ATM Access and Debit Disclosures

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Consumer Credit Card Agreement and Disclosure

CONSUMER CREDIT CARD AGREEMENT AND DISCLOSURE MASTERCARD This Consumer Credit Card Agreement and Disclosure together with the Account Opening Disclosure and any other Account opening documents or any subsequent documents provided to You related to this Account (hereinafter collectively referred to as “Agreement”) govern the terms and conditions of this Account. “We,” “Us,” “Our” and “Ours” and “Credit Union” refers to Pen Air Federal Credit Union with which this Agreement is made. “You,” “Your,” and “Yours” refers to each applicant and co-applicant for the Account; any person responsible for paying the Account; and anyone You authorize to use, access or service the Account. "Card" means the Mastercard® credit card and any other access devices, duplicates, renewals, or substitutions, the Credit Union issues to You. "Account" means the line of credit established by this Agreement and includes Your Card. SECURITY INTEREST You grant the Credit Union a security interest under the Uniform Commercial Code and under any common law rights the Credit Union may have in any goods You purchase. If You give the Credit Union a specific pledge of shares by signing a separate pledge of shares, Your pledged shares will secure Your Account. You may not withdraw amounts that have been specifically pledged to secure Your Account until the Credit Union agrees to release all or part of the pledged amount. You grant Us a security interest in all individual and joint share and/or deposit accounts You have with Us now and in the future to secure Your credit card Account. Shares and deposits in an IRA or any other account that would lose special tax treatment under state or federal law if given as security are not subject to the security interest You have given in Your shares and deposits. -

Credit Card Disclosure (PDF)

OPEN-END CONSUMER CREDIT AGREEMENTS AND TRUTH IN LENDING DISCLOSURES Effective July 1, 2016 FEDERALLY INSURED BY NCUA PATELCO CREDIT UNION in agreements governing specific services you have and your general OPEN-END CONSUMER CREDIT AGREEMENTS AND membership agreements with Patelco, and you must have a satisfactory TRUTH IN LENDING DISCLOSURES loan, account and membership history with Patelco. MASTERCARD® CREDIT CARDS 2. On joint accounts, each borrower can borrow up to the full amount of SECURED MASTERCARD CREDIT CARD the credit limit without the other’s consent. PERSONAL LINE OF CREDIT 3. Advances Effective: JULY 1, 2016 a. Credit Card Advances: Credit Cards will be issued as instructed on This booklet contains agreements and Truth in Lending Disclosures your application. To make a purchase or get a cash advance, you that govern your use of the following Patelco Credit Union open-end can present the Card to a participating MasterCard plan merchant, consumer credit programs: to the Credit Union, or to another financial institution, and sign Pure MasterCard Payback Rewards World MasterCard the sales or cash advance draft imprinted with your Card number. Keep sales and cash advance drafts to reconcile your monthly Pure Secured MasterCard Passage Rewards World Elite MasterCard statements. You can also make purchases by giving your Card Points Rewards World MasterCard Personal Line of Credit number to a merchant by telephone, over the internet, or by other means, in which case your only record of the transaction may In addition to this booklet, -

How to Find the Best Credit Card for You

How to find the best credit card for you Why should you shop around? Comparing offers before applying for a credit card helps you find the right card for your needs, and helps make sure you’re not paying higher fees or interest rates than you have to. Consider two credit cards: One carries an 18 percent interest rate, the other 15 percent. If you owed $3,000 on each and could only afford to pay $100 per month, it would cost more and take longer 1. Decide how you plan to pay off the higher-rate card. to use the card The table below shows examples of what it might You may plan to pay off your take to pay off a $3,000 credit card balance, paying balance every month to avoid $100 per month, at two different interest rates. interest charges. But the reality is, many credit card holders don’t. If you already have a credit card, let APR Interest Months history be your guide. If you have carried balances in the past, or think 18% = $1,015 41 you are likely to do so, consider 15% = $783 38 credit cards that have the lowest interest rates. These cards typically do not offer rewards and do not The higher-rate card would cost you an extra charge an annual fee. $232. If you pay only the minimum payment every month, it would cost you even more. If you have consistently paid off your balance every month, then you So, not shopping around could be more expensive may want to focus more on fees and than you think. -

