Fourth Quarter 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CERTIFICATE of APPROVAL Morguard Corporation And

CONTENT COPY OF ORIGINAL Ministry of the Environment Ministère de l’Environnement CERTIFICATE OF APPROVAL AIR NUMBER 8189-82YTXH Issue Date: February 25, 2010 Morguard Corporation and Bramalea City Centre Equities Inc. 25 Peel Centre Dr, No. Unit 127 Brampton, Ontario L6T 3R5 Site Location: 25 Peel Centre Drive City of Brampton, Regional Municipality of Peel L6T 3R5 You have applied in accordance with Section 9 of the Environmental Protection Act for approval of: - one (1) standby diesel generator set, having a rating of 125 kilowatts, to provide power for the facility during emergency situations; all in accordance with the Application for Approval (Air & Noise) dated November 26, 2009 and signed by Ernest De Vienna, Operations Manager, Morguard Corporation and Bramalea City Centre Equities Inc., and all supporting information associated with the application including additional information provided by Virtual Engineers, dated November 26, 2009, and signed by Bhagwant Singh, P.Eng. For the purpose of this Certificate of Approval and the terms and conditions specified below, the following definitions apply: (1) "Act" means the Environmental Protection Act; (2) "Certificate" means this Certificate of Approval issued in accordance with Section 9 of the Act; (3) "Equipment" means the diesel generator set described in the Owner's application(s), this Certificate and in the supporting documentation submitted with the application(s), to the extent approved by this Certificate; (4) "Manual" means a document or a set of documents that provide written instructions to staff of the Owner; (5) "Ministry" means the Ontario Ministry of the Environment; (6) "Owner" means Morguard Corporation and Bramalea City Centre Equities Inc., and includes its successors and assignees; (7) “Publication NPC-205" means Ministry Publication NPC-205, Sound Level Limits for Stationary Sources in Class 1 & 2 Areas (Urban), October, 1995; and (8) “Publication NPC-232" means Ministry Publication NPC-232, Sound Level Limits for Stationary Sources in Class 3 Areas (Rural), October, 1995. -

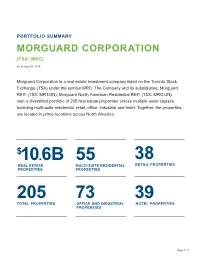

56 203 37 73 37 $10.1B

PORTFOLIO SUMMARY MORGUARD CORPORATION (TSX: MRC) As at March 31, 2021 Morguard Corporation is a real estate investment company listed on the Toronto Stock Exchange (TSX) under the symbol MRC. The Company and its subsidiaries, Morguard REIT (TSX: MRT.UN), Morguard North American Residential REIT (TSX: MRG.UN), own a diversified portfolio of 203 real estate properties across multiple asset classes including multi-suite residential, retail, office, industrial and hotel. Together, the properties are located in prime locations across North America. $10.1B 56 37 REAL ESTATE MULTI-SUITE RESIDENTIAL RETAIL PROPERTIES PROPERTIES PROPERTIES 203 73 37 TOTAL PROPERTIES OFFICE AND INDUSTRIAL HOTEL PROPERTIES PROPERTIES Page 1 / 5 MORGUARD CORPORATION PORTFOLIO SUMMARY As at March 31, 2021 MULTI-SUITE RESIDENTIAL PORTFOLIO Ownership Province/ Interest Total Ownership Property City State Ownership (%) Suites Suites CANADA Mayfair Village South Edmonton AB MRC 100 237 237 Square 104 Edmonton AB MRG 100 277 277 Margaret Place Kitchener ON MRG 100 472 472 Aspen Grove I Mississauga ON MRC 95 168 160 Aspen Grove II Mississauga ON MRC 95 168 160 Meadowvale Gardens Mississauga ON MRG 100 325 325 The Arista Mississauga ON MRG 100 458 458 The Elmwoods Mississauga ON MRG 100 321 321 The Forestwoods Mississauga ON MRG 97 300 291 The Maplewoods Mississauga ON MRG 97 300 291 The Valleywoods Mississauga ON MRG 98 373 366 Tomken Place Mississauga ON MRG 100 142 142 126 Sparks Ottawa ON MRC 100 36 36 160 Chapel Ottawa ON MRG 100 370 370 Downsview Park Townhomes Toronto ON MRG 100 60 60 Leaside Towers Toronto ON MRC 100 989 989 Rideau Towers I Toronto ON MRG 90 287 258 Rideau Towers II Toronto ON MRG 100 380 380 Rideau Towers III Toronto ON MRG 100 474 474 Rideau Towers IV Toronto ON MRG 100 400 400 Rouge Valley Residence Toronto ON MRG 100 396 396 The Bay Club Toronto ON MRC 100 293 293 The Heathview Toronto ON MRC 100 587 587 The Colonnade Toronto ON MRC 100 157 157 Condominium Suites Toronto ON MRC 100 5 5 SUBTOTAL 7,975 7,905 U.S. -

