Destination Management Plan Lasseter Region 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Year: 2016 Region: All Road Name Station Location Site Number

All Stations Year: 2016 Table: 4D Road Closures/Restrictions Region: All Road Name Station Location Site Days Month(s) Restriction Description Details Number Affected Affected Type Larapinta Drive 5Km West Of Areyonga Road RAVDC077 42 Jan - Feb Restricted 4Wd Only Changing Surface Conditions Larapinta Drive 1Km East Of Larapinta/Namatjira Junction RAVDP002 1 Dec Closed Road Closed Flooding Larapinta Drive 1Km East Of Larapinta/Namatjira Junction RAVDP002 5 Dec Closed Road Closed Flooding Larapinta Drive 14Km South Of Mereenie Oil Fields RAVDP013 15 Dec Restricted With Caution Changing Surface Conditions Larapinta Drive 14Km South Of Mereenie Oil Fields RAVDP013 2 Dec Closed Road Closed Flooding Larapinta Drive 14Km South Of Mereenie Oil Fields RAVDP013 1 Dec Closed Road Closed Flooding Larapinta Drive 14Km South Of Mereenie Oil Fields RAVDP013 5 Dec Closed Road Closed Flooding Larapinta Drive 14Km South Of Mereenie Oil Fields RAVDP013 42 Jan - Feb Restricted 4Wd Only Changing Surface Conditions Larapinta Drive At Alice Springs Town Boundary UAVDC044 5 Dec Closed Road Closed Flooding Lasseter Highway 500M West Of Stuart Highway RAVDP007 1 May Closed Road Closed Flooding Litchfield Park Road 2Km West Of Cox Peninsula Road RDVDC031 5 Jan Restricted Weight And Maximum Gvm 4.5 Tonne, Light Vehicles Only Litchfield Park Road 1Km North Of Wangi Falls Road RDVDC053 7 Aug Restricted Lane Closure Road Works Litchfield Park Road 1Km North Of Wangi Falls Road RDVDC053 1 Dec Restricted Weight And 100% Legal Axle Group Mass Limits, Maximum 13 Axles -

Driving Holidays in the Northern Territory the Northern Territory Is the Ultimate Drive Holiday Destination

Driving holidays in the Northern Territory The Northern Territory is the ultimate drive holiday destination A driving holiday is one of the best ways to see the Northern Territory. Whether you are a keen adventurer longing for open road or you just want to take your time and tick off some of those bucket list items – the NT has something for everyone. Top things to include on a drive holiday to the NT Discover rich Aboriginal cultural experiences Try tantalizing local produce Contents and bush tucker infused cuisine Swim in outback waterholes and explore incredible waterfalls Short Drives (2 - 5 days) Check out one of the many quirky NT events A Waterfall hopping around Litchfield National Park 6 Follow one of the unique B Kakadu National Park Explorer 8 art trails in the NT C Visit Katherine and Nitmiluk National Park 10 Immerse in the extensive military D Alice Springs Explorer 12 history of the NT E Uluru and Kings Canyon Highlights 14 F Uluru and Kings Canyon – Red Centre Way 16 Long Drives (6+ days) G Victoria River region – Savannah Way 20 H Kakadu and Katherine – Nature’s Way 22 I Katherine and Arnhem – Arnhem Way 24 J Alice Springs, Tennant Creek and Katherine regions – Binns Track 26 K Alice Springs to Darwin – Explorers Way 28 Parks and reserves facilities and activities 32 Festivals and Events 2020 36 2 Sealed road Garig Gunak Barlu Unsealed road National Park 4WD road (Permit required) Tiwi Islands ARAFURA SEA Melville Island Bathurst VAN DIEMEN Cobourg Island Peninsula GULF Maningrida BEAGLE GULF Djukbinj National Park Milingimbi -

Infrastructure Requirements to Develop Agricultural Industry in Central Australia