New Credit Card Rules

WHAT YOU NEED TO KNOW: New Credit Card Rules The Federal Reserve’s new rules for credit card companies mean new credit card protections for you. Here are some key changes you should expect from your credit card company beginning on February 22, 2010. What your credit card company has to tell you When they plan to increase your rate or other fees. Your credit card company must send you a notice 45 days before they can increase your interest rate; change certain fees (such as annual fees, cash advance fees, and late fees) that ap- ply to your account; or make other signifi cant changes to the terms of your card. If your credit card company is going to make changes to the terms of your card, it must give you the option to cancel the card before certain fee increases take effect. If you take that option, however, your credit card company may close your account and increase your monthly payment, subject to certain limitations. For example, they can require you to pay the balance off in fi ve years, or they can double the percentage of your balance used to calculate your minimum payment (which will result in faster repayment than under the terms of your account). The company does not have to send you a 45-day advance notice if you have a variable interest rate tied to an index; if the index goes up, the company does not have to provide notice before your rate goes up; your introductory rate expires and reverts to the previously disclosed “go-to” rate; your rate increases because you are in a workout agreement and you haven’t made your payments as agreed. -

American Express® Credit Card Cardmember Agreement

AMERICAN EXPRESS® CREDIT CARD CARDMEMBER AGREEMENT IMPORTANT: Before you use the enclosed American Express Credit Card, please read these Terms and Conditions carefully and thoroughly. If you keep or use the American Express Credit Card, you will be deemed to have unconditionally agreed to these Terms and Conditions and they will govern your use of the American Express Credit Card. If you do not wish to accept these Terms and Conditions, please cut the American Express Credit Card in half and return the pieces to us immediately to the address mentioned on the last page of this document. 1. DEFINITIONS: In these Terms and Conditions, the following words shall have the respective meanings set out hereunder unless the context otherwise requires: “Account” means any American Express Credit Card Account maintained by us under these Terms and Conditions. “Available Credit Limit” means the credit limit allocated by American Express to Cardmember’s Account inclusive of all Supplementary Cards less previous balances less all new Charges. “Basic Credit Cardmember” means the individual in whose name the Account is maintained. “Cash Advances” means any cash advance obtained by use of a Credit Card, PIN or otherwise authorised by you for debit to the Account. “Charge” means a transaction made or Charged with the Credit Card, whether or not a Record of Charge form is signed, and also includes Cash Advances, Express Cash transactions, drafts made from the Account, Balance Transfers and fees thereon, interest, taxes as may be applicable and all other amounts you have agreed to pay us or have agreed to be liable for under these Terms and Conditions. -

Consumer's Edge

Consumer’s Edge Consumer Protection Division, Maryland Office of the Attorney General Brian E. Frosh, Maryland Attorney General Credit Card Offers: What’s the Catch? The offers fill your mailbox: pre-approved credit cards, low Since June of 2010, the Federal Reserve has stipulated that interest rates, 0% interest balance transfer offers, frequent credit card companies must limit most of their penalties to flier miles or rebates, and more. They sound good, but many $25, unless a consumer has a consistent history of violations. consumers apply for new credit cards only to find that the In addition, credit card companies cannot charge consumers low interest rate doesn’t last or that the card comes with multiple fees for violating the same late payment, and penalty unexpected fees. To protect yourself: Read the details of the fees cannot exceed the owed dollar amount. For example, if a credit card offer before you apply for the card, and make sure bill is $10, the penalty fee cannot exceed $10. you fully understand the terms being offered. Balance transfer fee. Some cards, even if they offer 0% in- Although the rules require the card companies to make terest on balance transfers, charge a fee to transfer the balance disclosures more easily understood, the details may still be from one credit card to another. For example, a 4% balance in the small print. You might be surprised at what you find. transfer fee on a $2,000 balance transfer would cost you $80. Below are some things to consider when reviewing a credit And be careful to make certain that the balance transfer plus card offer: any balance transfer fee does not cause you to exceed your Interest rates. -

