do include an Act of God. In this alert we look at whether it is likely that courts will find that COVID-19 is an Act of God and if such consideration will actually be a defense against performance of a contract. In general, courts have found that an Act of God is a natural event that would not occur by the intervention of man, but proceeds from physical causes. -

What You Need to Know

What AutoAuto you InsuranceInsurance need to know A consumer information publication The Minnesota Department of Commerce has prepared this guide to help you better understand auto insurance. It gives you information on shopping for insurance, the different types of coverage, and a basic understanding of “no fault” coverage. The Minnesota Department of Commerce regulates insurance agents, agencies, adjusters, and companies operating in Minnesota. If they are licensed to do business in the State, they are responsible for adhering to the laws and rules that govern the industry. This guide does not list all of these regulations. If you have a question about your insurance, please contact the Department’s Consumer Response Team at 651-296-2488, or toll free 800-657-3602. Duplication of this guide is encouraged. Please feel free to copy this information and share it with others. Department of Commerce Auto Insurance can protect you from the financial costs of an accident or injury, provided you have the proper coverage. Yet many people are unclear about what their insurance policy cov- ers until it is too late. They may have difficulties settling a claim or face rate increases or termination of coverage. Auto Insurance I s ... Protection. Insurance is a way of transferring risk for a loss among a certain group of people. You, and others, pay premiums to an insurance company to be reimbursed if you have an acci- dent. The amount you can collect and under what circumstances are outlined in your policy. Required. Under most circumstances, a licensed vehicle in the state of Minnesota must have liability, personal injury protection, uninsured motorist, and underinsured motorist coverage. -

Force Majeure and COVID-19

Force Majeure and COVID-19 Not all “Acts of God” are Created Equal Alec W. Farr 1 Force Majeure Clauses Generally • Civil law concept written into contracts. • A “force majeure” is an adverse event outside the control of the parties that prevents a party from fulfilling a contract. – Also called an “Act of God” clause • Purpose: to limit damages in a case where the reasonable expectation of the parties and the performance of the contract have been frustrated by circumstances beyond the parties’ control. • Generally only excuses performance if it renders performance impossible, not merely harder or more expensive. • Highly dependent on the specific language of the contract and the circumstances of the case -- one size does not fit all. 2 Force Majeure Clauses Generally • Primary issue in determining whether a force majeure clause is applicable: does it list the specific type of event claimed, i.e. a “pandemic” or “epidemic”, as a force majeure event? • Force majeure clauses are interpreted narrowly. • Force majeure event must be the proximate cause of a party’s inability to perform. • The party seeking to invoke force majeure usually must show that it tried to perform. 3 Force Majeure Clauses Generally • Most clauses include a general reference to “Acts of God” • What is an “Act of God”? • Usually means an event outside human control that is so extraordinary and unprecedented as to be unforeseeable. • Most often invoked in cases of natural disasters -- earthquakes, floods, extraordinary weather events, etc. • But not all “Acts of God” are necessarily unforeseeable events that will excuse performance of the contract. -

Cargo Insurance What You Need to Know

Cargo Insurance What You Need to Know Making it easier for you Making it easier for you. Is Your Company Exposed? The rigors of international transit can expose your freight to a number of perils. Fires, collisions, storms, accidents, theft, quarantine, civil unrest and many other factors can result in lost or damaged freight and lead to major financial losses for your company. Reilly International wants you to know the risks and the liabilities, so you can make an informed decision about protecting your freight and safeguarding your company’s financial health. The Limits of Carrier Liability The “General Average” Loss It may surprise you to learn that carriers are not In some situations, you may be financially responsible even necessarily liable for your freight while it is in their if your freight was not lost or damaged. General Average possession. Whether ocean, air, truck or rail, there are refers to a partial ocean marine loss. It is determined when myriad situations where carriers can, and do, deny there is a voluntary sacrifice, e.g. jettisoning cargo or liability. At best, without insurance, you’re in for a long extinguishing a fire, in order to save cargo, vessel or life. and complicated legal process. In many cases, the carrier In a General Average, the loss to vessel and freight is will claim no responsibility and your company will have to identified. The financial burden is then divided between all cover the entire loss. the cargo owners. Your cargo is seized until your company Even if the carrier is found to be negligent, the maximum posts a General Average guarantee. -

