Medtronics / Animas

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Diabetes Close up December Supplement, 2005, No. 53 J&J To

Diabetes Close Up December supplement, 2005, No. 53 J&J To Buy Animas in Sublime Strategic Play T h e S h o r t e r V e r s i o n From the Editor: J&J’s LifeScan announced December 16 that it intends to buy Animas Corporation for $518 million in cash, or $24.50/share, a 35% premium over Animas’ closing price the 15th. We think this acquisition makes very good strategic sense – essentially, it’s the #1 glucose monitoring company buying the #2 pump player. In many respects, this was a classic J&J deal – Animas is newly profitable this year, the deal is immediately accretive, and it offers J&J an excellent leg up as it enters the pump market. Too, J&J had owned ~10% of Animas for some time. Now, while Animas is #2, it is still far behind leader Medtronic MiniMed, whose new(ish) leader, successful cardiac surgery veteran Bob Guezuraga has really impressed the diabetes community. Smart, ambitious, and seemingly hyper-focused, he appears very serious about taking the business to the next level and leaving success in diabetes as his legacy. What could be better for patients than significant focus industry-wide on better physiologic delivery? As competition heightens, we expect innovation to move faster – all good, from a patient perspective. Details on the acquisition are below – what J&J gets, what Animas gets, and what’s next. What a way to end what’s been a very dynamic year in diabetes … --Kelly L. Close DCU #53, December supplement 2005, J&J Buys Animas in Sublimely Strategic Deal. -

Caring for the World . . .One Person at a Time™ Inspires and Unites the People of Johnson & Johnson

OUR CARING TRANSFORMS 2007 Annual Report Caring for the world . .one person at a time™ inspires and unites the people of Johnson & Johnson. We embrace research and science—bringing innovative ideas, products and services to advance the health and well-being of people. Employees of the Johnson & Johnson Family of Companies work with partners in health care to touch the lives of over a billion people every day, throughout the world. The people in our more than 250 companies come to work each day inspired by their personal knowledge that their caring transforms people’s lives . one person at a time. On the following pages, we invite you to see for yourself. Our Caring Transforms ON THE COVER Johnson & Johnson is founding sponsor and continues to support Safe Kids Worldwide®. For 20 years the organization has grown, now teaching prevention as a way to save children’s lives in 17 countries around the world. In Brazil, Nayra Yara da Paz de Jesus carefully washes her hands, a safe, healthy habit she and other children are learning from a local Safe Kids® program. Find out more in our story on page 22. C H A I R M A N ’ S L E T T E R To Our Shareholders Caring for the health and well-being of people throughout the world is an extraordinary business. It is a business where people are passionate about their work, because it matters. It matters to their families, to their communities and to the world. It is a business filled with tremendous opportunity for leadership and growth in the 21st century; a business where unmet needs still abound and where people around the world WILLIAM C. -