Canada-2013-Finalists.Pdf

TRADITIONAL MARKETING ADVERTISING Centres 150,000 to 400,000 sq. ft. of total retail space Identity Crisis Rescued 10 Dundas East Toronto, Ontario Management Company: Bentall Kennedy (Canada) LP Owner: 10 Dundas Street Ltd. One World in the Heart of Your Community Jane Finch Mall Toronto, Ontario Management Company: Arcturus Realty Corporation Owner: Brad-Jay Investments Limited At the Heart of the Community Les Galeries de Hull Gatineau, Quebec Management Company/Owner: Ivanhoe Cambridge Here’s to the Best Things in Life Lynden Park Mall Brantford, Ontario Management Company/Owner: Ivanhoe Cambridge Must Visit MEC Montreal Eaton Centre Montreal, Quebec Management Company/Owner: Ivanhoe Cambridge Centres 400,000 to 750,000 sq. ft. of total retail space Break Out Your Style Cornwall Centre Regina, Saskatchewan Management Company: 20 Vic Management Inc. Owner: Kingsett Capital & Ontario Pension Board The Really Runway Dufferin Mall Toronto, Ontario Management Company: Primaris Management Inc. Owner: H&R Reit Les Rivieres: Inspired by Trends Les Rivières Shopping Centre Trois-Rivières, Quebec Management Company: Ivanhoe Cambridge Owner: Ivanhoe Cambridge & Sears Canada Medicine Hat Mall Motherload Medicine Hat Mall Medicine Hat, Alberta Management Company: Primaris Management Inc. Owner: H & R Reit Crate&Barrel | OAKRIDGE · SINCE MARCH 21, 2013 Oakridge Centre Vancouver, British Columbia Management Company/Owner: Ivanhoe Cambridge Wahoo! Uptown Victoria, British Columbia Management Company: Morguard Investments Limited Owner: Greystone Centres 750,000 to 1,000,000 sq. ft. of total retail space Entrepôts de Marques - Brand Factory Marché Central Montréal, Québec Management Company: Bentall Kennedy (Canada) LP Owner: bcIMC Realty Corporation The World Of Fashion In 200 Stores Place Rosemère Rosemère, Québec Management Company: Morguard Investments Limited Owner: Rosemère Centre Properties Limited An Independent Style Southcentre Calgary, Alberta Management Company /Owner: Oxford Properties Group St. -

Morguard Corporation Annual Information Form for the Year Ended December 31, 2014

Morguard Corporation Annual Information Form For the year ended December 31, 2014 Dated March 4, 2015 MORGUARD CORPORATION ANNUAL INFORMATION FORM DATED MARCH 4, 2015 TABLE OF CONTENTS Page ITEM 1 CORPORATE STRUCTURE ......................................................................................... 3 ITEM 2 GENERAL DEVELOPMENT OF THE BUSINESS ........................................................ 4 ITEM 3 NARRATIVE DESCRIPTION OF THE BUSINESS ....................................................... 9 ITEM 4 DIVIDEND POLICY ...................................................................................................... 16 ITEM 5 DESCRIPTION OF CAPITAL STRUCTURE ............................................................... 16 ITEM 6 MARKET FOR SECURITIES ....................................................................................... 23 ITEM 7 DIRECTORS AND OFFICERS .................................................................................... 24 ITEM 8 LEGAL PROCEEDINGS AND REGULATORY ACTIONS .......................................... 25 ITEM 9 INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS ........................................................................................................ 25 ITEM 10 TRANSFER AGENT AND REGISTRAR ..................................................................... .25 ITEM 11 MATERIAL CONTRACTS ........................................................................................... 26 ITEM 12 INTERESTS OF EXPERTS ........................................................................................ -

