Date: August 30, 2019 To: Representative Lyndon Carlson

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

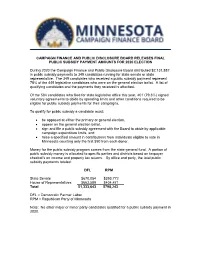

2020 Final Public Subsidy Payments

CAMPAIGN FINANCE AND PUBLIC DISCLOSURE BOARD RELEASES FINAL PUBLIC SUBSIDY PAYMENT AMOUNTS FOR 2020 ELECTION During 2020 the Campaign Finance and Public Disclosure Board distributed $2,131,887 in public subsidy payments to 349 candidates running for state senate or state representative. The 349 candidates who received a public subsidy payment represent 78% of the 449 legislative candidates who were on the general election ballot. A list of qualifying candidates and the payments they received is attached. Of the 504 candidates who filed for state legislative office this year, 401 (79.3%) signed voluntary agreements to abide by spending limits and other conditions required to be eligible for public subsidy payments for their campaigns. To qualify for public subsidy a candidate must: • be opposed at either the primary or general election, • appear on the general election ballot, • sign and file a public subsidy agreement with the Board to abide by applicable campaign expenditure limits, and • raise a specified amount in contributions from individuals eligible to vote in Minnesota counting only the first $50 from each donor. Money for the public subsidy program comes from the state general fund. A portion of public subsidy money is allocated to specific parties and districts based on taxpayer checkoffs on income and property tax returns. By office and party, the total public subsidy payments totaled: DFL RPM State Senate $670,054 $393,772 House of Representatives $663,589 $404,471 Total $1,333,643 $798,243 DFL = Democratic Farmer Labor RPM = Republican Party of Minnesota Note: No other major or minor party candidates qualified for a public subsidy payment in 2020. -

2013 Minnesota House of Representatives Minneapolis and Saint Paul Including February 12, 2013 Special Election Results North Oaks

2013 Minnesota House of Representatives Minneapolis and Saint Paul Including February 12, 2013 Special Election Results North Oaks Brooklyn Park St. Vincent Fridley ¤£10 Mahtomedi Humboldt 41A Connie Bernardy DFL Brooklyn Center Warroad ¦§¨694 Lancaster 40B Debra Hilstrom DFL Roseau New Brighton Birchwood Village Roosevelt Arden Hills Hallock Anoka Shoreview Kittson White Bear Lake Badger 42A Barb Yarusso DFL Gem Lake Vadnais Heights Lake Bronson Roseau Williams Greenbush Hilltop Baudette Halma Kennedy Columbia Heights Donaldson Lake of the Woods 45A Lyndon R. Carlson DFL 42B Jason Isaacson DFL Karlstad Ranier 41B Carolyn Laine DFL Strathcona International Falls Strandquist New Hope 01A Dan Fabian R Crystal ¦§¨694 Stephen ¤£75 Middle River Marshall Argyle Newfolden Littlefork 59A Joe Mullery DFL Robbinsdale Little Canada St. Anthony 43A Peter Fischer DFL Holt Grygla Koochiching Oslo Viking ¤£61 Alvarado Warren Roseville Maplewood North St. Paul Goodridge 60A Diane Loeffler DFL Big Falls 45B Mike Freiberg DFL Thief River Falls 02A Roger Erickson DFL Pennington Cook 66A Alice Hausman DFL 43B Leon M. Lillie DFL St. Hilaire Beltrami Orr East Grand Forks Plummer Kelliher Ramsey Lauderdale Winton Red Lake Falls Mizpah Ely Oakdale Polk Red Lake Golden Valley 01B Debra Kiel R Oklee Falcon Heights Northome 03A David Dill DFL Fisher Brooks Effie Cook Crookston Tower 59B Raymond Dehn DFL Trail Funkley Grand Marais 66B John Lesch DFL Gully Itasca Bigfork Mentor Gonvick Clearbrook Blackduck Erskine 67A Tim Mahoney DFL Climax St. Louis 60B Phyllis -

County Costs Counties Are Witnessing an Array of Costs Associated with the Coronavirus Pandemic