The RAM Health Insurance Cooperative Is NOW Thriving

Health Insurance Cooperative The RAM Health Insurance Cooperative is NOW thriving – and growing – in 2020! The program offers RAM members: A 3% DISCOUNT OFF PREMIUM RATES FOR SMALL BUSINESSES IN THE SMALL GROUP MARKET (Groups of 1-50 employees) ACCESS TO EVERY SMALL GROUP PLAN OFFERED BY BCBSMA & ALMOST ALL SMALL GROUP PLANS OFFERED BY FALLON HEALTH DEFINED CONTRIBUTION OPTIONS TO ADDRESS THE NEEDS OF BOTH YOUR BUSINESS AND YOUR EMPLOYEES And for those members who choose a BCBSMA plan, the program also offers additional value-added benefits including: A WELLNESS PROGRAM WITH POTENTIAL EMPLOYEE INCENTIVES OF UP TO $300 AND AN OPPORTUNITY TO EARN 7.5% IN BACK END EMPLOYER INCENTIVES A FREE SUPPLEMENTAL HOSPITALIZATION POLICY FOR ALL SUBSCRIBERS, WHICH COVERS $750 FOR A HOSPITAL ADMISSION AND $150 EACH ADDITIONAL DAY UP TO 10 DAYS A FREE $10,000 LIFE INSURANCE POLICY FOR ALL SUBSCRIBERS Visit www.retailersma.org or call us at (617) 523-1900 to learn more! Health Insurance Cooperative Dear RAM Member, RAMHIC is a service of the Retailers Association of Massachusetts—the leading voice for more choice and fairer premiums for small businesses and their employees in the Massachusetts insurance market. RAMHIC is an important example of our efforts to deliver economic equality for Main Street. Since the adoption of universal healthcare in Massachusetts, small businesses have received disproportionate increases in their health insurance premiums compared to their large competitors and government programs. In response, RAM fought for the creation of small business group purchasing cooperatives designed to allow like-minded businesses to join together and negotiate with carriers for reduced premium rates based on the projected experience of the group. -

Lloyd's Policy Signing Office, Quoting the Lloyd's Policy Signing Office Number and Date Or Reference Shown in the Table

Lloyd’s Policy of the Syndicates whose definitive numbers We, Underwriting Members and proportions are shown in the Table attached hereto (hereinafter referred to as 'the Underwriters'), hereby agree, in consideration of the payment to Us by or on behalf of the Assured of the Premium specified in the Schedule, to insure against loss, including but not limited to associated expenses specified herein, if any, to the extent and in the manner provided in this Policy. The Underwriters hereby bind themselves severally and not jointly, each for his own part and not one for another, and therefore each of the Underwriters (and his Executors and Administrators) shall be liable only for his own share of his Syndicate's proportion of any such Loss and of any such Expenses. The identity of each of the Underwriters and the amount of his share may be ascertained by the Assured or the Assured's representative on application to Lloyd's Policy Signing Office, quoting the Lloyd's Policy Signing Office number and date or reference shown in the Table. If the Assured shall make any claim knowing the same to be false or fraudulent, as regards amount or otherwise, this Policy shall become void and all claim hereunder shall be forfeited. In Witness whereof the General Manager of Lloyd's Policy Signing Office has signed this Policy on behalf of each of Us. LLOYD'S POLICY SIGNING OFFICE General Manager If this policy (or any subsequent endorsement) has been produced to you in electronic form, the original document is stored on the Insurer's Market Repository to which your broker has access. -