58 176 41 68 9 $8.3B

PORTFOLIO SUMMARY MORGUARD CORPORATION (TSX: MRC) As at September 30, 2016 Morguard Corporation is a real estate investment company listed on the Toronto Stock Exchange (TSX) under the symbol MRC. The Company and its subsidiaries, Morguard REIT (TSX: MRT.UN) and Morguard North American Residential REIT (TSX: MRG.UN), own a diversified portfolio of 176 real estate properties across multiple asset classes including multi-suite residential, retail, office, industrial and hotel. Together, the properties are located in prime locations across North America. $8.3B 58 41 REAL ESTATE MULTI-SUITE RESIDENTIAL RETAIL PROPERTIES PROPERTIES PROPERTIES 176 68 9 TOTAL PROPERTIES OFFICE AND INDUSTRIAL HOTEL PROPERTIES PROPERTIES Page 1 / 5 MORGUARD CORPORATION PORTFOLIO SUMMARY As at September 30, 2016 MULTI-SUITE RESIDENTIAL PORTFOLIO Ownership Province/ Interest Total Ownership Property City State Ownership (%) Suites Suites CANADA Mayfair Village South Edmonton AB MRC 100 237 237 Square 104 Edmonton AB MRG 100 277 277 Margaret Place Kitchener ON MRG 100 472 472 Aspen Grove I Mississauga ON MRC 95 168 160 Aspen Grove II Mississauga ON MRC 95 168 160 Meadowvale Gardens Mississauga ON MRG 100 325 325 The Arista Mississauga ON MRG 100 458 458 The Elmwoods Mississauga ON MRG 100 321 321 The Forestwoods Mississauga ON MRG 89 300 267 The Maplewoods Mississauga ON MRG 87 300 261 The Valleywoods Mississauga ON MRG 91 373 339 Tomken Place Mississauga ON MRG 100 142 142 126 Sparks Ottawa ON MRC 100 36 36 160 Chapel Ottawa ON MRG 100 370 370 Leaside Towers Toronto ON MRC 100 989 989 Rideau Towers I Toronto ON MRG 90 287 258 Rideau Towers II Toronto ON MRG 100 380 380 Rideau Towers III Toronto ON MRG 100 474 474 Rideau Towers IV Toronto ON MRG 100 400 400 Rouge Valley Residence Toronto ON MRG 100 396 396 The Bay Club Toronto ON MRC 100 293 293 The Heathview Toronto ON MRC 100 587 587 The Colonnade Toronto ON MRC 100 157 157 Condominium Suites Toronto ON MRC 100 4 4 SUBTOTAL 7,914 7,763 U.S. -

Morguard Corporation

MORGUARD CORPORATION SUSTAINABILITY REPORT 2017 DETAILED RESULTS OF SUSTAINABLE MORGUARD MORGUARD 2017 SUSTAINABILITY REPORT TABLE OF CONTENTS EXECUTIVE STATEMENT ....................................................................................................................................... 1 PROFILE .................................................................................................................................................................. 2 OUR SUSTAINABILITY STRATEGY ........................................................................................................................ 4 OUR 2035 LONG-TERM OBJECTIVES ................................................................................................................... 5 OUR VOICE – ADVOCATING FOR SUSTAINABLE REAL ESTATE ....................................................................... 6 OUR STAKEHOLDERS AND MATERIALITY ........................................................................................................... 6 COMMITMENT TO EXTERNAL INITIATIVES .......................................................................................................... 8 RESPONSIBLE PROPERTY INVESTMENT – SUSTAINABILITY ADVISER TO OUR CLIENTS ........................... 9 REACHING NET ZERO – PARTNERING TO ACHIEVE SUSTAINABLE BUILDINGS .......................................... 10 GREEN BUILDING CERTIFICATIONS .................................................................................................................. 11 INNOVATION – BENCHMARKING -