April 21, 2020 Senator Julie Rosen Chair, Senate Finance Committee 95 University Avenue West Minnesota Senate Building, Room 2113 Saint Paul, MN 55155 Re: County Budget Pressures Related to COVID-19 Dear Senator Rosen: Thank you for your recent inquiry regarding local government budget pressures related to COVID- 19. On behalf of all 87 Minnesota counties, the Association of Minnesota Counties (AMC) appreciates your awareness that the effects of this public health emergency are far reaching— impacting residents, families, businesses, and local governments—and supports your work to make sure that federal monies appropriated to the state for COVID-19 relief are also appropriately allocated to local government partners. In response to your questions, we surveyed our membership to get clearer understanding of the fiscal impacts on counties. The results of that survey are summarized below. County Costs Counties are witnessing an array of costs associated with the coronavirus pandemic. It is important to note that these costs are not uniform across the state and are expected to increase significantly in time as the full impacts of the pandemic are realized. • Upfront costs (technology, remote work, paid leave mandates, and workers compensation) Counties across the state faced immediate, unplanned costs for the logistical and infrastructure needs for creating remote work environments along with the purchasing of personal protective gear for employees. We are also facing direct costs for administering additional paid leave benefits mandated through the new Families First/FMLA laws (for which local governments are not eligible for tax credits), any realized COVID-related workers compensation claims, and costs associated with operating local emergency management response activities. -

Please Contact Legislators to Support NAZ Families Sample Email/Phone

Please Contact Legislators to Support NAZ Families Dear NAZ Supporters, We are asking you to contact state legislators today and tomorrow to encourage them to support House File 3172—a bill to bolster the groundbreaking work at the Northside Achievement Zone (NAZ). The bill is currently being worked on by a conference committee of House and Senate members. This bill will help NAZ reach our goal of enrolling 3,000 North Minneapolis children on a “cradle to career” path to college. Strong early evidence shows that the NAZ approach is working! Sample language is provided below, as well as a list of contact information. We are grateful for your help! Sample Email/Phone Language I’m asking for your support for House File 3172, which provides $1.1 million for the Northside Achievement Zone’s (NAZ) work to permanently close the achievement gap and end poverty in North Minneapolis. This funding will increase the number of low-income North Minneapolis families who can enroll in NAZ and become leaders in community transformation that will bolster an educated workforce for our entire state. The NAZ approach is already showing early results in North Minneapolis - arguably one of the most distressed areas in our state: • Young NAZ scholars are more likely to be ready for kindergarten. • NAZ scholars are jumping ahead substantially in reading and math through after school and summer programs. • NAZ reduced housing instability for 1/3 of enrolled families. With your support, NAZ can serve as an incubator for best practices for the entire state. Please support the full $1.1M proposal. -

Minnesota House of Representatives Seating Chart

The Minnesota House of Representatives House Leadership Seat Paul Thissen ........................................... 139 Minnesota House of Representatives Public Information Services, 651-296-2146 or 800-657-3550 Speaker of the House District Room* 296- Seat Erin Murphy ........................................... 102 60B Kahn, Phyllis (DFL) ............365 ....... 4257 ....... 97 Majority Leader 21A Kelly, Tim (R) ......................335 ....... 8635 ....... 12 53B Kieffer, Andrea (R) ..............213 ....... 1147 ....... 43 Minnetonka—44B Kurt Daudt ............................................... 23 Shoreview—42B Murdock—17A Jason Isaacson John Benson 1B Kiel, Debra (R) ....................337 ....... 5091 ....... 30 Andrew Falk Seat 124 Seat 135 Minority Leader Seat 129 9B Kresha, Ron (R) ...................329 ....... 4247 ....... 53 Seat 1 Seat 6 41B Laine, Carolyn (DFL) ..........485 ....... 4331 ....... 82 Seat 11 Joe Hoppe Mayer—47A Ernie Leidiger Mary Franson Chaska—47B House Officers Alexandria—8B 47A Leidiger, Ernie (R) ...............317 ....... 4282 ......... 1 Mary Sawatzky Faribault—24B Willmar—17B Virginia—6B Albin A. Mathiowetz ....... 142 Timothy M. Johnson ....... 141 Jason Metsa 50B Lenczewski, Ann (DFL) ......509 ....... 4218 ....... 91 Seat 123 Seat 128 Seat 134 Patti Fritz Seat 139 Chief Clerk Desk Clerk Paul Thissen 66B Lesch, John (DFL) ...............537 ....... 4224 ....... 71 Patrick D. Murphy .......... 143 David G. Surdez ............. 140 Minneapolis—61B Seat 7 Seat 2 26A Liebling, Tina (DFL) ...........367 ....... 0573 ....... 90 Seat 12 Speaker of the House Kelly Tim Bob Dettmer 1st Asst. Chief Clerk Legislative Clerk Bob Barrett Lindstrom—32B Red Wing—21A Forest Lake—39A 4A Lien, Ben (DFL) ..................525 ....... 5515 ....... 86 Gail C. Romanowski ....... 144 Travis Reese ...................... 69 South St. Paul—52A Woodbury—53A Richfield—50A 2nd Asst. Chief Clerk Chief Sergeant-at-Arms Linda Slocum 43B Lillie, Leon (DFL) ...............371 ...... -