Submission Number: 213 Attachment C INFRASTRUCTURE REQUIREMENTS TO DEVELOP AGRICULTURAL INDUSTRY IN CENTRAL AUSTRALIA 132°0'0"E 133°0'0"E 134°0'0"E 135°0'0"E 136°0'0"E 137°0'0"E Aboriginal Potential Potential Approximate Bore Field & Water Control Land Trust Water jobs when direct Infrastructure District (ALT) / Allocation fully economic Requirements Area (ML) developed value ($m) ($m) Karlantijpa 1000 20 Tennant ALT Creek + Warumungu $12m $3.94m Frewena ALT 2000 40 (Frewena) 19°0'0"S Frewena 19°0'0"S LIKKAPARTA Tennant Creek Karlantijpa ALT Potential Potential Approximate Bore Field & Water Aboriginal Control Land Trust Water jobs when direct Infrastructure District (ALT) / Area Allocation fully economic Requirements 20°0'0"S (ML) developed value ($m) ($m) 20°0'0"S Illyarne ALT 1500 30 Warrabri ALT 4000 100 $2.9m Western MUNGKARTA Murray $26m (Already Davenport Downs & invested via 1000 ABA $3.5m) Singleton WUTUNUGURRA Station CANTEEN CREEK Illyarne ALT Murray Downs and Singleton Stations ALI CURUNG 21°0'0"S 21°0'0"S WILLOWRA TARA Warrabri ALT AMPILATWATJA WILORA Ahakeye ALT (Community farm) ARAWERR IRRULTJA 22°0'0"S NTURIYA 22°0'0"S PMARA JUTUNTA YUENDUMU YUELAMU Ahakeye ALT (Adelaide Bore) A Potential Potential Approximate Bore Field & B Water LARAMBA Control Aboriginal Land Water jobs when direct Infrastructure C District Trust (ALT) / Area Allocation fully economic Requirements Ahakeye ALT (6 Mile farm) (ML) developed value ($m) ($m) Ahakeye ALT Pine Hill Block B ENGAWALA community farm 30 5 ORRTIPA-THURRA Adelaide bore 1000 20 Ti-Tree $14.4m $3.82m Ahakeye ALT (Bush foods precinct) Pine Hill ‘B’ 1800 20 BushfoodsATITJERE precinct 70 5 6 mile farm 400 10 23°0'0"S 23°0'0"S PAPUNYA Potentia Potential Approximate Bore Field & HAASTS BLUFF Water Aboriginal Control Land Trust l Water jobs when direct Infrastructure District (ALT) / Area Allocati fully economic Requirements on (ML) developed value ($m) ($m) A.S. -

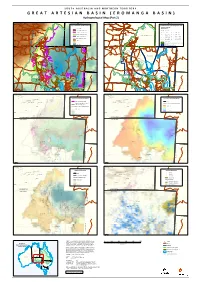

GREAT ARTESIAN BASIN Responsibility to Any Person Using the Information Or Advice Contained Herein

S O U T H A U S T R A L I A A N D N O R T H E R N T E R R I T O R Y G R E A T A R T E S I A N B A S I N ( E RNturiyNaturiyaO M A N G A B A S I N ) Pmara JutPumntaara Jutunta YuenduYmuuendumuYuelamu " " Y"uelamu Hydrogeological Map (Part " 2) Nyirri"pi " " Papunya Papunya ! Mount Liebig " Mount Liebig " " " Haasts Bluff Haasts Bluff ! " Ground Elevation & Aquifer Conditions " Groundwater Salinity & Management Zones ! ! !! GAB Wells and Springs Amoonguna ! Amoonguna " GAB Spring " ! ! ! Salinity (μ S/cm) Hermannsburg Hermannsburg ! " " ! Areyonga GAB Spring Exclusion Zone Areyonga ! Well D Spring " Wallace Rockhole Santa Teresa " Wallace Rockhole Santa Teresa " " " " Extent of Saturated Aquifer ! D 1 - 500 ! D 5001 - 7000 Extent of Confined Aquifer ! D 501 - 1000 ! D 7001 - 10000 Titjikala Titjikala " " NT GAB Management Zone ! D ! Extent of Artesian Water 1001 - 1500 D 10001 - 25000 ! D ! Land Surface Elevation (m AHD) 1501 - 2000 D 25001 - 50000 Imanpa Imanpa ! " " ! ! D 2001 - 3000 ! ! 50001 - 100000 High : 1515 ! Mutitjulu Mutitjulu ! ! D " " ! 3001 - 5000 ! ! ! Finke Finke ! ! ! " !"!!! ! Northern Territory GAB Water Control District ! ! ! Low : -15 ! ! ! ! ! ! ! FNWAP Management Zone NORTHERN TERRITORY Birdsville NORTHERN TERRITORY ! ! ! Birdsville " ! ! ! " ! ! SOUTH AUSTRALIA SOUTH AUSTRALIA ! ! ! ! ! ! !!!!!!! !!!! D !! D !!! DD ! DD ! !D ! ! DD !! D !! !D !! D !! D ! D ! D ! D ! D ! !! D ! D ! D ! D ! DDDD ! Western D !! ! ! ! ! Recharge Zone ! ! ! ! ! ! D D ! ! ! ! ! ! N N ! ! A A ! L L ! ! ! ! S S ! ! N N ! ! Western Zone E -