Rainer Nowak Sr. Chief General Operations & Borders Issues

Rainer Nowak MEMBERS Sr. Chief Alberta Investment Management Corporation Allied Properties REIT General Operations & Borders Issues Artis REIT Aspen Properties Ltd. Finance Canada Avison Young 140 O’Connor Street Baybridge Seniors Housing Inc. Bentall Kennedy Group Ottawa, Ontario K1A 0G5 BMO Capital Markets Real Estate Inc. Boardwalk REIT Brookfield Financial Real Estate Group September 28th, 2012 Brookfield Office Properties Brookfield Real Estate Opportunity Fund Build Toronto Inc. Cadillac Fairview Corporation Ltd., The Re: GST/HST Impacts on Canadian REITs Calloway REIT Canderel CAPREIT CB Richard Ellis Limited In response to a consultation on financial institution rules, REALpac would like to CIBC World Markets Inc. Colliers International. Inc. make the following issues known to Finance: Cominar REIT CREIT (Canadian REIT) Crombie REIT Cushman & Wakefield Ltd. It was recently brought to our attention that the GST/HST charged on the costs Dorsay Development Corp. related to capital raises and corporate transactions are not permitted to be claimed as Dundee REIT EPIC Realty Partners Inc. Input Tax Credits (“ITC”) on the REITs GST return (S. 185). For many Canadian Fengate Capital Management Ltd. Fiera Properties REITs that are in substantial growth mode, raising capital, be it debt or equity, is First Capital Realty Inc. First National Financial LP integral for the REIT to achieve its mandate. However, the inability to claim the ITC Gazit America Inc. on GST/HST charged on costs related to capital growth means that REIT “all in” GE Capital Real Estate Granite Real Estate costs are more expensive than their real estate counterparts structured as a Greystone Managed Investments Inc. -

MORGUARD REAL ESTATE INVESTMENT TRUST MANAGEMENT INFORMATION CIRCULAR March 12, 2020 VOTING INFORMATION

MORGUARD REAL ESTATE INVESTMENT TRUST MANAGEMENT INFORMATION CIRCULAR March 12, 2020 VOTING INFORMATION SOLICITATION OF PROXIES This Management Information Circular (“Circular”) is furnished in connection with the solicitation of proxies by or on behalf of management of Morguard Real Estate Investment Trust (the “Trust”) for use at the annual meeting (“Meeting”) of unitholders (the “Unitholders”) of the Trust to be held on May 6, 2020 at 9:45 a.m. (local time) at Rattlesnake Point Golf Club, 5407 Regional Road 25, Milton, Ontario L9T 2X5, and at all adjournments thereof. The solicitation will be made primarily by mail but proxies may also be solicited by telephone by employees of the Trust, board of trustees of the Trust (the “Board of Trustees” or “Board”, and each member of the Board a “Trustee”) or by the Trust’s transfer agent, Computershare Trust Company of Canada, at a nominal cost. The costs of solicitation will be borne by the Trust. The information contained in this Circular is given as at March 12, 2020 unless otherwise indicated. Appointment of Proxies The persons named in the enclosed form of proxy are Trustees. Each Unitholder has the right to appoint a person other than the persons named in the enclosed form of proxy, who need not be a Unitholder, to represent the Unitholder at the Meeting. This right may be exercised by inserting the name of the person to be appointed by the Unitholder in the space provided in the form of proxy or by completing another proper form of proxy. Proxies must be deposited with the Trust, c/o Computershare Trust Company of Canada, 100 University Avenue, 8th Floor, Toronto, Ontario, M5J 2Y1, Attention: Proxy Department, so as to arrive not later than 5:00 p.m. -

Morguard Continues Its Commitment to Being Sustainable Together

RESPONSIBLE PROPERTY INVESTMENT, COMMUNITY ADVOCACY, STAKEHOLDER COLLABORATION AND INDUSTRY LEADERSHIP: MORGUARD CONTINUES ITS COMMITMENT TO BEING SUSTAINABLE TOGETHER. 2017 SUSTAINABILITY HIGHLIGHTS ON THE COVER 77 CITY CENTRE DRIVE MISSISSAUGA, ON 2017 SUSTAINABLE TOGETHER No building is an island. Every building is part of a greater whole, an extension of the people it serves and an integral part of the community where it is located. That’s the essential philosophy of Sustainable Morguard, our company-wide sustainability program that addresses environmental, social and governance issues that impact our world today. As members of the real estate industry, we believe we have an obligation to minimize our environmental impact while at the same time to make a positive contribution to our community at large. But we can’t do it alone. We’re committed to actively working with our shareholders, clients, tenants, employees and communities – all of whom are helping us to be sustainable together. ASSET INVESTMENTS ACQUISITIONS MANAGEMENT JOINT VENTURES COMMUNITIES DEVELOPMENT LEASING TENANT SERVICES SUSTAINABILITY FELLOW STAKEHOLDERS Responsibility. Advocacy. Action. These are the core principles of Sustainable Morguard, our corporate sustainability program. We believe in taking responsibility for the environment in which we all live, in advocating for sustainability in our communities and in taking action to make positive change happen. In 2017, Sustainable Morguard contributed significantly to the quality of our properties, to the lives of our tenants, and to the health of our communities. We’re very proud of our accomplishments to date. Among our successes have been meaningful reductions in the environmental impact of our properties, and major contributions by our dedicated employees to our communities and our businesses. -