2016 House Committee Chairs

PUBLIC INFORMATION SERVICES 175 State Office Building Minnesota 100 Rev. Dr. Martin Luther King Jr. Blvd. St. Paul, MN 55155 House of 651-296-2146 Fax: 651-297-8135 Representatives 800-657-3550 Kurt Daudt, Speaker FOR IMMEDIATE RELEASE Date: Nov. 22, 2016 Contact: Lee Ann Schutz 651-296-0337 [email protected] House Committee structure, chairs named Committee membership is expected to be named in mid-December House Republican leadership has announced the committee structure and chairs for the 90th legislative biennium scheduled to convene Jan. 3, 2017. The plan is for 27 committees, divisions or subcommittees, one more than the 2015-16 biennium. Committee membership is expected to be named in mid-December. “Our committee chairs are eager to get to work tackling the critical issues facing Minnesota families,” House Speaker Kurt Daudt (R-Crown) said in a statement. “Lowering health care costs, growing good-paying jobs, and reducing the tax burden on middle-class families will be shared priorities of Republicans in Saint Paul, and we look forward to working with the new Senate Republican Majority to build a Minnesota that works.” “We’re particularly excited about subcommittees that will focus on key issues including making childcare more affordable, caring for our aging loved ones, and ensuring that key industries like mining, forestry, and tourism remain vibrant,” added House Majority Leader Joyce Peppin (R-Rogers). 2017-2018 Committee Names and Chair Agriculture Finance:........................................................................................Rod Hamilton (R-Mountain Lake) Agriculture Policy: ..........................................................................................Rep. Paul Anderson (R-Starbuck) Capital Investment: ........................................................................................ Rep. Dean Urdahl (R-Grove City) Civil Law and Data Practices Policy: ..................................................................Rep. -

October/November 2018

MINNESOTA EDUCATOR OCTOBER/NOVEMBER 2018 Organize, organize, organize: MFT ESPs engage with members all summer long MEA is here: everything you need to know before Oct. 18 Table of contents October/November 2018 – Volume 21, No. 2 The Minnesota Educator publishes every other The Minnesota National Board month. It is one of the union’s print and digital Certified Teacher Network provides publications to educate, inform and organize the community of members. The Educator is reported, support for Education Minnesota edited and designed by union staff members. The members applying for certification. paper is printed in LSC Communications’ union shop in Menasha, Wisconsin. Find copies of the page 6 Educator online at www.educationminnesota.org. Go to the News menu, then Minnesota Educator. Union members at St. Cloud To reach the publication for queries, Technical and Community story or commentary ideas College organize a “Great Big Email: [email protected] Giveaway” for students. Mail: Minnesota Educator 41 Sherburne Ave. page 7 St. Paul, MN 55103 To report a change of address or end Everything you need to know duplicate mailings, contact the Education about the MEA Conference, Minnesota membership department. including workshops, featured Email: [email protected] By web: www.educationminnesota.org and choose speakers, exhibitors and more. the Contact Us link to send a change of address. pages 9-12 To inquire about advertising in the Educator or on the website Thousands of worksite action Email: [email protected] Phone: 651-292-4864 leaders start on plans to motivate For general inquiries and business their colleagues to vote. -