Pakistan Overwhelmed by Quake Crisis

ITIJITIJ Page 22 Page 26 Page 28 Page 30 International Travel Insurance Journal ISSUE 58 • NOVEMBER 2005 ESSENTIAL READING FOR TRAVEL INSURANCE INDUSTRY PROFESSIONALS Europe panics at Pakistan overwhelmed by quake crisis avian flu threat On 8 October, a massive earthquake rocked Pakistan and northern India, The deadly strain of bird flu that has killed resulting in the extensive destruction of approximately 60 people in Asia has spread to property and the loss of thousands of Europe and the continent is in panic. Leonie lives. Initial estimates suggested that at Bennett reports on what is being done to stem the least 33,000 persons perished, now it spread of the virus seems this number is more likely to be around 80,000. Leonie Bennett reports On 13 October, scientists confirmed that the bird flu virus was found in poultry in Turkey, the first time Most of the casualties from the that the virus has been found outside Asia, marking earthquake, which measured 7.6 on the a new phase in the virus’s spread across the globe. Richter scale, were from Pakistan. The Then, on the 17 October, it was established that epicentre of the quake, which lasted for the virus had infected Romanian birds. It was over a minute, was near Muzzaffarabad, confirmed as the H5N1 strain that it is feared can capital of Pakistan-occupied Kashmir, at mutate into a human disease, potentially spiralling 9:20 a.m. Indian Standard Time. Tremors out of control and threatening the lives of millions of were reported in Delhi, Punjab, Jammu, people worldwide. -

PDF Hosted at the Radboud Repository of the Radboud University Nijmegen

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Radboud Repository PDF hosted at the Radboud Repository of the Radboud University Nijmegen The following full text is a publisher's version. For additional information about this publication click this link. http://hdl.handle.net/2066/157883 Please be advised that this information was generated on 2017-12-05 and may be subject to change. Accidental Harm Under (Roman) Civil Law Corjo Jansen Abstract A leading idea under Roman private law and nearly all European legal systems is that an owner has to bear the risk of an accidental loss (casus). An accident is a circumstance for which a third party cannot be blamed (culpa or fault). A person suffering damage from an accident had to bear that damage himself. This idea has been subject to attack throughout history. Every once in a while, it is said that ‘bad luck must be righted’ (‘pech moet weg’). This position has not become the prevailing viewpoint among lawyers. Although it does not seem very realistic, ‘bad luck must be righted’ did form the basis of social security policies of the Netherlands and some other western countries after World War II: social security ‘from womb to tomb’. The scope of social security benefits has been reduced in many countries in the last decades of the twentieth century, because the costs were no longer affordable. The idea that a owner has to bear the risk of casus has withstood the test of time quite well. That accidental harm must be borne by the one suffering it, is legally and morally justifiable. -

Understanding How Insurance Works: a Case Study About Lucy (Guide) Cfpb Building Block Activities Understanding-How-Insurance-Works-Lucy Guide.Pdf

BUILDING BLOCKS TEACHER GUIDE Understanding how insurance works: A case study about Lucy Students read about how insurance works, then review a case study to see how insurance choices can affect personal finances for a rural young adult. Learning goals KEY INFORMATION Big idea Building block: When you purchase insurance, you are Executive Function transferring financial risk from yourself to an Financial knowledge and insurance company. decision-making skills Essential questions Grade level: High school (9–12) § What is the main benefit of choosing to Age range: 13–19 purchase insurance? Topic: Protect (Managing risk) § How do the insurance company and the policyholder share risks and costs? School subject: CTE (Career and technical education), Math, Physical education or Objectives health, Social studies or history Teaching strategy: Cooperative learning, § Understand how insurance works Simulation § Apply insurance policy specifics to a case study to evaluate costs and benefits Bloom’s Taxonomy level: Understand, Apply, Evaluate What students will do Activity duration: 45–60 minutes § Read about how the insurance process works and discover what roles the insurance STANDARDS company and the policyholders play. § Review information about specific types of Council for Economic Education Standard VI. Protecting and insuring insurance policy coverage and costs. Jump$tart Coalition Risk management and insurance – Standard 1 To find this and other activities go to: Consumer Financial Protection Bureau consumerfinance.gov/teach-activities 1 of 7 Winter 2020 § Evaluate a case study to see how one policyholder’s insurance choices affected her financially. § Write an advice email about the value of insurance in that policyholder’s life.