Consumer Credit Card Agreement and Disclosure

CONSUMER CREDIT CARD AGREEMENT AND DISCLOSURE VISA BASIC/VISA REWARDS AND THE AGGIE CARD/SIMPLY PLATINUM/SIMPLY PLATINUM REBATE/VISA SIGNATURE This Consumer Credit Card Agreement and Disclosure together with the Account Opening Disclosure and any other Account opening documents or any subsequent documents provided to You related to this Account (hereinafter collectively referred to as “Agreement”) govern the terms and conditions of this Account. “We,” “Us,” “Our” and “Ours” and “Credit Union” refers to Goldenwest Federal Credit Union with which this Agreement is made. “You,” “Your,” and “Yours” refers to each applicant and co-applicant for the Account; any person responsible for paying the Account; and anyone You authorize to use, access or service the Account. "Card" means the Visa® credit card and any other access devices, duplicates, renewals, or substitutions, the Credit Union issues to You. "Account" means the line of credit established by this Agreement and includes Your Card. SECURITY INTEREST You grant the Credit Union a security interest under the Uniform Commercial Code and under any common law rights the Credit Union may have in any goods You purchase. If You give the Credit Union a specific pledge of shares by signing a separate pledge of shares, Your pledged shares will secure Your Account. You may not withdraw amounts that have been specifically pledged to secure Your Account until the Credit Union agrees to release all or part of the pledged amount. You grant Us a security interest in all individual and joint share and/or deposit accounts You have with Us now and in the future to secure Your credit card Account. -

Bankcard Agreement for United Cardholders G17222 1

BANKCARD AGREEMENT FOR UNITED CARDHOLDERS G17222 1. DEFINITIONS – In this Agreement, the word “Card” means a single Card or two or more Cards we have issued applicable local, state or federal law. You agree to indemnify and save the Bank harmless from any liability the Bank may pursuant to this Agreement. The words “you” and “yours” mean each applicant or person to whom we have issued a incur or damage it may suffer by reason of use of the Card for any such improper purpose. Card. The words “us,” “our,” “we” and the “Bank” mean United Bank. The word “Account” means the MasterCard 14. CURRENCY CONVERSION – The exchange rate between the transaction currency and the billing currency used for or VISA Account for which you were issued a Card or Cards and Checks imprinted with your name and Account number. processing international transactions is a rate selected by Visa and MasterCard from a range of rates available in wholesale “Authorized User” means any person whom you have given permission to use your Account. If your spouse, or anyone currency markets for the applicable central processing date, which may vary from the rate that Visa and MasterCard itself else, desires the same type of credit card to be issued in his or her name, he or she must sign a credit card application receives or the government-mandated rate in effect for the applicable central processing date, plus 2 percent. requesting the same. “Checks” mean the checks provided to you with your Account, should your Account type provide 15. USE OF ACCOUNT FOR QUASI-CASH TRANSACTIONS – The Account may be utilized for payment of certain quasi-cash for Checks. -

Mastercard® Credit Card Agreement

Amendments/Changes in Terms – We may change the terms of this Agreement at What To Do If You Think You Find A Mistake On Your Statement – If you think there is an any time unless otherwise prohibited by applicable law. We will give you notice of error on your statement, write to us at: P.O. Box 1500 any changes in accordance and as required by applicable law. The most recent Dunedin, FL 34697 credit card agreement is available on our website at www.achievacu.com. Achieva Credit Union, P.O. Box 1500 Dunedin, FL 34697 727.431.7680 | 800.593.2274 In your letter, give us the following information: Statements and Notices – Statements and notices will be mailed or emailed to you www.achievacu.com at the most recent postal address or email address you have provided to us. Notice • Your name and account number. provided to any Account owner will be considered notice to all. • The dollar amount of the suspected error. Change of Address – If your mailing address or contact information has changed, • If you think there is an error on your bill, describe what you believe is wrong and why or if the address as it appears on this billing statement is incorrect, you must notify you believe it is a mistake. us promptly by contacting us at the address or telephone number at the beginning of this Agreement or use our website at www.achievacu.com. If we note that mail You must contact us within 60 days after the error appeared on your statement. -