Minnesota House of Representatives Session Weekly

SESSION WEEKLY RESOURCES: LEGISLATIVE CONTACTS 2012 SESSION PREVIEW MEET THE NEW MEMBER CHARTER SCHOOL FUNDING PLENTY OF BONDING PROPOSALS HF1762 - HF1986 A NONPARTISAN PUBLICATION MINNESOTA HOUSE OF REPRESENTATIVES • PUBLIC INFORMATION SERVICES VOLUME 29, NUMBER 1 • JANUARY 27, 2012 Flashback to 2002 Vikings propose sharing stadium with the Gophers The 2002 legislative session began with the challenge of Welcome to Session Weekly and fixing a $1.95 billion deficit and dealing with task force the 2012 legislative session recommendations on a new Twins baseball park and a new Each week, Session Weekly staff will bring to you a non- football stadium to be shared by the Minnesota Vikings and partisan look at the issues before the House and the people the University of Minnesota. who shape the legislation. While the Session Weekly newsmagazine, now in its State participation in a new Twins stadium would be 29th year, remains our cornerstone publication, we are providing more online opportunities to access nonpartisan contingent on the reform of baseball’s economic structure, news from the House. including some form of payroll equalization between teams, Session Daily provides stories about committee and floor the task force proposed. action, including links to bill and member information, per- tinent reports and video coverage, when available. You can also access our social media accounts: The Vikings proposed a $500 million retractable-roof Facebook — www.facebook.com/MNHouseInfo facility to be shared with the Gophers on the University of Twitter — twitter.com/MNHouseInfo YouTube — youtube .com/user/MNHouseInfo Minnesota campus. Renovation of the Metrodome was not Other services to help you stay informed during session considered viable by the task force. -

Protect Minnesota Orange Star Leaders MN State Legislature As of June 1, 2019

Protect Minnesota Orange Star Leaders MN State Legislature As of June 1, 2019 Orange Star members have shown themselves to be committed to saving lives by passing gun violence prevention bills. It’s very important that we communicate our sincere thanks to these legislators... Orange Star MN Senate Members 51 Jim Carlson 40 Chris Eaton 52 Matt Klein 45 Ann Rest 59 Bobby Joe Champion 49 Melisa Franzen 41 Carolyn Laine 7 Erik Simonson 57 Greg Clausen 19 Nick Frentz 46 Ron Latz 63 Patricia Torres Ray 64 Richard Cohen 67 Foung Hawj 58 Matt Little 43 Charles Wiger 48 Steve Cwodzinski 62 Jeff Hayden 66 John Marty 50 Melissa Wiklund 61 Scott Dibble 42 Jason Isaacson 37 Jerry Newton 60 Kari Dziedzic 53 Susan Kent 65 Sandra Pappas Orange Star MN House Members These members all voted to pass the Criminal Background Checks and ERPO bills in 2019. 44B Patty Acomb 62B Aisha Gomez 20B Todd Lippert 52B Ruth Richardson 34B Kristin Bahner 51B Laurie Halverson 60A Diane Loeffler 53B Steve Sandell 42B Jamie Becker-Finn 52A Rick Hansen 61B Jamie Long 25B Duane Sauke 41A Connie Bernardy 62A Hodan Hassan 67A Tim Mahoney 7A Jennifer Schultz 57A Robert Bierman 66A Alice Hausman 56B Alice Mann 36A Zack Stephenson 19A Jeff Brand 64A Kaohly Her 65B Carlos Mariani 55A Brad Tabke 56A Hunter Cantrell 61A Frank Hornstein 51A Sandra Masin 40B Samantha Vang 50B Andrew Carlson 50A Michael Howard 42A Kelly Moller 63B Jean Wagenius 45A Lyndon Carlson 57B John Huot 65A Rena Moran 38B Ami Wazlawik 39B Shelly Christensen 44A Ginny Klevorn 33B Kelly Morrison 46A Ryan Winkler 54A Anne Claflin 37A Erin Koegel 03B Mary Murphy 14B Dan Wolgamott 19B Jack Considine 48B Carlie Kotyza-Witthuhn 40A Michael Nelson 67B Jay Xiong 63A Jim Davnie 41B Mary Kunesh-Podein 60B Mohamud Noor 53A Tou Xiong 59B Raymond Dehn 59A Fue Lee 07B Liz Olson 46B Cheryl Youakim 49A Heather Edelson 66B John Lesch 05A John Persell 49B Steve Elkins 26A Tina Liebling 64B Dave Pinto 36B Speaker Melissa Hortman 43A Peter Fischer 4A Ben Lien 27B Jeanne Poppe 45B Mike Freiberg 43B Leon Lillie 48A Laurie Pryor . -

What Percentage of Incumbent Minnesota Legislators Are Returned to Office After Each General Election?