58 205 41 67 39 $9.1B

PORTFOLIO SUMMARY MORGUARD CORPORATION (TSX: MRC) As at December 31, 2016 Morguard Corporation is a real estate investment company listed on the Toronto Stock Exchange (TSX) under the symbol MRC. The Company and its subsidiaries, Morguard REIT (TSX: MRT.UN), Morguard North American Residential REIT (TSX: MRG.UN), and Temple Hotels Inc. (TSX: TPH), own a diversified portfolio of 205 real estate properties across multiple asset classes including multi-suite residential, retail, office, industrial and hotel. Together, the properties are located in prime locations across North America. $9.1B 58 41 REAL ESTATE MULTI-SUITE RESIDENTIAL RETAIL PROPERTIES PROPERTIES PROPERTIES 205 67 39 TOTAL PROPERTIES OFFICE AND INDUSTRIAL HOTEL PROPERTIES PROPERTIES Page 1 / 5 MORGUARD CORPORATION PORTFOLIO SUMMARY As at December 31, 2016 MULTI-SUITE RESIDENTIAL PORTFOLIO Ownership Province/ Interest Total Ownership Property City State Ownership (%) Suites Suites CANADA Mayfair Village South Edmonton AB MRC 100 237 237 Square 104 Edmonton AB MRG 100 277 277 Margaret Place Kitchener ON MRG 100 472 472 Aspen Grove I Mississauga ON MRC 95 168 160 Aspen Grove II Mississauga ON MRC 95 168 160 Meadowvale Gardens Mississauga ON MRG 100 325 325 The Arista Mississauga ON MRG 100 458 458 The Elmwoods Mississauga ON MRG 100 321 321 The Forestwoods Mississauga ON MRG 89 300 267 The Maplewoods Mississauga ON MRG 87 300 261 The Valleywoods Mississauga ON MRG 91 373 339 Tomken Place Mississauga ON MRG 100 142 142 126 Sparks Ottawa ON MRC 100 36 36 160 Chapel Ottawa ON MRG 100 370 370 Leaside Towers Toronto ON MRC 100 989 989 Rideau Towers I Toronto ON MRG 90 287 258 Rideau Towers II Toronto ON MRG 100 380 380 Rideau Towers III Toronto ON MRG 100 474 474 Rideau Towers IV Toronto ON MRG 100 400 400 Rouge Valley Residence Toronto ON MRG 100 396 396 The Bay Club Toronto ON MRC 100 293 293 The Heathview Toronto ON MRC 100 587 587 The Colonnade Toronto ON MRC 100 157 157 Condominium Suites Toronto ON MRC 100 4 4 SUBTOTAL 7,914 7,763 U.S. -