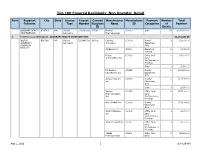

Open PDF File, 175.47 KB, for Top 100 Covered Recipients, Non Hospital

Top 100 Covered Recipients, Non Hospital, Detail Rank Recipient City State License License Covered Manufacturer Manufacturer Payment Number Total Fullname Type Number Recipient Name ID Categories of Payment ID Events QUADRANT HEALTH BEVERLY MA Clinical 22D2063293 357395 Novartis CC0243 Other 61 $2,251,831.00 STRATEGIES INC Laboratory Pharmaceuticals 1 Total for Covered Recipient : QUADRANT HEALTH STRATEGIES INC $2,251,831.00 BOSTON BOSTON MA Clinical 22D0996308 241308 Celgene CC0109 Grants/ 2 $30,000.00 UNIVERSITY Laboratory Corporation Educational SCHOOL OF Gifts MEDICINE Csl Behring Llc CC0101 Education/ 2 $5,000.00 Training Depuy CC0135 CMEs, third- 2 $26,000.00 Orthopaedics, Inc., party Conferences, or Meetings Other 1 $7,500.00 Dr. Reddy's CC0592 Grants/ 2 $121,820.00 Laboratories, Inc Educational Gifts Janssen Biotech, CC0194 Grants/ 2 $105,000.00 Inc. Educational Gifts Other 1 $1,500.00 Janssen CC0535 CMEs, third- 2 $175,000.00 Pharmaceuticals, party Inc. Conferences, or Meetings Novo Nordisk Inc. CC0006 Grants/ 2 $136,436.00 Educational Gifts Smith & Nephew, CC0402 CMEs, third- 1 $1,000.00 Inc. party Conferences, or Meetings Stryker Corporation CC0290 CMEs, third- 1 $1,000.00 party Conferences, or Meetings Takeda CC0300 CMEs, third- 2 $60,218.00 Pharmaceuticals party Aug 1, 2016 1 8:44:29 AM Top 100 Covered Recipients, Non Hospital, Detail Rank Recipient City State License License Covered Manufacturer Manufacturer Payment Number Total Fullname Type Number Recipient Name ID Categories of Payment ID Events BOSTON BOSTON MA Clinical 22D0996308 241308 America, Inc CC0300 Conferences, or UNIVERSITY Laboratory Meetings SCHOOL OF Grants/ 3 $800,000.00 MEDICINE Educational Gifts Valeant CC0346 CMEs, third- 2 $5,000.00 Pharmaceuticals party North America Conferences, or Meetings W.L. -

2016 Annual Report

ANNUAL REPORT 2016 MARCH 2017 TO OUR SHAREHOLDERS ALEX GORSKY Chairman and Chief Executive Officer I’ve worked in the health care industry for Rather, true innovations are the result of WE ARE UNITED nearly 30 years. It’s been both an honor and collaboration. And that collaboration is AND INSPIRED a privilege to work for Johnson & Johnson, driven by a diversity of ideas, individuals BY OUR CREDO, a company that touches the lives of over and disciplines – working together toward WHICH RINGS a billion people every day, around the a common goal. AS TRUE TODAY world. As I look at today’s health care AS IT DID WHEN landscape, it’s incredibly clear that the Today, more than ever, the world needs IT WAS WRITTEN pace of change has never been greater, leaders who are committed to working MORE THAN 70 or frankly, more exciting. together to help bring improved health YEARS AGO. and wellness to every person in every Today’s rapid change brings both corner of the globe. As the world’s largest opportunities and risks for any company and most broadly based health care in health care, and we are prepared company, we are uniquely positioned to help to address both. There are significant transform global health care; to shine a light challenges to overcome, but the tools, the on the most important issues we are facing; insights, the technologies, the innovations to collaborate across boundaries and – both evolutions and revolutions – all borders; to uncover scientific insights and combine to make today one of the most ideas; and to dedicate resources towards promising times for human health and for creating tomorrow’s breakthroughs. -

2012 Annual Report (Essentials)

Please visit jdrf.org/2012annualreport to view the entire Annual Report online. 2012 Annual Report (Essentials) 42 YEARS. 42 REASONS. Please visit jdrf.org/2012annualreport to view the entire Annual Report online. Table of Contents CEO Message ...........................................................3 JDRF Supporters ....................................................5 Financials ................................................................24 Leadership ..............................................................25 About JDRF JDRF is the leading global organization focused on type 1 diabetes (T1D) research. Type 1 diabetes is an autoimmune disease that strikes both children and adults. Unrelated to diet or lifestyle, T1D causes lifelong dependence on injected or pumped insulin and carries the constant danger of life-threatening complications. It requires intensive, 24/7 management. There are no days off, and there is no cure. Parents founded JDRF in 1970 to help their children with T1D by funding research to find a cure for this poorly understood and often deadly disease. Driven by passionate, grassroots volunteers connected to children, adolescents, and adults with this disease, JDRF has grown to become the largest nongovernmental funder of T1D research. JDRF has awarded more than $1.7 billion to diabetes research since our founding. Our goal is simple: we want to create a world without T1D. JDRF is the only global organization with a strategic plan to bring a continuous stream of life-changing therapies, and ultimately, a cure for T1D. 2 Please visit jdrf.org/2012annualreport to view the entire Annual Report online. CEO Message A Vision for the Future Our 2012 Annual Report is a JDRF isn’t just imagining keeping patients healthy celebration of JDRF’s 42nd this future. We’re making it and safe until our vision is year highlighting many of happen. -

UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (X) Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the quarterly period ended April 1, 2007 or ( ) Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from to Commission file number 1-3215 JOHNSON & JOHNSON (Exact name of registrant as specified in its charter) NEW JERSEY 22-1024240 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) One Johnson & Johnson Plaza New Brunswick, New Jersey 08933 (Address of principal executive offices) Registrant's telephone number, including area code (732) 524-0400 Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. (X) Yes ( )No Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act. Large accelerated filer (X) Accelerated filer ( ) Non-accelerated filer ( ) Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ( ) Yes (X) No Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date. -

Hoofdblad IE 1019 6 Maart 2019

Nummer 10/19 06 maart 2019 Nummer 10/19 2 06 maart 2019 Inleiding Introduction Hoofdblad Patent Bulletin Het Blad de Industriële Eigendom verschijnt The Patent Bulletin appears on the 3rd working op de derde werkdag van een week. Indien day of each week. If the Netherlands Patent Office Octrooicentrum Nederland op deze dag is is closed to the public on the above mentioned gesloten, wordt de verschijningsdag van het blad day, the date of issue of the Bulletin is the first verschoven naar de eerstvolgende werkdag, working day thereafter, on which the Office is waarop Octrooicentrum Nederland is geopend. Het open. Each issue of the Bulletin consists of 14 blad verschijnt alleen in elektronische vorm. Elk headings. nummer van het blad bestaat uit 14 rubrieken. Bijblad Official Journal Verschijnt vier keer per jaar (januari, april, juli, Appears four times a year (January, April, July, oktober) in elektronische vorm via www.rvo.nl/ October) in electronic form on the www.rvo.nl/ octrooien. Het Bijblad bevat officiële mededelingen octrooien. The Official Journal contains en andere wetenswaardigheden waarmee announcements and other things worth knowing Octrooicentrum Nederland en zijn klanten te for the benefit of the Netherlands Patent Office and maken hebben. its customers. Abonnementsprijzen per (kalender)jaar: Subscription rates per calendar year: Hoofdblad en Bijblad: verschijnt gratis Patent Bulletin and Official Journal: free of in elektronische vorm op de website van charge in electronic form on the website of the Octrooicentrum Nederland. -

Johnson & Johnson

JOHNSON & JOHNSON FORM 10-K (Annual Report) Filed 02/24/16 for the Period Ending 01/03/16 Address ONE JOHNSON & JOHNSON PLZ NEW BRUNSWICK, NJ 08933 Telephone 732-524-2455 CIK 0000200406 Symbol JNJ SIC Code 2834 - Pharmaceutical Preparations Industry Biotechnology & Drugs Sector Healthcare Fiscal Year 01/01 http://www.edgar-online.com © Copyright 2016, EDGAR Online, Inc. All Rights Reserved. Distribution and use of this document restricted under EDGAR Online, Inc. Terms of Use. UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended January 3, 2016 Commission file number 1-3215 JOHNSON & JOHNSON (Exact name of registrant as specified in its charter) New Jersey 22-1024240 (State of incorporation) (I.R.S. Employer Identification No.) One Johnson & Johnson Plaza New Brunswick, New Jersey 08933 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code: (732) 524-0400 SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT Title of each class Name of each exchange on which registered Common Stock, Par Value $1.00 New York Stock Exchange 4.75% Notes Due November 2019 New York Stock Exchange 5.50% Notes Due November 2024 New York Stock Exchange Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. -