Minnesota Legislative Reference Library www.leg.mn/lrl What Percentage of Incumbent Minnesota Legislators Are Returned to Office After Each General Election? (What percentage of Minnesota legislators who run for re-election win?) Election Date: November 2, 2010 Legislative Chamber: House Number of incumbents who ran: 119 134 Total number of legislators in the chamber Minus 15 Number of incumbents who did not run Equals 119 Number of incumbents who ran Number of incumbents who were defeated: 21 36 Number of new legislators after election Minus 15 Number of incumbents who did not run Equals 21 Number of incumbents who were defeated Number of incumbents who won: 98 119 Number of incumbents who ran Minus 21 Number of incumbents who were defeated Equals 98 Number of incumbents who won Percent of incumbents re-elected: 82.4 % 98 Number of incumbents who won Divided by 119 Number of incumbents who ran Equals .8235 x 100 = 82.35 Percent of incumbents re-elected What Percentage of Incumbent Minnesota Legislators Are Returned to Office After Each General Election? (What percentage of Minnesota legislators who run for re-election win?) Election Date: November 2, 2010 Legislative Chamber: Senate Number of incumbents who ran: 58 67 Total number of legislators in the chamber Minus 9 Number of incumbents who did not run Equals 58 Number of incumbents who ran Number of incumbents who were defeated: 15 24 Number of new legislators after election Minus 9 Number of incumbents who did not run Equals 15 Number of incumbents who were defeated Number of incumbents -

2013 Minnesota Legislative Voting Record & Bill Summary

MINNESOTA CHAMBER of COMMERCE 2013 Minnesota Legislative Voting Record & Bill Summary Table of Contents Introduction ........................................................... 3 Legislature Bills & Commentary Education & Workforce, Elections ..................... 4 Energy, Environment ........................................ 5 Fiscal, Health Care ............................................ 6 Labor, Transportation ....................................... 7 Senate Voting Record ............................................. 8 House Voting Record .............................................. 10 The Minnesota Chamber of Commerce will proactively lead the business community statewide to: • Advance pro-business, responsible Minnesota public policy that creates jobs and grows the economy • Provide member services to address evolving business needs • Be nonpartisan For the first time in more than 20 reforms and initiatives. The result years, the Minnesota Legislature is more government at higher and executive branch were governed cost with no guarantee of by single-party control. The 2012 better results or improved election swept Democrats into quality of life for Minnesotans. the majority with Governor Mark Government spending will Dayton at midpoint in his first term. grow by nearly $3 billion, an 8% increase in FY 2014-2015, With this political backdrop, and nearly $4 billion, an 11% the Minnesota Chamber worked increase in FY 2016-2017. hard on behalf of our 2,300 members statewide to bring The 2013 Legislative Voting balance to the debate -

Minnesota House of Representatives Members at the 2016 State Fair

PUBLIC INFORMATION SERVICES 175 State Office Building Minnesota 100 Rev. Dr. Martin Luther King Jr. Blvd. St. Paul, MN 55155 House of 651-296-2146 Fax: 651-297-8135 Representatives 800-657-3550 Kurt Daudt, Speaker FOR IMMEDIATE RELEASE Date: Aug. 23, 2016 Contact: Lee Ann Schutz 651-296-0337 [email protected] You‘re invited to speak your mind Talk with legislators, be the House speaker, voice your opinion Fairgoers are invited to weigh in on hot political topics and meet with legislators during their visit to the House of Representatives’ booth at the Minnesota State Fair. Record your visit on social media with a photo as you stand behind of a replica of the House speaker’s desk. Complete with flags and the Abraham Lincoln portrait, the display gives you a feel for what it is like to stand in this position of power. Be sure to find out the fascinating history behind the portrait. The annual House opinion poll draws the attention of around 10,000 participants and will, once again, be available. Fairgoers can let their opinions be known on a number of issues including this fall’s ballot question on who should set legislators’ salaries; a requirement for individuals to use restroom and locker room facilities in schools and businesses based on biological sex, as defined at birth; and criminal background checks for all gun purchases. Poll results should be available on the House website Sept. 6, the day after the fair closes. The House of Representatives exhibit is located in the Education Building on Cosgrove Street, just north of Dan Patch Avenue.