Calendar of Events Unsafe Areas for Spectators

CALENDAR UNSAFE AREAS BUILD A EXTINGUISH OF EVENTS FOR SPECTATORS SAFE FIRE A CAMP FIRE Make sure there is a 4 x 4 metre clearing Remove slow burning logs and completely extuingish with water WHAT, WHERE & WHEN OF FINKE RACING VEHICLES CAN OVERSHOOT. Dig a hole about 90 cm in diameter and 30 cm State of Origin Screening - 6:00pm deep Shovel the boundary soil over the fire to completely cover it Wednesday 9th June - Lasseters Casino Use the soil that you have removed to make a Finke Street Party & Night Markets - 5:00pm FOR YOUR SAFETY WE INSIST YOU DON’T boundary for the fire Never leave a burning fire unattended Thursday 10th June - Todd Mall STAND/CAMP IN THE MARKED AREAS Build your fire in the hole Ensure all campfires are extinguished before Scrutineering - 4:00pm leaving the campsite Friday 11th June - Start/Finish Line Precinct Have some water nearby Prologue - 7:30am Saturday 12th June - Start/Finish Line Precinct Race Day 1 - 7:00am Under Section 74 of the Bushres Management Act Sunday 13th June - Start/Finish Line Precinct TIGHT CORNERS KEEP LEFT OR RIGHT 2016 (NT) if is an oence if a person leaves a re Race Day 2 - 7:30am unattended. Monday 14th June - Start/Finish Line Precinct No standing & camping zone No standing & camping zone Presentation Night - 6:30pm 4 Meters 90 cm 4 Meters Maximum penalty 500 penalty units or 5 years Monday 14th June - A/S Convention Centre imprisonment (1 penalty unit = $155) TIGHT CORNERS TURN AT CROSS ROAD MERCHANDISE No standing & camping zone No standing & camping zone ADMISSION FINKE -