Amity University

AMITY UNIVERSITY We nurture talent --------------------UTTAR PRADESH-------------------- (Established by Ritnand Balved Education Foundation) THIS IS TO CERTIFY THAT PROJECT REPORT ENTITLED “PROBLEM IDENTIFICATION AND RECTIFICATION IN CLAIM SETTLEMENT”, IN JOHNSON & JOHNSON, NEW DELHI IS PREPARED BY DEEPAK BEHAL OF MBA (GENERAL) 3rd SEMESTER, AMITY UNIVERSITY, LUCKNOW CAMPUS, UNDER MY SUPERVISION. PLACE: LUCKNOW FACULTY GUIDE: DATE: (DR. NIMISH GUPTA) STUDENT’S CERTIFICATE Certified that this report is prepared based on the summer internship project undertaken by me in Johnson & Johnson from 4th June 2007 to 16th July 2007, under the able guidance of Mr. Ajay Rangaraj, Regional Manager, sales (north) in partial fulfilment of the requirement for award of degree of Master in Business Administration From Amity University Uttar Pradesh. Date: _____________ Signature: __________ Signature: __________ Signature: __________ Name: _____________ Name: _____________ Name: _____________ Student Faculty Guide Director ABS ACKNOWLEDGEMENT The satisfaction and Euphoria that accompany the successful completion any task would be without the mention of people who make it possible and whose constant guidance and encouragement leads all effects with success. I would like to express my sincere and profound gratitude to my project guide Dr. Nimish gupta who has been a constant source of inspiration throughout my project. I thank him for the guidance given by him to complete my project. I would also like to thank my Industry guide Mr. Ajay Rangaraj who has been of great help to me and helping me whenever I needed help. Last but not the least I would like to thank Mr. Sabharwal (ABI), Mr Harish rathuri(ABI), Mr Kashif Husain(ABI), Mr Ramesh Jaswani(ABI), Mr Suresh Nandwani(FLM), and all the staff of Johnson & Johnson who helped me in successful completion of the project without them it would have been very difficult for me to complete the project successfully. -

Johnson & Johnson

9/9/13 Johnson & Johnson - Wikipedia, the free encyclopedia Johnson & Johnson Coordinates: 40°29′55″N 74°26′37″W From Wikipedia, the free encyclopedia Johnson & Johnson is a U.S multinational Johnson & Johnson medical devices, pharmaceutical and consumer packaged goods manufacturer founded in 1886. Its common stock is a component of the Dow Jones Industrial Type Public Average and the company is listed among the Fortune 500. Traded as NYSE: JNJ (http://www.nyse.com/about/listed/lcddata.html? Johnson & Johnson ranked at the top of ticker=jnj) Harris Interactive's National Corporate Dow Jones Industrial Average Component Reputation Survey for seven consecutive S&P 500 Component years up to 2005,[2] was ranked as the world's most respected company by Industry Medical equipment Barron's Magazine in 2008,[3] and was the Pharmaceutical first corporation awarded the Benjamin Founded 1886 Franklin Award for Public Diplomacy by Founder(s) Robert Wood Johnson I, the U.S. State Department in 2005 for its James Wood Johnson, funding of international education programs. Edward Mead Johnson However, in recent years the company's reputation has been adversely affected by Headquarters New Brunswick, New Jersey, United States product recalls, fines for pharmaceutical Area served Worldwide marketing practices, litigation with a group of shareholders, and other legal issues. Key people William Weldon (Chairman of the Board) Johnson & Johnson is headquartered in Alex Gorsky New Brunswick, New Jersey with the (Chief Executive Officer) consumer division being located in Products See list of Johnson & Johnson products Skillman, New Jersey. The corporation includes some 250 subsidiary companies Revenue US$ 65.030 billion (2012)[1] with operations in over 57 countries and Operating US$ 12.361 billion (2012)[1] products sold in over 175 countries. -