Questions and Answers About Obtaining and Managing Credit

C r e d i t t r a i n i n g m a n u a l Questions and answers Q& aboutA obtaining and Managing Credit A Consumer Action Publication Table of Contents 1 introduCtion 2 types of Credit 3 uses of Credit 4 Cost of Credit 5 obtaining Credit 6 Credit Cards 7 Credit reports and sCores 10 using Credit wisely 12 ConsuMer rights introduCtion Even for those who budget and live within their income, credit can be an important tool. It offers safety and convenience—there’s no need to carry large amounts of cash or worry that a personal check will not be accepted. It provides access to borrowed money in an emergency. And the wise use of credit can make it possible to get a loan for a car or home in the future. By understanding how credit works, what it costs, and how to avoid accumulating too much debt, consumers can use credit to their advantage. The “Credit Training Manual” can help answer many questions about credit. This publication is part of a module that includes a multilingual companion brochure, “Staying on Track with Credit” (available in Chinese, English, Korean, Spanish and Vietnamese); a training guide for classes and seminars; PowerPoint slides; and class activities. The brochure and other materials in this module are free for individuals, non-profits and community-based organizations. For more about these materials, visit the Consumer Action website at www.consumer-action.org or call Consumer Action at 800-999-7981. 1 types of Credit What is credit? Credit is the opportunity to borrow money to use now and then repay it over time at an agreed upon cost. -

ATM CARD AGREEMENT and DISCLOSURE Union Will Pay for Transactions That Overdraw Your Account, Days After We Hear from You and Will Correct the Error Promptly

• If, through no fault of ours, you do not have the funds in first deposit to the account (new accounts), we will tell you the results your account to make the transfer or the transfer would go of our investigation within twenty (20) business days. If we need over the credit limit on your line of credit. more time, however, we may take up to forty-five (45) calendar days • If you used the PIN, the ATM, or the card in an incorrect to investigate your complaint or question (ninety (90) calendar days manner. for POS transaction errors, new account transaction errors, or errors • If the ATM where you are making the transfer does not involving transactions initiated outside the United States.) If we decide have enough cash. to do this, we will re-credit your account within ten (10) business days • If the ATM or POS terminal was not working properly (five (5) business days for POS purchase transactions) for the amount and you knew about the problem when you started the you think is in error, so that you will have the use of the money during transaction. the time it takes us to complete our investigation. If we ask you to put • If circumstances beyond our control (such as fire, flood or your complaint or question in writing and we do not receive it within power failure) prevent the transaction. then (10) business days, we may not re-credit your account. • If the money in your account is subject to legal process or If we decide after our investigation that an error did not occur, we other claim. -

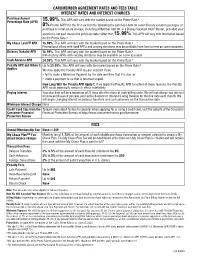

CARDMEMBER AGREEMENT RATES and FEES TABLE INTEREST RATES and INTEREST CHARGES Purchase Annual

CARDMEMBER AGREEMENT RATES AND FEES TABLE INTEREST RATES AND INTEREST CHARGES Purchase Annual . This APR will vary with the market based on the Prime Rate.a Percentage Rate (APR) 15.99% 0% Promo APRb for the first six months following the purchase date on select Disney vacation packages or purchase of a real estate interest, including a Member Add On, in a Disney Vacation Club® Resort, provided your account is not past due on the purchase date.e After that, 15.99%. This APR will vary with the market based on the Prime Rate.a My Chase LoanSM APR 15.99%. This APR will vary with the market based on the Prime Rate.a Promotional offers with fixed APRs and varying durations may be available from time to time on some accounts. Balance Transfer APR 15.99%. This APR will vary with the market based on the Prime Rate.a Introductory APRs with varying durations may be available on some accounts. Cash Advance APR 24.99%. This APR will vary with the market based on the Prime Rate.c Penalty APR and When It Up to 29.99%. This APR will vary with the market based on the Prime Rate.d Applies We may apply the Penalty APR to your account if you: • fail to make a Minimum Payment by the date and time that it is due; or • make a payment to us that is returned unpaid. How Long Will the Penalty APR Apply?: If we apply the Penalty APR for either of these reasons, the Penalty APR could potentially remain in effect indefinitely.