Family News 67

Family News Edition 67 Lexi Ward from Aputula and story on pg4 © Waltja Tjutangku Palyapayi Aboriginal Corporation “ doing good work with families” Postal: PO Box 8274 Alice Springs NT 0871 Location: 3 Ghan Rd Alice Springs NT 0870 Ph: (08) 8953 4488 Fax: (08) 89534577 Website: www.waltja.org.au Waltja Chairperson 2020ngka ngarangu watjil, watjilpa, tjilura, tjiluru nganampa Waltja tjutaku. Ngurra tjutanya patirringu marrkunutjananya ngurrangka nyinanytjaku wiya tawunukutu ngalya yankutjaku. Tjananya watjanu wiya, ngaanyakuntjaku Waltja kutjupa tjutangku tjana patikutu nyinangi Waltjangku, katjangku, yuntalpanku, tjamuku nyaakuntja wiya. Ngurra purtjingka nyinapaiyi tjutanya, Kapumantaku marrkunu tjananya nyinantjaku ngurrangka Tjanaya watjil watjilpa, nyinangi wiya nganana yuntjurringnyi tawunukatu yankutjaku mangarriku, yultja mantjintjaku Waltjalu? Tjanampa yiyanangi yultja tjuta ngurra winkikutu. Tjana yunparringu ngurra winkinya mangarriku Walytjalu yiyanutjangka. Walytjalu yilta tjananya puntura alpamilaningi. Panya Sharijnlu watjanutjangka. Yanangi warrkana tjutanya ngurra tjutakutu. Youth worker, NDIS, culture anta governance tjuta warrkanarripanya Walytjaku kimiti tjutanyalatju tjungurrikula miitingingka wankangi 12 times Member tjutangku miitingingka wangkangi AGM miitingi. Panya minta kuyangkulampa yangatjunu. AGM miitingi ngaraku March-tjingka (2021-ngngka) Nganana yuntjurrinyi minmya tjutaku ngurra tjutaku. Yukarraku, Ulkumanuku, nganana yuntjurringanyi. Palyaya nyinama ngurrangka Walytja tjuta kunpurringamaya. Palya Nangala. 2020 was a hard year, a sad year for people. The remote communities were locked down and no visiting each other. No shopping in Alice Springs. Everyone was crying for warm clothes and food. Oh we were too busy at Waltja clothes and food everywhere! Sending to every community. The rest of the year we were working with Sharijn to do all the programs, help the workers to go bush. Youth work, NDIS, culture and governance work. -

PARKS and WILDLIFE COMMISSION of the NORTHERN TERRITORY Annual Report 2013-14

PARKS AND WILDLIFE COMMISSION OF THE NORTHERN TERRITORY Annual Report 2013-14 The Parks and Wildlife Commission of the Northern Territory is responsible for the management, protection and sustainable development of the Territory’s parks and reserves. The Commission provides high-quality, unique recreational, cultural, and natural experiences, which enhance tourism, create greater opportunities for recreation, protect important natural assets, and deliver economic benefits for the entire Northern Territory community. The Parks and Wildlife Commission works closely with a range of stakeholders to facilitate opportunities for development, while conserving the intrinsic natural and cultural values of the parks estate. The Commission also oversees the sustainable management of native wildlife throughout the Northern Territory. The Commission works closely with the community to ensure ongoing education and appropriate management of the Territory’s wildlife, through the administration of the permit system, effective management of pest wildlife, protection of native populations, and enforcement of illegal activities. Purpose of the Report The Parks and Wildlife Commission of the Northern Territory has achieved significant outcomes against our environmental, community and visitor goals. The report focuses on recognising our achievements against our strategic goals and outcomes, while also acknowledging regional highlights that have resulted in outcomes for conservation, management, visitor satisfaction, tourism, or community engagement. Pursuant to section 28 of the Public Sector Employment and Management Act, the report aims to inform Parliament, Territorians, and other stakeholders of: • The primary functions and responsibilities of the Commission; • Significant activities undertaken during the year highlighting specific achievements against budget outputs; and • The Commission’s fiscal management and performance. -

NT Seniors Card 2020-21 Business Discount Directory Information and Discounts for Territory Seniors

NT Seniors Card 2020-21 Business Discount Directory Information and discounts for Territory seniors www.ntseniorscard.org.au i 17% LIFETIME DISCOUNT* ON LIFE INSURANCE FOR NT SENIORS CARD MEMBERS Tourism NT/Shaana McNaught Why switch to NobleOak Life Insurance? Most awarded Australian Direct Life Insurer of 2019 Client satisfaction rating of 94.4%^ Comprehensive, fully-underwritten Life Insurance Lump sum payment if diagnosed with a terminal illness# Get an instant quote at: nobleoak.com.au/seniorscardnt Or call NobleOak for a quote: 1300 041 494 and mention ‘SENIORS CARD - NT’ to switch and save. NobleOak Life Limited ABN 85 087 648 708 AFSL No. 247302 issues the products. This information is of a general nature only and does not consider your individual objectives, financial situation or needs. Please consider the My Protection Plan Product Disclosure Statement (on website). Age limitations apply. People who seek to replace an existing Life Insurance policy should consider their circumstances including continuing the existing cover until the replacement policy is issued and cover confirmed. Online quotes are indicative only - actual premiums depend on factors such as health, age and pastimes. *Important information - savings information and discount. Considerable savings are possible - visit www.nobleoak.com.au/seniorscardnt/ for details of average savings on term life cover based on a premium comparison with life cover offered by a range of other Life Insurance companies undertaken in September 2019. Please note the premium comparison includes the 17% discount, which applies to usual term life cover premium rates. T&C apply (details on website) and the discount is on term life cover, available to Seniors Card Members (not in conjunction with a discount from any other program). -