Student Opportunities

A Legacy of Caring Student Opportunities Throughout the Johnson & Johnson Family of Companies, we aim to make the world a better and healthier place through everything we do—the products we discover and develop, the positions we take on public policy issues, the way we run our business every day, and the programs and alliances we build and join. We see corporate citizenship, or sustainability, as intrinsic to all of Harnessing the sun’s power our activities, aligned with the spirit of caring that The Titusville campus of the emanates from Our Credo. Janssen Pharmaceutical Companies of Johnson & Johnson Sustainable business practices include quality and has the largest solar panel arrays safety, environmental protection and conservation in New Jersey. It is expected to Next Steps… of natural resources, improving access to health provide 70 percent of the site’s Would you like to be vital and make your care, ethical business practices, conducting annual electricity needs. mark within the Johnson & Johnson responsible research, and other areas. Through Family of Companies? our corporate giving, we work with partners on over 700 community-based programs that improve For more information and to apply for specific health and well-being in more than 50 countries. positions, please visit careers.jnj.com. In the last decade, Johnson & Johnson and its To use the “Search Jobs” function, first make operating companies have provided more than appropriate selections on the dropdown $4.3 billion in grants, product donations, and lists, then follow directions to view posted patient assistance. positions. Please apply only to positions in the country or countries where you are Green/Sustainability/Corporate Citizenship permanently authorized to work. -

2013 AB 128 Code of Conduct Compliant Companies

Manufacturers and Wholesalers Street City ST Zip 1109 Spring Holdings, LLC 1109 Spring Managing Member, LLC Abbott Diabetes Care Division Abbott Diagnostic Division Abbott Laboratories 100 Abbott Park Road Abbott Park IL 60064 Abbott Medical Optics Abbott Molecular Division Abbott Nutrition Products Division Abbott Point of Care Division Abbott Vascular Division AbbVie, Inc. 1 N. Waukegan Road North Chicago IL 60064 Abraxis Bioscience, LLC. 11755 Wilshire Blvd., Suite 2000 Los Angeles CA 90025 Access Closure, Inc. 645 Clyde Ave. Mountain View CA 94043 Acclarent, Inc. 1525-B O'Brien Dr. Menlo Park CA 94025 Accuri Cyometers, Inc. Ace Surgical Supply, Inc. 1034 Pearl St. Brockton MA 02301 Acorda Therapeutics, Inc. 15 Skyline Drive Hawthorne NY 10532 Actelion Pharmaceuticals US, Inc. 5000 Shoreline Court, Suite 200 S. San Francisco CA 94080 Actient Pharmaceuticals, LLC 150 S. Sanders Rd. #120 Lake Forest IL 60045 AcuteCare, Inc. Advanced Orthopeadic Solutions, Inc. 336 Beech Ave., unit B6 Torrence CA 90501 Advanced Respiratory, Inc. Advanced Sterilization Products 33 Technology Drive Irvine CA 92618 Aegerion Pharmaceuticals, Inc. 101 Main Street, Suite 1850 Cambridge MA 02142 Aesculap Implant Systems, Inc. 3773 Corporate Parkway Center Valley PA 18034 Aesculap, Inc. 3773 Corporate Parkway Center Valley PA 18034 Afaxys, Inc. PO Box 20158 Charleston SC 29413 AGN Seabreeze, LLC Akrimax Pharmaceuticals, LLC 11 Commerce Drive, 1st Floor Cranford NJ 07016 Alaven Pharmaceuticals, LLC 2260 Northwest parkway Suite A Marietta GA 30067 Alcon Laboratories, Inc. 6201 South Freeway Fort Worth TX 76134 Alexion Pharmaceuticals, Inc. 352 Knotter Drive Cheshire CT 06410 Alkermes, Inc. 852 Winter Street Waltham MA 02451 Allen Medical Systems, Inc.