55 207 39 74 39 $10.6B

PORTFOLIO SUMMARY MORGUARD CORPORATION (TSX: MRC) As at December 31, 2019 Morguard Corporation is a real estate investment company listed on the Toronto Stock Exchange (TSX) under the symbol MRC. The Company and its subsidiaries, Morguard REIT (TSX: MRT.UN), Morguard North American Residential REIT (TSX: MRG.UN), and Temple Hotels Inc. (TSX: TPH), own a diversified portfolio of 207 real estate properties across multiple asset classes including multi-suite residential, retail, office, industrial and hotel. Together, the properties are located in prime locations across North America. $10.6B 55 39 REAL ESTATE MULTI-SUITE RESIDENTIAL RETAIL PROPERTIES PROPERTIES PROPERTIES 207 74 39 TOTAL PROPERTIES OFFICE AND INDUSTRIAL HOTEL PROPERTIES PROPERTIES Page 1 / 5 MORGUARD CORPORATION PORTFOLIO SUMMARY As at December 31, 2019 MULTI-SUITE RESIDENTIAL PORTFOLIO Ownership Province/ Interest Total Ownership Property City State Ownership (%) Suites Suites CANADA Mayfair Village South Edmonton AB MRC 100 237 237 Square 104 Edmonton AB MRG 100 277 277 Margaret Place Kitchener ON MRG 100 472 472 Aspen Grove I Mississauga ON MRC 95 168 160 Aspen Grove II Mississauga ON MRC 95 168 160 Meadowvale Gardens Mississauga ON MRG 100 325 325 The Arista Mississauga ON MRG 100 458 458 The Elmwoods Mississauga ON MRG 100 321 321 The Forestwoods Mississauga ON MRG 97 300 291 The Maplewoods Mississauga ON MRG 97 300 291 The Valleywoods Mississauga ON MRG 98 373 366 Tomken Place Mississauga ON MRG 100 142 142 126 Sparks Ottawa ON MRC 100 36 36 160 Chapel Ottawa ON MRG 100 370 370 Downsview Park Townhomes Toronto ON MRG 100 60 60 Leaside Towers Toronto ON MRC 100 989 989 Rideau Towers I Toronto ON MRG 90 287 258 Rideau Towers II Toronto ON MRG 100 380 380 Rideau Towers III Toronto ON MRG 100 474 474 Rideau Towers IV Toronto ON MRG 100 400 400 Rouge Valley Residence Toronto ON MRG 100 396 396 The Bay Club Toronto ON MRC 100 293 293 The Heathview Toronto ON MRC 100 587 587 The Colonnade Toronto ON MRC 100 157 157 Condominium Suites Toronto ON MRC 100 4 4 SUBTOTAL 7,974 7,904 U.S. -

Morguard Corporation (Tsx: Mrc)

PORTFOLIO SUMMARY MORGUARD CORPORATION (TSX: MRC) As at June 30, 2020 Morguard Corporation is a real estate investment company listed on the Toronto Stock Exchange (TSX) under the symbol MRC. The Company and its subsidiaries, Morguard REIT (TSX: MRT.UN), Morguard North American Residential REIT (TSX: MRG.UN), own a diversified portfolio of 205 real estate properties across multiple asset classes including multi-suite residential, retail, office, industrial and hotel. Together, the properties are located in prime locations across North America. $10.6B 55 38 REAL ESTATE MULTI-SUITE RESIDENTIAL RETAIL PROPERTIES PROPERTIES PROPERTIES 205 73 39 TOTAL PROPERTIES OFFICE AND INDUSTRIAL HOTEL PROPERTIES PROPERTIES Page 1 / 5 MORGUARD CORPORATION PORTFOLIO SUMMARY As at June 30, 2020 MULTI-SUITE RESIDENTIAL PORTFOLIO Ownership Province/ Interest Total Ownership Property City State Ownership (%) Suites Suites CANADA Mayfair Village South Edmonton AB MRC 100 237 237 Square 104 Edmonton AB MRG 100 277 277 Margaret Place Kitchener ON MRG 100 472 472 Aspen Grove I Mississauga ON MRC 95 168 160 Aspen Grove II Mississauga ON MRC 95 168 160 Meadowvale Gardens Mississauga ON MRG 100 325 325 The Arista Mississauga ON MRG 100 458 458 The Elmwoods Mississauga ON MRG 100 321 321 The Forestwoods Mississauga ON MRG 97 300 291 The Maplewoods Mississauga ON MRG 97 300 291 The Valleywoods Mississauga ON MRG 98 373 366 Tomken Place Mississauga ON MRG 100 142 142 126 Sparks Ottawa ON MRC 100 36 36 160 Chapel Ottawa ON MRG 100 370 370 Downsview Park Townhomes Toronto ON MRG 100 60 60 Leaside Towers Toronto ON MRC 100 989 989 Rideau Towers I Toronto ON MRG 90 287 258 Rideau Towers II Toronto ON MRG 100 380 380 Rideau Towers III Toronto ON MRG 100 474 474 Rideau Towers IV Toronto ON MRG 100 400 400 Rouge Valley Residence Toronto ON MRG 100 396 396 The Bay Club Toronto ON MRC 100 293 293 The Heathview Toronto ON MRC 100 587 587 The Colonnade Toronto ON MRC 100 157 157 Condominium Suites Toronto ON MRC 100 5 5 SUBTOTAL 7,975 7,905 U.S.