Suggested Itinerary – Central Australia | 7 Day

SUGGESTED ITINERARY: RED CENTRE DAY 1: ALICE SPRINGS TO GLEN HELEN 7 DAY RED CENTRE 4WD Our friendly team at our Alice Springs depot will introduce you to the vehicle, its equipment and explain all the features including T a n am the 4WD controls. i T ra ck Gemtree ( to B r Trephina oom Arltunga Historical Reserve This suggested itinerary begins your adventure on the 130 West MacDonnell e) Gorge Ruby Gap National Park Nature Park Nature Park kilometre drive to Glen Helen Gorge through the stunning Western Ross River Glen Helen Alice Springs McDonnell Ranges. This natural landscape features towering Hermannsburg sandstone walls and mountain pools for a refreshing swim. The Watarrka National Park Finke Gorge National Park Rainbow Valley views are both plentiful and spectacular, including the changing Kings Conservation Reserve Canyon Uluru–Kata Tjuta colours of Mount Sonder throughout the light of the day. Mt Chambers Pillar National Park Curtin Ebenezer Historical Reserve Yulara Springs Kata Erldunda The Finke River rungs through the Gorge to the Simpson Tjuta Uluru Mt Conner Kulgera SIMPSON Desert. It is home to nine species of fish, a number of migrating DESERT waterbirds and according to the local Traditional Owners, the birthplace of their revered Rainbow Serpent. ROUTE: Alice Springs to Alice Springs loop NUMBER OF DAYS: 7 days The Glen Helen Resort offers both camping and comfortable HIGHLIGHTS: Glen Helen Gorge / Palm Valley / motel options as well as a popular restaurant. Scenic Helicopter Kings Canyon / Uluru / Kata Tjuta. rides can also be booked here. DAY 2: GLEN HELEN TO PALM VALLEY From Glen Helen drive past iconic landscapes that include Gosse Bluff, a large meteorite crater, on your way to Palm Valley within the Finke Gorge National Park. -

Chapter 9: Northern Territory Intervention and Indigenous Land

Chapter 9 187 Northern Territory intervention and Indigenous land The federal government on 21 June 2007 announced measures to tackle sexual abuse against Aboriginal children in the Northern Territory. The legislation it passed to implement the measures has significant implications for Aboriginal owned and controlled land. This chapter sets out the main provisions in that legislation that affect land. Concerns are identified. A more comprehensive analysis of the intervention in the Northern Territory and human rights is set out in my Social Justice Report 2007. In that report I provide an overview of the main human rights standards and legal obligations relevant to the government’s intervention. In this Native Title Report 2007 I focus on native title and land issues. The areas addressed are: n compulsory five-year leases; n town camps; n effects of other laws; and n rights in construction areas and infrastructure. Overview Legislation giving effect to the Australian Government’s intervention into Aboriginal communities in the Northern Territory received Royal Assent1 on 17 August 2007. The main provisions dealing with the federal government’s acquisition of rights, titles and interests in land are contained in Part 4 of the Northern Territory National Emergency Response Act 2007 (Cth) (NTNER Act). There are also provisions dealing with infrastructure in Schedule 3 (Infrastructure) of the Families, Community Services and Indigenous Affairs and Other Legislation Amendment (Northern Territory National Emergency Response and Other Measures) Act 2007 (Cth) (FCSIA(NTNER) Act). That Act amends the Aboriginal Land Rights (Northern Territory) Act 1976 (Cth) (ALRA) inserting Part IIB (Statutory rights over buildings or infrastructure). -

To Questions

Question No : 291 Question : Black Spot Funding Question Date : 29/06/93 Member : Mr BELL To : MINISTER for TRANSPORT and WORKS With reference to Black Spot Funding listed on page 42 of the 1991-92 Annual Report of the Department of Transport and Works, which projects were funded under - (a) the original Black Spot 10 Point Plan; and (b) the additional Black Spot Funding program. ANSWER The projects included under the Black Spot Program against the funding detailed in the 1991-92 Department of Transport and Works Annual Report are detailed on following pages - ORIGINAL BLACK SPOT PROGRAM 1991-92 - $1.7m 1991-92 PROGRAM PROJECT DESCRIPTION AUTHORITY LOCATION TREATMENT APPROVED COST TO PROGRAM __________________________________________________________________________ NTG Lasseter Highway Shoulder Sealing $ 100 000 Ch 221 to 224 km NTG Arnhem Highway Shoulder Sealing $ 205 000 (West Jabiru) (206 to 219 km) NTG Arnhem Highway Shoulder Sealing $ 80 000 (Jabiru East) NTG Cox Peninsula Shoulder Sealing $ 170 000 Road (0 to 9 km) NTG Roper Highway Curve Delineation $ 190 000 NTG Daly Waters Road Improved Sight $ 190 000 Distance NTG Buchanan Highway Roadside Fencing $ 145 000 (70 km) NTG Lasseter Highway Roadside Fencing $ 135 000 (40 km) NTG Carpentaria Highway Off Road Rest Areas $ 140 000 NTG - Various Northern Road Network Install Seat Belt $ 50 000 Signs Darwin CC Nightcliff Road Roundabout $ 240 000 Progress Drive Installation Katherine TC Acacia Drive Intersection $ 15 000 Martin Terrace Channelization Litchfield SC Hillier Road Street -

PDF Herunterladen

DEINE AUSTRALIENREISE IST ERST KOMPLETT, WENN DU IM WARST! OUTBACK Dein Guide für den perfekten Trip durch Australiens Northern Territory In den Sonnenuntergang segeln, Darwin Harbour Litchfield Nationalpark Australiens „Die Menschen im Northern Territory erritory nehmen sich und das Northern T Leben nicht allzu ernst – und du solltest es auch as Northern Territory du dir beim Fall schirmsprung in ist un ver gleichlich. denSonnenuntergangamUluṟu Ellery Creek Big Hole, nicht. Hier herrscht (Ayers Rock), beim rasanten Quad West MacDonnell Ranges guteStimmung,ganz Larrimah Wayside Inn DVon der unberührten Küste bis zur Schönheit des fahren auf einer Rinderfarm ohnedieAttitüdeder oder Auge in Auge mit einem Red Centre – seine wilden 5MeterKrokodilim„Käfigdes Großstadt.“ LandschaftenbietendirEr Todes“. Wenn du lieber eine Jack, Alice Springs leb nisse, die du an keinem ruhigere Kugel schiebst, mach anderenOrtderErdefin eine Kanufahrt durch uralte Fels den wirst. Hier ist das wahre schluchten oder campe unterm Outback,undhierherkom Sternenhimmel. Oder lass dir Hallo men junge Menschen aus voneinemAborigineGuidezei EWIGER der ganzen Welt, um unter gen, wie man einen Boome rang der Sonne des „ewigen wirft.AuchinDarwinundAlice Som mers“ das Abenteuer Springs lässt es sich wunderbar zu suchen. Diese Region chillen: In Cafés, Bars und Maguk, Kakadu Nationalpark Kings Canyon, Watarrka Nationalpark hält einfach alles für das Hostels lernst du das Stadtleben ErlebnisdeinesLebensbe abseits der Massen kennen. reit! Triffdieliebenswerten Bereit Locals,erlebedieüber Außerdem gibt es zahlreiche für tolle Jobmöglich keiten; und weil wältigendeNaturunddie das Northern Territory als Kultur der Ureinwohner bei neue „Regional Area“ anerkannt ist, einem Roadtrip durch das Abenteuer lässt sich dein Working Holiday Northern Territory (kurz ,NT‘) Visum pro blemlos um ein Wie wär’s mit einem weiteres Jahr verlängert.